Sample Category Title

Forex Traders Focus on Trump’s Tariff News

As April 2 approaches—the date when Trump's international trade tariffs are set to take effect—traders are increasingly concentrating on this highly uncertain issue.

Yesterday, the U.S. president stated that:

→ Tariffs on cars would be introduced "soon" (but not all possible tariffs would be imposed);

→ Some countries might receive exemptions;

→ Nations purchasing oil from Venezuela could face 25% tariffs.

Following these remarks:

→ Oil prices rose;

→ U.S. stocks gained as Wall Street (according to Reuters) interpreted the comments as a sign of flexibility in trade negotiations.

Given this backdrop, the EUR/CAD chart is particularly interesting, as both Europe and Canada frequently feature in news related to the White House's trade policies.

EUR/CAD Exchange Rate Today

As seen on the EUR/CAD chart, the pair has slightly declined at the start of the week, dipping towards 1.54450. However, market volatility remains high:

→ The pair has gained approximately 2.85% since early March;

→ The decline from March’s peak is around 2.6%.

Technical Analysis of EUR/CAD

The pair’s volatile price swings have formed a trend channel (marked in blue).

Notably, the 1.57750 level has shifted from support to resistance, signalling bearish dominance. This is further reflected in the price movement within the red channel. If bears maintain control, EUR/CAD may drop towards a support zone, which includes:

→ The median of the blue channel;

→ The 1.54000 support level, drawn from early March’s local low.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Navigating the US Dollar (DXY): Tariffs, Data, and Technicals

- The US Dollar Index (DXY) rose to a three-week high due to positive US business activity data and improved sentiment.

- US Services PMI showed growth, driving the overall positive economic data.

- Market focus shifts to Friday's PCE data and developments around the proposed tariffs due on April 2nd.

The US Dollar Index (DXY) rose to a three-week high earlier in the US session. The Dollar stretched its gains into a fourth consecutive day thanks to an uptick in US Business activity and tariff chatter.

The tariff chatter came in the form of a report that President Trump will be flexible with his upcoming ‘universal tariff’ proposal. It appears as though markets are now expecting tariffs to be less severe on April 2nd.

Risk sentiment as a whole improved on the news with risk assets across the board benefitting.

US DATA Surprises

S&P Global's flash U.S. Composite PMI Output Index, which measures activity in manufacturing and services, rose to 53.5 in March from 51.6 in February, signaling growth in the private sector (anything above 50 shows expansion).

S&P Global Services PMI

Source: LSEG

The increase was driven by the services sector, helped by warmer spring weather. Meanwhile, manufacturing slipped back into contraction after two months of growth.

The fact that the services sector was a driving force is key as the US is primarily a service driven economy, something the Trump administration is looking to change. Whether or not it is achieved will be interesting to observe at the least.

Looking Ahead

Looking ahead to the rest of the week, attention will shift to Friday's PCE data release.

I however expect markets and the Dollar will largely be taking their cues from developments, reports and any chatter around the proposed tariffs due on April 2nd. If markets perceive the comments as a sign that severe tariffs are on the way, risk sentiment could take a hit and so could the US Dollar.

Technical Analysis - US Dollar Index

From a technical standpoint, the US Dollar Index (DXY) closed above a key resistance level on Friday.

This set the stage for a move higher to start the week with a clear run ahead toward the 105.00 handle. However, market sentiment has been shifting pretty quickly of late and I would not rule out a retest of immediate support at the 104.00 handle.

If the DXY is able to reach the 105.00 handle which houses the 200 day MA, a break above this level will bring the 105.63 handle into focus.

Meanwhile, on the downside a break of 104.00 support may bring the 103.65 handle into focus.

The RSI period-14 may prove useful as well. Monitor its behavior as it approaches the neutral 50 level with a break above a good sign that momentum may potentially have shifted. A rejection may mean a retest of recent lows.

US Dollar Index Chart, March 24, 2025

Source: TradingView (click to enlarge)

Support

- 104.00

- 103.65

- 103.17

Resistance

- 105.00 (200-day MA)

- 105.63

- 106.13

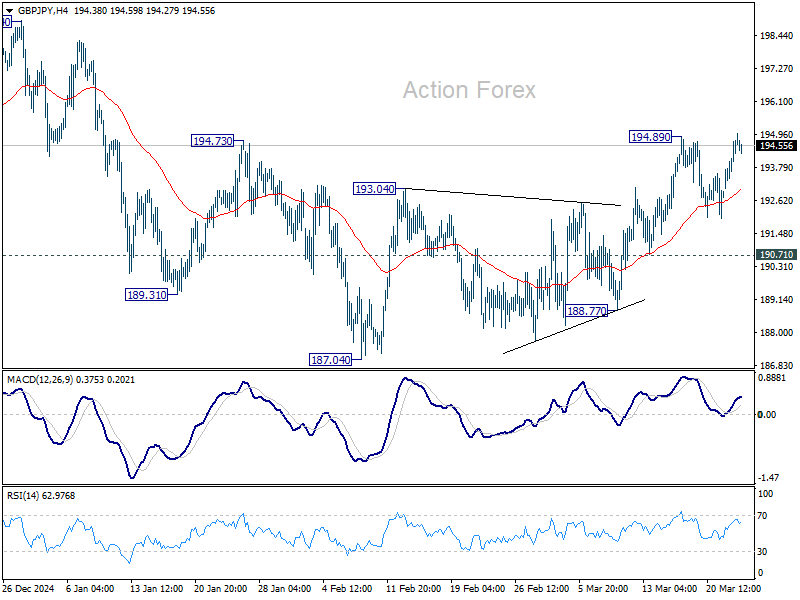

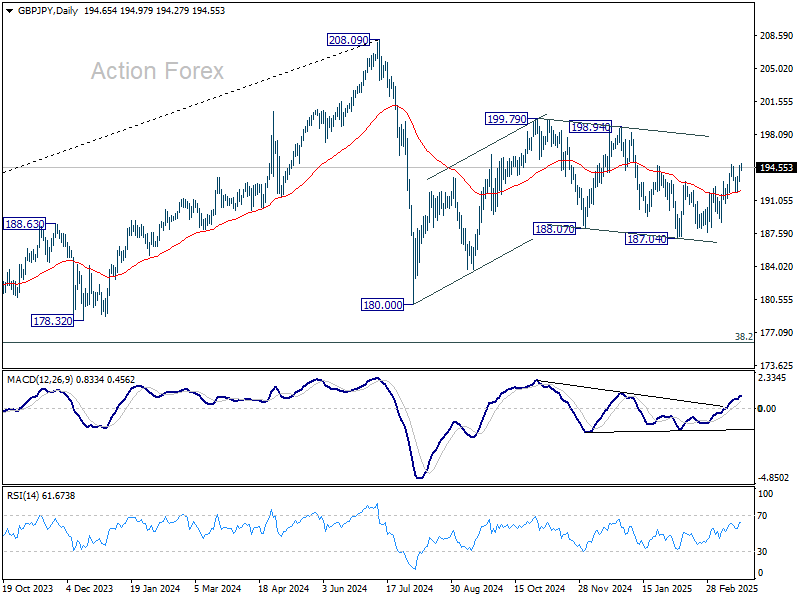

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.26; (P) 194.02; (R1) 195.51; More...

Intraday bias in GBP/JPY stays neutral at this point. On the upside, above 194.89 will resume the rebound from 187.04 towards 198.94 resistance. On the downside, break of 190.71 will bring deeper fall back to 187.04 support. Overall, corrective pattern from 180.00 is still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

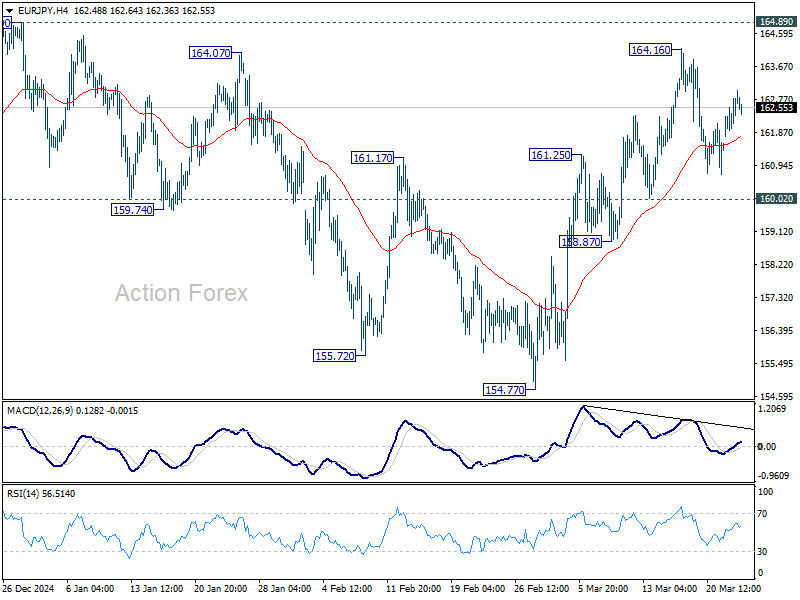

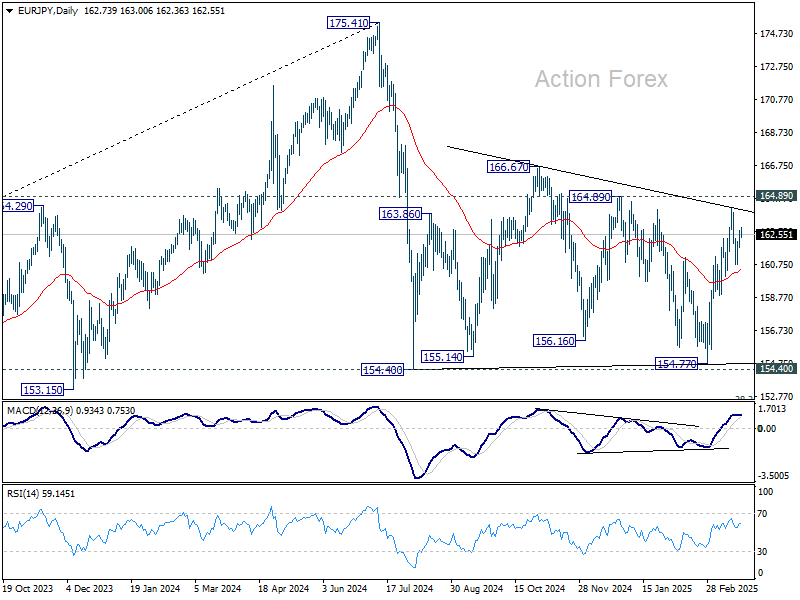

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.93; (P) 162.37; (R1) 163.22; More...

EUR/JPY is extending consolidation below 164.16 and intraday bias stays neutral. Further rally remains in favor as long as 160.02 support holds. Above 164.16 will target 164.89 and then 166.67. On the downside, however, break of 160.02 will argue that rise from 154.77 has completed and turn bias to the downside. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

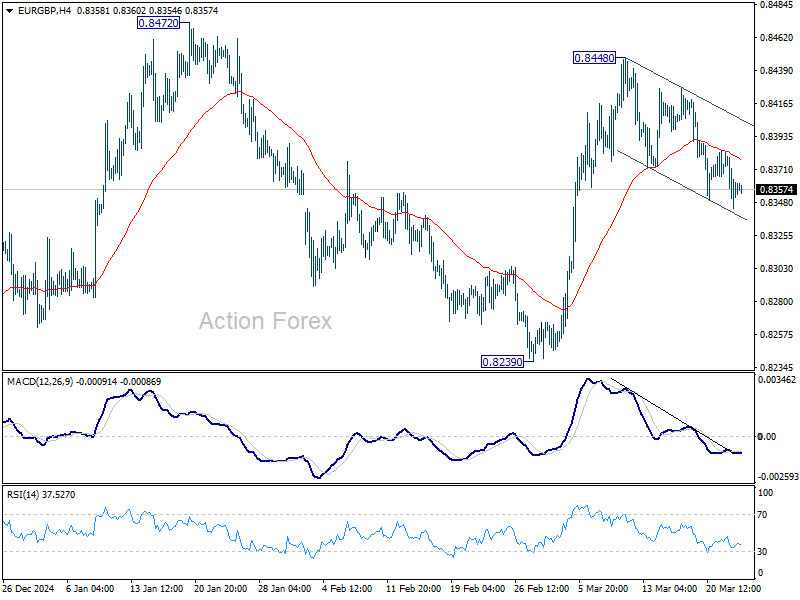

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8339; (P) 0.8365; (R1) 0.8384; More...

Intraday bias in EUR/GPB remains neutral first. On the downside, sustained break of 55 D EMA (now at 0.8347) will suggest that rise from 0.8239 has completed and turn bias back to the downside for 0.8239. On the upside. break of 0.8488 will resume the rise from 0.8239 through 0.8472 resistance to medium term falling channel resistance (now at 0.8495).

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

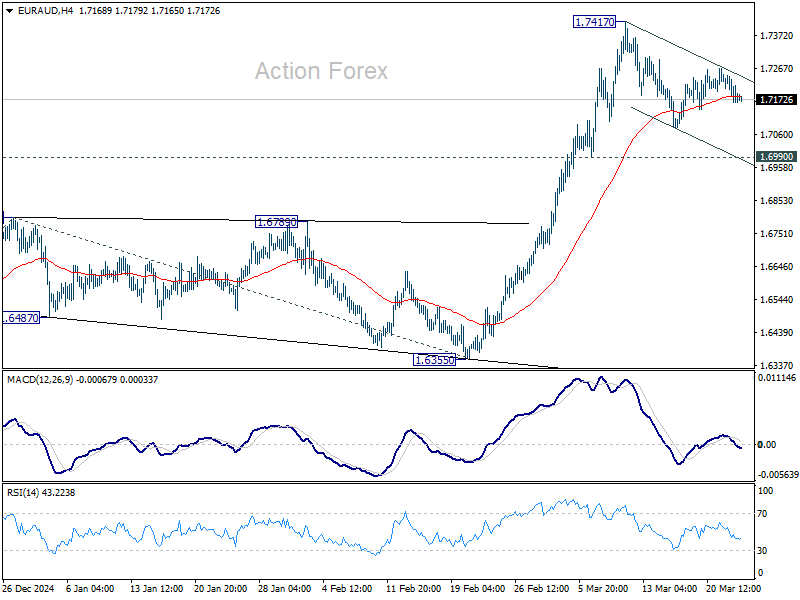

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7146; (P) 1.7202; (R1) 1.7240; More...

EUR/AUD's consolidation from 1.7417 is still extending and intraday bias remains neutral. Downside of retreat should be contained by 0.6990 support to bring rebound. On the upside, break of 1.7417 will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

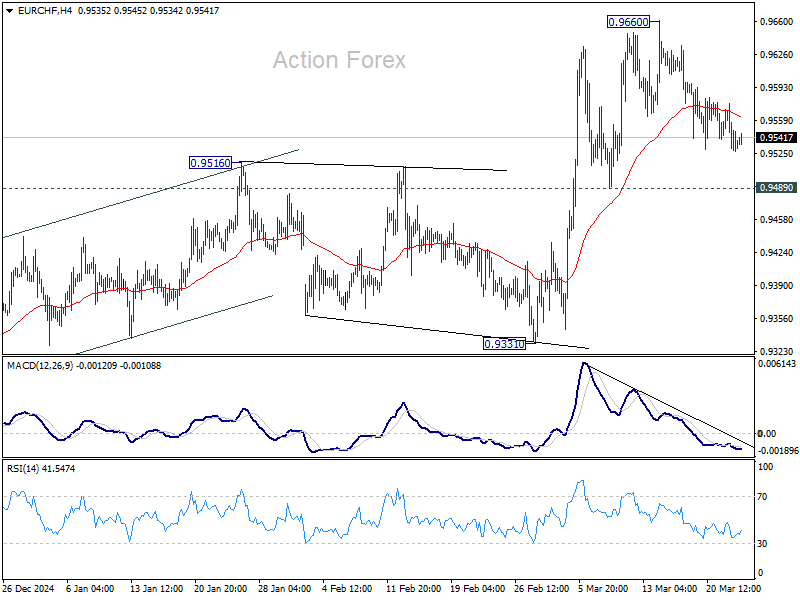

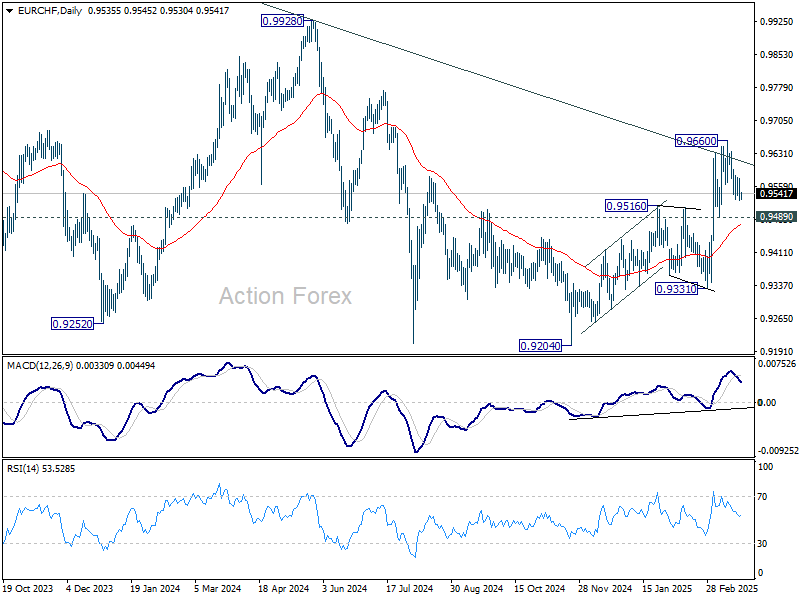

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9518; (P) 0.9548; (R1) 0.9567; More....

No change in EUR/CHF's outlook as consolidations continue below 0.9660. Intraday bias remains neutral for the moment. Further rally is expected as long as 0.9489 support holds. Break of 0.9660 will resume whole rise from 0.9204.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9487) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9618) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be seen to 0.9928 key resistance at least.

Look Out Whether Recent USD Bottoming Has Further Legs

Markets

US markets yesterday enjoyed an eye-catching ‘risk-on rebound' with higher equities, higher yields and a stronger dollar. Europe this time lagged the move in the US. Headlines of US administration potentially turning to a more targeted/selective approach when introducing reciprocal tariffs on April 2 was said to ease worries on US growth. Even so, there is still a lot of noise on the US tariffs strategy as the US president indicated that tariffs on specific sectors like autos might be announced soon. Whatever, yesterday’s US reflation trade accelerated after a stronger than expected US March PMI. The composite index jumping from 51.6 to 53.5 gave some comfort against recent stagflation fears. Yet, details were mixed. The rebound was solely driven by services (54.3 from 51.0). Activity in the manufacturing sector dropped back in contraction territory as front-running of tariffs faded. Business also turned increasingly cautious on the economic out outlook. Costs rises both related to tariffs, but also to wage growth are accelerating sharply. Whatever the news flow, US markets yesterday saw the glass half full. US equities rebounded up to 2.27% (Nasdaq). US yields jumped between 9.2 bps (5-y) and 7.4 bps (30-y) across the curve. Joining Powell’s debate on the temporary inflationary impact of tariffs, Fed’s Bostic indicated that he sees only room for one rate cut this year as tariffs might slow the disinflation process. As indicated, European markets were not able to follow the US risk-on. EMU equities failed to maintain earlier gains, even as a more moderate approach on tariffs (if it were to occur) also should be good news for export-oriented Europe (Eurostoxx 50 -0.15%). The EMU PMI’s also didn’t convince investors. The headline composite index improved only marginally from 50.2 tot 50.4. The outlook improved, but investors apparently had hoped for a more outspoken reaction already to the fiscal U-turn. EMU yields basically closed unchanged at the end of the day. Also UK yields hardly reacted to a stronger than expected UK PMI (52.0 from 50.2). The upcoming budget update and several key data probably prevented an more pronounced reaction. On FX markets, the dollar extended the tentative bottoming/rebound that developed last week (DXY close 104.25). EUR/USD struggles not to fall below the 1.08 barrier. Sterling managed to limited the damage against the dollar and further rebounded against a soft euro (close EUR/GBP 0.836).

This morning, Asian markets are trading mixed and don’t really extend yesterday’s WS risk rally. Markets might keep more of a cautious wait-and-see approach with the end of the quarter and the April 2 tariffs deadline coming ever closer. Data releases today include the German IFO business climate, the Philly Fed non-manufacturing activity index and US consumer confidence (conference board). Especially for the latter, more signs pointing to a stagflationary mindset might complicate a continuation of yesterday’s US reflation move. We also look out whether recent USD bottoming has further legs. DXY 104.4 marks first minor resistance. A sustained break below EUR/USD 1.08 also might indicated some further EUR/USD retracement with next support at 1.0763 (23% Retracement Feb low March top). The previous range top stands at 1.063.

News & Views

Iwona Duda of the Polish Monetary Policy Council said that rates are set to stay on hold in the coming months but flagged the July inflation projections as being key for potential rate cuts afterwards. Her comments came after a series of weaker than expected data, including yesterday’s retail sales, prompted several other members to raise the possibility of cuts around mid-2025. But Duda said that “Only the July projection can provide arguments decisive for the prospects of interest rate cuts, both in terms of timing and scale.” Any reduction should happen cautiously and be small (i.e. 25 bps), she added. Duda warned that some elements in core inflation prove sticky and is worried about the impact of energy prices once government caps are phased out. She also noted a continued lax fiscal policy and a strong job market. PLN strengthened throughout the day yesterday with EUR/PLN moving towards 4.175.

The Turkish finance Simsek and central bank governor Karahan are scheduled to meet with foreign investors later today. They’ll try to sooth market concerns in the wake of president Erdogan’s key opposition figure Imamoglu. That triggered a massive sell-off in Turkish assets that required government intervention to bring it to a halt. Measures included an emergency rate hike to 46%, FX interventions and a ban for shorting Turkish stocks. Additional moves are being considered, with news of a potential lower tax on Turkish lira deposits floated yesterday. It is hoped this will support the currency and dissuade locals from converting their savings into dollars or other FX. USD/TRY shot up to a record high above 41 shortly after Imamoglu’s arrest before paring gains to around 38. EUR/TRY trades around 41 compared to the 43 levels seen at the volatility peak.

Too Early to Call the End of the US Selloff

The week started on quite a positive note on hope that the next wave of US tariffs – expected to hit the ground on April 2nd - would be more targeted and more measured than previously thought. But Trump still threatened to impose 25% levies on countries that buy oil from Venezuela.

Chinese equities are under pressure this morning as the country buys oil from Venezuela and is concerned by the new tariff threats from the White House. And the barrel of US crude gained around 1.30%, though offers weighed heavier into the $69.5pb mark. Trend and momentum indicators are growing stronger, hinting that a rise above the $70pb is increasingly possible in the short run. But the long-term demand and supply dynamics remain in favour of cheaper oil – an expectation that’s already priced in, but could still prevent oil bulls from gaining too much traction after a potential break of the $70pb resistance.

Risk-on?

In the US, the low-risk assets including gold and treasuries sold off on Monday while equities gained. The S&P500 jumped 1.76%, cleared the 200-DMA resistance and closed the session above this level, Nasdaq 100 rallied more than 2% and one of the most severely hammered stocks of late, Tesla, rebounded almost 12% despite the news that its biggest rival BYD earned more than $107bn in 2024, more than Tesla ($97.7bn). BYD’s profit jumped 34% to around $5.6bn but remained short of Tesla’s $7.1bn. That’s perhaps why BYD investors preferred taking profit on the back of good and better-than-expected results, along with the fear of more tariffs on Chinese goods. But given the tariff story is hard to price in, the price pullbacks for a company like BYD are certainly interesting opportunities to strengthen long positions. As per Tesla, the latest numbers continue to look bad: the company’s European sales fell by 40% in February...

Elsewhere, the US small and medium cap indices gained more than 2% while the European indices were under pressure with the Stoxx600 retreating 0.13%.

Overall, Monday saw a correction of the rotation trade that hit the US equities and boosted the European and Chinese equivalents so far this year. Whether it’s the beginning of the end of the rotation, or just a correction is yet to be seen. The fact that the Federal Reserve (Fed) showed support despite the tariff-led inflation worries, and the fact that the European and Chinese stimulus news have already been priced in increase the need for new ingredients to keep the rotation on track. Note that the S&P500 tipped a toe into the correction zone by posting a 10% selloff from an ATH level earlier this month but avoided a further fall into that pit. Equity strategists at JPM, Morgan Stanley and Evercore ISI now think that the worst of the US market downturn is already over. Yet April 2nd will be the next important test for the global markets depending on the announcement of reciprocal tariffs - which will probably upset more than one. US and European futures are all slightly in the negative at the time of writing.

In the FX

The dollar index benefits from a broad-based rebound on relief – or fatigue – from the tariff talk. The EURUSD shortly retreated below the 1.08 mark yesterday despite a set of stronger-than-expected manufacturing PMI numbers from France and Germany thanks to the expectation of massive infrastructure and security spending, while services PMI came in lower than expected. But if we compare the two, manufacturing has a higher multiplier than the service-led spending, hence the latest PMI numbers are encouraging.

Across the Channel, the numbers tell a different story. The contraction in the manufacturing activity accelerated while services expanded faster. British inflation and the spring budget announcement will be the biggest drivers of sterling later this week, and there is a chance that we see sterling softer by the end of the week than otherwise provided that Rachel Reeves has no choice but to cut her spending plans. The latter would be negative for UK growth expectations and sterling if the Bank of England (BoE) doesn’t step in to compensate. And the BoE is not in a hurry to give support when global and trade uncertainties loom. In other words, the 1.30 resistance could be hard to clear for Cable, unless the US dollar experiences another selloff.

Focus on US Consumer Confidence

In focus today

In the US, the Conference Board's consumer confidence survey for March will be released. Earlier, a similar preliminary survey from the University of Michigan showed a clear weakening in consumer confidence due to political uncertainty. NY Fed's Williams will give remarks in the afternoon.

In Germany, we will receive the IFO growth indicator. It will be interesting to see if the release mirrors the positive surprise in the manufacturing PMI or the downtick in services counterpart.

In Sweden, February PPI data will be released this morning. Focus will be on the subcomponent that has the closest correspondence to CPI, the so-called domestic supply prices (mix of import and home market prices) for consumer goods.

In Hungary, the central bank will announce its policy rate. We and consensus expect the bank to keep the rate unchanged at 6.50%.

In China, PBoC will set the policy rate, the 1-year Medium-Term Lending Facility rate. We expect it to be unchanged again as we believe the central bank will continue to be sidelined for now until we move closer to another Fed cut.

Economic and market news

What happened yesterday

In the euro area, PMIs came in slightly weaker than expected in March, with the composite PMI rising to 50.4 (cons: 50.7) from 50.2. The rise was driven by a stronger-than-expected uptick in the manufacturing sector to 48.7 (cons: 48.2), while the service sector disappointed with a decline to 50.4 (cons: 51.1, prior: 50.6). The composite PMI signals that the euro area economy has had a positive start to 2025 and likely grew around 0.2% q/q. For the ECB's rate decision in April, the PMI data does not clearly point in either direction, with market pricing staying unchanged.

In the US, March Flash PMIs came in at 49.8, down from 52.7 in February. This indicates a contrasting trend compared to the euro area. In line with the weaker signals from the regional Fed indices, the manufacturing PMI has plunged back to contractionary territory amid tariff uncertainty - reflected by input prices rising sharply and production, domestic orders and employment weakening. However, the services index rebounded strongly to 54.3 (from 51.0), moving higher across the board, spurring the uptick in the composite index. Overall, the signals are rather mixed, yet it is positive that tariff uncertainty has not yet affected broader services activity, despite the pessimistic consumer sentiment surveys. Following the release, EUR/USD ticked lower. President Donald Trump announced Monday that auto tariffs are on the horizon but suggested that not all planned duties will take effect on 2 April, with some nations potentially receiving exemptions. Hence, significant uncertainty remains regarding Trumps tariffs.

In the UK, preliminary PMIs for March exceeded expectations, leading to a drop in EUR/GBP upon release. The composite index rose to 52.0 (cons: 50.5), driven by a rise in services to 53.2 (cons: 51.0) with more pronounced weakness in manufacturing at 44.6 (cons: 47.2). Despite a weak February print, employment indicators are showing improvement although from a low level and should be read with caution given the impending rise in employers' national insurance contribution from April. Price pressures are easing in the service sector, while manufacturing is more of a mixed bag. Overall, the release was positive news for the BoE, supporting a gradual quarterly cutting cycle.

In geopolitics, following Sunday's discussions in Saudi Arabia, US and Russian officials engaged in further talks on Monday, aiming to establish a Black Sea maritime ceasefire before negotiating a broader ceasefire in Ukraine. Despite US optimism, ongoing strikes by Russia and Ukraine underscore the fragile nature of the proposed 30-day ceasefire, while European powers remain sceptical about Putin's willingness to make real concessions. Today delegators from the US and Ukraine are scheduled to meet in Saudi Arabia.

Equities: Tariff relief made US stocks rally yesterday, with S&P 500 1.8%, Nasdaq 2.3% and small cap Russell 2000 2.6%. Investors bought the dip with Mag 7 leading the market, with this being the best day for the group since January and especially Tesla the standout up 12%. Meanwhile, European equities were unchanged although rosy PMIs would have suggested otherwise. However, underneath risk-on was evident here as well with cyclical sectors (especially banks and materials) outperforming defensives. Optimism is fading this morning though with Asian equities wavering and US and European stock futures pointing lower.

FI&FX: US equities rallied and S&P500 closed back above the 200dma on potential tariff de-escalation. US yields tracked higher under minor flattening and also European yields rose across the curve, with a minor spread tightening to peripherals. EUR/USD is hovering around 1.08 after yesterday's mixed bag of PMI's, and the positive risk sentiment weighed on the Yen. Canada's PM Carney has called for a snap election April 28, but as this was heavily expected the reaction in CAD has been muted. The NOK found support in rising oil prices, with EUR/NOK trading below 11.40. Neighbouring SEK had a strong finish to yesterday's session, breaking through 10.90 and currently trading at its lowest level since late-2022.