Sample Category Title

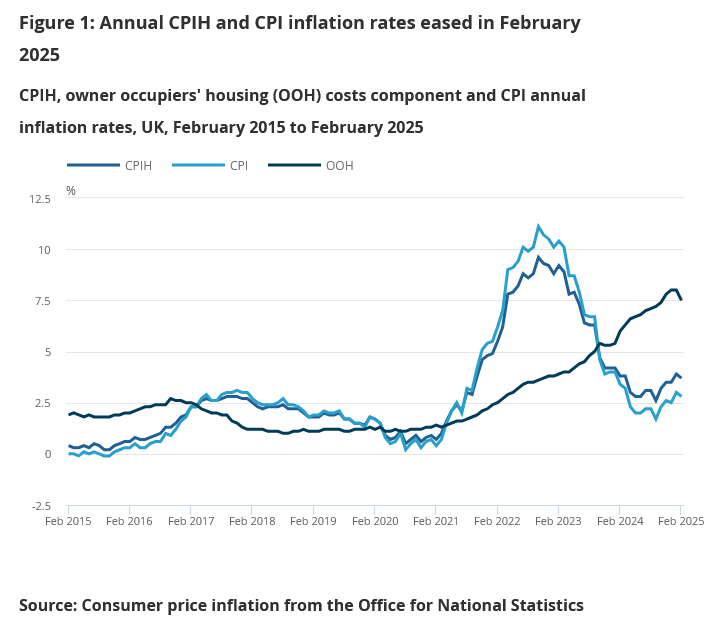

UK CPI slows to 2.8% in Feb, core down to 3.5%

UK CPI slowed from 3.0% yoy to 2.8% yoy in February, below expectation of 2.9% yoy. CPI Core (excluding energy, food, alcohol and tobacco) fell from 3.7% yoy to 3.5% yoy, below expectation of 3.6% yoy.

CPI goods annual rate slowed from 1.0% to 0.8%, while the CPI services annual rate was unchanged at 5.0%.

On a monthly basis, CPI rose by 0.4% mom.

US Strikes Ukraine-Russia Ceasefire

In focus today

In the US, February durable goods orders will be released. In the evening, the Fed's Musalem will be on the wires.

In the UK, the day is packed with action. We get inflation data for February, where focus is on the momentum in core services, which continues to prove remarkably sticky. In the afternoon, Chancellor Reeves will present the Spring Statement, where the Labour government faces some tough choices in meeting its fiscal objective while aiming to improve the UK economy's growth prospects. Previously, such fiscal announcements have proved important for UK markets, with substantial spillover particularly affecting global rates markets.

In Sweden, two key releases are in focus. The latest Economic Tendency Survey from NIER will be published. Our primary focus will be on the price plans within the retail and service sectors, as they will be crucial for the near-term inflation development. Additionally, we will observe whether the recent dip in consumer confidence persists, as this could further relay the consumption-led economic recovery. The minutes from last week's Riksbank meeting are also set to be released. We are particularly interested in the individual board members assessment of the balance of risks between recent high inflation prints and the real economy, and whether the general sentiment supports the latest money-market repricing.

In China, we still await the PBoC policy rate decision, the 1-year Medium-Term Lending Facility rate. We expect it to be unchanged again as we believe the central bank will continue to be sidelined for now until we move closer to another Fed cut.

Economic and market news

What happened overnight

In the US, while Chicago Fed President Goolsbee (dove and voter) stressed that he expects interest rates to be a "fair bit lower" in 12-18 months, he emphasized that it may take longer than expected to reach these levels amid economic uncertainty, favouring a "wait and see"- when facing uncertainty.

In commodity space, oil prices neared a three-week high around USD73.20/bbl in early trading amid supply concerns related to the US' efforts to curb Venezuelan oil exports and a larger-than-expected drop in US crude inventories. The U.S. imposed new sanctions on Venezuelan oil, with Trump authorizing 25% tariffs on imports from any buyer. This stalled Venezuelan oil trade with China as refiners awaited guidance.

What happened yesterday

In Germany, the IFO index rose as expected in March, mirroring the movement seen in yesterday's PMIs. Both the current situation assessment and expectations indices increased, indicating a stabilisation of German activity. While this suggests the decline may be ending, a rebound has yet to be observed. We expect a slow rise in German activity during 2025, supported by lower policy rates and rising real incomes, as evident in the expectations component reaching a five-month high. The rising expectations in March were primarily driven by the manufacturing sector. We expect that the effect from the fiscal package passed last week is likely some years ahead of us, as planning and implementing large infrastructure projects requires time.

In the US, the March Consumer Confidence Index fell short of expectations at 92.9 (cons: 94.0), according to the Conference Board. While economic expectations have reached their lowest since 2013 and inflation expectations tick higher, like the Michigan survey, perceptions of labour market conditions (the Jobs Plentiful index) remain unchanged. Household intentions for major purchases are also unchanged, with an increase in respondents planning vacations, indicating that while concerns exist, they may not be significant enough to alter consumer behaviour.

In Sweden, the February PPI figures came in lower than expected at -0.1% m/m (prior: 1.7%). Looking at the details, there is some relief in for example food prices which seem to be levelling out, at least from the producer side. Since foodstuffs has been perhaps the biggest driver for the topside surprises in Swedish inflation thus far into 2025, this would be a welcome development.

In Hungary, the NBH leaves the base rate unchanged at 6.50% as expected. The rate decision is crucial to anchor inflation expectations and stabilise the currency.

In geopolitics, following the parallel talks in Saudi Arabia, the US brokered maritime and energy ceasefires between Ukraine and Russia on Tuesday. The agreements are the first formal commitment since President Trump took office. However, the outlook for implementation remains uncertain, as it depends on Moscow securing the lifting of sanctions on Russian banks involved in agriculture, along with their reinstatement in the SWIFT messaging system; both of which require EU approval.

Equities: Equities were mostly higher yesterday, in a "no news is good news" manner. Investors locked in another 0.2% to the S&P 500, on top of the Monday rally. We see the rebound in US equities as an effect of volatility coming down. Just look at VIX closing in at 17 yesterday from 28 two weeks ago. Stoxx 600 did some catchup, rising 0.7%. Cyclical growth stocks rebounded in both regions, including most of the Mag 7 names. However, tech stocks shared the outperformance with banks and energy. This is a quite rare combination, but I guess both tech and European bank stocks can be considered "momentum" these days. Defensives sold off with health care and staples some of the few sectors in red. Futures are broadly unchanged this morning.

FI&FX: Back-and-forth headlines over a potential Ukraine-Russia ceasefire made for some choppy price action across asset classes. The US yield curve steepened somewhat, led by a lower front-end following a solid US2y auction. EUR/USD continued consolidation around 1.08 whereas USD/JPY traded lower, defying the risk-on sentiment within FX. UK inflation data will be scrutinized today, as will the Riksbank minutes especially considering current money market pricing and the last session's strong run for the SEK.

Elliott Wave View: CADJPY Looking to Rally in 7 Swing WXY Structure

Short Term Elliott Wave view in CADJPY suggests pair ended cycle from 11.20.2024 high in wave (W) at 101.35 as the 1 hour chart below shows. Pair is looking to correct cycle from 11.20.2024 high within wave (X). Internal subdivision of wave (X) is unfolding as a double three Elliott Wave structure. Up from wave (W), wave ((a)) ended at 103.64 and pullback in wave ((b)) ended at 102.02. Wave ((c)) higher ended at 105.029 which completed wave W in higher degree.

Down from there, wave ((a)) ended at 104.16 and wave ((b)) rally ended at 104.92. Wave ((c)) lower ended at 103.13 which completed wave X in higher degree. The pair resumes higher in wave Y with subdivision as a double three structure. Up from wave X, wave ((w)) ended at 105.49. Pullback in wave ((x)) is in progress to correct cycle from 3.20.2025 low before it resumes higher. Near term, as far as pivot at 101.35 low stays intact, expect dips to find buyers in 3, 7, or 11 swing for further upside. Potential target for wave Y higher is 100% – 161.8% Fibonacci extension of wave W. This area comes at 106.75 – 109 area where sellers may appear for further downside.

CADJPY 60 Minutes Elliott Wave Chart

CADJPY Video

https://www.youtube.com/watch?v=BgmlWQZobBI

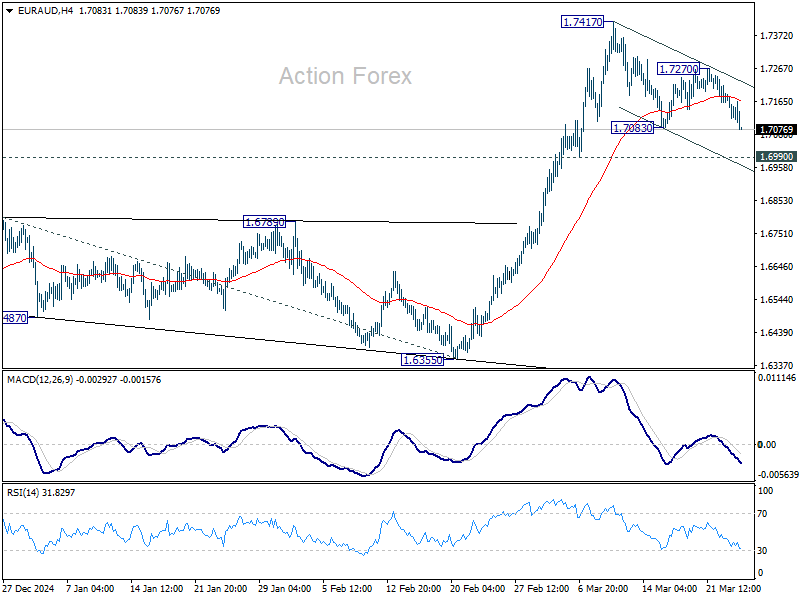

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7092; (P) 1.7143; (R1) 1.7173; More...

EUR/AUD's corrective fall from 1.7417 short term top is resuming and intraday bias is mildly on the downside. Still, downside of the pullback should be contained by 1.6990 support to bring rebound. On the upside, above 1.7270 will bring retest of 1.7417 first. Break there will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

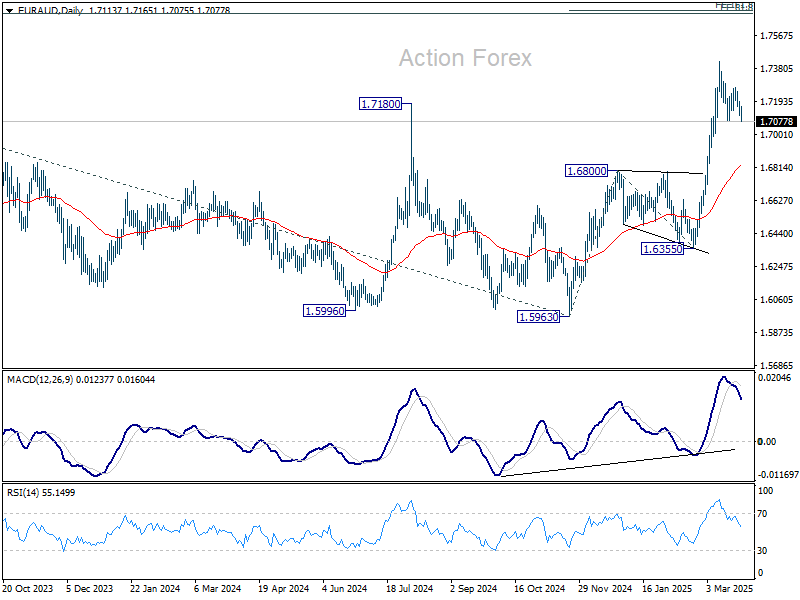

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

Commodities Lift AUD and CAD as Tariff Speculation Builds

Commodity currencies are finding a bid in Asian session today, though still largely range-bound against Dollar. A sharp rally in Copper prices, driven by US tariff fears, is likely giving Aussie a tailwind, countering lingering drag from today’s slightly weaker-than-expected inflation data. Meanwhile, Loonie is benefitting from speculation that Canada may be assigned lower tariffs under US President Donald Trump’s upcoming global trade measures.

According to a Toronto Star report, the Trump administration is preparing a tiered structure for its reciprocal tariffs, grouping trading partners into low, medium, and high tariff categories. Though details remain vague, sources suggest that Canada could be in the "low" tier—but with a twist: tariffs may be cumulative across sectors. The lack of clarity on what qualifies as “high” is keeping markets on edge too, with figures ranging from 25% to triple digits being floated.

Despite the moves in FX, the broader market isn’t displaying strong risk-on conviction. Yen and Swiss Franc are both under pressure—typically a signal of risk appetite—but equities have yet to respond in kind. Yen, in particular, is back as the day’s worst performer, following a recovery yesterday. The lack of follow-through in stocks suggests traders remain hesitant ahead of next week’s highly anticipated “Liberation Day” tariffs announcement on April 2.

In Europe, UK CPI data will be the key focus today. Barring any dramatic surprises, the figures should support BoE’s current stance of slow, measured easing, with rate cuts expected once per quarter. That likely caps any Sterling upside for now, even as traders shift focus toward Euro and GBP cross flows for near-term positioning.

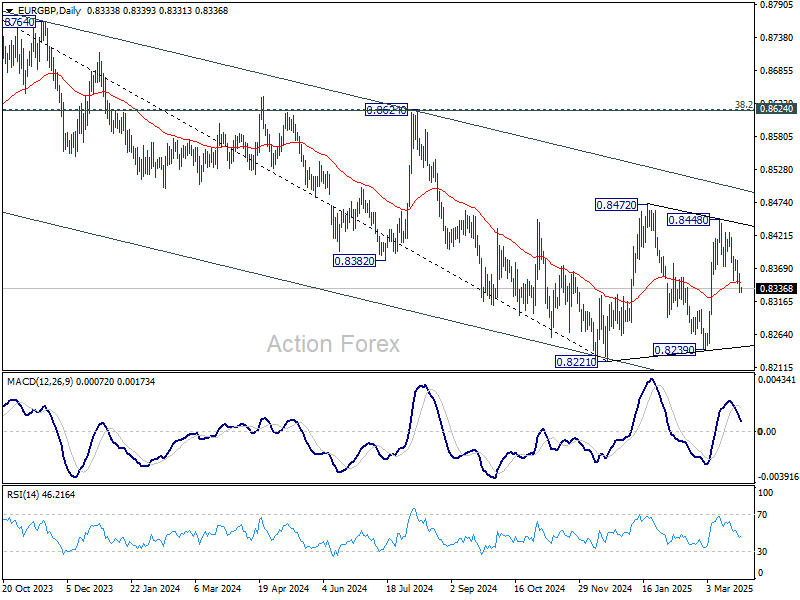

Technically, EUR/GBP's break of 55 D EMA now argues that rebound from 0.8239 has completed at 0.8448 already, as a leg inside the sideway pattern from 0.8221. Deeper fall would be mildly in favor back to 0.8239 support next.

In Asia, at the time of writing, Nikkei is up 1.02%. Hong Kong HSI is up 0.25%. China Shanghai SSE is up 0.02%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.014 at 1.587. Overnight, DOW rose 0.01%. S&P 500 rose 0.16%. NASDAQ rose 0.46%. 10-year yield fell -0.024 to 4.307.

Fed's Goolsbee sees surging inflation expectations as a red flag

Chicago Fed President Austan Goolsbee warned that a shift in market-based long-run inflation expectations toward the elevated levels seen in consumer surveys, such as the University of Michigan’s, would be a "major red flag" demanding immediate Fed attention.

He emphasized that if investor sentiment converges with households' expectations, now at the highest since 1993, Fed would have little choice but to respond.

Goolsbee noted that Fed has moved into “a different chapter” marked by heightened uncertainty, contrasting with the “golden path” of 2023 and 2024, when inflation eased without damaging growth or jobs.

While he still sees interest rates being “a fair bit lower” in the next 12–18 months, he acknowledged that economic unpredictability, particularly surrounding trade policy, may delay Fed’s next move. His stance: “wait and see is the correct approach,” though not without costs.

In conversations with business leaders, Goolsbee said April 2—the date of expected US tariff announcements—has become a key flashpoint of anxiety. This uncertainty, he said, is fueling a broad hesitancy in investment and hiring decisions across the Fed district.

BoJ’s Ueda: Vigilant on upside inflation risks, signals readiness for stronger action

BoJ Governor Kazuo Ueda emphasized today that the central bank remains "vigilant" to upside surprises in "underlying inflation.

While recent "very high" inflation has been driven largely by temporary factors like import costs and food prices, there’s still a possibility that underlying inflation could accelerate more quickly than expected.

Ueda warned that if such "broad-based inflation" materializes, BoJ would need to respond by raising interest rates and even take “stronger steps”.

However, for now, he reaffirmed the view that underlying inflation remains “just a bit” short of the 2% target, though it is on track to gradually converge to that level.

Meanwhile, data released today showed Japan’s services producer price index rose 3.0% yoy in February, a deceleration from January’s 3.2% and below expectations of 3.1%.

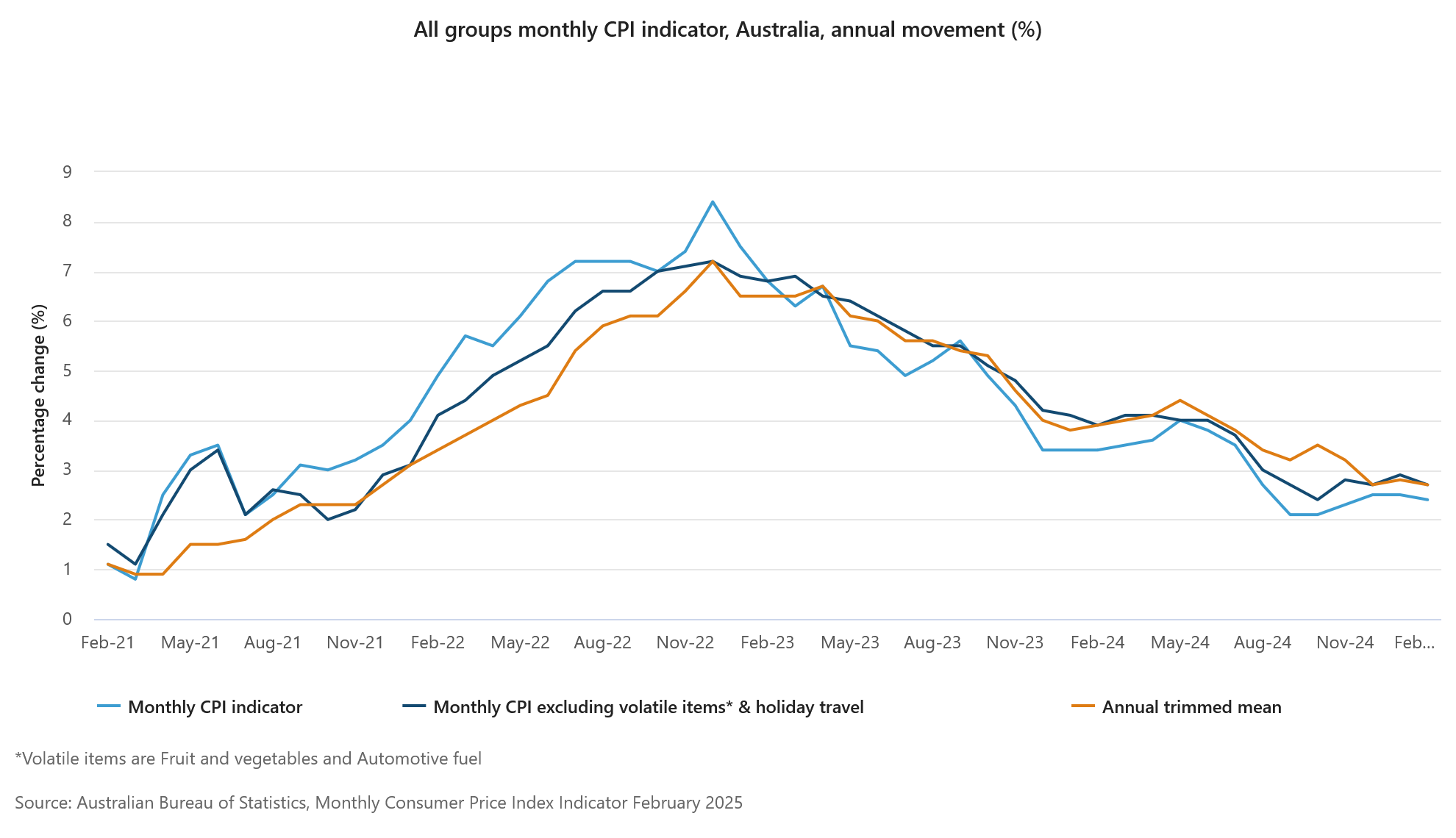

Australia CPI slows to 2.4% in Feb, trimmed mean ticks down to 2.7%

Australia’s monthly CPI eased to 2.4% yoy in February, slightly below expectations of 2.5% yoy and marking a step down from the steady 2.5% yoy pace seen over the past two months.

Core inflation measures also softened, with the trimmed mean slipping from 2.8% yoy to 2.7% yoy. CPI excluding volatile items and holiday travel eased from 2.9% yoy to 2.7% yoy.

The largest contributors to annual inflation were food and non-alcoholic beverages (+3.1%), alcohol and tobacco (+6.7%), and housing (+1.8%).

Still, the overall slowdown adds to the case for RBA to remain on hold at its upcoming meeting. The central bank has made it clear that February’s rate cut does not set an automatic path for further easing. With the more comprehensive Q1 CPI data still to come, today’s numbers are unlikely to shift policy expectations in a meaningful way.

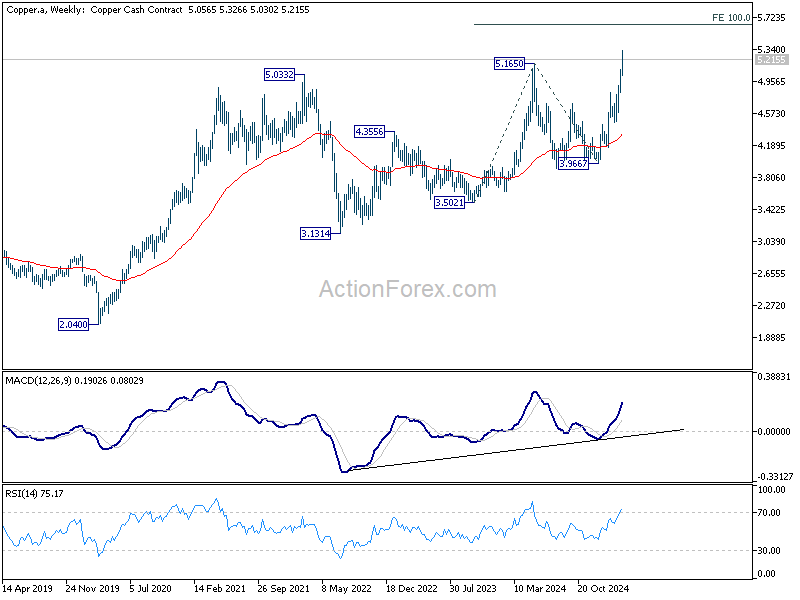

Tariff fears drive Copper to record in classic commodity fifth-wave extension

US Copper prices surged to fresh record highs, driven by rising expectations that President Donald Trump may soon impose tariffs on copper imports.

Traders are responding to signals that the Commerce Department’s review—ordered by Trump in February—is advancing quickly, and that a decision, possibly imposing tariffs of up to 25%, could be announced within weeks.

The surge reflects not only speculative buying but also a defensive scramble as traders and manufacturers brace for supply disruptions. A key driver of the move is fear, with the current rally taking the form of a classic fifth-wave extension seen in commodity markets—when panic buying exacerbates already tight conditions.

Technically, the uptrend from January low at 3.9667 is now in its final leg of a five-wave sequence. While there may still be some upside left, strong resistance lies ahead.

Despite the bullish momentum, Copper should soon face strong resistance soon. Two key projection levels—5.538 (161.8% of the 4.1568 to 4.8168 move from 4.4702) and 5.6298 (100% projection of 3.5021 to 5.1650 from 3.9667)—form a crucial zone that should cap the rally.

Looking ahead

UK CPI is the main focus in European session while Swiss will release UBS economic expectations. Later in the day, US durable goods orders will be published. BoC will release summary of deliberations.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7092; (P) 1.7143; (R1) 1.7173; More...

EUR/AUD's corrective fall from 1.7417 short term top is resuming and intraday bias is mildly on the downside. Still, downside of the pullback should be contained by 0.6990 support to bring rebound. On the upside, above 1.7270 will bring retest of 1.7417 first. Break there will resume rise from 1.6335 to 161.8% projection of 1.5963 to 1.6800 from 1.6355 at 1.7709 next.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

Fed’s Goolsbee sees surging inflation expectations as a red flag

Chicago Fed President Austan Goolsbee warned that a shift in market-based long-run inflation expectations toward the elevated levels seen in consumer surveys, such as the University of Michigan’s, would be a "major red flag" demanding immediate Fed attention.

He emphasized that if investor sentiment converges with households' expectations, now at the highest since 1993, Fed would have little choice but to respond.

Goolsbee noted that Fed has moved into “a different chapter” marked by heightened uncertainty, contrasting with the “golden path” of 2023 and 2024, when inflation eased without damaging growth or jobs.

While he still sees interest rates being “a fair bit lower” in the next 12–18 months, he acknowledged that economic unpredictability, particularly surrounding trade policy, may delay Fed’s next move. His stance: “wait and see is the correct approach,” though not without costs.

In conversations with business leaders, Goolsbee said April 2—the date of expected US tariff announcements—has become a key flashpoint of anxiety. This uncertainty, he said, is fueling a broad hesitancy in investment and hiring decisions across the Fed district.

Tariff fears drive Copper to record in classic commodity fifth-wave extension

US Copper prices surged to fresh record highs, driven by rising expectations that President Donald Trump may soon impose tariffs on copper imports.

Traders are responding to signals that the Commerce Department’s review—ordered by Trump in February—is advancing quickly, and that a decision, possibly imposing tariffs of up to 25%, could be announced within weeks.

The surge reflects not only speculative buying but also a defensive scramble as traders and manufacturers brace for supply disruptions. A key driver of the move is fear, with the current rally taking the form of a classic fifth-wave extension seen in commodity markets—when panic buying exacerbates already tight conditions.

Technically, the uptrend from January low at 3.9667 is now in its final leg of a five-wave sequence. While there may still be some upside left, strong resistance lies ahead.

Despite the bullish momentum, Copper should soon face strong resistance soon. Two key projection levels—5.538 (161.8% of the 4.1568 to 4.8168 move from 4.4702) and 5.6298 (100% projection of 3.5021 to 5.1650 from 3.9667)—form a crucial zone that should cap the rally.

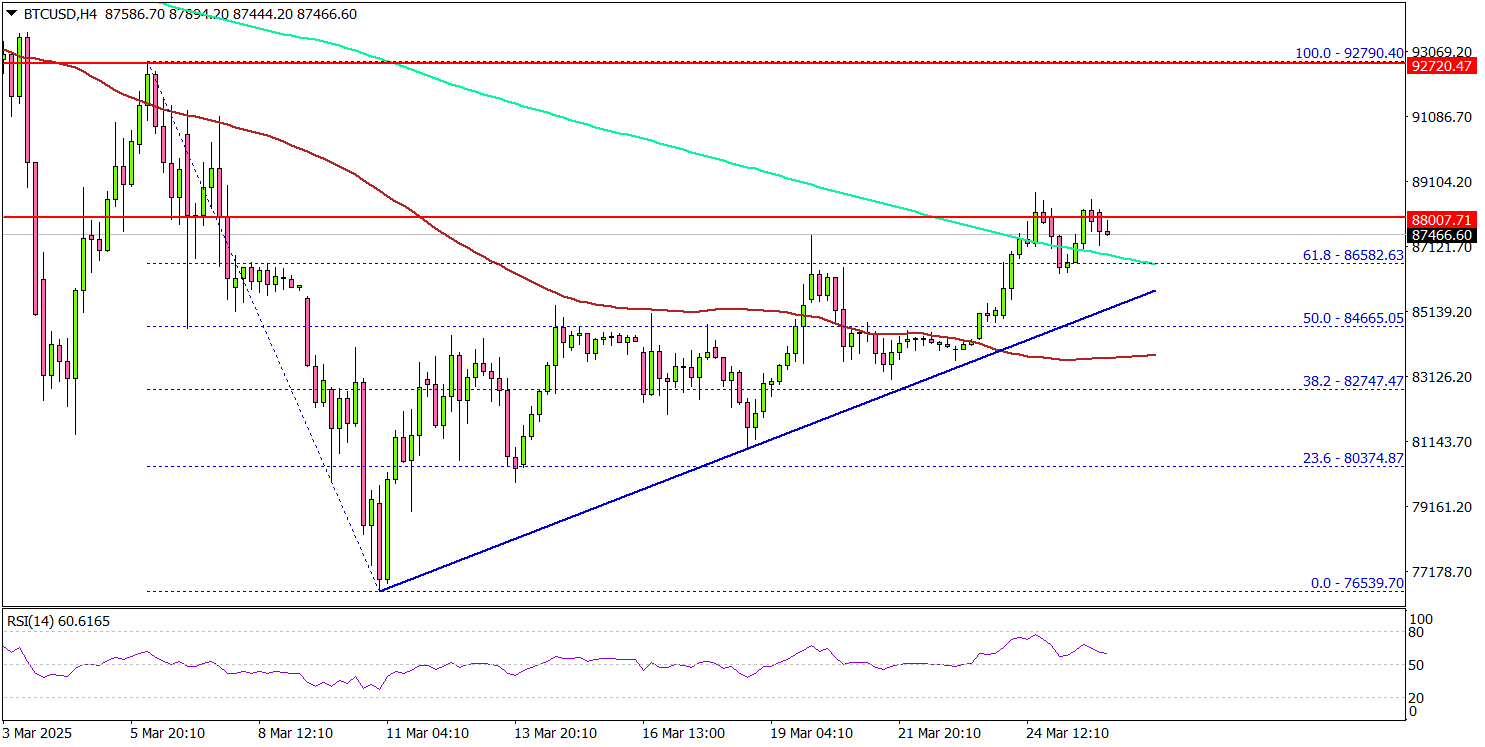

Bitcoin Eyes $90K Comeback—Can Bulls Regain Control?

Key Highlights

- Bitcoin price started a recovery wave above the $85,000 resistance zone.

- BTC is following a bullish trend line with support at $85,400 on the 4-hour chart.

- Ethereum price also recovered and climbed above the $2,000 level.

- Gold could aim for a fresh increase if it stays above $3,000.

Bitcoin Price Technical Analysis

Bitcoin price remained stable above $82,000 and started a recovery wave against the US Dollar. BTC cleared the $84,500 and $85,000 resistance levels.

Looking at the 4-hour chart, the price settled above the $85,500 level, the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). There was a move above the 50% Fib retracement level of the downward move from the $92,790 swing high to the $76,539 low.

BTC is now following a bullish trend line with support at $85,400 on the same chart. On the upside, the price could face resistance near the $88,800 level.

The next key resistance is $89,500. The main resistance could be $90,000. A successful close above $90,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $92,000 level. Any more gains might call for a test of $92,500.

Immediate support is near the $85,500 level. The next key support sits at $83,800. A downside break below $83,800 might send Bitcoin toward the $82,500 support. Any more losses might send the price toward the $81,200 support zone.

Looking at Ethereum, there was a decent upward move and the bulls were able to clear the $2,000 resistance zone.

Today’s Economic Releases

- US Durable Goods Orders for Feb 2025 – Forecast -1.0% versus +3.2% previous.

Australia CPI slows to 2.4% in Feb, trimmed mean ticks down to 2.7%

Australia’s monthly CPI eased to 2.4% yoy in February, slightly below expectations of 2.5% yoy and marking a step down from the steady 2.5% yoy pace seen over the past two months.

Core inflation measures also softened, with the trimmed mean slipping from 2.8% yoy to 2.7% yoy. CPI excluding volatile items and holiday travel eased from 2.9% yoy to 2.7% yyo.

The largest contributors to annual inflation were food and non-alcoholic beverages (+3.1%), alcohol and tobacco (+6.7%), and housing (+1.8%).

Still, the overall slowdown adds to the case for RBA to remain on hold at its upcoming meeting. The central bank has made it clear that February’s rate cut does not set an automatic path for further easing. With the more comprehensive Q1 CPI data still to come, today’s numbers are unlikely to shift policy expectations in a meaningful way.

BoJ’s Ueda: Vigilant on upside inflation risks, signals readiness for stronger action

BoJ Governor Kazuo Ueda emphasized today that the central bank remains "vigilant" to upside surprises in "underlying inflation.

While recent "very high" inflation has been driven largely by temporary factors like import costs and food prices, there’s still a possibility that underlying inflation could accelerate more quickly than expected.

Ueda warned that if such "broad-based inflation" materializes, BoJ would need to respond by raising interest rates and even take “stronger steps”.

However, for now, he reaffirmed the view that underlying inflation remains “just a bit” short of the 2% target, though it is on track to gradually converge to that level.

Meanwhile, data released today showed Japan’s services producer price index rose 3.0% yoy in February, a deceleration from January’s 3.2% and below expectations of 3.1%.