Sample Category Title

Summary 3/24 – 3/28

Monday, Mar 24, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Mar P | 50.4 | |

| 22:00 | AUD | Services PMI Mar P | 50.8 | |

| 00:30 | JPY | Manufacturing PMI Mar P | 49.2 | 49 |

| 00:30 | JPY | Services PMI Mar P | 53.7 | |

| 08:15 | EUR | France Manufacturing PMI Mar P | 46.2 | 45.8 |

| 08:15 | EUR | France Services PMI Mar P | 46.3 | 45.3 |

| 08:30 | EUR | Germany Manufacturing PMI Mar P | 47.7 | 46.5 |

| 08:30 | EUR | Germany Services PMI Mar P | 52.3 | 51.1 |

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | 48.3 | 47.6 |

| 09:00 | EUR | Eurozone Services PMI Mar P | 51.2 | 50.6 |

| 09:30 | GBP | Manufacturing PMI Mar P | 47.3 | 46.9 |

| 09:30 | GBP | Services PMI Mar P | 51.2 | 51 |

| 13:45 | USD | Manufacturing PMI Mar P | 51.9 | 52.7 |

| 13:45 | USD | Services PMI Mar P | 51.2 | 51 |

| 23:50 | JPY | BoJ Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:00 | AUD | Manufacturing PMI Mar P | |

| Forecast: | Previous: 50.4 | ||

| 22:00 | AUD | Services PMI Mar P | |

| Forecast: | Previous: 50.8 | ||

| 00:30 | JPY | Manufacturing PMI Mar P | |

| Forecast: 49.2 | Previous: 49 | ||

| 00:30 | JPY | Services PMI Mar P | |

| Forecast: | Previous: 53.7 | ||

| 08:15 | EUR | France Manufacturing PMI Mar P | |

| Forecast: 46.2 | Previous: 45.8 | ||

| 08:15 | EUR | France Services PMI Mar P | |

| Forecast: 46.3 | Previous: 45.3 | ||

| 08:30 | EUR | Germany Manufacturing PMI Mar P | |

| Forecast: 47.7 | Previous: 46.5 | ||

| 08:30 | EUR | Germany Services PMI Mar P | |

| Forecast: 52.3 | Previous: 51.1 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Mar P | |

| Forecast: 48.3 | Previous: 47.6 | ||

| 09:00 | EUR | Eurozone Services PMI Mar P | |

| Forecast: 51.2 | Previous: 50.6 | ||

| 09:30 | GBP | Manufacturing PMI Mar P | |

| Forecast: 47.3 | Previous: 46.9 | ||

| 09:30 | GBP | Services PMI Mar P | |

| Forecast: 51.2 | Previous: 51 | ||

| 13:45 | USD | Manufacturing PMI Mar P | |

| Forecast: 51.9 | Previous: 52.7 | ||

| 13:45 | USD | Services PMI Mar P | |

| Forecast: 51.2 | Previous: 51 | ||

| 23:50 | JPY | BoJ Minutes | |

| Forecast: | Previous: | ||

Tuesday, Mar 25, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Germany IFO Business Climate Mar | 87 | 85.2 |

| 09:00 | EUR | Germany IFO Current Assessment Mar | 85 | |

| 09:00 | EUR | Germany IFO Expectations Mar | 85.4 | |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | 4.60% | 4.50% |

| 13:00 | USD | Housing Price Index M/M Jan | 0.20% | 0.40% |

| 14:00 | USD | Consumer Confidence Mar | 94.2 | 98.3 |

| 14:00 | USD | New Home Sales Feb | 682K | 657K |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Germany IFO Business Climate Mar | |

| Forecast: 87 | Previous: 85.2 | ||

| 09:00 | EUR | Germany IFO Current Assessment Mar | |

| Forecast: | Previous: 85 | ||

| 09:00 | EUR | Germany IFO Expectations Mar | |

| Forecast: | Previous: 85.4 | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Jan | |

| Forecast: 4.60% | Previous: 4.50% | ||

| 13:00 | USD | Housing Price Index M/M Jan | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 14:00 | USD | Consumer Confidence Mar | |

| Forecast: 94.2 | Previous: 98.3 | ||

| 14:00 | USD | New Home Sales Feb | |

| Forecast: 682K | Previous: 657K | ||

Wednesday, Mar 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Feb | 2.50% | 2.50% |

| 07:00 | GBP | CPI M/M Feb | -0.10% | |

| 07:00 | GBP | CPI Y/Y Feb | 2.90% | 3% |

| 07:00 | GBP | Core CPI Y/Y Feb | 3.60% | 3.70% |

| 07:00 | GBP | RPI M/M Feb | -0.10% | |

| 07:00 | GBP | RPI Y/Y Feb | 3.60% | 3.60% |

| 09:00 | CHF | UBS Economic Expectations Mar | 3.4 | |

| 12:30 | USD | Durable Goods Orders Feb | -0.70% | 3.20% |

| 12:30 | USD | Durable Goods Orders ex Transportation Feb | 0.40% | 0% |

| 14:30 | USD | Crude Oil Inventories | 1.7M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Feb | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 07:00 | GBP | CPI M/M Feb | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | CPI Y/Y Feb | |

| Forecast: 2.90% | Previous: 3% | ||

| 07:00 | GBP | Core CPI Y/Y Feb | |

| Forecast: 3.60% | Previous: 3.70% | ||

| 07:00 | GBP | RPI M/M Feb | |

| Forecast: | Previous: -0.10% | ||

| 07:00 | GBP | RPI Y/Y Feb | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 09:00 | CHF | UBS Economic Expectations Mar | |

| Forecast: | Previous: 3.4 | ||

| 12:30 | USD | Durable Goods Orders Feb | |

| Forecast: -0.70% | Previous: 3.20% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Feb | |

| Forecast: 0.40% | Previous: 0% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.7M | ||

Thursday, Mar 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 3.80% | 3.60% |

| 12:30 | USD | Initial Jobless Claims (Mar 21) | 225K | 223K |

| 12:30 | USD | GDP Annualized Q4 F | 2.30% | 2.30% |

| 12:30 | USD | GDP Price Index Q4 F | 2.40% | 2.40% |

| 12:30 | USD | Goods Trade Balance (USD) Feb P | -134.6B | -155.6B |

| 12:30 | USD | Wholesale Inventories Feb P | 0.80% | |

| 14:00 | USD | Pending Home Sales M/M Feb | -4.60% | |

| 14:30 | USD | Natural Gas Storage | 9B | |

| 23:30 | JPY | Tokyo CPI Y/Y Mar | 2.90% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Mar | 2.20% | 2.20% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Mar | 2.20% | |

| 23:50 | JPY | BoJ Summary of Opinions |

| GMT | Ccy | Events | |

|---|---|---|---|

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | |

| Forecast: 3.80% | Previous: 3.60% | ||

| 12:30 | USD | Initial Jobless Claims (Mar 21) | |

| Forecast: 225K | Previous: 223K | ||

| 12:30 | USD | GDP Annualized Q4 F | |

| Forecast: 2.30% | Previous: 2.30% | ||

| 12:30 | USD | GDP Price Index Q4 F | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | Goods Trade Balance (USD) Feb P | |

| Forecast: -134.6B | Previous: -155.6B | ||

| 12:30 | USD | Wholesale Inventories Feb P | |

| Forecast: | Previous: 0.80% | ||

| 14:00 | USD | Pending Home Sales M/M Feb | |

| Forecast: | Previous: -4.60% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 9B | ||

| 23:30 | JPY | Tokyo CPI Y/Y Mar | |

| Forecast: | Previous: 2.90% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Mar | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Mar | |

| Forecast: | Previous: 2.20% | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

Friday, Mar 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany GfK Consumer Confidence Apr | -22.2 | -24.7 |

| 07:00 | GBP | Retail Sales M/M Feb | -0.30% | 1.70% |

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -16.8B | -17.4B |

| 07:00 | GBP | GDP Q/Q Q4 F | 0.10% | 0.10% |

| 07:00 | GBP | Current Account (GBP) Q4 | -16.7B | -18.1B |

| 08:00 | CHF | KOF Economic Barometer Mar | 102.6 | 101.7 |

| 08:55 | EUR | Germany Unemployment Change Feb | 10K | 5K |

| 08:55 | EUR | Germany Unemployment Rate Feb | 6.20% | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Mar | 96.3 | |

| 10:00 | EUR | Eurozone Industrial Confidence Mar | -11.4 | |

| 10:00 | EUR | Eurozone Services Sentiment Mar | 6.2 | |

| 10:00 | EUR | Eurozone Consumer Confidence Mar F | -14.5 | |

| 12:30 | CAD | GDP M/M Jan | 0.20% | |

| 12:30 | USD | Personal Income Feb | 0.40% | 0.90% |

| 12:30 | USD | Personal Spending Feb | 0.60% | -0.20% |

| 12:30 | USD | PCE Price Index M/M Feb | 0.30% | |

| 12:30 | USD | PCE Price Index Y/Y Feb | 2.50% | |

| 12:30 | USD | Core PCE Price Index M/M Feb | 0.30% | |

| 12:30 | USD | Core PCE Price Index Y/Y Feb | 2.60% | |

| 14:00 | USD | Michigan Consumer Sentiment Index Mar F | 57.9 | 57.9 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany GfK Consumer Confidence Apr | |

| Forecast: -22.2 | Previous: -24.7 | ||

| 07:00 | GBP | Retail Sales M/M Feb | |

| Forecast: -0.30% | Previous: 1.70% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | |

| Forecast: -16.8B | Previous: -17.4B | ||

| 07:00 | GBP | GDP Q/Q Q4 F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 07:00 | GBP | Current Account (GBP) Q4 | |

| Forecast: -16.7B | Previous: -18.1B | ||

| 08:00 | CHF | KOF Economic Barometer Mar | |

| Forecast: 102.6 | Previous: 101.7 | ||

| 08:55 | EUR | Germany Unemployment Change Feb | |

| Forecast: 10K | Previous: 5K | ||

| 08:55 | EUR | Germany Unemployment Rate Feb | |

| Forecast: | Previous: 6.20% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Mar | |

| Forecast: | Previous: 96.3 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Mar | |

| Forecast: | Previous: -11.4 | ||

| 10:00 | EUR | Eurozone Services Sentiment Mar | |

| Forecast: | Previous: 6.2 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Mar F | |

| Forecast: | Previous: -14.5 | ||

| 12:30 | CAD | GDP M/M Jan | |

| Forecast: | Previous: 0.20% | ||

| 12:30 | USD | Personal Income Feb | |

| Forecast: 0.40% | Previous: 0.90% | ||

| 12:30 | USD | Personal Spending Feb | |

| Forecast: 0.60% | Previous: -0.20% | ||

| 12:30 | USD | PCE Price Index M/M Feb | |

| Forecast: | Previous: 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Feb | |

| Forecast: | Previous: 2.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Feb | |

| Forecast: | Previous: 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Feb | |

| Forecast: | Previous: 2.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Mar F | |

| Forecast: 57.9 | Previous: 57.9 | ||

Weekly Economic & Financial Commentary: Increased Uncertainty Complicates the FOMC’s Job

Summary

United States: February Bounce More Likely a Head Fake

- Retail sales, industrial production, existing home sales and housing starts all jumped in February, rebounding from the declines posted the month prior. On closer examination, however, the underlying data point to economic growth hitting a soft patch.

- Next week: New Home Sales (Tue.), Durable Goods (Wed.), Personal Income & Spending (Fri.)

International: Active Week for Foreign Central Bank Announcements

- It was a busy week for foreign central bank announcements. The Bank of England and Bank of Japan both held rates steady, though we see the former as still on course for a May rate cut, and the latter for a May rate hike. Sweden's central bank held rates steady, while the Swiss National Bank cut its policy rate by 25 bps, and in both cases, we view the easing cycle as likely finished. Brazil's central bank raised its Selic Rate 100 bps and signaled a slower pace of tightening going forward.

- Next week: Eurozone PMIs (Mon.), Norges Bank Policy Rate (Thu.), Banxico Policy Rate (Thu.)

Interest Rate Watch: Increased Uncertainty Complicates the FOMC's Job

- As widely expected, the FOMC kept its target range for the federal funds rate unchanged at its policy meeting this week. The post-meeting statement noted the obvious by stating "uncertainty around the economic outlook has increased."

Topic of the Week: Thoughts on Germany's Fiscal Reform

- A sea change in German fiscal policy is underfoot with a massive package of fiscal stimulus measures for defense and infrastructure expected to be signed into law today. At the core of the pro-growth policy is an adjustment to the country's famously strict borrowing rules and fiscal austerity paired with a renewed energy for German rearmament.

What’s Next: Flash PMIs, UK CPI & US PCE

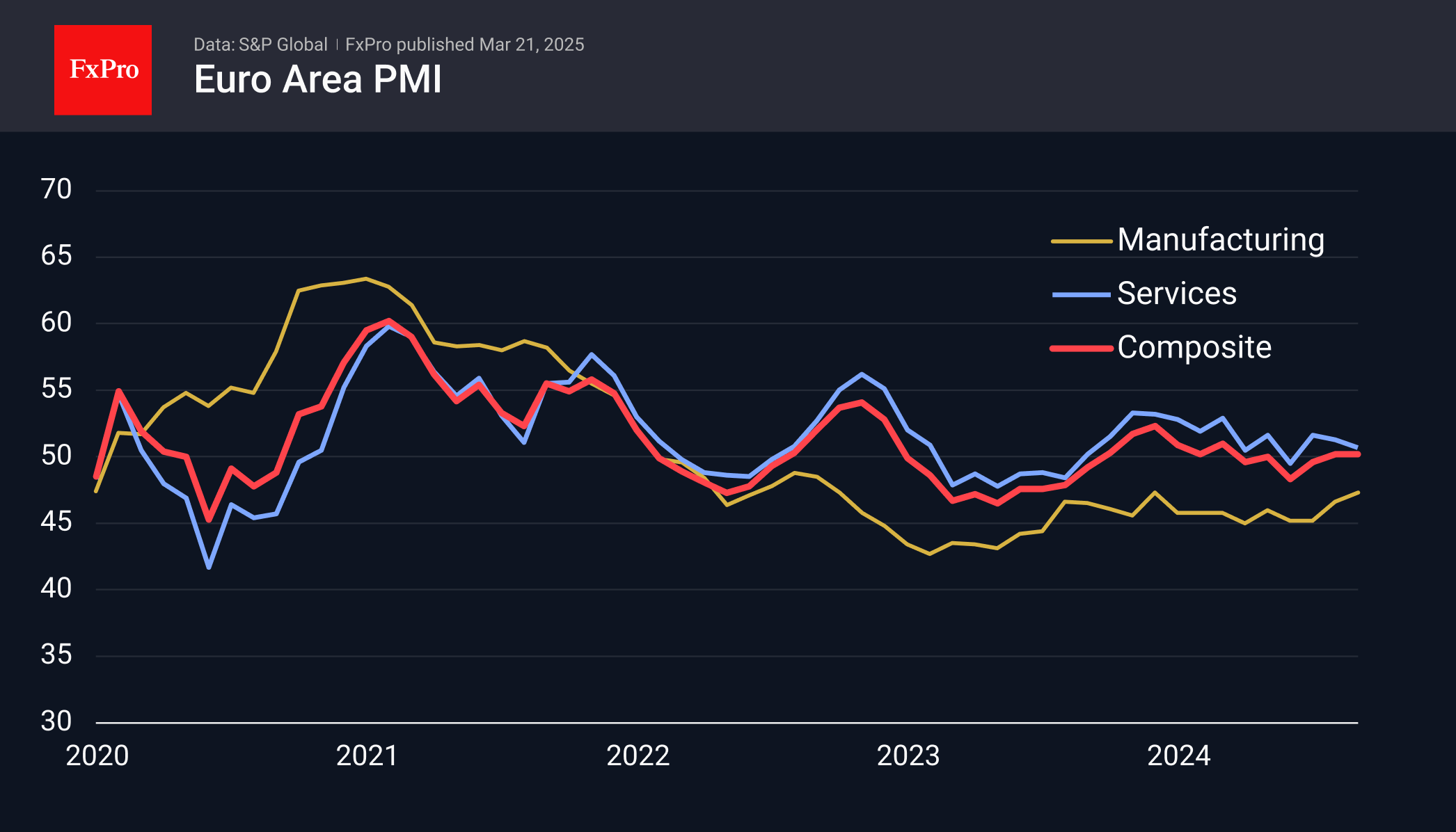

The new week will start with the first estimate of the PMI business activity indexes for March, which will be influential for the single European currency. In recent months, this indicator has picked up considerably, which has helped equities and the euro. There are growing expectations that not only the service sector but also manufacturing activity will return to growth territory after many months of contraction.

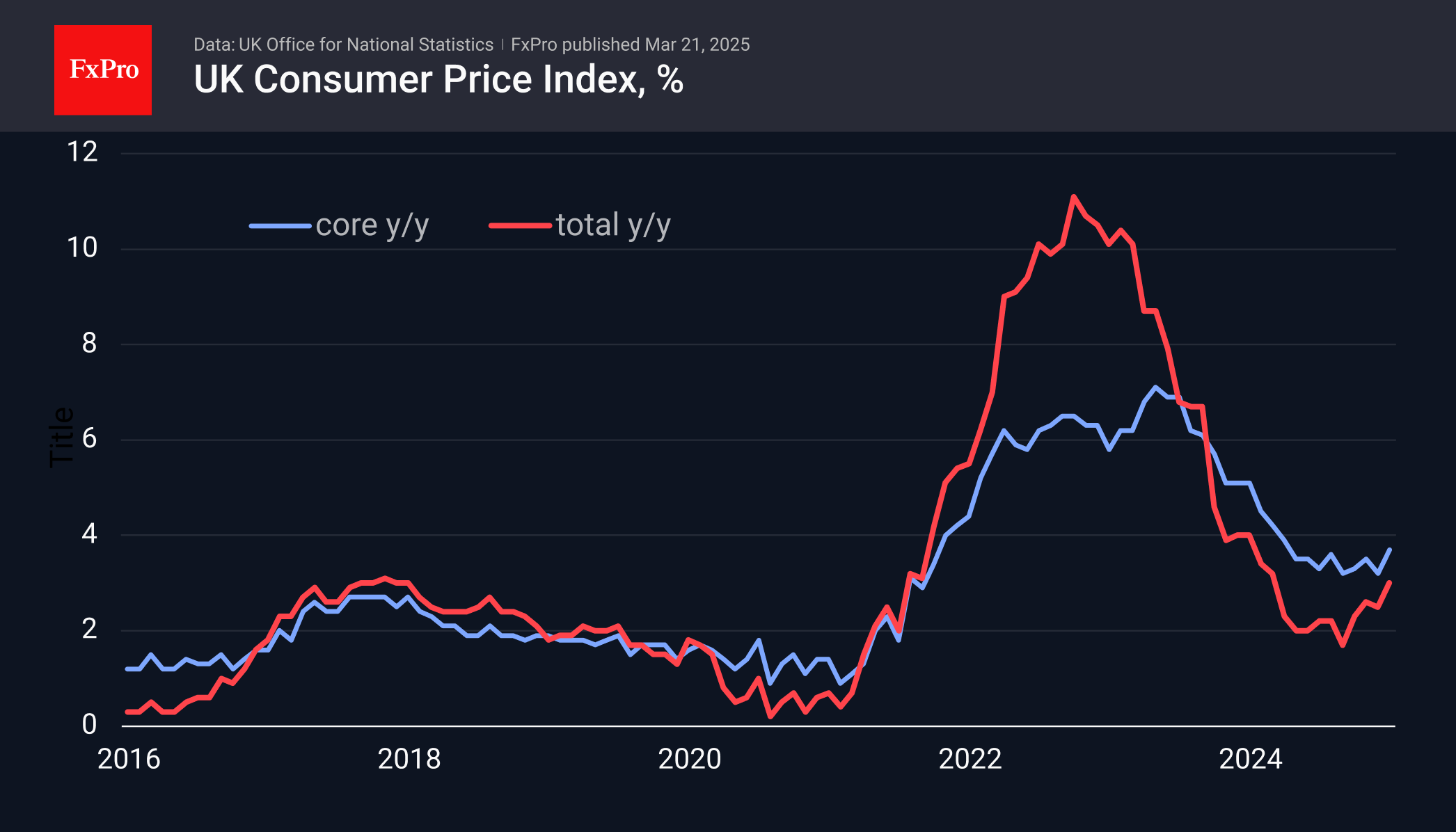

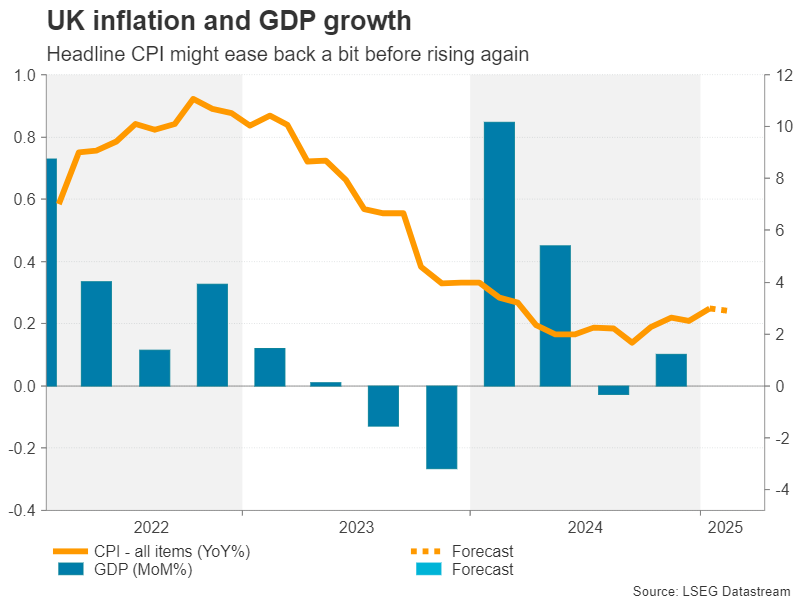

On Wednesday, it is worth paying attention to the UK inflation figures, where we see an acceleration since October. This is an important reason why the Bank of England is not cutting rates. Analysts, on average, forecast a slowdown from 3.0% to 2.9%. Deviations from forecasts will drive the pound.

Friday sees the release of personal income and household spending statistics and the Fed’s preferred measure of inflation. There was a slowdown here in January, will it persist in February? It won’t be easy for the dollar to continue strengthening if that’s the case.

Week Ahead – Flash PMIs, US and UK Inflation Eyed as Tariff War Rumbles On

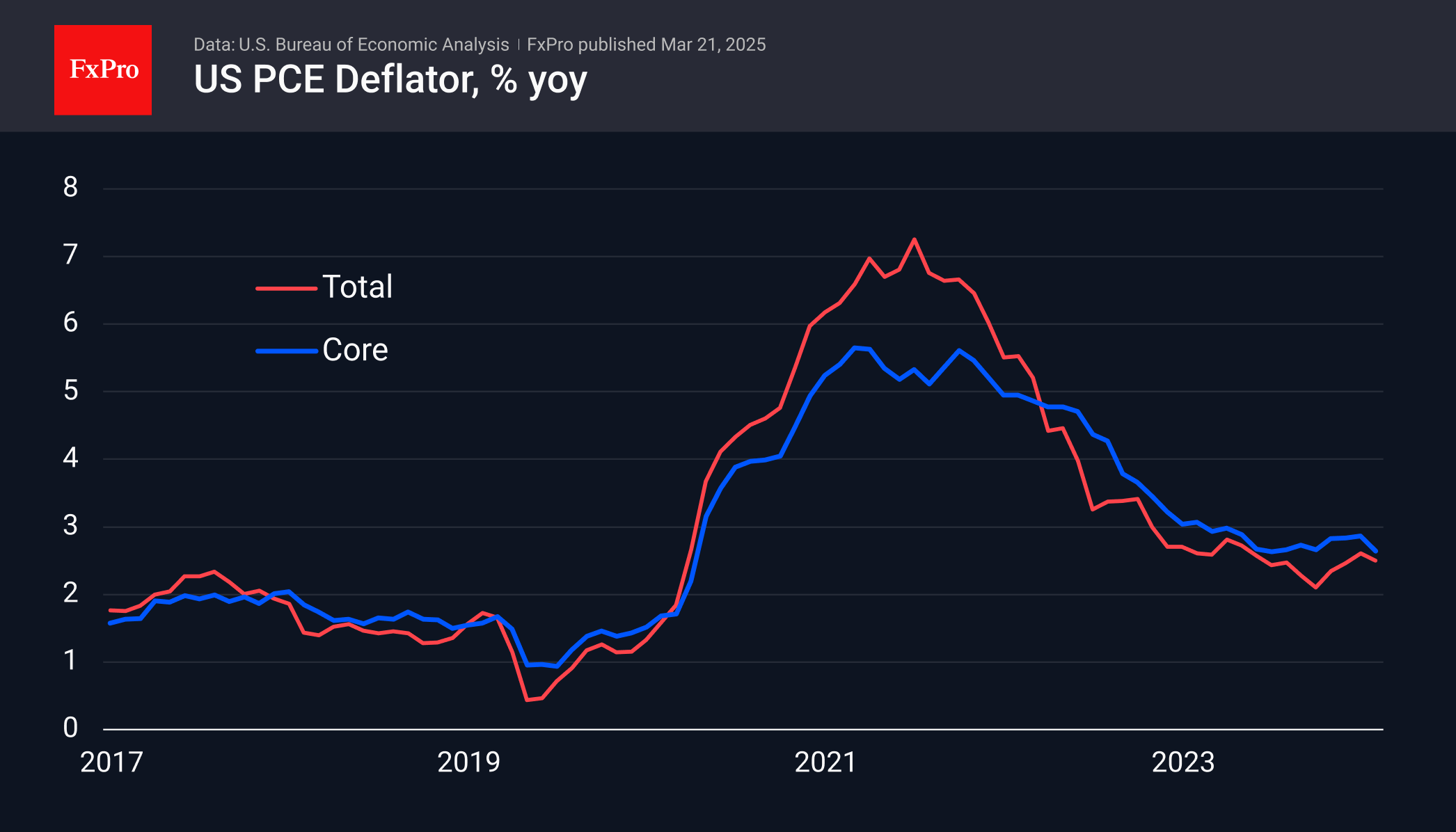

- US PCE inflation up next, but will consumption data matter more?

- UK budget and CPI in focus after hawkish BoE decision.

- Euro turns to flash PMIs for bounce as rally runs out of steam.

- Inflation numbers out of Tokyo and Australia also on the agenda.

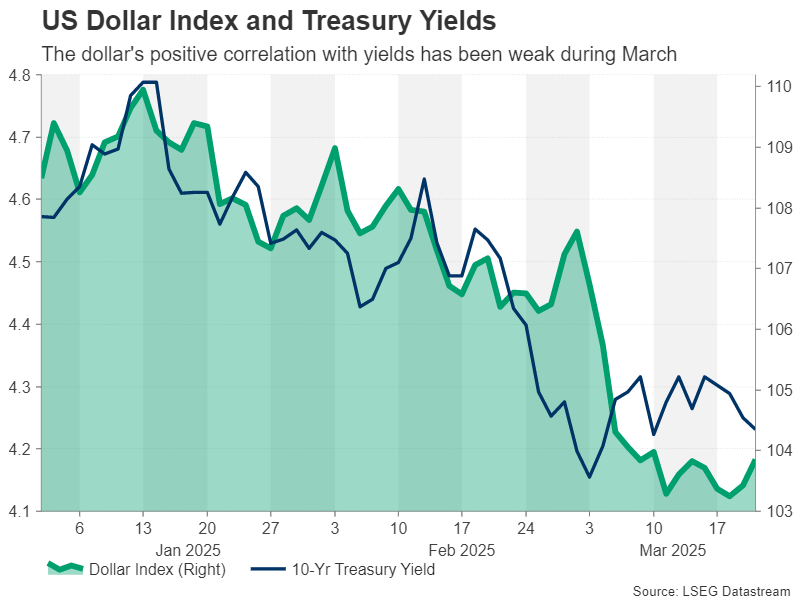

Dollar ignores Powell’s dovish soundbites

The US dollar has been on a positive footing since the March FOMC meeting, as Fed Chair Jerome Powell downplayed the risk of a recession while maintaining caution over the inflation outlook. Treasury yields, in contrast, dipped after the meeting, and stocks on Wall Street rose, backing the notion of a dovish surprise by the Fed.

The dollar’s contradictory response could be explained by the fact that it hadn’t been tracking the recovery in yields from earlier this month, so this was just catchup. However, it’s debatable how dovish Powell really was. Yes, he soothed market nerves by suggesting that any inflationary effect from higher tariffs would likely be transitory, but he wasn’t particularly upbeat about the Fed hitting its 2% target anytime soon either.

The fact that FOMC members maintained their prediction of just two 25-basis-point-cuts this year and signalled gradual easing over the course of the forecast period indicates the Fed is still in inflation fighting mode. Markets, on the other hand, think there’s a strong likelihood of a third cut this year, as many investors are betting that the US economy will slow more than what the Fed is projecting.

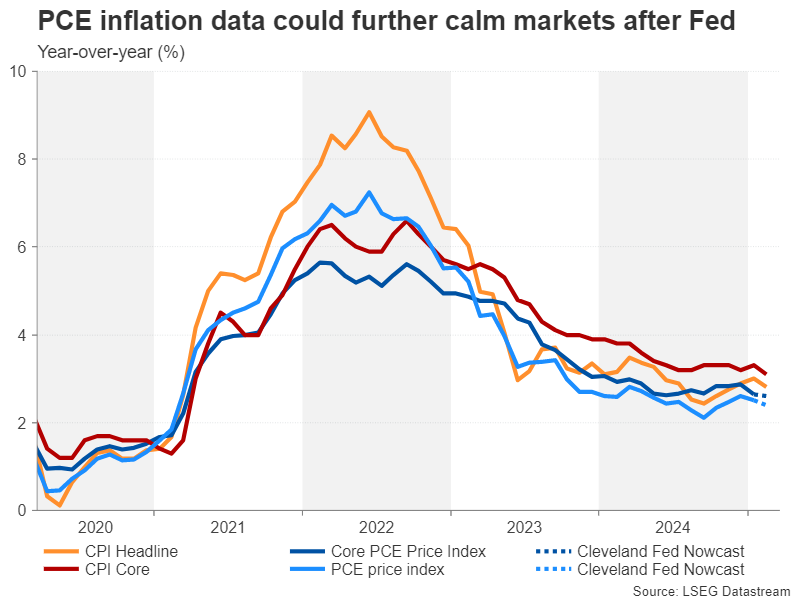

Is the US consumer still spending?

Hence, growth data could climb to the top of investors’ minds over the coming months, if it hasn’t already, with inflation metrics attracting somewhat less attention. The highlight next week will be Friday’s personal income and outlays report, which includes the PCE inflation readings.

The Cleveland Fed’s own Nowcast model is estimating that the headline PCE price index moderated from 2.5% to 2.4% y/y in February but that the core PCE price index stayed unchanged at 2.6% y/y.

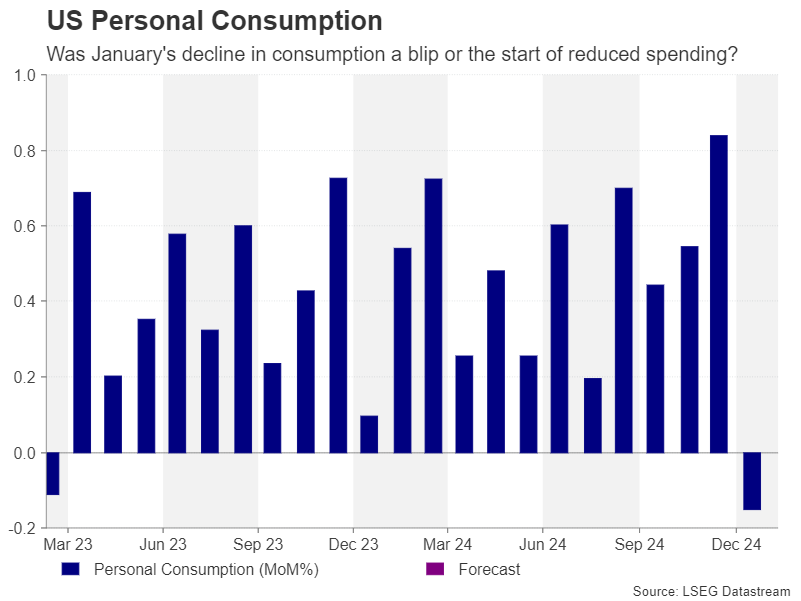

Such numbers are likely to neither please nor upset the markets, and so the personal income and spending component of the report could take the spotlight. Personal consumption fell by 0.2% m/m in January. But this was after several months of strong increases. Analysts are forecasting a rebound of 0.6% m/m in February. Therefore, any unexpected weakness could revive slowdown fears, putting the dollar on the backfoot again.

Recession angst could return

It’s possible, though, that recession concerns could resurface much earlier in the week, as the March flash PMI survey by S&P Global is out on Monday. The Conference Board’s consumer confidence index will be watched on Tuesday along with new home sales. Durable goods orders for February will follow on Wednesday, with pending home sales and the final estimate for Q4 GDP drawing some interest on Thursday.

Any unforeseen softness in the upcoming releases could have a devastating impact on risk appetite if they are accompanied by fresh tariff headlines. The April 2 deadline for the Trump administration’s reciprocal tariffs is fast approaching and the President may decide to ratchet up the rhetoric ahead of it.

Pound on stagflation watch

March has been a strong month for sterling, as it’s surged by about 3% against the US dollar. Much of that is attributed to the dollar’s dramatic pullback. But another factor is that UK economic indicators over the past couple of months have been somewhat better than expected. More importantly, inflation is on the rise again.

The Bank of England is facing a difficult dilemma, as it’s worried about a possible rise in both unemployment and inflation in the months ahead. The high risk of stagflation could cap further gains for the pound, although the UK’s exclusion from Trump’s trade war is a significant source of support for the time being.

The March PMI numbers due Monday will provide a crucial update as to whether British businesses are being affected by the global trade uncertainty, if any of them are planning to reduce their workforce and if prices pressures are easing or not. But investors will probably be focusing more on Wednesday’s CPI report for February.

The headline CPI rate jumped to 3.0% y/y in January, which is at the top of the Bank of England’s 1.0%-3.0% inflation buffer. The Bank expects CPI to reach 3.75% in Q3, so another reading above 3.0% is unlikely to alarm markets. Instead, investors will be looking underneath the surface, to see whether core and services CPI are accelerating at a similar rapid pace.

Last chance for reeves?

Any upside surprises could cast a dark cloud over the UK’s embattled finance minister Rachel Reeves’ Spring Statement later in the day where she is expected to outline big spending cuts. The bulk of the reductions will likely come from the welfare system – something that’s bound to be greeted more positively by the market than by voters.

A cut in spending would not only be taken as a sign that the government is not keen on any further tax increases to close the budget hole, but it’s also disinflationary, potentially making it easier for the BoE to resume rate cuts later in the year. For the pound, however, there could be an immediate boost from the budget update if Reeves also announces some new measures aimed at kickstarting the stagnant economy.

The run of data will continue on Friday with February retail sales and revised Q4 GDP figures.

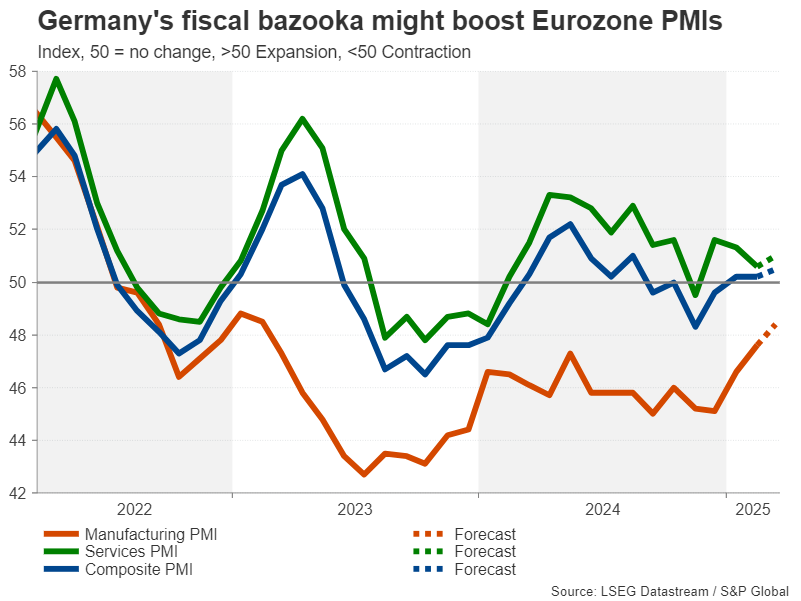

Euro bulls pin hopes on PMIs as uptrend stalls

The euro’s incredible rally on the back of the German government’s substantial fiscal package and reform to borrowing rules appears to be petering out. The single currency is still the best performing major against the dollar in the year to date, but for investors to take the uptrend to the next level, they will probably need some fresh incentives.

That could come in the form of Monday’s flash PMI figures, but the odds aren’t looking good as business confidence has deteriorated in the face of US tariffs and Trump’s fury at the European Union’s retaliatory levies.

The Eurozone composite PMI was flat in February, as an improvement in manufacturing activity was offset by a weaker services PMI. A pickup in the latter, however, can’t be ruled out as the services sector is less exposed to the immediate effects of higher tariffs, and so the euro stands some chance of receiving a lift from the data.

Traders will also be keeping an eye on Germany’s Ifo business climate gauge on Tuesday for signs that the new coalition’s spending plans are boosting optimism.

Tariffs complicate RBA and BoJ policy paths

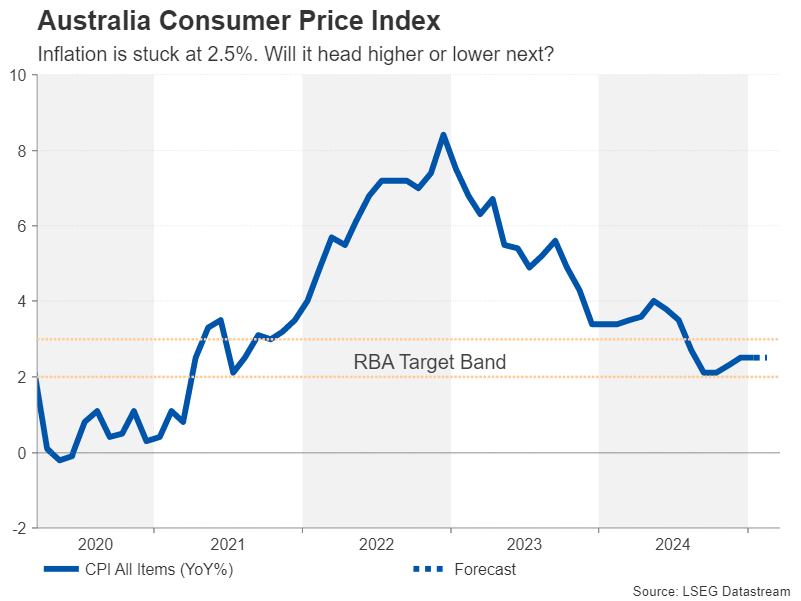

Elsewhere, inflation will be the dominant theme in Australia and Japan where the latest releases are expected on Wednesday and Friday, respectively. Inflation in Australia is forecast to have stayed at 2.5% y/y for the third consecutive month in February, which may not be very encouraging. However, concerns are growing about the economy amid the trade tensions that threaten to cause turmoil in Australia’s largest export market – China.

The Australian dollar hasn’t enjoyed much of a rally against the greenback, but a stronger-than-forecast CPI print could push it higher if investors reduce their rate cut bets for the RBA.

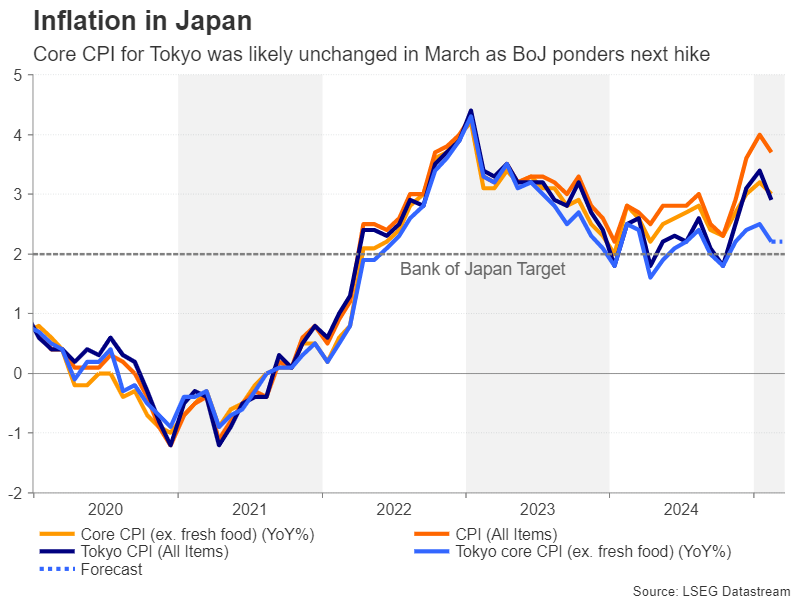

In Japan, tariffs are also weighing on the outlook and the Bank of Japan is hesitant to commit to a timeline for further rate hikes. The absence of more hawkish signals from the BoJ has led to a bit of a pullback in the yen, though not so much against the dollar.

But the yen could resume its ascent if the incoming data points to ongoing price pressures, bolstering the case for a near-term rate increase. Producer prices for the services sector are out on Wednesday, while the March CPI estimates for the Tokyo region are due on Friday.

A potentially bigger driver for the yen, however, could be Friday’s Summary of Opinions of the BoJ’s March meeting. If the summary reveals board members are keener on further tightening than indicated by Governor Ueda in his latest press conference, investors might bring forward their rate hike expectations, bolstering the yen.

Weekly Focus – Fed Sees Weaker Growth and Higher Inflation

After some volatile weeks, markets were relatively calm this week, as there were no big surprises, also not from the US central bank. As expected, the Fed did not change interest rates, but the bank lowered its forecast for GDP growth this year from 2.1% to 1.7%, while increasing its inflation forecast from 2.5% to 2.7%, both consistent with a larger effect of tariffs. Whether that speaks for higher or lower interest rates than would otherwise be the case depends on whether tariffs are expected to persistently lift inflation and not just cause a one-off price increase. Fed chair Powell seems to think that a persistent effect is unlikely, and markets reacted to the adjustments by sending yields slightly lower, also because 18 out of 19 members of the monetary policy committee indicated that they see risks for growth mostly to the downside, whereas the outlook was balanced 12 months ago. As we see it, the US economy is slowing down somewhat, and there is a good case for the Fed to gradually make monetary policy less restrictive. However, unemployment is low, and the bank is not in a hurry, and our main scenario is for them to wait and see what happens politically also at the May meeting before cutting in June.

In Europe, the German parliament as expected passed the large fiscal spending bill of the incoming government before the old parliament is dissolved and the new one takes over next week. Many interesting and potentially market moving decisions remain though, as the plan must be implemented and the new government formed.

Like the Fed, the Bank of England kept rates unchanged while signalling that it still sees room for cuts later. The Swedish Riksbank also held steady but here, the signals are not for more cuts, see also page 3. The Swiss national bank did cut rates amid the very low inflation there, and as widely expected the Bank of Japan did not change rates this time but given the renewed vitality in the economy, we see a strong case for more rate hikes in the future.

China published data for January and February (at the same time because of the Chinese New Year holiday), with upside surprises in retail sales and home sales, but continued decline in house prices. It is a strong priority for the government to get consumer spending going, and stabilisation in the housing market is seen as a precondition for that. This week, the State Council presented a plan to 'vigorously boost' consumer spending. If successful, that would also have implications for global goods demand.

The ECB has stated that incoming data will determine whether rates are cut in April, and one of the crucial data points in that regard is likely to be the March PMIs out on Monday. The growth picture has improved somewhat this year, and we expect that to continue driven by manufacturing, despite the great uncertainty. We also get the first March inflation numbers (for France and Spain) on Friday.

The US data calendar for the coming week is fairly light, with the Conference Board's consumer confidence on Tuesday as a potential highlight. In the UK, Chancellor Reeves will present the Spring Statement where the Labour government faces some tough choices in meeting its fiscal objective while aiming to improve the UK economy's growth prospects.

Sunset Market Commentary

Markets

Markets build on recent momentum today in absence of eco data of any significance on both sides of the Atlantic. European stock markets correct a second session straight up and over 1% (underwhelming outcome EU Summit?!) with opening losses of similar magnitude in the US. Disappointing earnings by the likes of FedEx and Nike add to stalling US growth fears. Core bonds advance with US Treasuries slightly outperforming German Bunds. The front end of the curve outperforms with yields changes in the US varying between -1.8 bps (30-yr) to -4.5 bps (2-yr). We don’t believe this is a lasting comeback of core bonds in light of this week’s developments. Central bankers around the globe sent a clear signal that upside inflation risks outweigh downside growth risks, going from the Fed’s updated Summary of Economic Projections, over the BoE’s more hawkish 8-1 status quo vote or the Riksbank end to the cutting cycle to BoC governor Macklem just spelling it out-loud and the Brazilian central bank taking its policy rate beyond the post-Covid peak. Inflation is here to stay with inflation expectations becoming at risk of being de-anchored. “Transitory” is how Fed chair Powell labelled the inflationary impact from tariffs. Fool me once, shame on you; fool me twice shame on me. Markets won’t get fooled around this time. German Bund yields correct 1.9 bps (30-yr) to 4 bps (5-yr) lower with the German upper house as expected passing the spending package. Defense spending in excess of 1% of GDP will be exempt from borrowing restrictions, an off-budget infrastructure fund will be able to raise another €500bn over the next 12 years with €100bn earmarked for the Climate and Transition Fund and €100bn for regional projects and Germany’s states get room to borrow up to 0.35% of GDP instead of having to run balanced budgets. The US dollar recovers some ground, but gains remain technically insignificant. Recapturing the 104 area on a trade-weighted basis would be a first sign of some short term peace. Previous resistance near 1.08 is similarly the first reference for EUR/USD (currently changing hands at 1.0833).

Next week’s eco calendar looks promising with March PMI surveys immediately on Monday. Early March German confidence indicators suggest a significant improvement for European gauges linked to fiscal U-turn, while US indicators might show more of the recession fatigue. In Tuesday’s US consumer confidence, we especially eye the evolution of inflation expectations given the recent surge in this component (both short term and long term) in the Michigan survey. Wednesday is key for UK markets with February CPI numbers and UK Chancellor Reeves’ Spring Budget. On Thursday’s there’s a special reference to the US Congressional Budget Office’s 30-yr US budget outlook which risks becoming another red flag for (long term) US Treasuries with President Trump’s fiscal agenda and the higher interest rate climate set to significantly raise future budget deficits. US PCE deflators wrap things up on Friday after which we rapidly approach Tariff Day (April 2nd).

News & Views

Czech confidence data improved more than expected in March. The overall composite confidence indictor improved from 97.8 to 99.5, while a near stabilization was expected. The rise was supported by both a similar improvement in consumer sentiment (98.8 from 96.6) and in business confidence (99.6 from 98.0). CSO also analyzed that both the composite and the business indicator where higher compared to the same month last year. In the consumer survey, the share of consumers expecting the economic situation in the Czech Republic to deteriorate over the next twelve months decreased, but remained relatively high. The share of households expecting their financial situation to deteriorate also decreased slightly. Business confidence increased across all sectors. Compared with February, it increased the most in trade (+2.3 points), followed by selected services (+1.8 points), industry (+1.3 points) and construction (+1.1 points).

Belgian consumer confidence fell sharply in March, almost completely wiping out the increase in February. The indicator dropped from -4 to -10. The decline was due to rising pessimism over the general economic situation in Belgium (-35 from -24) and increased fears over unemployment (20 from 8), which had abated considerably last month. On a personal level, households’ expectations concerning their own financial situation remained unchanged. However, their savings intentions fell, after having risen by almost the same degree last month (17 from 20).

NY Fed’s Williams: Policy rate ‘appropriate’ amid high uncertainty and mixed signals

New York Fed President John Williams highlighted the elevated level of uncertainty facing the US economy. Speaking at a public event, Williams acknowledged that “it’s hard to know with any precision how the economy will evolve,” pointing to a wide range of potential scenarios shaped by fiscal and trade policy shifts, geopolitical risks, and other external developments.

Williams noted that both hard economic data and forward-looking indicators have been giving mixed signals. He added that the recent surge in policy uncertainty measures.

Despite the murky backdrop, he defended Fed’s current stance, describing the 4.25% to 4.5% policy rate range as “modestly restrictive” and “entirely appropriate.” With inflation still running slightly above target and labor markets remaining solid, there appears to be little urgency to shift course in the near term.

Fed’s Goolsbee: Uncertainty warrants patience, but rates likely be lower in 12-18 months

Chicago Fed President Austan Goolsbee struck a cautious but balanced tone in his latest remarks, saying Fed should "wait to see some of these things get cleared up" given the high degree of policy uncertainty.

Speaking to CNBC, he noted a shift in tone among business and civic leaders in recent weeks, highlighting growing "anxiety" and delayed capital spending decisions as companies weigh the impact of tariffs and other fiscal policy developments.

Despite the cautious near-term stance, Goolsbee reaffirmed his longer-term view that interest rates are likely to be lower 12 to 18 months from now.

While the Fed may not be in a rush to act immediately, he emphasized the importance of continued progress on inflation as a key condition for future easing.

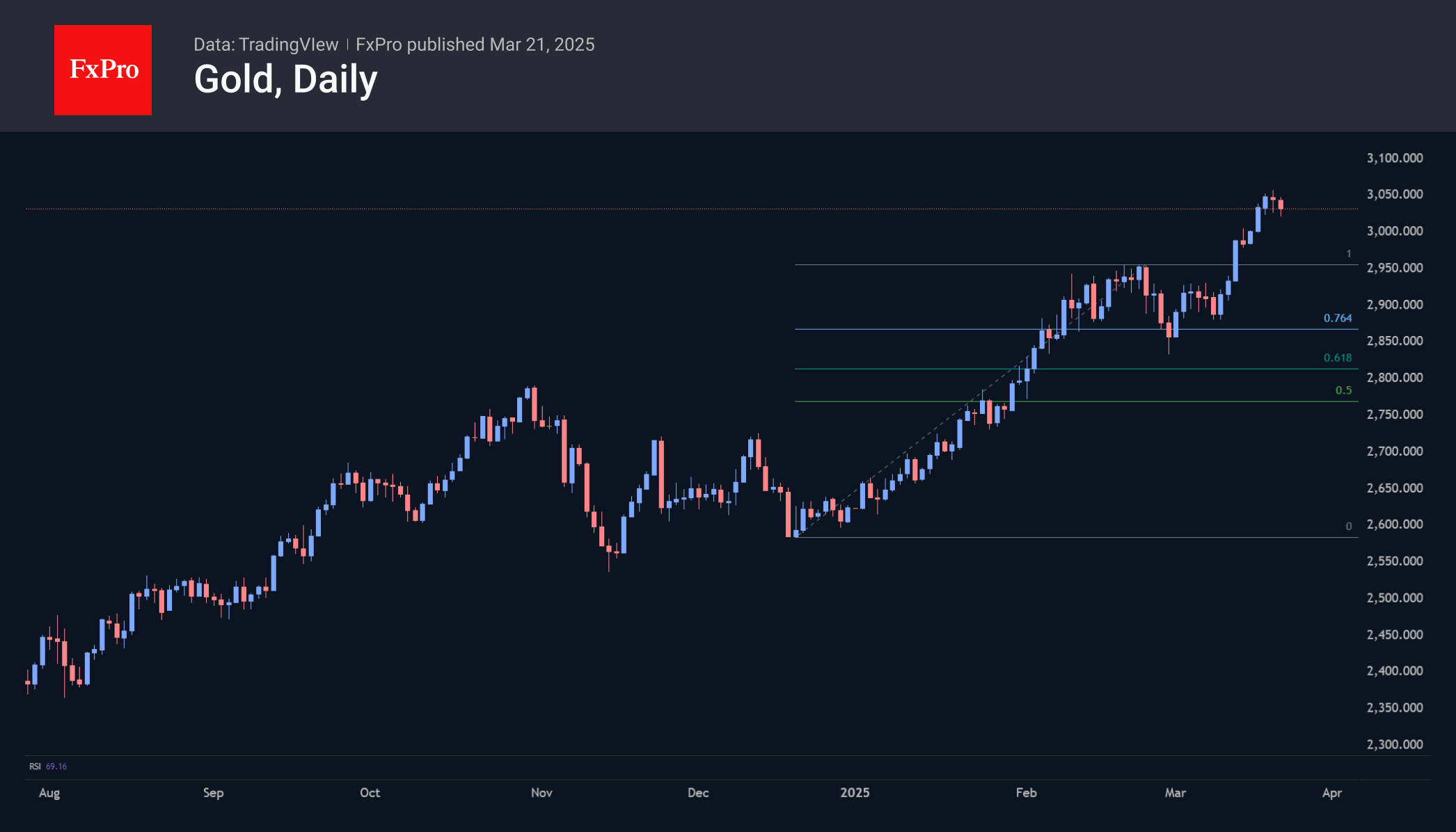

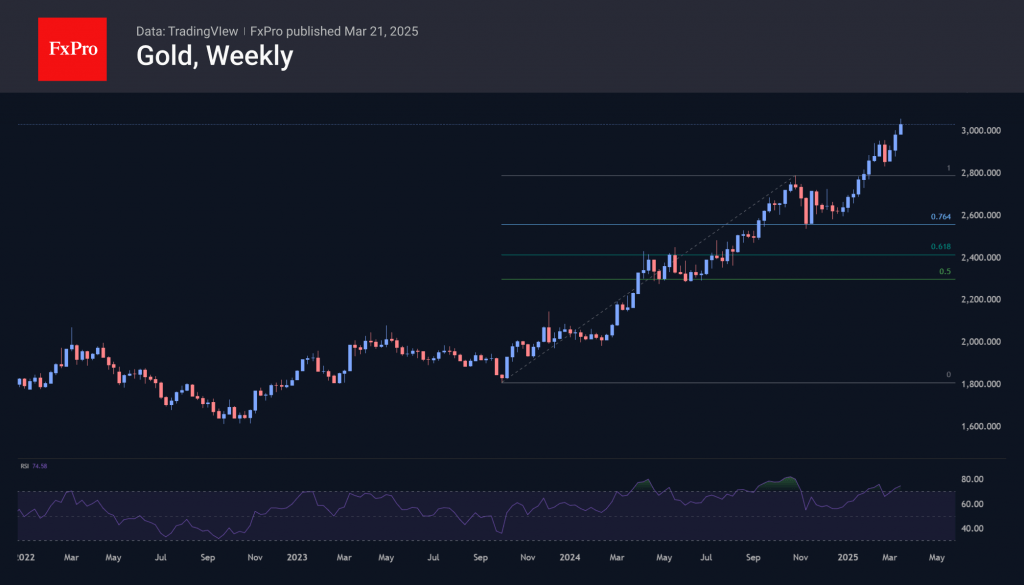

Gold: Growth Opportunities

Gold has been in an uptrend since the beginning of March, and the rally accelerated as gold hit new highs at the end of last week, when the spot price hit a new record of $3057. We see this breakout as the start of a new expansionary momentum with an upside potential of $3180/oz, which represents 161.8% of the upside momentum from the start of the year to the February peak.

The alternative view is also bullish. According to it, gold has completed a correction since the beginning of the year, following the rally from October 2023 to November 2024. The bulls are now targeting the level of $3400 an ounce. This seems like the bulls’ target for the coming months. However, we should not lose sight of the fact that the current rally in gold is accumulating extreme overbought conditions on both the daily and weekly timeframes.

This disposition leaves room for sharp rallies in the near term on a short squeeze, i.e. liquidation of short positions. However, the pause in growth may well be followed by a broad correction, which we will be sure to report on in the future.

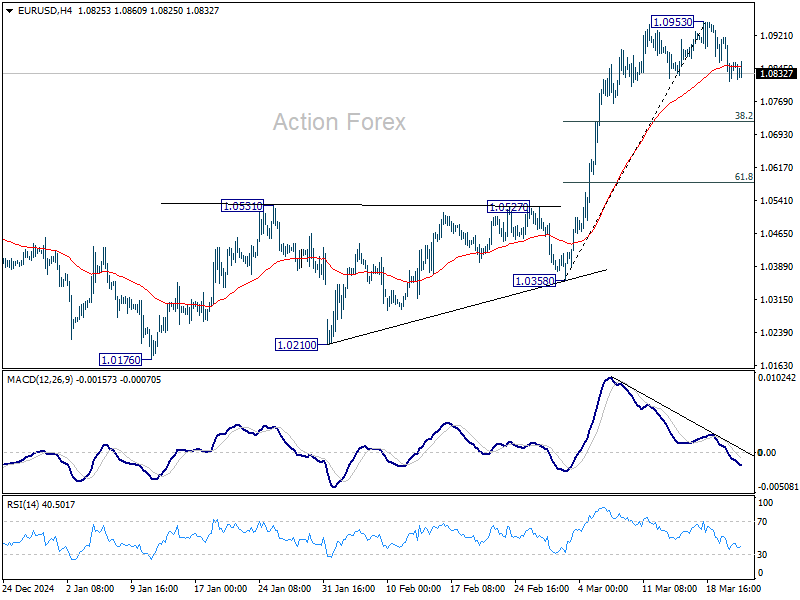

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0806; (P) 1.0862; (R1) 1.0908; More...

No change in EUR/USD's outlook and intraday bias stays on the downside. Pull back from 1.0953 short term top would extend to 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Strong support should be seen there to bring rebound. Meanwhile, break of 1.0953 will resume the rally from 1.0176 towards 1.1274 key resistance.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.