Sample Category Title

EUR/USD Correcting Lower for a Third Day

Markets

European markets unlike their US counterpart had a pessimistic view on the Fed’s policy decision. While the latter took comfort from chair Powell’s reassuring message during the presser, the former seem to eye the stagflationary risks in the updated forecasts. Stocks, core bond yields and the euro dropped. Sentiment then took a turn for the better around the start of US dealings. News of the EU delaying retaliatory tariffs until mid-April (from April 1) to allow for dialogue helped the turnaround, as did way stronger than expected housing data a bit later. Equities in Europe bottomed though still finished 1% lower in the close. WS shrugged off most of the initial contagion losses during the US session. European yields cut their previous losses in half, ending around 2-3 bps lower in a daily perspective. US rates (almost) fully wiped out declines of up to 7 bps. EUR/USD bounced off 1.082 to close at 1.085. Sterling rose as high as EUR/GBP 0.835 before paring some of those gains to 0.837. The labour market report was a tad better than anticipated and the Bank of England held rates steady. A deeper dive in the 8-1 split vote (one member voting for a cut) showed two policymakers who voted for cuts at all three previous meetings taking a cautious turn by supporting the rates hold. UK money markets pared some of the easing bets from more than to slightly below two rate cuts this year.

Asian (and more specially Chinese) risk-off is set to spillover in some degree to Europe with stock futures pointing at a 0.4% lower open. Risk sentiment will probably remain key for markets in absence of an inspiring economic calendar and ahead of the weekend. We expect technical trading in FX and FI markets. The dollar is trying to build on a bottoming out process with DXY attacking the 104 resistance area. EUR/USD is correcting lower for a third day but should find support around 1.08. The US 10-yr yield holds tight in a narrow sideways trading range while the 10-yr EU swap grinds lower. The January high at 2.63% serves as a strong support. The unpredictable tariff narrative appears to gain some traction again as the April 2 reciprocal date draws closer. The EU’s olive branch yesterday was answered by White House press secretary Leavitt with renewed “big tariff” threats. Yesterday’s EU summit revealed some divisions, first and foremost with Hungary again opposing the €5bn in Ukrainian aid. Southern countries are seeking a broader definition in terms of what to include under “defense spending”, which is exempted for 1.5% of GDP from the deficit rules. French president Macron late yesterday announced a new summit in Paris next week during which he is looking for a coalition of the willing.

News & Views

In a speech in Calgary yesterday, Tiff Macklem elaborated on the difficult context that the central bank is facing due to uncertainty surrounding US tariffs on Canadian imports. The Bank of Canada governor indicated that it could be appropriate for the bank consider a range of economic estimates rather than one single forecast. He also pointed to the dangers of adjusting policy too quickly based on an uncertain outlook. In the current environment policy should be less forward looking until the situation is clearer and then act more quickly ‘when things crystallize’. This at least suggest the BOC is moving to a wait-and-see approach. Macklem nonetheless indicated that there should be no doubt that the BOC stays committed to low inflation. The Bank wants to avoid that higher import costs due to the deprecation of the currency and retaliatory tariffs will spread to consumer prices and affect the anchoring of inflation expectations. The impact of the tariffs war limits the Banks’ room to support the economy. The market currently only sees about a 35% for an additional 25 bps BOC rate cut next month.

British consumers’ moral in March turned slightly more positive for the third consecutive month. The GFK consumer confidence index improved from -20 to -19 to be compared to short-term low of -22 in January. Even so, the indicator remains well below the long-term average near -10. Consumers turned slightly more optimistic about the economic situation, both in the last 12 months (-42 from -44- and also for the next 12 months (-29 from –31). At the same time consumer again turned less positive on their personal finances. "The current stability is to be welcomed but it won't take much to upset the fragile consumer mood," Neil Bellamy, consumer insights director at GfK was quoted.

Rotation Trade Gives Signs of Exhaustion

A big week of central bank decisions is coming to an end with the central bankers bathing in uncertainty of the tariffs and the economic implications of the rapidly escalating trade war. The Federal Reserve (Fed) maintained rates unchanged this week, cut its growth projections, lifted its inflation forecasts, said that a tariff-led pick up in inflation would be ‘transitory’ and decided to reduce the pace of QT. Then, the Riksbank maintained status quo while signalling the end of policy easing, the Bank of England (BoE) kept its policy unchanged, meanwhile, the Swiss National Bank (SNB) announced a much expected 25bp cut in an effort to counter the franc’s appreciation when inflation sits at 0.4% on a yearly basis. As a result, the franc and sterling fell on SNB’s rate trimming and BoE’s uncertain outlook respectively. The SMI gained in a session that saw the major European indices offered, while the FTSE 100 closed flat, outperforming most of the European index complex hit by an overall pessimism.

The US stock markets couldn’t extend the Fed optimism into a second session as FedEx – that’s results are seen as an indicator of economic health – lowered its profit forecast for the third straight quarter. The rapid loss of appetite hints that there is a stronger case for a further selloff in US stocks than a sustainable rebound. But the good news is that a period of economic slowdown doesn’t necessarily mean lower asset prices; the central bank policies tend to be supportive of asset valuations in periods of economic slowdown.

Rotation trade gives signs of slowing

Capital flows toward the European equities were the major theme of the Q1 but flows toward the European equities and the euro could start slowing in Q2 as many investors now consider that most of the upcoming European infrastructure and defence spending is already priced in. Consequently, the EURUSD may have consumed its short-term upside potential and could opt for a deeper downside correction before finding the courage to rechallenge the 1.10 offers. Elsewhere, the yen is softer this morning against the dollar on the back of softer-than-expected inflation figures in February. The US dollar weakness that started by mid-January could be gently coming to a bottom and we could see a rebound in the US dollar across the board.

Another leg of the rotation trade is also showing signs of weakness this week. The Hang Seng index was down more than 2% yesterday and shed another 2.40% today on the waning stimulus-backed purchases and the tariff shenanigans. Chinese technology stocks have room to close the gap with the Nasdaq 100 stocks for the next three months but the gains could be vulnerable to a global selloff.

Appetite loss and rising inflation expectations back oil and gas stocks. While oil companies are dealing with lower oil prices, they are lucky enough to be in a sector that will be explicitly be supported by the Trump administration for about four more years, they pay good dividends, they offer strong buybacks, and they could simply ditch their expensive plans of green transition to focus on money-making traditional fossil-fuel business. SPDR’s energy sector fund has been outperforming the S&P500 peers since the beginning of the year and should see stable inflows from investors looking to hedge against the risk of surging global inflation.

Germany Set to Pass the Largest Fiscal Package in Three Decades

In focus today

Germany's fiscal package is anticipated to pass in the Bundesrat, potentially delivering the largest fiscal boost to the German economy in over three decades. The package has the backing of a two-thirds majority, including the CDU/CSU, SPD, Greens and Bavarian Free Voters. For insights into the implications, read our analysis: Research Germany - Fiscal policy to boost growth but also inflation concerns, 19 March.

In the broader euro area, focus turns to the euro area consumer confidence indicator for March. This is one of the important data points ahead of the ECB meeting in April as consumer's mood and thus private consumption is key for the growth outlook in the euro area. Following declining confidence at the end of last year confidence has partly rebounded in the first months of 2025 and is expected to have increased further in March.

Economic and market news

What happened overnight

In Japan, core inflation rose to 3% y/y slightly exceeding the expectations of 2.9% y/y. Headline inflation eased to 3.7% y/y from 4% seen last month, although significantly above the BoJ's 2% target. The data print paves the way for considering further rate hikes by the BoJ. Food prices remain the most important inflation driver, while core price pressures are modest. The local Tokyo data for February indicates this trend has not changed. The big question is whether it will, once consumers gain purchasing power after an expected wage bump this spring.

What happened yesterday

In the central bank space, the Riksbank, the Bank of England (BoE) and the Swiss National Bank (SNB) all moved forward with rates that met market expectations.

The Riksbank stayed on hold at 2.25% and presented a flat rate path. We continue to expect the Riksbank will be on hold from here. Read more in our Riksbank - March 2025: Unchanged at 2.25% and flat policy rate path - as expected, 20 March.

The BoE kept the Bank Rate unchanged at 4.50%, with a hawkish vote split of 8-1 for unchanged (1 for cut). The central bank maintained its previous guidance noting that monetary policy will need to remain restrictive until risks to inflation returning to the 2% level have dissipated. Although the vote split was slightly to the hawkish side, nothing indicated a broad shift in sentiment within the MPC. We expect the next 25bp cut in May with the Bank Rate ending the year at 3.75%. While we have previously highlighted that we saw the risks skewed towards a swifter cutting cycle in 2025, we now see the risk picture as more balanced. See more in Bank of England Review - Slow and steady, 20 March.

The SNB delivered a 25bp cut, bringing the policy rate to 0.25%. Overall, the SNB stuck to its previous guidance noting that it "remains willing to be active in the foreign exchange market as necessary" and that the SNB "will adjust its monetary policy if necessary to ensure inflation remains within the range consistent with price stability over the medium term". While marginally adjusting the conditional inflation forecast upwards, the SNB signalled that risks are skewed to the downside for both the inflation and growth outlooks. We stick to our call of final cut to the policy rate of 25bp at the next meeting in June, which would bring the policy rate to 0%.

In the UK, the January/February jobs report met expectations. Wage growth excluding bonuses remained elevated at 5.9% and the unemployment rate likewise remained at 4.4% for the three months to January. The data supports the BoE's gradual approach to easing monetary conditions.

In Norway, the regional survey from Norges Bank showed capacity utilisation rising from 34 to 35. Both wage growth expectations and employment growth expectations marginally exceeded the central bank's own expectations, although wage growth expectations have decreased since the last survey- pointing towards a gradually disinflationary trend ahead.

Equities: Global equities were lower yesterday across regions, with cyclicals underperforming and yields moving lower. This occurred on a day with several policy meetings and important macroeconomic data releases. The monetary outcomes were very close to expectations, and the macroeconomic data, in our perspective, was very positive when considering all the signals. Hence, it is somewhat counterintuitive to see risky assets underperforming.

We are, of course, aware of the substantial political impact these days, and we could also attribute yesterday's lack of investor optimism to political factors. That being said, we observed the VIX moving lower, the MOVE index is far from its highs two weeks ago, and other asset classes are behaving well. Therefore, without the significant uncertainty related to politics, we should expect positive equity markets.

In the US yesterday, the Dow was down 0.03%, S&P 500 down 0.2%, Nasdaq down 0.3%, and Russell 2000 down 0.7%. Asian markets are mostly lower this morning, with Japan going against the trend. Again, there is no adverse macro data to highlight, rather the opposite, with fears of tariffs being mentioned as the reason for lower stock prices. US and European futures are marginally lower, suggesting volatility sliding further.

FI&FX: EUR/USD dropped below 1.09 yesterday on a day marked by sour risk sentiment in equity markets and declining bond yields. This development also benefitted the JPY, while CHF lost ground after the SNB cut interest rates. In Scandies, expectations of a Norges Bank rate cut next week were on retreat yesterday after the release of the Regional Network Survey, which further help NOK higher. The Riksbank kept interest rates unchanged.

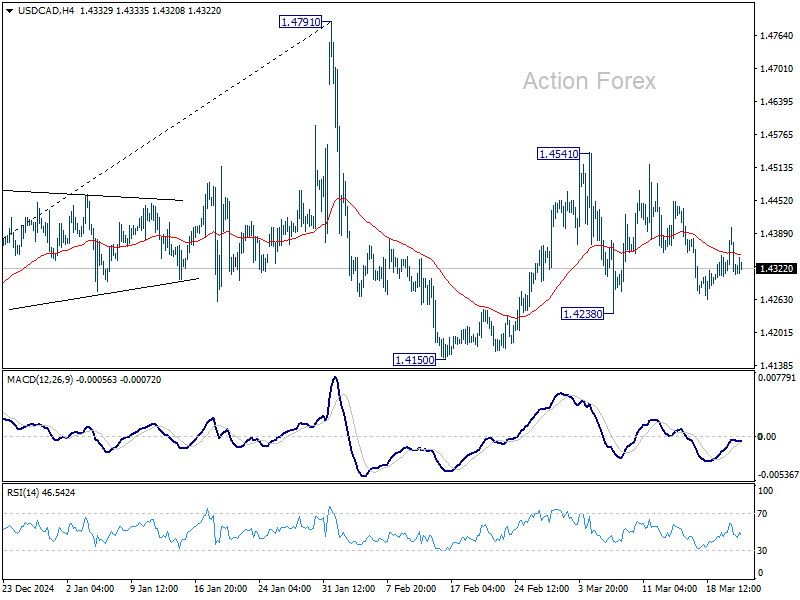

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4290; (P) 1.4346; (R1) 1.4379; More...

Intraday bias in USD/CAD remains neutral as range trading continues. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Dollar Recovery Remains Fragile While Bitcoin Struggles for Traction

Dollar continues to grapple with reversing its recent bearish trend, but momentum behind the rebound remains tentative at best. The greenback has received modest support from Fed’s stance, with policymakers emphasizing there’s no urgency to resume rate cuts. This, combined with a general reassessment of earlier bearish bets, has helped slow the pace of decline in Dollar, even as sentiment remains cautious.

One of the key themes driving recent market behavior has been the ongoing trade war narrative. Despite rising concerns about a recession in the US triggered by escalating tariffs, those fears have yet to materialize in hard data. Even Fed Chair Jerome Powell maintained a relatively balanced tone in this week’s FOMC press conference, holding back from sounding overly pessimistic. Traders may now be stepping back from aggressive short positions, waiting for more clarity—particularly around the reciprocal tariffs due in early April.

Looking across the currency markets, Yen is the worst performer so far this week, gaining little traction even after stronger-than-expected inflation data from Japan. Aussie follows, pressured by disappointing jobs data, while the Euro is beginning to consolidate gains following renewed optimism over the EU’s large-scale fiscal expansion plans. On the flip side, the Canadian Dollar surprisingly leads, despite Canada’s exposure to US tariffs, with Swiss Franc and Kiwi following Dollar and Sterling are relatively mixed, occupying the middle of the pack.

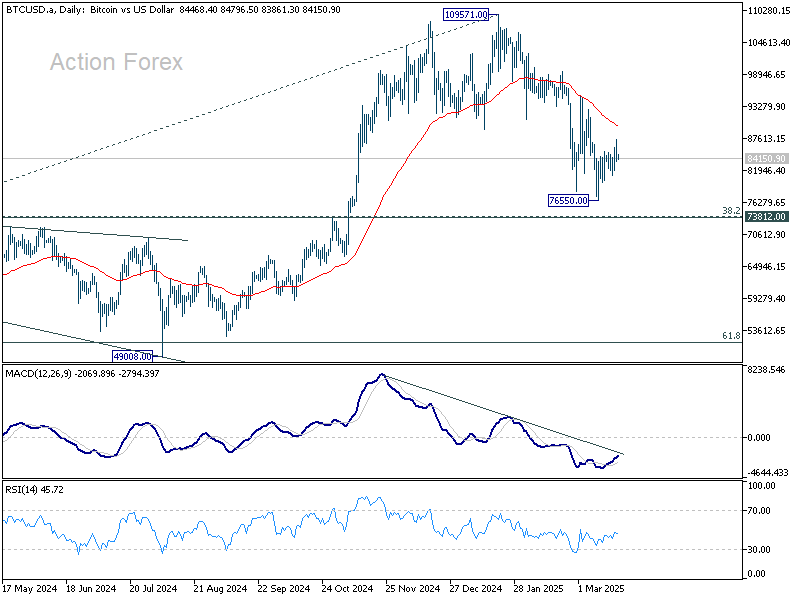

Meanwhile, Bitcoin’s recovery is showing signs of fatigue after hitting 87462 earlier in the week. President Donald Trump’s bold declaration that the US will become the global “undisputed Bitcoin superpower” at a recent crypto conference failed to spark meaningful market response. Despite the rhetoric, traders seem more focused on underlying technical and macroeconomic factors than political promises.

Nevertheless, technically, Bitcoin is still holding firmly above 73812 cluster support (38.2% retracement of 15452 to 109571 at 73617. The choppy decline from 109571 is viewed as a correction only. Firm break of 55 D EMA (now at 89980) will argue that the pullback has already completed, and bring stronger rebound back to retest 109571 high.

In Asia, Nikkei fell -0.20%. Hong Kong HSI is down -2.06%. China Shanghai SSE is down -1.29%. Singapore Strait Times is down -0.08%. Japan 10-year JGB yield fell -0.004 to 1.527. Overnight, DOW fell -0.03%. S&P 500 fell -0.22%. NASDAQ fell -0.33%. 10-year yield fell -0.023 to 4.233.

Japan’s CPI core slows less than expected to 3% in Feb

Japan’s core consumer inflation eased for the first time in four months in February, but less than market expectations. While the data strengthens the case for another BoJ rate hike at the April 30–May 1 meeting, policymakers may still choose to wait until July to better assess the impact of US tariff escalation and broader global financial market risks.

CPI core (excluding fresh food) slowed from 3.2% yoy to 3.0% yoy, slightly above expectations of 2.9%. The moderation was partly due to the resumption of government subsidies on utility bills. Despite this, core inflation has stayed above BoJ’s 2% target since April 2022.

More significantly, core-core CPI (excluding food and energy) rose from 2.5% yoy to 2.6% yoy, marking the fastest pace since March 2024. This continued strength in underlying inflation, even as services inflation softened slightly from 1.4% yoy to 1.3% yoy, reflects steady pass-through of higher labor costs.

Meanwhile, headline CPI slowed from 4.0% yoy to 3.7% yoy.

New Zealand posts NZD 510m trade surplus as exports surge across key markets

New Zealand posted a surprise trade surplus of NZD 510m in February, defying expectations of a NZD -235m deficit.

Goods exports jumped 16% yoy to NZD 6.7B, led by strong demand from key trading partners including China, Australia, and the EU. Notably, exports to China surged by 16% yoy, while shipments to Australia and the EU rose by 17% yoy and 37% yoy, respectively. The only major decline was seen in exports to the US, which slipped by -5.5% yoy.

Goods imports edged up a modest 2.1% yoy to NZD 6.2B, with notable volatility in country-level data. Imports from the US spiked 41% yoy, while those from South Korea plunged -57% yoy. Imports from Australia (-9.3% yoy) and the EU (-3.3% yoy)also declined. Despite the pickup from the US and China (3.8% yoy), subdued import figures from other regions helped tilt the trade balance into surplus.

BoC Governor: Crucial to Stop Initial Tariff Price Shocks from Becoming Generalized Inflation

Bank of Canada Governor Tiff Macklem issued a stark warning on the economic consequences of prolonged US tariffs, emphasizing that broad-based and long-lasting trade barriers will depress Canadian exports, reduce overall output, and push consumer prices higher.

In a speech overnight, Macklem noted that the unpredictability of US tariffs, marked by "constant policy reversals", has injected significant uncertainty into the outlook for Canadian businesses and households.

Macklem highlighted two major areas of concern: uncertainty about which tariffs will be imposed and for how long, and uncertainty about their economic impact.

Already, the BoC has observed that businesses are cutting back investment and hiring, and many households are growing more cautious with spending. He warned that if broad-based tariffs remain in place, the result will be "less demand, less economic growth and higher inflation".

While monetary policy cannot prevent the initial rise in prices caused by tariffs, Macklem stressed that it must act to "prevent those initial, direct price increases from spreading".

"We must ensure that higher prices from tariffs do not become ongoing generalized inflation," he emphasized.

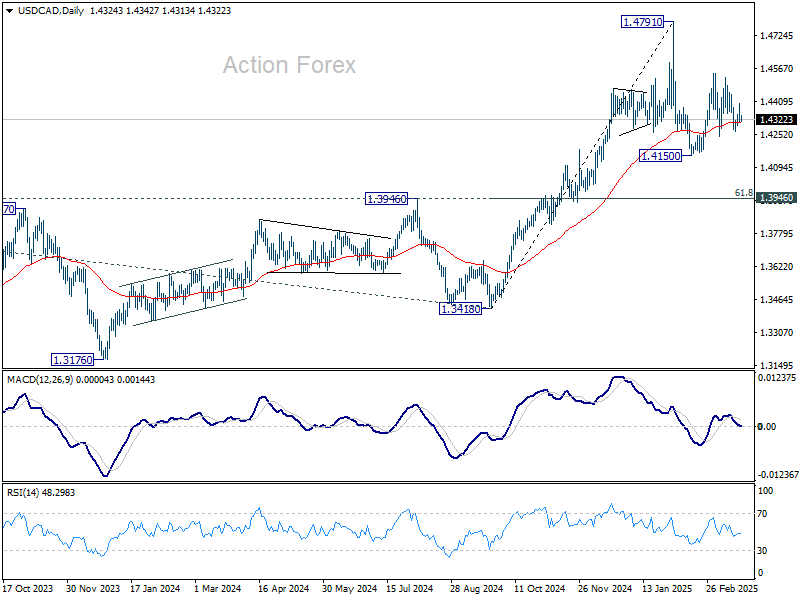

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4290; (P) 1.4346; (R1) 1.4379; More...

Intraday bias in USD/CAD remains neutral as range trading continues. On the downside, break of 1.4238 support will argue that corrective pattern from 1.4791 has started the third leg already. Intraday bias will be back on the downside for 1.4150 support and below. On the upside, though, break of 1.4541 will resume the rebound from 1.4150, as the second leg of the pattern.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Japan’s CPI core slows less than expected to 3% in Feb

Japan’s core consumer inflation eased for the first time in four months in February, but less than market expectations. While the data strengthens the case for another BoJ rate hike at the April 30–May 1 meeting, policymakers may still choose to wait until July to better assess the impact of US tariff escalation and broader global financial market risks.

CPI core (excluding fresh food) slowed from 3.2% yoy to 3.0% yoy, slightly above expectations of 2.9%. The moderation was partly due to the resumption of government subsidies on utility bills. Despite this, core inflation has stayed above BoJ’s 2% target since April 2022.

More significantly, core-core CPI (excluding food and energy) rose from 2.5% yoy to 2.6% yoy, marking the fastest pace since March 2024. This continued strength in underlying inflation, even as services inflation softened slightly from 1.4% yoy to 1.3% yoy, reflects steady pass-through of higher labor costs.

Meanwhile, headline CPI slowed from 4.0% yoy to 3.7% yoy.

Cliff Notes: Time to Take Stock

Key insights from the week that was.

In Australia, the February Labour Force Survey provided a major surprise relative to market expectations. The main result was a significant contraction in the size of the labour force, seeing the participation rate fall from 67.2% to 66.8% – declines of this magnitude having only occurred in 11 out of the 564 months the survey has been conducted. This appeared as a –52.8k decline in the level of employment. Given these individuals left the labour market entirely, measures of labour market slack were broadly unchanged. Indeed, if anything, they tightened at the margin, the unemployment rate on the cusp of rounding down to 4.0% and the underemployment rate falling to 5.9%.

The ABS offered some more colour in the media release, stating that there were “[f]ewer older workers returning to work” and “higher levels of retirement in Australia over recent months”; while in contrast, “we continue to see growth in employment for people aged 15 to 54.” With this context, falling participation can have a variety of interpretations. One prominent explanation is that, with cost-of-living pressures having moderated, older workers that were pulled into the labour market to support household incomes under pressure are now starting to leave. It could also be interpreted as a signal of easing labour demand, although elevated job vacancies cast doubt over this view.

Either way, the scale of the decline in the month suggests some one-off factors are at play; we will have to wait until next week for more data to confirm the outcomes across age brackets. Until then, the RBA are unlikely to read too much into the latest result. Given the key measures of labour market slack are still consistent with a tight labour market, the Board will remain focused on the inflation and wage trends.

With limited new data, Chief Economist Luci Ellis’ essay this week investigates the evolution of structural trends and market psychology. Ahead of next Tuesday’s Federal Budget 2025-26, Chief Economist Luci Ellis' video update focuses on the fiscal dynamics at play and likely policy priorities.

New Zealand GDP provided a detailed update of activity across the Tasman. The 0.7% gain was welcome following two quarters of decline. As discussed by our NZ economics team, arguably the result overstates growth in the quarter owing to some technical issues. Still, there were some genuine positives in the detail, and the economy is expected to continue growing through 2025, albeit most likely at a below-trend pace. This outlook supports NZ economics’ view that the RBNZ cash rate will trough at 3.25% in coming months.

Moving further afield, policy makers’ actions were again the focus as the FOMC, Bank of England and Bank of Japan met.

The FOMC kept the fed funds rate unchanged as expected at their March meeting while making the “technical” decision “to slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $25 billion to $5 billion [from April]”. Chair Powell noted in the press conference that this decision followed some evidence of “tightness in money markets” and has no implications for the stance of monetary policy. Changes to the forecasts were more telling on the policy outlook.

On GDP, the 2025 forecast has been revised from 2.1%yr at December to 1.7%yr in March. The range of Committee forecasts is also now heavily skewed to the downside. For 2025 and 2026, the low of the range has shifted from 1.6%yr in December to 1.0%yr and 1.4%yr to 0.6%yr respectively. The FOMC’s initial take on the inflation effect of tariffs meanwhile suggests pressures will be contained and temporary, the core PCE forecast for 2025 revised up from 2.5%yr to 2.8%yr while projections for 2026 and 2027 were left unchanged at 2.2%yr and 2.0%yr. The range of Committee core PCE forecasts remain wide and biased up, however. The top end only edges lower from 3.5%yr in 2025 to 3.2%yr in 2026, then 2.9%yr in 2027.

Just as the FOMC must assess the net economic effect of policy change across trade, immigration and regulation, they also are intent on setting policy to suit the balance of risks across inflation, the labour market and demand. The unchanged fed funds rate projection from December – including 50bps of cuts forecast by end-2025, another 50bps in 2026 and one more cut come 2027 – suggests their view changes are largely offsetting. Our modestly weaker growth view for 2025 warrants the two cuts forecast by the FOMC in 2025, but we then expect the Committee to hold at 3.875% as tariff inflation effects linger and capacity constraints also buoy consumer inflation.

The Bank of England's decision to remain on hold in March was subsequently decided 8-to-1, the dissenter favouring a 25bp cut. "Domestic price and wage pressures are moderating, but remain somewhat elevated". "The Committee will continue to monitor closely the risks of inflation persistence and what the evidence may reveal about the balance between aggregate supply and demand in the economy. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further." Like the FOMC, the Bank of England clearly intends to determine policy meeting-by-meeting based on incoming data.

In the middle of a rate hiking cycle, in contrast to the FOMC and BoE, the Bank of Japan also held steady in March. Post-meeting communications highlighted concern over the implications of US tariffs for global economic activity; but the BoJ continued to show confidence in the domestic economy, recent activity data having been broadly in line with expectations and the wage data modestly above. Yen weakness on the BoJ decision was short lived, USD/JPY holding to a JPY148-150 range since, as has been the case for most of the past month. On the outlook for wages, trade confederation RENGO announced at the end of last week that it had secured a 5.46% wage increase against a 6.0% demand, exceeding the FY24 outcome of 5.28%. The caveat here is that the survey mostly reflects large businesses which have a greater capacity to fund wage increases. With inflation anticipated to remain elevated versus history, its important wage gains continue to be seen broadly across both big business and small. Such a trend will help shore up consumer confidence and sustain spending growth, allowing the BoJ to continue hiking to around 1.0%.

Economic data released outside of Australia and New Zealand this week was of little consequence for the outlook. The latest data round from China is worthy of study, however. The February data was the first major release for the calendar year, given the variable timing of lunar new year holidays year-to-year. On the consumer, the update was favourable, retail sales growth accelerating from 3.5%ytd in December to 4.0%ytd. Fixed asset investment also surpassed expectations, accelerating from 3.2%ytd in December to 4.1%ytd currently despite entrenched weakness in property investment, -9.8%ytd in February. Month-on-month price declines accelerated for new and existing homes in February, making clear the need for additional concerted action by authorities. Thankfully, this looks to be forthcoming, authorities making clear at the beginning of the week that new initiatives to strengthen employment, income and social security were being finalised for implementation in 2025. Additional aid for the housing sector is also progressing. 2025 therefore promises to be a much better year for Chinese consumer demand than 2024 or 2023, particularly with equities continuing to rally and key sub-sectors of private industry, such as technology, being encouraged to accelerate development and expansion. A full view of our outlook for China can be found in the recently released March Market Outlook.

New Zealand posts NZD 510m trade surplus as exports surge across key markets

New Zealand posted a surprise trade surplus of NZD 510m in February, defying expectations of a NZD -235m deficit.

Goods exports jumped 16% yoy to NZD 6.7B, led by strong demand from key trading partners including China, Australia, and the EU. Notably, exports to China surged by 16% yoy, while shipments to Australia and the EU rose by 17% yoy and 37% yoy, respectively. The only major decline was seen in exports to the US, which slipped by -5.5% yoy.

Goods imports edged up a modest 2.1% yoy to NZD 6.2B, with notable volatility in country-level data. Imports from the US spiked 41% yoy, while those from South Korea plunged -57% yoy. Imports from Australia (-9.3% yoy) and the EU (-3.3% yoy)also declined. Despite the pickup from the US and China (3.8% yoy), subdued import figures from other regions helped tilt the trade balance into surplus.

When It All Unravels

Big trends win out in the end. New realities can take time to emerge, but when they do, things can break quickly. The US outlook is a case in point.

When we commented back in January that ‘Higher interest rates and a seemingly overvalued exchange rate. One can’t help thinking that reality will bite the US exceptionalism narrative sooner or later.’, we did not expect some of that reckoning to come so soon. The shift in sentiment – and its speed – illustrate two key features of a world shaped by evolving trends.

First, big trends win out in the end. The world changes, and anything that is not compatible with the evolving trend will eventually need to adjust to be in line with it.

Second, when the current reality rests in large part on people’s beliefs and behaviour, then the timing of a shift to be compatible with the new reality will be hard to predict. But when it happens, it can happen quickly. The collapse of communism in a so-called ‘preference falsification cascade’ is the canonical example. The shifting US narrative is a double-bump version of the same mechanism. First came the ‘vibe shift’ break from the prevailing sociopolitical norms following the election, and then the break of the US exceptionalism narrative in recent weeks. We don’t see that narrative coming back.

Moore’s law galore

One of the elements of the US exceptionalism narrative had been a bullish view of US dominance in AI and crypto, spurred on by actual and expected policy announcements. The presumption had been that the US would have an unassailable first-mover advantage. Its deep capital markets and depth of engineering talent complemented the access to data advantages of a handful of US-headquartered firms. DeepSeek’s release of its AI chatbot – particularly the decision to release the technology as open source – punctured that bubble. Yet an understanding of the economics of technological progress would tell you not to have believed in an unassailable advantage in the first place.

It is in the nature of technologies in the early, rapid phase of development that costs and prices decline quickly as technology advances. Compute-intensive technologies are especially vulnerable to this dynamic because of Moore’s Law, the empirical regularity that chips’ computing power doubles roughly every two years.

It is also in the nature of compute-intensive technologies that advances can sometimes occur in leaps. When your product is purely algorithmic, you are vulnerable to someone else coming along with a better algorithm, cutting costs and prices by an order of magnitude in the process.

Electricity shock treatment

This combination of rapid cost decline and occasional big leaps is not confined to obviously computer-oriented technologies. Genomics is another example: recall that the Human Genome Project cost about $US2.7 billion back in 2000 to sequence a single human genome. Nowadays, that cost is about $US1000, and people in the field talk about the $100 genome being not far off. Part of that cost decline lines up with Moore’s Law, but there have clearly also been some big leaps along the way. While this might seem like an esoteric example, the potential implications for health outcomes are profound.

An example with more obviously pervasive implications comes from the energy sector. The relative cost of renewable generation technologies continues to decline. And while some of the costs of different energy sources are a policy choice – think approval processes and safety standards – the underlying driver of this relative cost shift is technological.

Relatedly, it is easy to forget that technological progress also improves the efficiency of energy consumption. If you do, you can end up overcooking your forecasts of future energy demand (see Figure 5.1 in the Finkel Report, for example). New appliances are typically more energy efficient: for example, a new washing machine typically consumes about half the electricity used by a 15-year-old model. Improvements in insulation, logistics planning and other activities also matter. Here, too, there are the occasional leaps, such as the switch from halogen to LED, lowering energy consumption for lighting by an order of magnitude.

The exponential trends that emerge from these technological drivers are among the underpinnings of the adage that people overestimate the change that will occur over the next couple of years but underestimate the change that will occur over the next ten years.

If, suddenly, there is an alternative

The dynamics of technological change should have led to more scepticism about the technological elements of the US exceptionalism narrative. The financial market context has a similar ‘this can’t last’ flavour.

The US dollar is overvalued. That is the big trend that will win out. History would suggest that periods of exchange rate overvaluation eventually correct via depreciation, though it can take a few years. It is essentially impossible to say exactly when the next leg down will occur, especially as fiscal trends imply US rate differentials are likely to at least partly compensate for the growth risks. This overvaluation could therefore persist for a while, just not forever.

Another reason why the US dollar can stay overvalued for a while is that investors have a bit of a TINA problem: There Is No Alternative to US Treasuries. Investors feeling nervous about the prospect of a significant depreciation of USD-denominated assets over the next few years would need to invest in something else. So far, though, no other low-risk asset class has the size and depth of the US Treasury market that would allow it to be that alternative.

This is why some of the recent shifts in policy in Europe could have profound implications. European sovereign bonds are currently fragmented with different risks and circumstances. If that fragmentation were to diminish, European sovereign bonds would all be of comparable credit standing. Indeed, a structural shift in European debt dynamics could be underway already. Consider the growing issuance of pan-European bonds by the European Commission, the collective move to raise and co-ordinate defence spending across the continent, and success in narrowing fiscal divergences between member nations. If investors gain confidence in this longer-term evolution, we could see attitudes shift towards treating European bonds more like a single, deeper market – and thus a true alternative to Treasuries.

As recent weeks have shown, when human collective beliefs and decisions are involved, things can unravel much sooner and faster than you think.

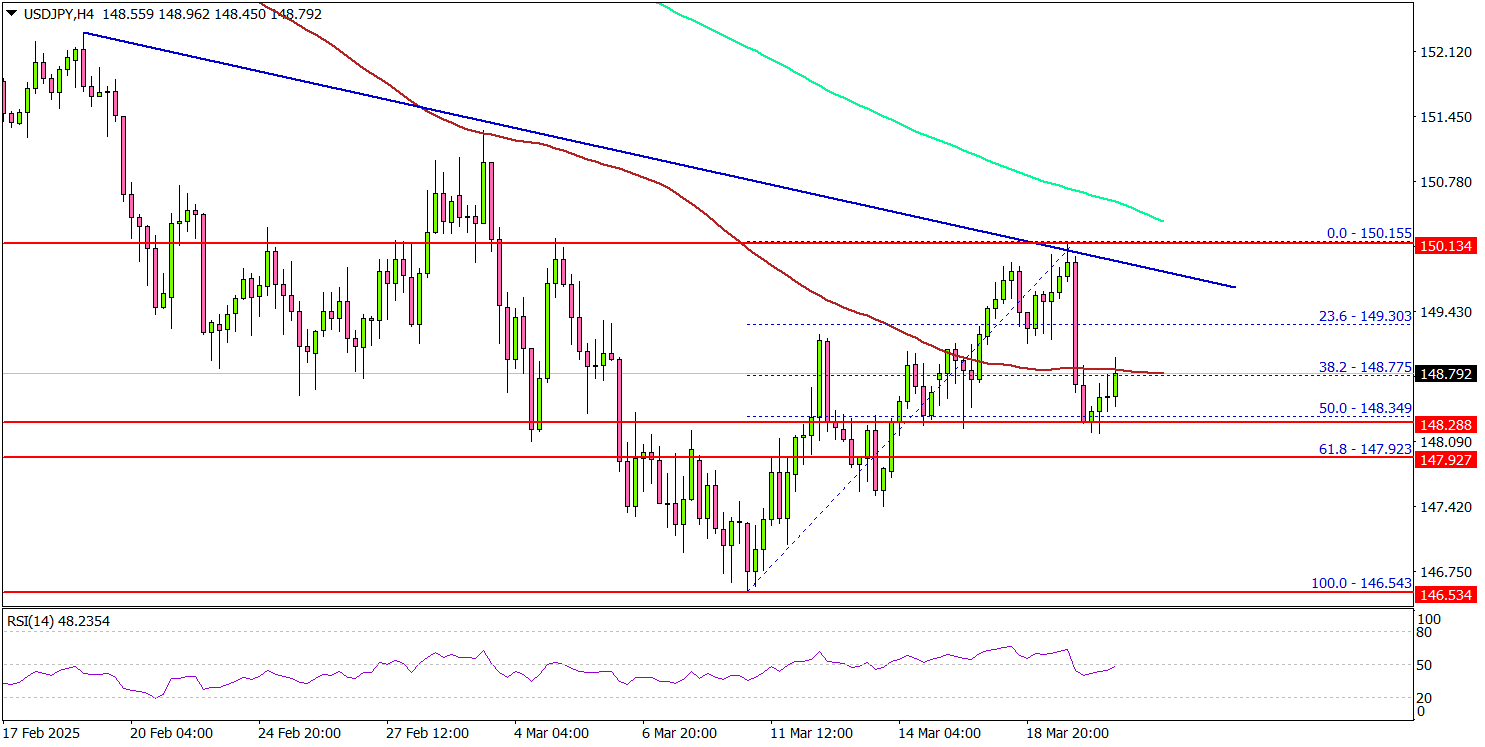

USD/JPY Faces Obstacles on The Path Higher

Key Highlights

- USD/JPY struggled to continue higher above the 150.15 level.

- A connecting bearish trend line is forming with resistance at 150.00 on the 4-hour chart.

- GBP/USD could gain pace for a move above the 1.3000 resistance.

- Gold surged to another record high above the $3,040 zone.

USD/JPY Technical Analysis

The US Dollar declined heavily below the 152.00 level against the Swiss Franc. USD/JPY even spiked toward 146.50 before it found some support.

Looking at the 4-hour chart, the pair recovered some losses and traded above the 148.50 level. However, the bears were active near the 150.00 zone. A high was formed at 150.15 and the pair corrected lower.

There is also a connecting bearish trend line forming with resistance at 150.00 on the same chart. The pair remained below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the upside, the pair is facing resistance near the 149.20 level. The next major resistance is near the 149.50 level. The main resistance is now forming near the 150.00 zone.

A close above the 150.00 level could set the tone for another increase. In the stated case, the pair could even clear the 151.20 resistance.

On the downside, immediate support sits near the 148.00 level. The next key support sits near the 147.40 level. Any more losses could send the pair toward the 146.50 level.

Looking at GBP/USD, the pair remains supported and might aim for a move above the 1.3000 resistance zone.

Upcoming Economic Events:

- Fed's Williams speech.