Sample Category Title

China’s inflation turns negative, but seasonal factors skew the picture

Released over the weekend, China’s consumer inflation dipped into negative territory for the first time in over a year, with February’s CPI coming in at -0.7% yoy, weaker than the expected -0.5% yoy, and a sharp reversal from January’s 0.5% yoy gain.

Core CPI, which strips out food and energy prices, also slipped by -0.1% yoy—its first decline since January 2021—signaling weak underlying demand.

On a month-over-month basis, consumer prices fell -0.2%, more than the expected -0.1%, reversing some of January’s 0.7% increase.

While the decline may raise concerns about deflationary pressures, NBS attributed much of the drop to seasonal distortions tied to the timing of the Lunar New Year. Stripping out this factor, NBS estimates that CPI actually rose 0.1% yoy.

Given these distortions, a clearer picture of China’s inflation trajectory will likely emerge in March when seasonal effects fade.

Meanwhile, producer prices remained in contraction for the 29th consecutive month, with PPU declining -2.2% yoy, slightly better than January’s -2.3% yoy but still below expectations of -2.1% yoy.

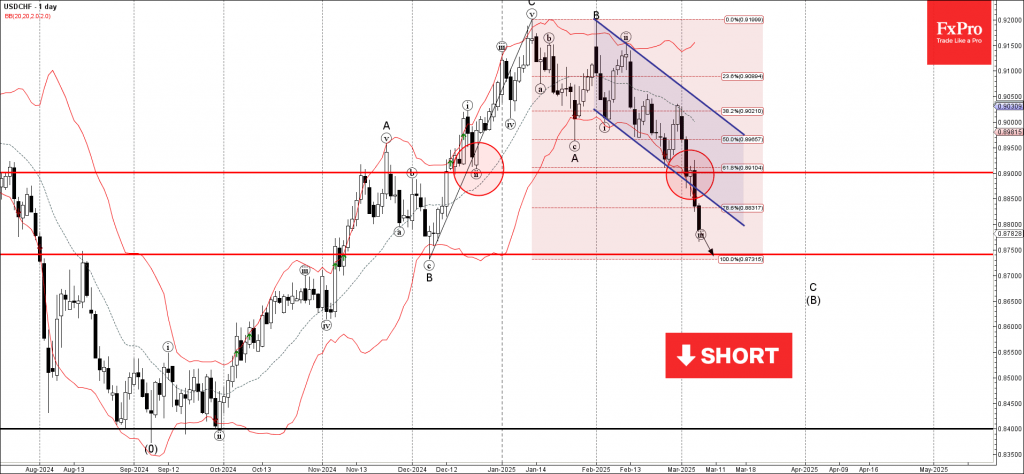

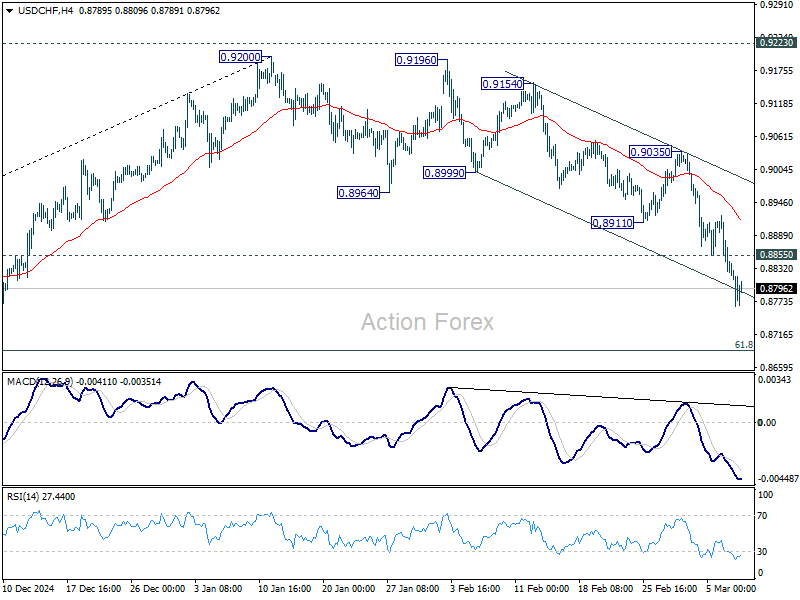

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF broke the support zone

- Likely to fall to support level 0.8750

USDCHF currency pair recently broke the support zone between the support level 0.8900 (which has been reversing the price from December), the support trendline of the daily down channel from January and the 61.8% Fibonacci correction of the upward impulse from December.

The breakout of this support zone accelerated the active strong downward impulse wave C of the ABC correction (B) from January.

USDCHF currency pair can be expected to fall further to the next support level 0.8750 (the monthly low from December and the target for the completion of wave C).

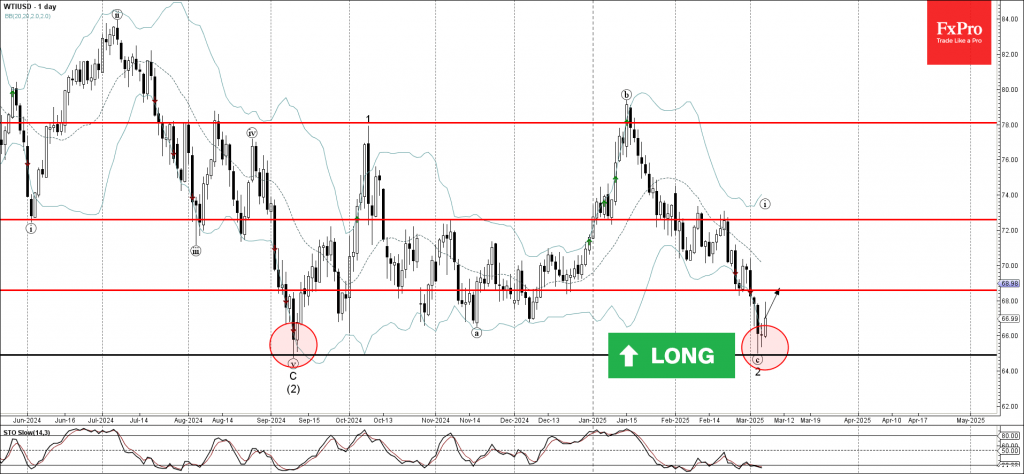

WTI Crude Oil Wave Analysis

WTI crude oil: ⬆️ Buy

- WTI reversed from the multi-month support level 64.90

- Likely to rise to resistance level 68.60

WTI crude oil recently reversed sharply from the powerful multi-month support level 64.90, which stopped the previous sharp downtrend at the start of September.

The upward reversal from the support level 64.90 will likely form the daily Japanese candlesticks reversal pattern Morning Star Doji.

Given the strength of the support level 64.90 and the oversold daily Stochastic, WTI crude oil can be expected to rise further to the next resistance level 68.60.

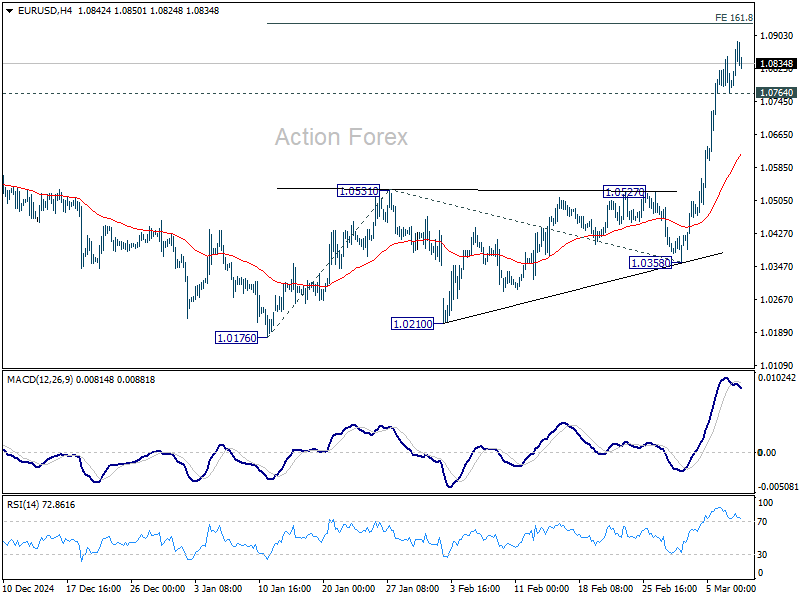

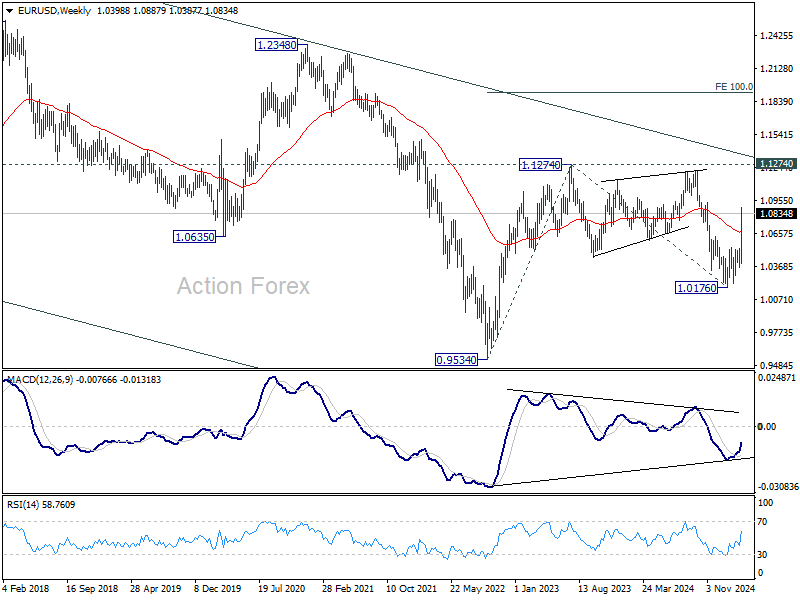

EUR/USD Weekly Outlook

EUR/USD's rebound from 1.0176 resumed last week with strong upside acceleration. Initial bias stays on the upside this week for 161.8% projection of 1.0176 to 1.0531 from 1.0358 at 1.0932. Firm break there will pave the way back to 1.1274 key resistance next. On the downside, below 1.0764 minor support will turn bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

In the long term picture, the case of long term bullish reversal is building up. Sustained break of falling channel resistance (now at around 1.1400) will argue that the down trend from 1.6039 (2008 high) has completed at 0.9534. A medium term up trend should then follow even as a corrective move. Nevertheless, rejection by the channel resistance will keep outlook bearish.

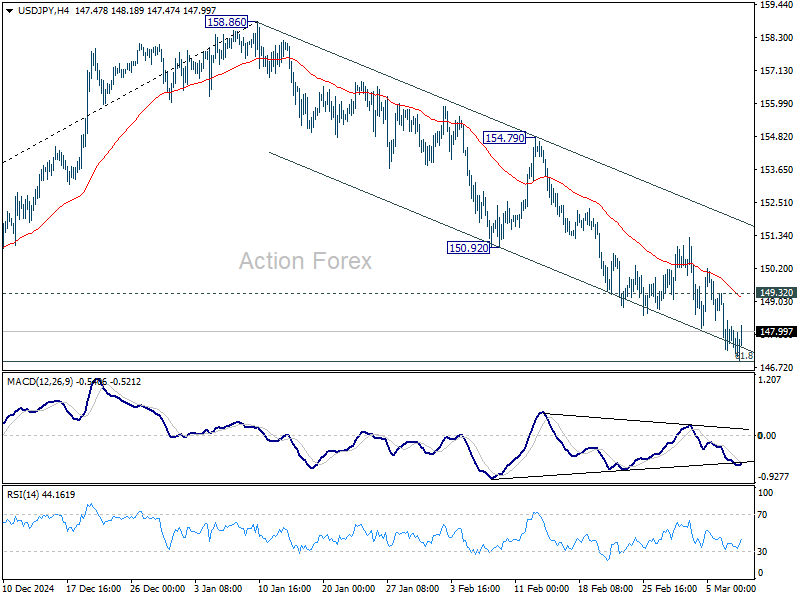

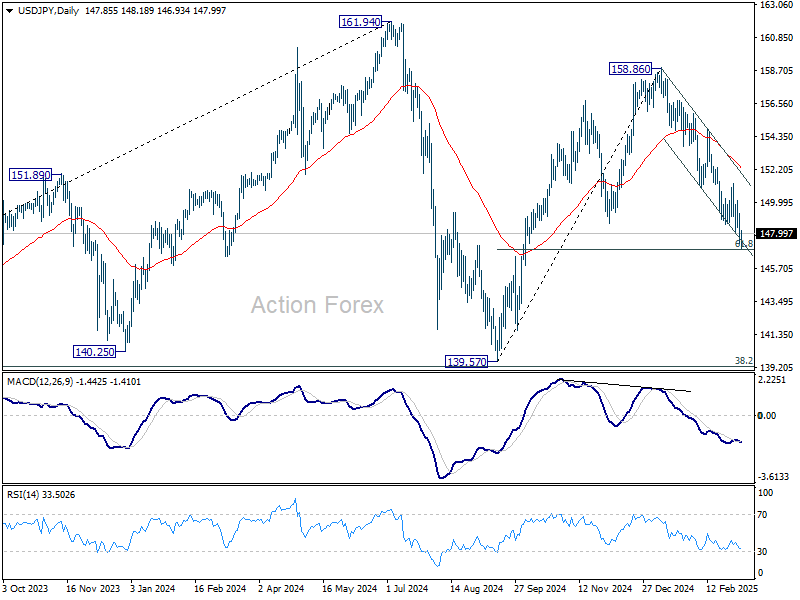

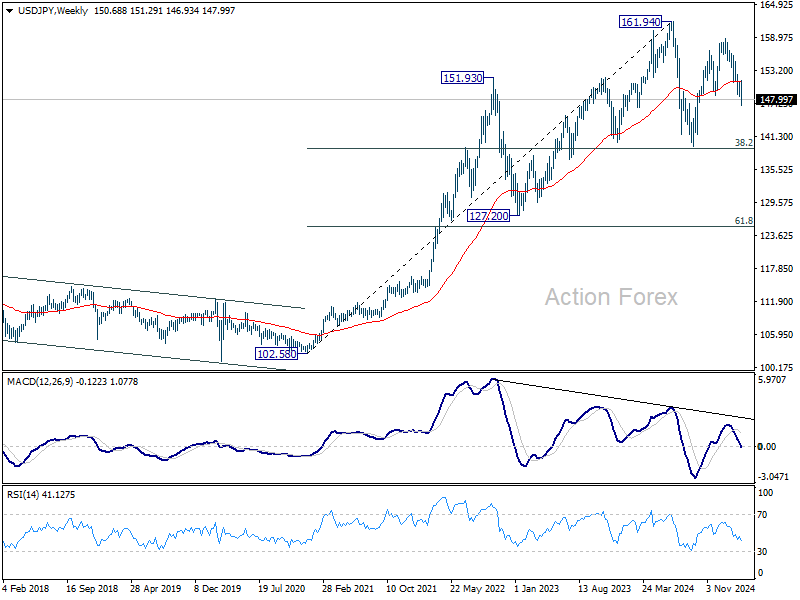

USD/JPY Weekly Outlook

USD/JPY's fall from 158.86 extended lower last week but downside momentum was somewhat limited by near term falling channel. Still, initial bias stays on the downside this week. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. On the upside, 149.32 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. A medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 136.88).

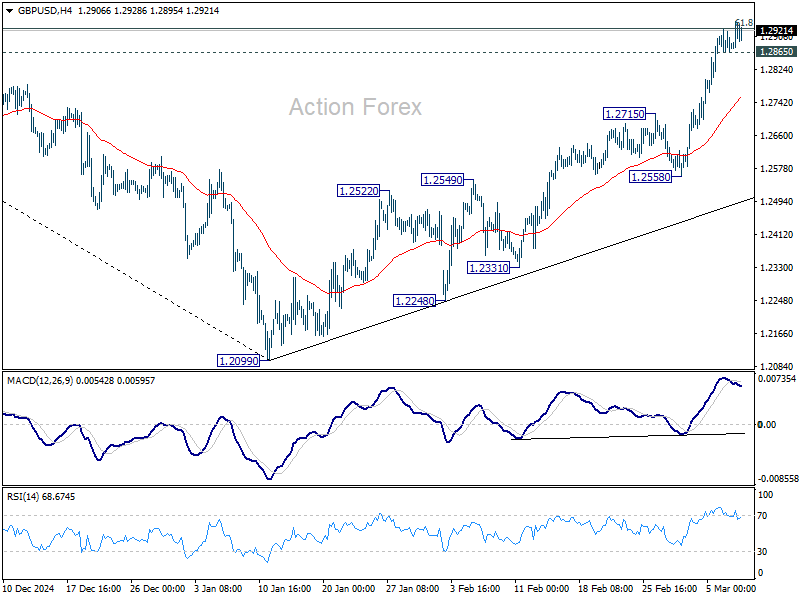

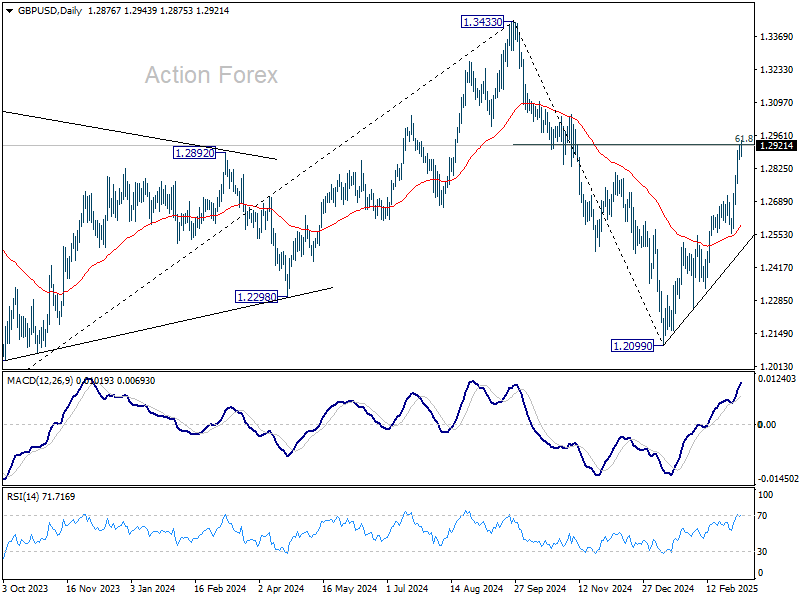

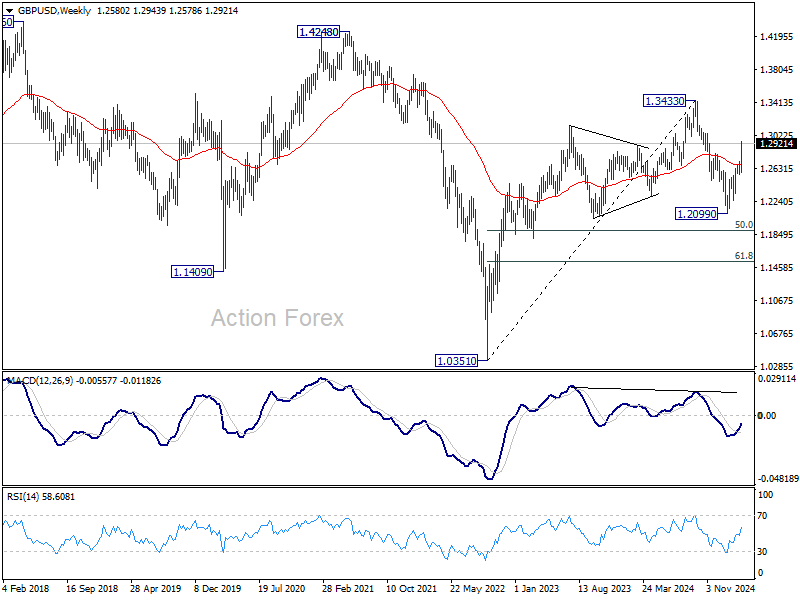

GBP/USD Weekly Outlook

GBP/USD's rally from 1.2099 resumed last week and the development argues that fall from 1.3433 has already completed. Initial bias stays on the upside this week. Sustained break of 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high. On the downside, below 1.2865 minor support will turn intraday bias neutral again and bring consolidations.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

In the long term picture, price actions from 1.0351 (2022 low) are seen as a corrective pattern to the long term down trend from 2.1161 (2007 high) only. Outlook will be neutral at best as long as 1.4248 structural resistance holds, even in case of strong rebound.

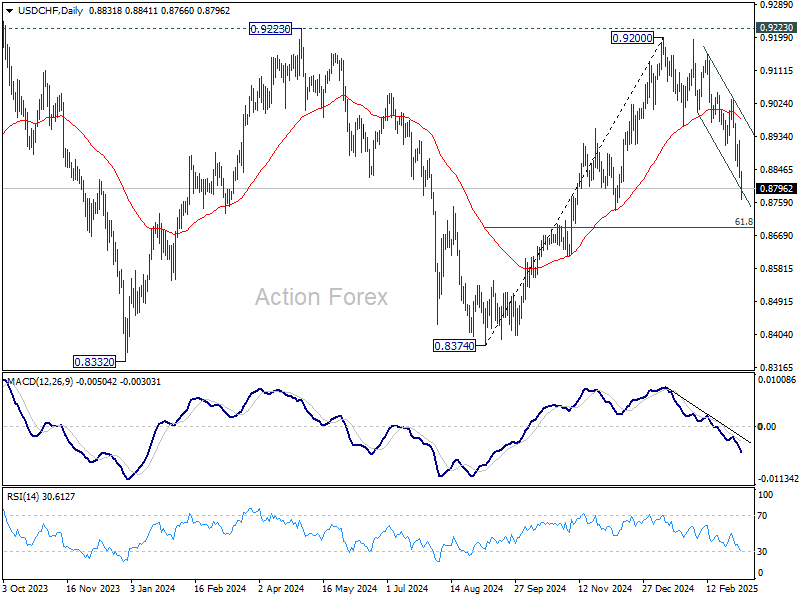

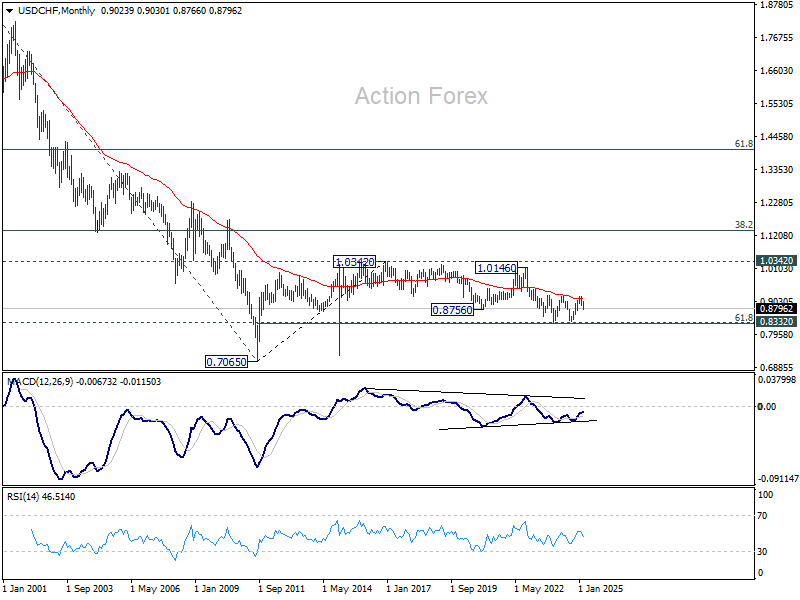

USD/CHF Weekly Outlook

USD/CHF's extended decline last week indicates that rise from 0.8374 has already completed at 0.9200, after rejection by 0.9223 key resistance. Initial bias stays on the downside this week for 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support. On the upside, above 0.8855 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Sustained break of 55 M EMA (now at 0.9115) will indicate that the third leg has already started. However, rejection by 55 M EMA again, followed by break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317, will pave the way back to 0.7065.

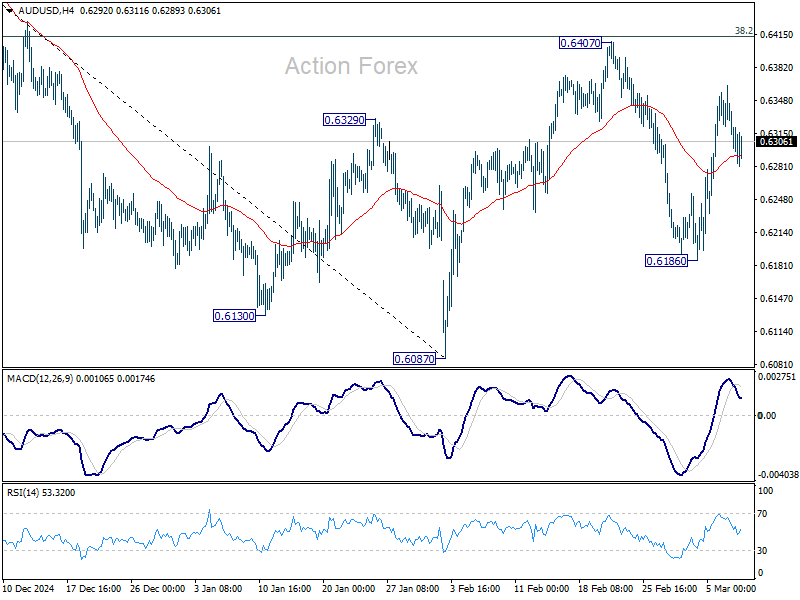

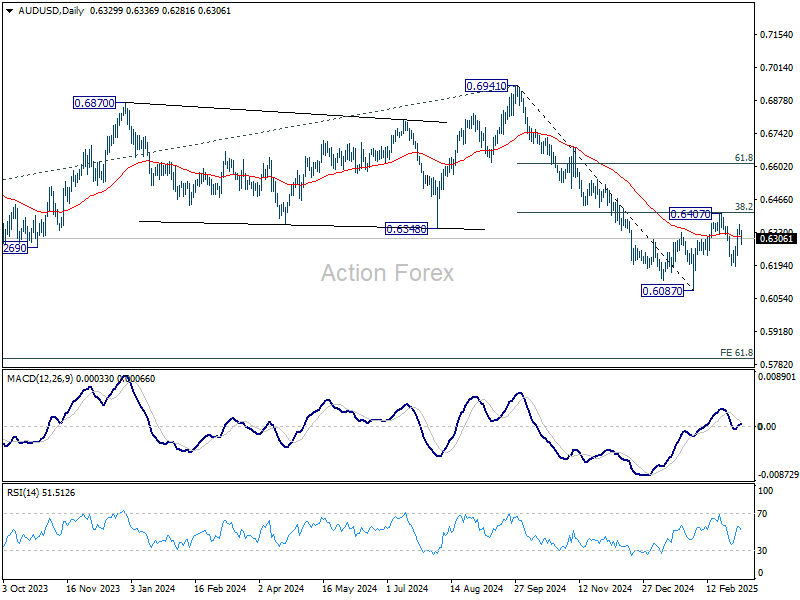

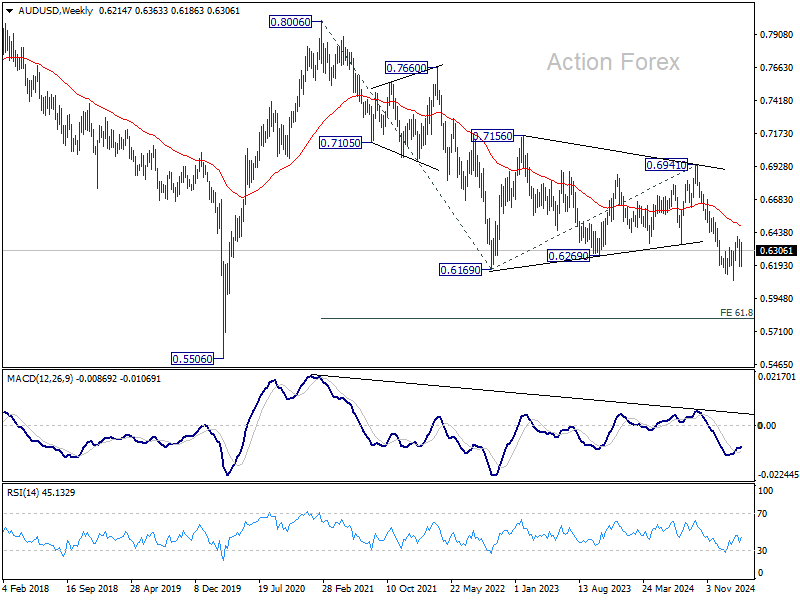

AUD/USD Weekly Report

AUD/USD's strong rebound last week mixed up the near term outlook. Initial bias stays neutral this week first. On the downside, break of 0.6186 will target 0.6087 support first. Firm break there will resume whole decline from 0.6941. However, sustained trading above 38.2% retracement of 0.6941 to 0.6087 at 0.6413 will raise the chance of near term bullish reversal, and target 61.8% retracement at 0.6615 next.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6487) holds.

In the long term picture, prior rejection by 55 M EMA (now at 0.6823) is taken as a bearish signal. But for now, fall from 0.8006 is still seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper fall, strong support should emerge above 0.5506 to contain downside to bring reversal. However, this view is subject to adjustment if current decline accelerates further.

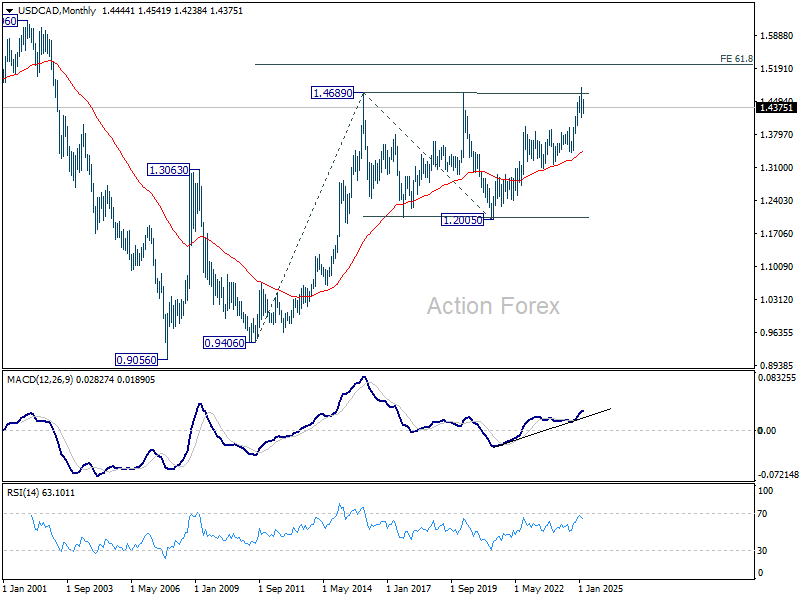

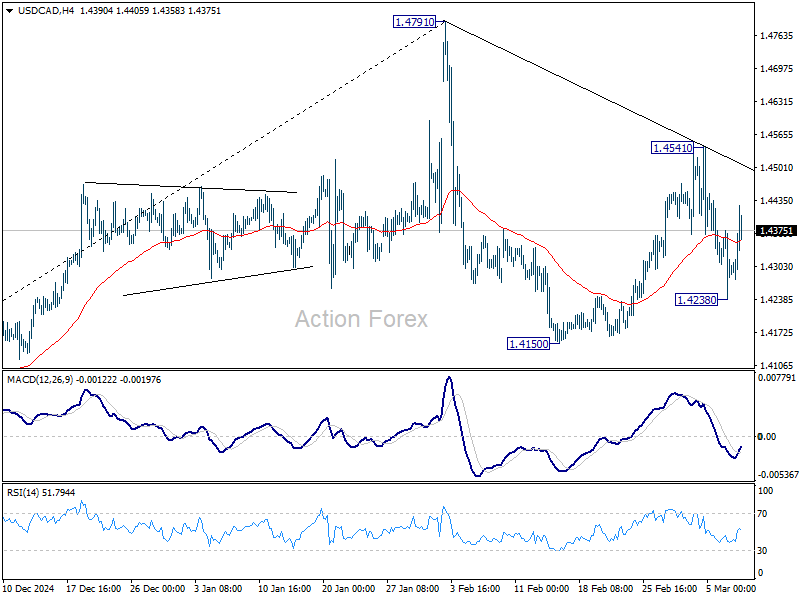

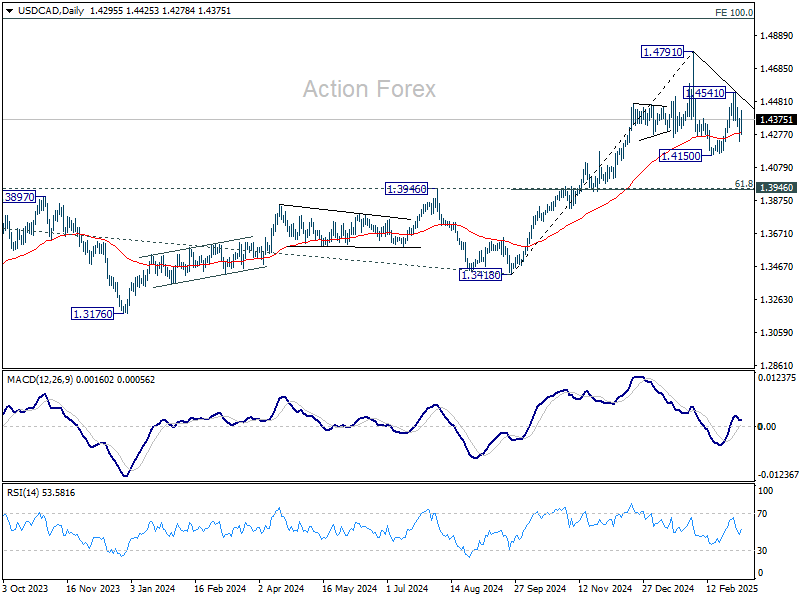

USD/CAD Weekly Outlook

USD/CAD reversed after edging higher to 1.4541 last week but subsequent decline was contained at 1.4238. Initial bias is turned neutral this week first. Overall, corrective pattern from 1.4791 should still be extending. Below 1.3248 will target 1.4150 support and possibly below. Meanwhile, break of 1.4541 will bring stronger rise back to retest 1.4791.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

In the longer term picture, up trend from 0.9506 (2007 low) is in progress and possibly resuming. Next target is 61.8% projections of 0.9406 to 1.4689 from 1.2005 at 1.5270. While rejection by 1.4689 will delay the bullish case, further rally will remain in favor as long as 55 M EMA (1.3430) holds.