Sample Category Title

British Pound Edges Higher, Investors Eye ADP Employment Report

The British pound has posted gains on Tuesday, continuing the upward movement seen on Monday. In North American trade, GBP/USD is trading at 1.3884, up 0.26% on the day. In economic news, there are no major indicators in the US or the UK. In the US, Factory Orders were unexpectedly soft, with a decline of 1.4%. This was well short of the estimate of -0.4%. On Wednesday, the US releases ADP Nonfarm Employment Change.

Tensions are growing between London and Brussels as the Brexit deadline of March 2019 looms ever closer. Last week, there were sharp exchanges between the two sides after the EU releases a draft of the legal framework of the Brexit agreement. On Friday, Prime Minister May outlined her vision of relations between the EU and Britain after Brexit. May sought to lower the recent sharp rhetoric surrounding Brexit, saying that both sides needed to show flexibility in order to reach an agreement. May said that she was seeking a free trade agreement with the EU that included financial services. The response from Brussels has been lukewarm, with some policymakers saying that Britain continues to operate under the illusion that it can leave the club but still enjoy the benefits.

Over in the US, the “tariff tussle” shows no sign of being resolved anytime soon. US President Trump appears set on applying stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week sent the dollar broadly lower, and if the tariffs are introduced, negative investor sentiment could send the greenback to lower levels.

25000 too much for DOW? Mnuchin backs tariffs

25000 proves to be too much for DOW? It opened higher and hit as high as 24995.24. But stocks seem to response negatively to Treasurer Steve Mnuchin's backing on steel and aluminum tariffs. Mnuchin said in House:

- Regarding Trump's tariffs - "I am supportive of them and I am supportive of the mechanisms that the president has announced,"

- “To the extent that we’re successful in renegotiating Nafta, those tariffs won’t apply to Mexico and Canada.” (same position as Trump)

- "We're not looking to get into trade wars."

- "We're looking to make sure that U.S. companies can compete fairly around the world."

- He brought up China too. (?!) "President Trump has been very clear: We want to make sure U.S. companies have the same ability to do business in China as Chinese companies have here."

- And, "our priority at the moment is to renegotiate NAFTA and to focus on our trade relationships with China and have fair and balanced trade with China."

Facts: China is the 11th imports of steel to US in 2017. India ranked 10 with contribution merely 2%. Canada was top at 16%, Mexico 4th at 9%.

Japanese Yen Ticks Higher, GDP Next

The Japanese yen has posted small gains in the Tuesday session. In North American trade, USD/JPY is trading at 106.17, down 0.03% on the day. On the release front, there are no Japanese indicators on the schedule. In the US, Factory Orders were unexpectedly soft, with a decline of 1.4%. This was well short of the estimate of -0.4%. On Wednesday, the US releases ADP Nonfarm Employment Change and Japan publishes Final GDP.

The Japanese yen continues to look strong, and last week, the dollar dropped close to the 105 line, its lowest level since early November. The yen received a boost on Friday, as Bank of Japan Governor Haruhiko Kuroda said that the BoJ would consider exiting from its ultra-accommodative monetary policy if its inflation target of around 2020 was reached in early 2020. Kuroda’s remarks were unusual in that they mentioned a possible “exit” from its stimulus program, and this caught the markets off guard. The BoJ has been lagging behind the Fed and other central banks in winding up stimulus, but Kuroda added that the Bank would normalize policy if “economic conditions become favorable and our price target is achieved”. Although inflation remains well below target, any further hints about normalization from the BoJ could strengthen the yen.

The “tariff tussle” shows no sign of being resolved anytime soon. US President Trump appears set on applying stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs last week bolstered the yen, and if the tariffs are introduced, negative investor sentiment could send the greenback to lower levels.

BoJ Meets with Yen Trading at Elevated Levels; Japan’s Revised GDP Numbers also Due

The Bank of Japan will be concluding its meeting on monetary policy on Friday, with a decision on rates being made public at 0400 GMT. Markets project the Bank to maintain its ultra-easy monetary policies firmly in place. However, despite no change being expected, the meeting is gathering more attention than past ones on the back of mounting speculation that the Japanese central bank is preparing the ground for an exit from ultra-loose policies, something which has allowed the yen to post notable gains relative to other majors so far in 2018.

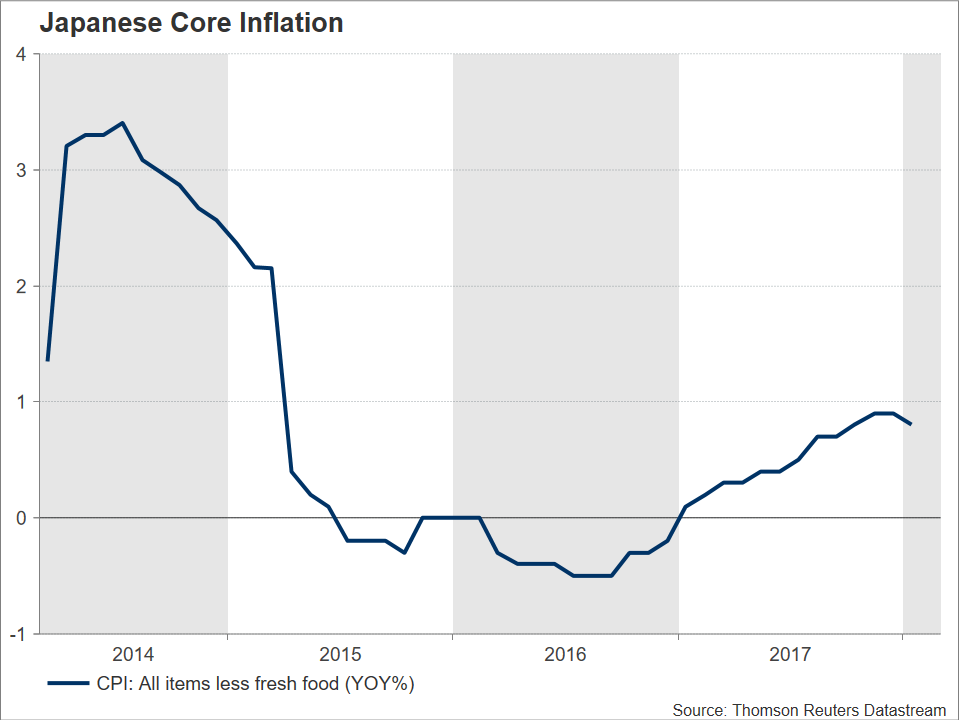

Japan’s central bank is anticipated to keep its short-term interest rate unchanged at -0.1% and continue to target the yield of 10-year Japanese government bonds with the scope of maintaining it around 0% in the face of core inflation – the measure that includes oil products but excludes volatile fresh food items and which is targeted by the Japanese central bank – well undershooting the Bank’s annual target of 2%.

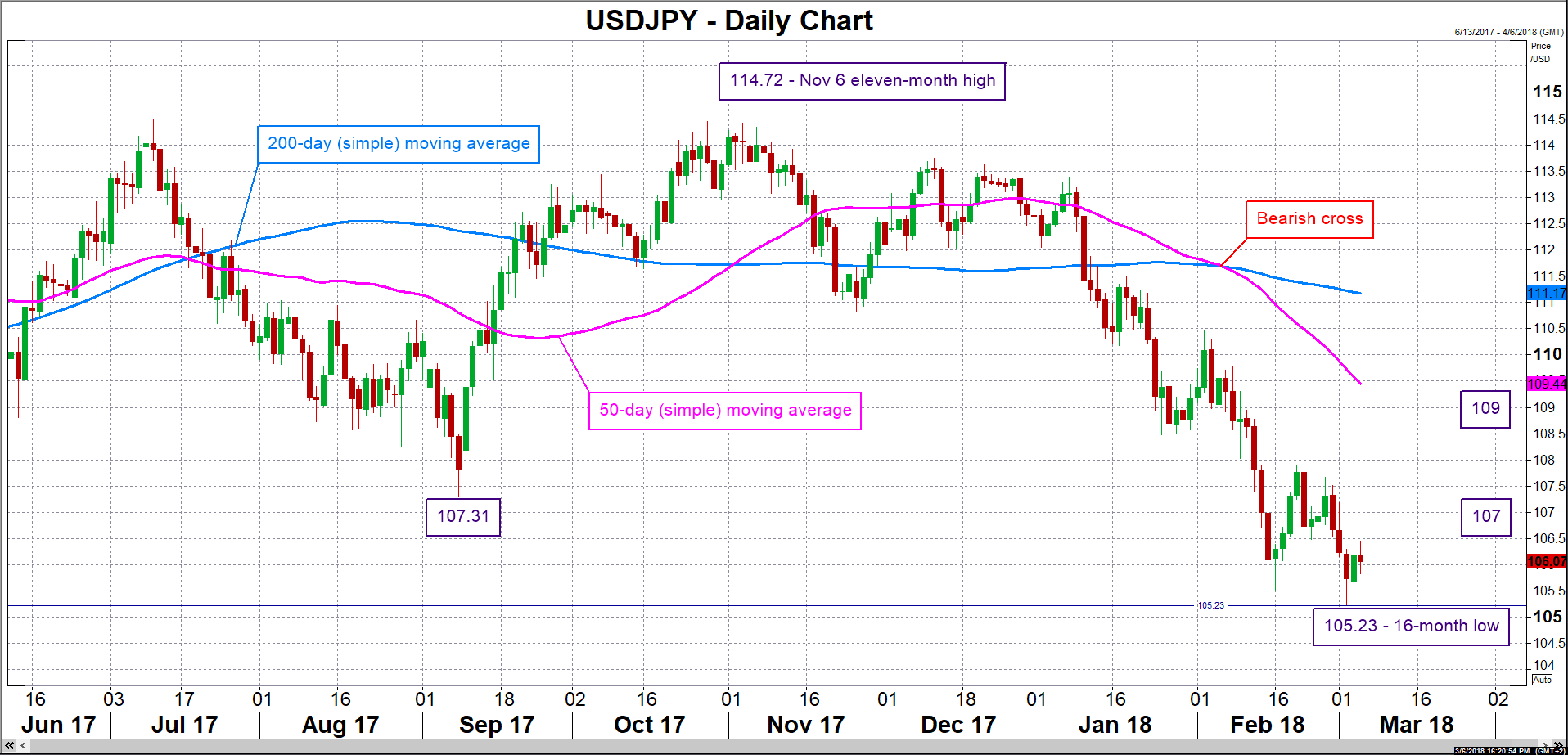

Ever-growing expectations that the BoJ is paving the way for policy normalization have been one of the main drivers behind the yen’s year-to-date appreciation by around 6% versus the US currency. Last Friday, dollar/yen hit a 16-month low of 105.23 as BoJ Governor Haruhiko Kuroda said that the Bank will start thinking about how to exit its ultra-loose monetary policy stance around the fiscal year starting in April 2019.

Ever-growing expectations that the BoJ is paving the way for policy normalization have been one of the main drivers behind the yen’s year-to-date appreciation by around 6% versus the US currency. Last Friday, dollar/yen hit a 16-month low of 105.23 as BoJ Governor Haruhiko Kuroda said that the Bank will start thinking about how to exit its ultra-loose monetary policy stance around the fiscal year starting in April 2019.

Despite Kuroda saying that stimulus withdrawal is dependent on the inflation target being met – something which might allow someone to argue that nothing essentially new was said – still it didn’t stop the markets from placing long yen positions. Also, on Tuesday, there was limited reaction to comments by Kuroda, who clarified what he meant last Friday by saying that in fiscal 2019, the BoJ “would be discussing how to move forward with exit [from monetary easing]” and adding “I never said we would be exiting immediately in fiscal 2019″. All these might mean that markets are anchoring towards a BoJ normalization narrative, being much more willing to buy the yen on hawkish-perceived comments than sell it on remarks on the other side of the spectrum. This might present opportunities for savvy investors. However, it should be kept in mind that besides monetary policy there are other currency drivers and it might be those that are supporting a stronger yen at the moment – for example, some fear that Trump’s trade rhetoric could backfire, weighing on the US’ growth outlook, and this is one factor acting to the detriment of the greenback.

Turning back to the upcoming meeting, a press conference by Governor Kuroda will follow the Bank’s rate decision. His comments and the Bank’s views on the outlook for growth and inflation have the capacity to lead to movements in yen pairs.

Focusing on dollar/yen, should views that the BoJ is getting closer to normalizing policy receive a boost, then the pair is expected to record losses. In this case, support could come around last week’s 16-month low of 105.23, with sharper declines shifting the focus to the area around 103 which was relatively congested back in 2016. If on the other hand the BoJ decisively shuts the door on tightening coming any time soon, the pair might head higher. The range around 107, which also encapsulates a bottom from the recent past, might act as a barrier to the upside. Further above, the area around 109 was congested recently and may be of significance.

In terms of data out of the world’s third largest economy, revised Q4 2017 GDP figures will be made public on Wednesday at 2350 GMT. The growth rate is anticipated to be revised to 0.9% on an annualized basis from the preliminary reading of 0.5%; this compares to Q3’s respective reading of 2.2%. The projected upward revision is expected to have come on the back of a stronger than previously recorded capex contribution, as corporations accelerated their investments in plant and equipment during the last quarter of 2017. Quarter-on-quarter, analysts project growth to stand at 0.2% in Q4. The Japanese economy posting positive growth in Q4 constitutes the eighth straight quarter of uninterrupted expansion, this being the longest such stretch since a period between 1986-1989 when the economy grew for 12 consecutive quarters and which was later linked to a bubble. Wednesday’s growth numbers also have the potential to lead to positioning on the yen. (GDP figures for Q4 2017 in the chart below correspond to the preliminary release.)

In terms of data out of the world’s third largest economy, revised Q4 2017 GDP figures will be made public on Wednesday at 2350 GMT. The growth rate is anticipated to be revised to 0.9% on an annualized basis from the preliminary reading of 0.5%; this compares to Q3’s respective reading of 2.2%. The projected upward revision is expected to have come on the back of a stronger than previously recorded capex contribution, as corporations accelerated their investments in plant and equipment during the last quarter of 2017. Quarter-on-quarter, analysts project growth to stand at 0.2% in Q4. The Japanese economy posting positive growth in Q4 constitutes the eighth straight quarter of uninterrupted expansion, this being the longest such stretch since a period between 1986-1989 when the economy grew for 12 consecutive quarters and which was later linked to a bubble. Wednesday’s growth numbers also have the potential to lead to positioning on the yen. (GDP figures for Q4 2017 in the chart below correspond to the preliminary release.)

Data on January’s current account surplus will be released alongside Wednesday’s GDP numbers, while household spending figures for the month of January will go public on Thursday at 2350 GMT. These will also be attracting interest.

Data on January’s current account surplus will be released alongside Wednesday’s GDP numbers, while household spending figures for the month of January will go public on Thursday at 2350 GMT. These will also be attracting interest.

Lastly, it should be noted that the currency – a perceived safe-haven – could receive flows should trade tensions following the Trump administration’s decision to impose tariffs on imported steel and aluminum escalate. However, one should keep in mind that if Japan, a major exporting power, is seen as losing out from developments on trade, then safe-haven flows might instead be diverted to other assets, such as gold.

Sunset Market Commentary

Markets

Today, risk sentiment was the major driver for global bond trading as there were few data with market moving potential. German bunds, which outperformed US Treasuries of late, finally met growing selling pressure. Maybe there was some repositioning out of safe haven bunds as the Italian political event risk was out of the way, at least for now. German bunds came under further pressure as the headlines on a potential denuclearization in Korea hit the screens, triggering a broad-based rally of risky assets. In this move German bunds still underperformed US Treasuries. At the time of writing, US yields rose less than 1 bp with the 30 year outperforming (-0.8 bp). The German yield curve is shifting higher between 1.8 bp (2-y) and 4.5 bp (5 & 10y). Intra-EMU 10-y yield spreads versus Germany narrowed across the board with Greece (-11 bp), Portugal (-7 bp) and Italy (-5 bp) outperforming.

Over the previous days political event risk was the dominant factor for global FX trading and this remained the case today. However, the dynamics was different. Since last week, the fear for protectionist action from the Trump administration weighed on the dollar. Today, dollar selling eased as markets hoped that senior members of the Republican party would be able to convince president Trump not to engage in an outright trade war. EUR/USD settled in the mid 1.23 area. USD/JPY drifted back to the 106 area. Around noon, markets were surprised by a positive event risk as South Korean officials declared that North Korea was prepared to talk about denuclearization. Risky assets jumped higher and so did USD/JPY and EUR/JPY. The short-squeeze in EUR/JPY also pushed EUR/USD briefly back above the 1.24 level. For now, the yen decline is easing as markets try to assess the real meaning of the developments on the Korean peninsula. The US trade/tariffs issue also isn't solved yet. USD/JPY trades currently in the 106.25 area. EUR/USD maintains most of its intraday gains and is changing hands just below 1.24. Interesting, in the risk-on repositioning, interest rate differentials also narrowed in favour of the euro.

EUR/GBP held a very tight sideways trading range in the 0.8900/0.8930 area. There were plenty of high level meetings between EU and UK politicians preparing a key EU Summit on Brexit later this month. However, for now there were no indications of a breakthrough on any of the key pending issues. Tomorrow, the EU is expected to publish a draft paper including the negotiation position of the EU.

News Headlines

North Korea is willing to hold talks with the United States on denuclearisation and will suspend nuclear tests while those talks are under way, South Korean officials said on Tuesday after a delegation returned from a meeting with North Korean leader Kim Jong Un. The announcement caused a broad-based 'risk-on' repositioning on global markets.

France maintains its view that there is little chance of securing a free trade deal that would include financial services the way that Britain hopes it to be. "Financial services cannot be in a free trade agreement ... we have to rely on equivalence regimes, that is the best solution for financial services," le Maire told BBC radio, citing the need for stability and supervision in the sector.

'It is too early, there risk is too big' for the Riksbank to raise interest rates now, Riksbank Governor Ingves said in a testimony before Parliament today. The Riksbank governor added that Sweden would have a problem meeting the inflation target if the crown strengthens too fast. The Swedish crown touched a multi-year low against the euro today at EUR/SEK 10.20.

Canada Ivey PMI Feb: 59.6, US factory orders Jan: -1.4%

Canada Ivey PMI Feb: 59.6 vs exp 56.3, prior 55.2

US factory orders Jan: -1.4% vs exp -1.3% prior 1.8% (revised from 1.7%)

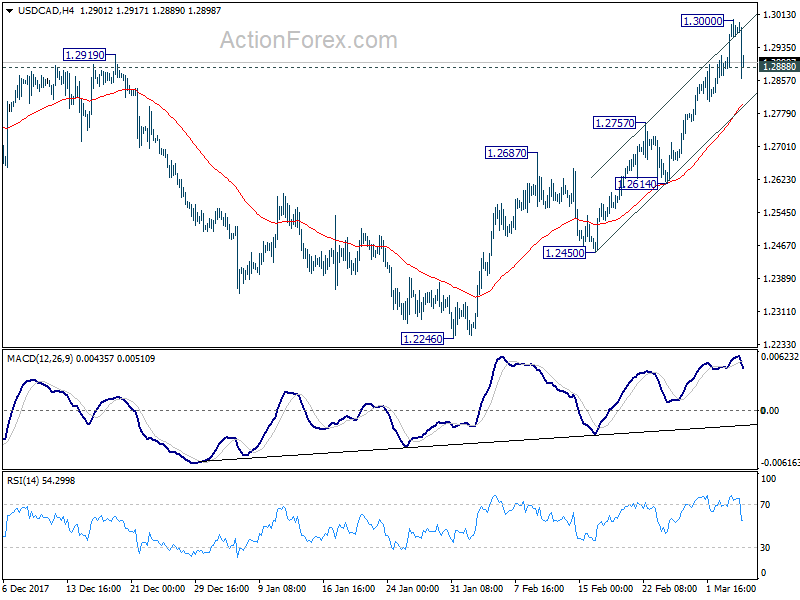

USD/CAD dips sharply on broad based dollar weakest today. A temporary top is formed at 1.3000. Deeper pull back would be seen in the session. Strong support could be seen around 4 hour 55 EMA at 1.2794, close to near term channel support.

Dallas Fed Kaplan: It’s three hikes this year

Dallas Fed President Robert Kaplan on rate hikes:

- "It's three for this year. I think we should get started sooner rather than later, though."

- "Unemployment rate is going into the 3s during 2018."

- "We are either at or below full employment right now."

- "But the thing I'll be watching is the history of overshooting full employment in the United States and having a soft landing is not a long history. So the reason I want to start removing accommodation, raising the fed funds rate, is I think that will give us the best chance to extend this expansion for longer."

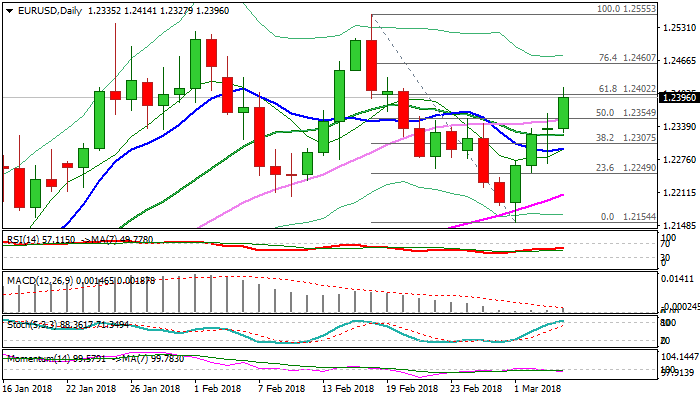

EURUSD Rallies on Potential for Koreas’ Talks; Probes above Pivotal 1.24 Barrier

The Euro surged to new two-week highs at 1.2400 zone, on fresh bullish sentiment from news about summit between North and South Korea, which was planned for late April, regarding denuclearization and normalizing ties. Surprise decision of meeting of two neighboring countries in more than a decade, triggered fresh action in the markets. The greenback was sharply lower against risk-sensitive currencies, like Euro; sterling and Aussie and hitting new lows on Tuesday. The EURUSD pair accelerated higher after holding within narrow range during Asian and early European trading. Fresh acceleration signals continuation of recovery leg from 1.2154 trough after Monday's long-legged Doji signaled indecision and pause in the rally. Bulls cracked pivotal barrier at 1.2400 (Fibo 61.8% of 1.2555/1.2154 downleg), looking for further upside if a number of stops above are triggered. Scope for bullish extension exists and requires firm break above 1.24 pivot to open targets at 1.2460 (Fibo 76.4%) and psychological 1.2500 barrier. Setup of daily MA's improved, however, overbought slow stochastic and bearishly aligned momentum, keep in play risk of corrective easing. Daily 20SMA holds today's action and marks solid support at 1.2323, which is expected to keep the downside protected.

Res: 1.2400; 1.2414; 1.2435; 1.2460

Sup: 1.2354; 1.2323; 1.2297; 1.2268

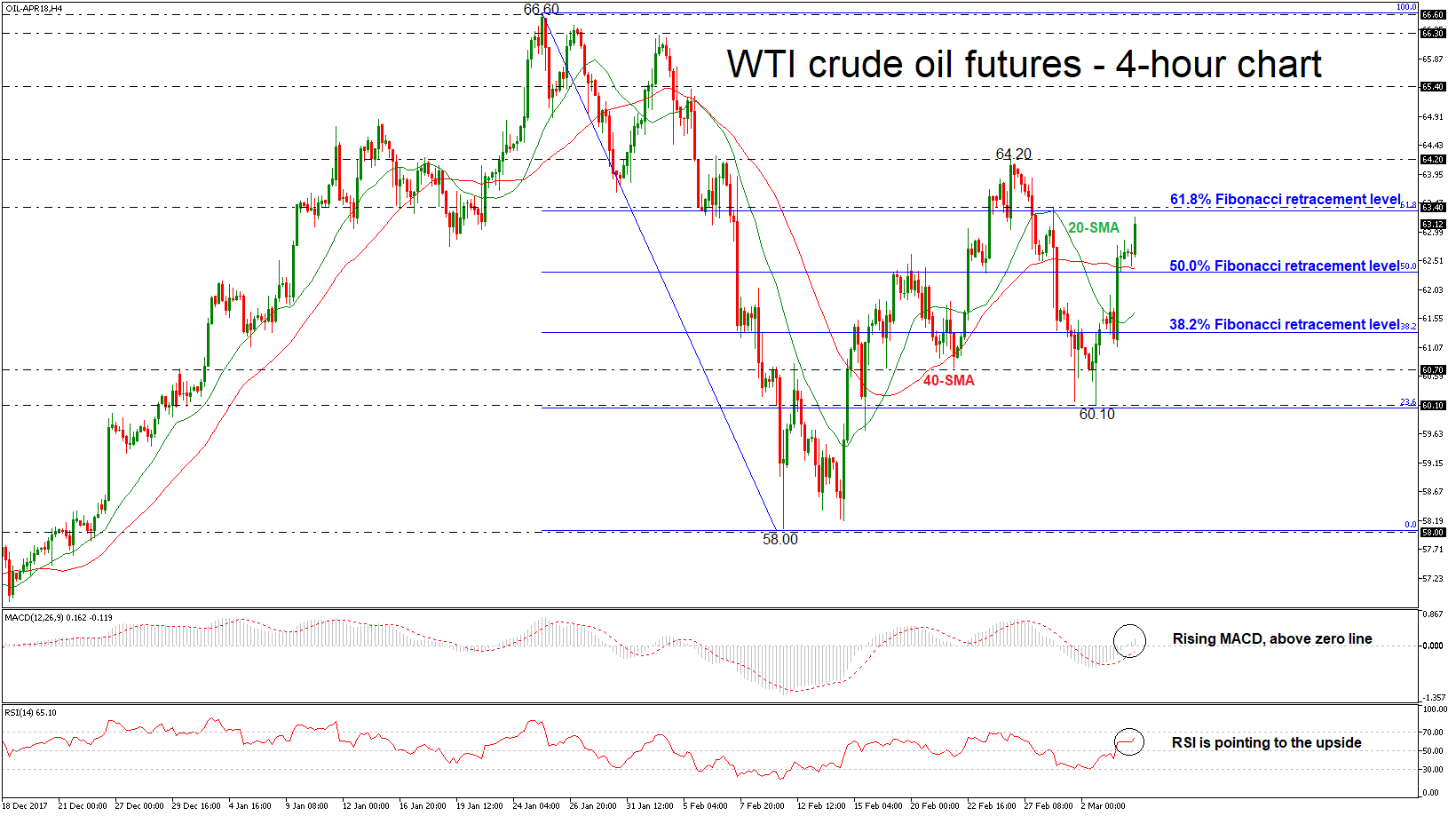

WTI Crude Oil Futures Extend Their Gains; Move Towards 61.8% Fibonacci Retracement Level

WTI crude oil futures are surging after the rebound on the 60.10 support level, which overlaps with the 23.6% Fibonacci retracement level of the downleg from 66.60 to 58.00. Currently, the price is aggressively approaching the 61.8% Fibonacci mark near the 63.40 resistance level, while it jumped above the 40-simple moving average in the 4-hour chart.

Technically, in the short-term, the MACD oscillator climbed above the zero line with strong momentum and the RSI indicator is pointing to the upside after flat sessions. Also, the latter indicator is moving towards the 70 level and the overbought territory.

If price action surpasses the 63.40 resistance level, this could open the door for the 64.20 barrier, taken from the peak on February 26.

In the event of a downside reversal, the 50.0% Fibonacci mark at 62.32 could act as a barrier before being able to re-challenge the 38.2% Fibonacci retracement level around the 61.30 support level.