Sample Category Title

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7737; (P) 0.7754; (R1) 0.7782; More...

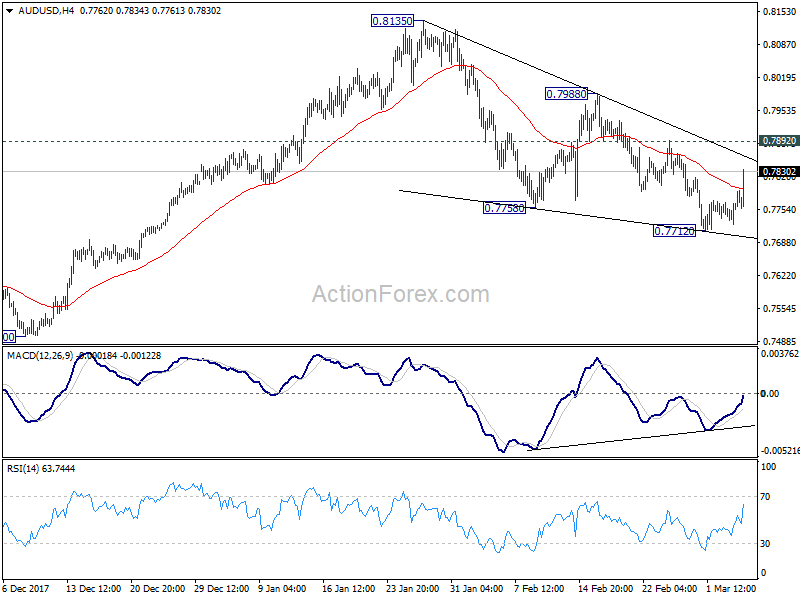

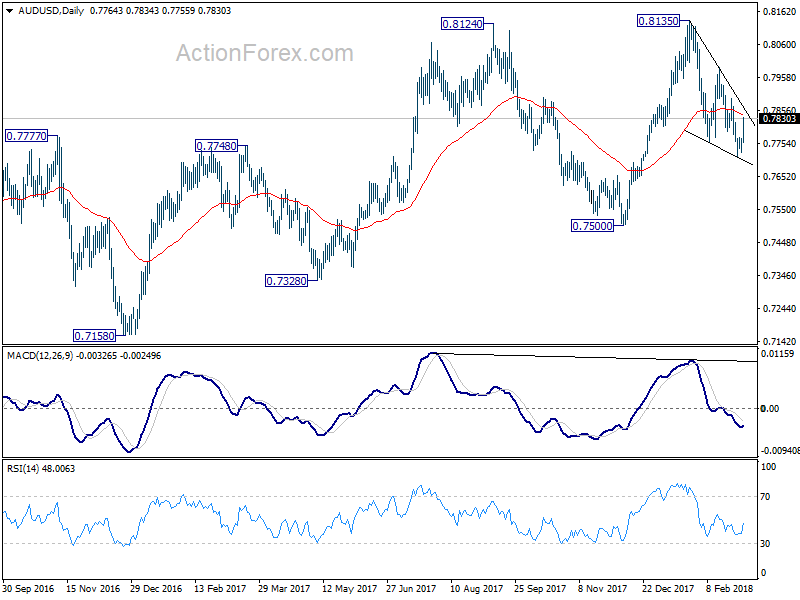

AUD/USD's rebound from 0.7712 extends to as high as 0.7834 so far today. But still it's limited below 0.7892 resistance. Such rebound could still be a corrective move only. Intraday bias stays neutral first. On the downside, break of 0.7712 will extend the fall from 0.8135 towards 0.7500 key support level. However, break of 0.7892 will suggest that the pull back from 0.8135 is already completed. In such case, intraday bias will be turned back to the upside for 0.7988 and then 0.8135 again.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Risk Appetite Returns as EU’s Retaliatory Tariff Proposal Would Force Trump to Fold His Cards

Kiwi and Aussie are leading the way higher in the currency markets as risk appetite returns. On the other hand, Yen and Dollar are trading as the weakest ones today. Markets are increasing getting convinced that US President Donald Trump will back off from his steel and aluminum tariffs. He's facing strong opposition from his own party and closest aides, as well as from global leaders. In partcular EU's counter-threat of retaliatory tariff would add pressure to Trump to fold his cards. At the time of writing FTSE is up 0.79%, DAX up 1.08%, CAC up 0.77%. Earlier, Nikkei closed up 1.79%. US futures point to another day of rebound.

EU proposes 25% retaliatory tariff to US

It's reported that EU is preparing retaliatory tariff to the US, should Trump impose the 25% tariff on steel and 10% on aluminum imports. Bloomberg reported that EU targets to apply 25% tariff on a range of US goods that costs as much as EUR 2.8b. And the list obtained include motorcycles, jeans and bourbon whiskey. Around EUR 1b will be on consumer goods, motorbikes and pleasure boat. EUR 0.95b will be on whiskeys and agricultural products. Meanwhile, EUR 8.5b will be on steel and other industrial products. The list was discussed by the European Commission on Monday evening.

European Commission's chief spokesman Margaritis Schinas said regarding March 7 EC meeting. He noted that "the Commissioners will discuss our reaction. It will be swift, firm, and proportionate - based on three main criteria compatible with WTO rules." Also, EU "cannot be expected to bury our heads in the sand when someone takes unilateral and unfair actions against us that put thousands of European jobs at risk". But he also emphasized that "trade policy is not a zero-sum game" and it "can and should be win-win."

EU Verhofstadt urged May to move beyond aspirations

European Parliament's Brexit representative Guy Verhofstadt is meeting UK Brexit Secretary David Davids in 9 Downing Street today. Verhofstadt will also meet Cabinet Office minister David Lidington and Home Secretary Amber Rudd at 10 Downing Street where Prime Minister Theresa May would stop by. Verhofstadt urged May to move beyond "vague aspirations" and give "credible proposals" after her Mansion House speech last Friday

May called for a system of "mutual recognition " on the trade deal with EU after Brexit. That is, the two trading partners should recognize each other rule, yet they're free to adopt their own ways. The system is to be overseen by a joint UK-EU court. EU negotiator Michel Barnier's chief adviser Stefaan de Rynck blasted it as a "failed" system. He said "there was a time we thought it would lead to market efficiency, but with the financial crisis we have gone for an approach of more harmonization and centralization and more EU bodies overseeing that and stronger powers for those bodies." And, "if you are in a very integrated market with a third country but you don't have the joint enforcement structures, then you can see the potential for all kinds of difficult situations.

Eurozone retail PMI improved to 52.3

Eurozone retail PMI rose to 52.3 in Feb, up from Jan's 50.8. Markit noted in the statement that "the latest data highlight another positive month for the eurozone retail sector, with sales up at a quicker pace on a monthly basis. In turn, this contributed to a renewed bout of optimism, with the survey's measure of business confidence among the highest over the last year. Further expansions in purchasing activity and employment underscore retailers' positive outlook. Nevertheless, gross margins continued to be squeezed, suggesting business conditions remain challenging."

Swiss CPI closed to 0.6% yoy

Swiss CPI rose 0.4% mom, 0.6% yoy in February, versus expectation of 0.3% mom, 0.6% yoy. Swiss Federal Statistical Office FSO said in the released that "the 0.4% increase compared with the previous month can be explained by several factors including rising prices for air transport. Foreign package holidays also recorded an increase, as did clothing and footwear due to the end of the seasonal sales. In contrast, prices for heating oil, coffee and overnight stays in hotels decreased."

BoJ Kuroda: May think about stimulus exit 2019, but not necessarily doing

BoJ Governor Haruhiko Kuroda appeared in his confirmation hearing in the upper house today. Kuroda said that there is not plan to raise short-term rates or abandon negative rates right now. The central bank start thinking about stimulus exit in fiscal 2019, when inflation is forecast to meet the 2% target. But Kuroda added that "right now it's too early to debate what tools we should use, and what kind of pace we should take." He also emphasized that BoJ might not exit stimulus even then.

RBA: Rate of wage growth troughed

Aussie trades mildly higher after RBA kept the cash rate unchanged at 1.50% as widely expected. The statement is almost likely a carbon copy of the prior one. Nonetheless, RBA sounded more optimistic on wage growth as it said that "the rate of wage growth appears to have troughed". Regarding the economy, Australian economy is expected to grow fast in 2018 than in 2018. Regarding inflation RBA maintained that "the central forecast is for CPI inflation to be a bit above 2 per cent in 2018." The statement concluded by maintaining "holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time."

More on RBA: RBA Left Cash Rate Unchanged At 1.5% As Property Markets Cooled

Released earlier in Australia retail sales rose 0.1% mom in January, below expectation of 0.4% mom. Current account deficit widened to AUD -14.0b in Q4.

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7737; (P) 0.7754; (R1) 0.7782; More...

AUD/USD's rebound from 0.7712 extends to as high as 0.7834 so far today. But still it's limited below 0.7892 resistance. Such rebound could still be a corrective move only. Intraday bias stays neutral first. On the downside, break of 0.7712 will extend the fall from 0.8135 towards 0.7500 key support level. However, break of 0.7892 will suggest that the pull back from 0.8135 is already completed. In such case, intraday bias will be turned back to the upside for 0.7988 and then 0.8135 again.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Feb | 0.60% | 0.50% | 0.60% | |

| 0:30 | AUD | Current Account Balance (AUD) Q4 | -14.0B | -12.3B | -9.1B | -11.0B |

| 0:30 | AUD | Retail Sales M/M Jan | 0.10% | 0.40% | -0.50% | |

| 3:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:15 | CHF | CPI M/M Feb | 0.40% | 0.30% | -0.10% | |

| 8:15 | CHF | CPI Y/Y Feb | 0.60% | 0.60% | 0.70% | |

| 9:10 | EUR | Eurozone Retail PMI Feb | 52.3 | 50.8 | ||

| 15:00 | USD | Factory Orders Jan | -1.30% | 1.70% | ||

| 15:00 | CAD | Ivey PMI Feb | 56.3 | 55.2 |

NZD and AUD strongest as risk appetite returns

NZD and AUD generally higher into US session. JPY and USD weakest. That's very much thanks to return of risk appetite. At the time of writing, FTSE is up 0.79%, DAX up 1.08%, CAC up 0.77%. Earlier, Nikkei closed up 1.79%.

Trump's response to EU's counter-threat of 25% retaliatory tariff something to watch. Calendar is light with US factory orders and Canada Ivey PMI featured only. But there are some speeches to watch though, including Fed Dudley, BoE Haldane and RBA Lowe.

Trump's response to EU's counter-threat of 25% retaliatory tariff something to watch. Calendar is light with US factory orders and Canada Ivey PMI featured only. But there are some speeches to watch though, including Fed Dudley, BoE Haldane and RBA Lowe.

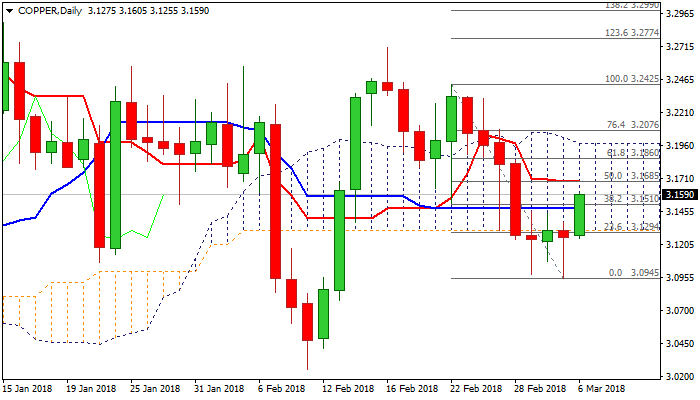

Technical Outlook: COPPER – Fresh Recovery Is Forming Reversal Pattern On Daily Chart

Copper advanced on Tuesday and penetrated thick daily cloud, after three-day congestion remained capped by cloud base.

Fresh advance is generating reversal signal after repeated strong downside rejections left higher base at $3.0950 zone and fresh rally dented pivotal barrier at $3.1510 (Fibo 38.2% of $3.2425/$3.0945 descend).

Existing fears of global trade war intensified again after President Trump said he will stick to his guns despite growing pressure to drop the tariff plan, boosting copper price on Tuesday.

Fresh bullish tone is developing on lower timeframes, but studies on daily chart remain in firm bearish mode.

Bulls need firm break into daily cloud as minimum requirement, with break above Fibo barrier at $3.1510 and nearby 100SMA at $3.1545, required for firmer bullish signal.

However, plethora of barriers that lies above, weighs on near-term action. Stronger acceleration through $3.1623/$3.1751 zone (20/10/30SMA’s) is required to further inflate bulls and signal further recovery towards next pivots at $3.1865 (Fibo 61.8% of $3.2425/$3.0945) at $3.1975 (daily cloud top).

Res: 3.1623, 3.1751, 3.1865, 3.1975

Sup: 3.1510, 3.1312, 1.1255, 3.1075

Trumps Tariff Pushback Dents Trade War Fears

Tuesday March 6: Five things the markets are talking about

Global equities have extended their rebound overnight as investors judge the recent selloff sparked by global trade fears as a tad overdone. President Trump continues to face mounting domestic resistance to his planned levies on steel and aluminum imports.

The ‘big” dollar and oil are trading steady as U.S Treasury yields again back up.

Strong job growth and a deeper decline in the unemployment rate are the calls for this week’s U.S highlight – Friday’s non-farm payroll (NFP) at 08:30 am EDT.

Note: Today’s U.S factory orders are expected to reveal a sizable January decline (-0.4% vs. +1.7%).

Trade data will be the highlight tomorrow morning and an increasing U.S deficit would only support Trump’s discussion about tariffs. In the afternoon, its the release of the Beige Book where the economic assessments have until now, at least, been subdued.

On tap: Central bank rate activity this week – BoC (Mar 7), ECB (Mar 8) and BoJ (Mar 8/9). The ECB is not expected to change policy on Thursday, but the Governing Council may discuss a change to pave the way for the end of QE.

1. Stocks jump as fears recede

In Japan, the Nikkei share average rallied overnight to snap a four-day losing run. The ‘bid’ dollars bounce lifted exporter shares. The Nikkei ended the day up +1.79%, while the broader Topix rallied +1.27%.

Down-under, Aussie shares edged higher as export-based stocks rallied on receding fears of a global trade war. The S&P/ASX 200 index rose +1.1% to 5,962.4 at the close of trade. The benchmark ended down -0.6% on Monday. In S. Korea, the Kospi closed up+1.53%.

Note: The Reserve Bank of Australia (RBA) left its cash rate at +1.5% overnight, a widely expected decision given policy makers have signalled a steady outlook for some time to come.

In Hong Kong, stocks rebounded aggressively amid fears that Trump is facing growing pressure from political allies to pull back from his proposed tariffs plans. The Hang Seng index rose +2.1%, while the China Enterprises Index gained +2.7%.

In China, stocks too rebounded overnight, aided by robust gains in shares of real estate and healthcare firms. At the close, the Shanghai Composite index was up +1%, while the blue-chip CSI300 index was up +1.2%.

In Europe, regional indices have rebounded following strong gains stateside yesterday and in Asia overnight.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.7% at 373.5, FTSE +1.0% at 7184, DAX +1.1% at 12227, CAC-40 +0.7% at 5203, IBEX-35 +0.4% at 9631, FTSE MIB +1.1% at 22056, SMI +0.1% at 8816, S&P 500 Futures +0.2%

2. Oil inches up on strong demand forecasts, gold higher

2. Oil inches up on strong demand forecasts, gold higher

Oil futures have rallied overnight for a third consecutive session, supported by robust demand forecasts and as ministers from OPEC touted the strength of its agreement to cut output to bolster prices.

Brent crude futures are at +$65.67 per barrel, up +8c, or +0.12%. U.S West Texas Intermediate (WTI) crude futures are at +$62.68 a barrel, up +11c, or +0.18%.

The IEA said yesterday that global oil demand was expected to grow over the next five years, while output from OPEC producers would rise at a much slower pace.

To fill the gap between OPEC and global demand, the IEA said the U.S would supply much of the oil demand as its shale oil production was set to surge.

Note: U.S crude production has risen to more than +10m bpd, overtaking top exporter Saudi Arabia.

Expect dealers to take their cues from the weekly inventory reports. Today, API is set to release its inventory data at 4:30 pm EST and tomorrow the EIA is scheduled to report its data at 10:30 am EST.

Ahead of the U.S open, gold prices have edged up a tad on a softer dollar and as the market covers some short positions amid trade war fears. Spot gold is up +0.1% at +$1,321.05 per ounce.

3. Sovereign yields push higher

Overnight, the Reserve Bank of Australia (RBA) left its cash rate target unchanged at +1.50% (as expected). The accompanying policy statement was unrevised. It reiterated the view that low level of interest rates was continuing to support the Aussie economy and that inflation was expected to remain low for some time – An appreciating exchange rate (A$0.7767) could slow economic activity and inflation.

In Japan, the Bank of Japan (BoJ) Governor Kuroda tried to clarify some of his earlier comments made during the Confirmation Hearings on March 2 – he stated that the BoJ would consider an exit around Fiscal 2019 because of the chances of hitting inflation target at that time. Kuroda reiterated that the BoJ was keeping policy “very accommodative” as it took time to get rid of deflationary mindset. In other words, fewer stimuli remains unthinkable before reaching the CPI target.

Elsewhere, German Bund yields trade slightly higher, while Italian BTP versus Bund spreads trade narrower in a sign that investors apparently have absorbed, at least for now, the outcome of Italy’s elections. The 10-year Bund yield is trading at +0.65%, up +2 bps. Dealers will now turn their attention to the ECB’s Governing Council’s meeting on Thursday.

The yield on 10-year U.S Treasuries has decreased -1 bps to +2.87%, while in the U.K, the 10-year Gilt yield increased +1 bps to +1.495%, the highest in a week.

4. Dollar confined to tight ranges

The FX market remains subdued, confined to tight trading ranges ahead of three major rate decisions announcements this week – Bank of Canada (BoC) tomorrow, European Central Bank (ECB) Thursday and Bank of Japan (BoJ) on Friday.

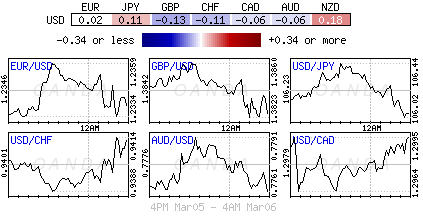

The EUR/USD is steady just under the mid-€1.23 area as negatives from the hung Parliament after Sunday’s Italian elections seemed to dissipate. The EUR ‘bull’ is expecting the ‘single’ unit to retest the upper end of its recent trading range

USD/JPY (¥106.16) is off its Asian session highs after the BoJ’s Kuroda played down his recent commentary regarding a potential exit from its ultra-loose policy stance.

Elsewhere, EUR/SEK (€10.1888) hit a fresh eight-year high as Riksbank Governor Ingves stressed that “monetary policy needed to proceed cautiously with future hikes.”

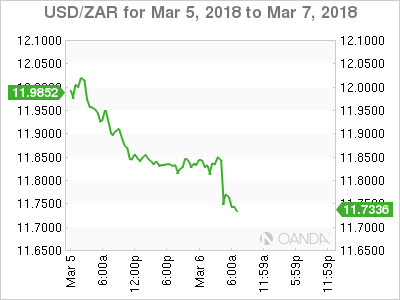

USD/ZAR ($11.7516) is lower as South Africa GDP beat expectations. Also, the South Africa Parliament has delayed a planned debate relating to the SARB (Central Bank) mandate and Independence. The SARB has been under the radar to possibly be nationalized.

5. Eurozone retail sales continues to grow

Data collected by Markit in February showed that Eurozone retailers reported an eleventh consecutive monthly rise in “like-for-like” sales during the month. Moreover, the rate of expansion quickened from January’s five-month low and was solid overall.

The acceleration at the eurozone level reflected sharper rises in Germany and France, and renewed growth in Italy.

The headline print rose to 52.3 in February, from 50.8 in January.

Digging deeper, sales were broadly unchanged when compared to the same month one-year prior, after having been down the previous two months.

EUR/USD – Euro Subdued As Investors Look For Cues

The euro continues to have a quiet week. In the Tuesday session, EUR/USD is trading at 1.2354, up 0.14% on the day. On the release front, it’s a light day for fundamentals, with non major indicators. In the eurozone, Retail PMI improved to 52.3, pointing to slight expansion. On Wednesday, the eurozone releases revised GDP, and the US will publish ADP nonfarm payrolls.

The ECB will be on center stage on Thursday, as the Bank will set the benchmark rate, followed by a press conference with Mario Draghi. The interest rate has been pegged at a flat 0.0% for the past two years, and no change is expected. The markets will be keeping a close eye on the language of the rate statement, in particular, whether the easing bias stance will be removed. If so, this would likely be interpreted as a plan to eventually tighten policy and would be bullish for the euro. Inflation remains weak, so there is little pressure on the ECB to tighten policy anytime soon. Recent indicators show that inflation in the eurozone is steady, but remains well below the ECB target of around 2 percent. Eurozone CPI dipped to 1.2% in February, down from 1.3% in January.

The “tariff tussle” shows no sign of being resolved anytime soon. US President Trump appears set on applying stiff tariffs on steel imports, much to the consternation of the European Union and other US trading partners. However, there is plenty of domestic opposition to Trump’s plan, as Republican lawmakers, including House Speaker Paul Ryan, have come out strongly against the move. If Trump doesn’t back down, the Republicans could even resort to legislation to limit Trump’s authority on tariffs. The announcement of the tariffs briefly sent the dollar lower, and if the tariffs are introduced, negative investor sentiment could send the greenback to lower levels.

Stocks Bounce Despite Trade War Concerns

- Markets Rebound as Republicans Oppose Trump Tariffs Plan;

- European Markets Unfazed By Italian Result, For Now;

- Central Bank Speakers Stand Out in Quiet Session.

Markets Rebound as Republicans Oppose Trump Tariffs Plan

Investors may have been rattled by the prospect of a trade war after Donald Trump’s recent tariffs announcement, but equity markets are once again recovering as it becomes clear that the US President does not have the full backing of his party of this one.

Some Republicans, including House Speaker Paul Ryan, have warned against starting a trade war that could damage the economy and undo the benefits of the recently passed tax reforms, highlighting that Trump is lacking the full support of his party on this particular issue. Trump’s comments linking the tariffs to NAFTA negotiations also suggested that they could be dropped if a new agreement is signed, suggesting he may simply be using the threat of tariffs to put pressure on others to deliver what he considers to be fair and reciprocal trade.

That may enable Trump to extract some concessions from Mexico and Canada, or at least allow him to claim credit for securing a better deal, but it’s unlikely to work as well with the European Union and China, among others. The prospect of a trade war will be a big concern for markets, with many of the view that such action would drive up prices for all and weigh on economic growth.

European Markets Unfazed By Italian Result, For Now

While markets are rebounding, US indices are still more than 5% off their highs having gone through an unusual rough patch over the last month or so, while some in Europe are faring even worse. The German DAX is almost 10% below its January highs, with the long drawn out negotiations not helping matters, although this did come to an end this weekend with the SPD voting to join a grand coalition again. The prospect of tighter monetary policy may also be weighing on European markets at a time when the euro area economy is gathering some momentum.

The Italian election weighed heavily on the FTSE MIB heading into the weekend and at the start of the week, although we have seen a strong rebound over the last 24 hours. The strong performance of populist euroskeptic movements in Italy and corresponding underperformance of the established parties will be a concern to those hoping for political stability and a pro-EU government. It will also cause a major headache for the rest of the EUs desire for an ever-closer union in the unlikely event that the two main populist parties go into coalition.

At the moment the impact on the wider market has been minimal, which may reflect the change in tone from euroskeptics from demanding a referendum on membership to simply criticizing the project and opposing a closer union. While this stance could revert once in power, especially in the case that the euroskeptic parties go into coalition, at the moment the risk of a referendum and vote to leave is still slim. The greater issue is prolonged political instability and weak growth.

Central Bank Speakers Stand Out in Quiet Session

While today is looking a little quieter in terms of major economic events, particularly when compared to the rest of the week, there are a few central bankers making appearances which will be of interest. These include Lael Brainard from the Federal Reserve, Andy Haldane from the Bank of England and Governor Philip Lowe from the Reserve Bank of Australia.

Market Update – European Session: Trade Issues Remain In Focus

Notes/Observations

Markets continue to shrugged off the threats of Protectionism

Asia:

South Korea Feb CPI M/M: 0.8% v 0.5%e; Y/Y: 1.4% v 1.2%e

Australia Jan Retail Sales M/M: 0.1% v 0.4%e

RBA left its Cash Rate Target unchanged at 1.50% (as expected). Policy statement unrevised which reiterated view that low level of interest rates was continuing to support the Australian economy and that that inflation to remain low for some time. An appreciating exchange rate could slow economic activity and inflation

BoJ Gov Kuroda Confirmation Hearings had the gov reiterated that BOJ was keeping policy very accommodative as it took time to get rid of deflationary mindset. Less stimulus was unthinkable before reaching CPI target

China National Development and Reform Commission (NDRC) Chairman expressed confidence that China would reach 6.5% GDP target

Europe:

EU's initial offer on trade will not be very detailed; The lack of detail in the offer would leave the UK having to renegotiate large parts of its trade agreement with the EU during the post-Brexit period. The UK has been seeking to have the entire trade accord squared away before the March 2019 Brexit

Senior EU Brexit negotiator Rynck: not likely that there will be certainty about future ties to the EU by this fall [*Note: previously EU had sought to wrap up trade negotiations by Nov]

Americas:

President Trump: Will not back down on trade; I don't think we will have a trade war; Reiterates threat to raise tax on car imports

Trump expected to discuss impact of planned tariffs with US companies that use aluminum and steel on Thursday, Mar 8th

Energy:

OPEC Sec Gen Barkindo: Demand has not been this solid and positive since before the financial crisis; Have to wait on a decision about whether production cuts will be extended into 2019; Shale producers are interested in a dialogue with OPEC, but will not be discussion production cuts or prices

Economic Data:

(AT) Austria Feb Wholesale Price Index M/M: -1.0% v +0.9% prior; Y/Y: No est v 3.3% prior

(HU) Hungary Q4 Final GDP Q/Q: 1.3% v 1.3%e; Y/Y: 4.4% v 4.4%e (highest annual pace since 2014)

(CH) Swiss Feb CPI M/M: 0.4% v 0.3%e; Y/Y: 0.6% v 0.6%e

(CH) Swiss Feb CPI EU Harmonized M/M: +0.3% v -0.5% prior; Y/Y: 0.5% v 0.8% prior

(DE) Germany Feb Construction PMI: 52.7 v 59.8 prior

(SE) Sweden Jan Private Sector Production M/M: 0.5% v 1.9%e; Y/Y: 4.5% v 3.9% prior,

(SE) Sweden Jan Industrial Orders M/M: -0.5% v -0.5% prior; Y/Y: 8.3% v 6.3% prior

(IS) Iceland Feb Preliminary Trade Balance (ISK): -5.3B v -5.7B prior

(NO) Norway Feb Region Survey: Output Past 3 Months: 1.32 v 1.22 prior, Output Next 6 Months: 1.42t v 1.19 prior

(EU) Euro Zone Feb Retail PMI: 52.3 v 50.8 prior

(DE) Germany Feb Retail PMI: 53.8 v 53.0 prior

(FR) France Feb Retail PMI: 51.8 v 51.0 prior

(IT) Italy Feb Retail PMI: 50.4 v 47.3 prior

(ZA) South Africa Q4 GDP Annualized Q/Q: 3.1% v 1.8%e; Y/Y: 1.5% v 1.3%e

Fixed Income Issuance:

(ID) Indonesia sold total IDR5.095 in 6-month Islamic Bills; 2-year, 4-year, 7-year and 15-year Project-based Sukuk (PBS)

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2026, 2030, 2032 and 2044 bonds

(ES) Spain Debt Agency (Tesoro) sold total €4.92B vs. €4.5-5.5B indicated range in 6-month and 12-month bills

(AT) Austria Debt Agency (AFFA) sold total €1.15B vs. €1.15B indicated in 2022 and 2028 RAGB bonds

(CH) Switzerland sold CHF399.0M in 3-month Bills; Yield: -0.892% v -0.892% prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.7% at 373.5, FTSE +1.0% at 7184, DAX +1.1% at 12227, CAC-40 +0.7% at 5203 , IBEX-35 +0.4% at 9631, FTSE MIB +1.1% at 22056 , SMI +0.1% at 8816, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices rebound following strong gains in Wallstreet and Asia overnight and stronger US futures this morning. On the corporate front in Switzerland Oerlikon, Bucher trade higher on earnings while Dorma and Kaba, and Lindt trade lower. In the UK, Aggreko trades sharply lower after results, with Just Eat and Ashtead also lower, while Thales in France trades higher after upbeat results and guidance. In the M&A space Smurfit Kappa trades sharply higher after rejecting a bid from International Paper, while William Hill and Helical trade higher after divesting units. Looking ahead notable earnings include retailer Target, alongside Ciena and Donaldson Company.

Movers

Consumer Discretionary [ Just Eat [JE.UK] -9% (Earnings), Ashtead [ASH.UK] -4.4% (Earnings), Aggreko [AGK.UK] -11.2% (Earnings), McCarthy and Stone [MCS.UK] -2.8% (Earnings), Williams Hill [WMH.UK] +1.6% (Divestment) ]

Industrials [ Smurfit Kappa [SKG.UK] +18.7% (Rejects offer from IP), Thales [HO.FR] +6% (Earnings), Oerlikon [OERL.CH] +7% (Earnings), Dorma + Kaba [DOKA.CH] -7.9% (Earnings)]

Financial [ Helical [HLCL.UK] +3.4% (Divestment) ]

Speakers

EU Commission said to consider retaliatory tariffs of 25% totaling €2.8B on US steel, apparel, textile and footwear and selected industrial goods

Sweden Central Bank (Riksbank) Gov Ingives: Monetary policy needed to proceed cautiously; exchange rate movements were a risk factor. Weaker inflationary pressures was creating uncertainty and reiterated view that SEK currency (Krona) was expected to appreciate slowly

Sweden Central Bank (Riksbank) Dep Gov Ohlsson (hawk): Inflation had remained close to target for some time; unemployment appeared to have bottomed out. Have seen a stable, upward trend in inflation over the past year and could not let temporary variations in inflation affect monetary policy

Italy Stats Agency (ISTAT) Monthly Economic Note stated that thedomestic economy was growing at a strong pace in the short-term

BoJ Gov Kuroda: Did not mean policy exit would begin as soon as FY19/20 (**Reminder: On Mar 2nd Kuroda stated at his confirmation hearing that BOJ would consider an exit around Fiscal 2019 because of the chances of hitting inflation target at that time)

Currencies

FX markets were again generally subdued in price action during the session. There are 3 more major rate decisions this week (Bank of Canada on Wed, ECB on Thursday and BOJ on Friday)

EUR/USD was steady just under the mid-1.23 area as negatives from the hung Parliament in the recent Italian elections seemed to dissipate. Dealers noting that the pair could be poised to retest the upper end of its 1.21-2.5 trading range

USD/JPY was off its Asian session highs as BOJ Gov Kuroda played down his recent commentary regarding a potential exit from its ultra-loose policy stance. Kuroda noted that less stimulus was unthinkable before reaching CPI target

EUR/SEK hit a fresh 8-year high as Riksbank Gov Ingves stressed that monetary policy needed to proceed cautiously with future hikes. The cross test above 10.20 before consolidating

USD/ZAR was lower as South Africa GDP beat expectations with the pair testing 11.75 area. South Africa Parliament delayed a planned debate relating the SARB (Central Bank) mandate and Independence. The SARB has been under the radar to possibly be nationalized.

Fixed Income

Bund Futures trades 15 ticks higher at 156.95 following the move from Treasuries. Upside targets 158.50, while a return lower targets the156.75 level.

Gilt futures trade at 122.02 down 2 ticks as Gilts take a break from the 2 ½ week rally. Support continues to stand at 120.75 then 120.15, with upside resistance at 122.85 then 123.35.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.878T from €1.885T prior. Use of the marginal lending facility fell to €51M from €45M prior.

Corporate issuance saw 2 issuers raise $1.7B in the primary market

Looking Ahead

(RU) Russia Feb Light Vehicle Car Sales Y/Y: No est v 31% prior

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (EU) ECB allotment in 7-day Main Financing Tender

05:30 (DE) Germany to sell combined €1.0B in 2026 and 2030 Inflation-linked bonds (Bundei)

05:30 (UK) DMO to sell 1.5% 2047 Gilts

05:30 (BE) Belgium Debt Agency (BDA) to sell 3-month and 12-month Bills

06:30 (TR) Turkey Feb Effective Exchange Rate (REER): No est v 85.53 prior

06:30 (EU) ESM to sell €2.0B in 3-month bills; Avg Yield: % v -0.612% prior; Bid-to-cover: x v 4.9x prior (Feb 6th 2018)

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia announces weekly OFZ bond auction

07:00 (BR) Brazil Jan Industrial Production M/M: -2.1%e v 2.8% prior; Y/Y: 5.2%e v 4.3% prior

07:30 (US) Fed's Dudley (dove, FOMC voter) speaks at U.S. Virgin Islands

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:15 (UK) Baltic Dry Bulk Index

08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Feb Consumer Confidence: 84.1e v 84.2 prior

09:00 (MX) Mexico Dec Gross Fixed Investment: -0.6%e v -4.5% prior

09:20 (BR) Brazil Feb Vehicle Production: No est v 216.8K prior; Vehicle Sales: No est v 181.3K prior; Vehicle Exports: No est v 47.0K prior

09:30 (NZ) Fonterra Global Dairy Trade Auction: Dairy Trade price index

10:00 (US) Jan Factory Orders: -1.4%e v +1.7% prior; Factory Orders (Ex-Transportation: No est v 0.7% prior

10:00 (US) Jan Final Durable Goods Orders: -3.6%e v -3.7% prelim; Durables Ex Transportation: No est v -0.3% prelim, Capital Goods Orders (Non-defense/ex-aircraft): No est v 0.2% prelim, Capital Goods Shipment (Non-defense/ex-aircraft): No est v 0.1% prelim

10:00 (CA) Canada Feb Ivey Purchasing Managers Index (Seasonally Adj): No est v 55.2 prior

11:00 (NZ) New Zealand Feb QV House Prices Y/Y: No est v 6.4% prior

11:30 (US) Treasury to sell 4-Week Bills

12:00 (US) DOE Short-Term Crude Outlook

15:00 (MX) Mexico Citibanamex Survey of Economists

16:00 (NZ) New Zealand Government 7-Month Financial Statements

16:30 (US) Weekly API Oil Inventories

19:00 (US) Fed’s Brainard (voter, dove) in NY

19:30 (AU) Australia Q4 GDP Q/Q: 0.5%e v 0.6% prior; Y/Y: 2.5%e v 2.8% prior

EU MEP Verhofstadt meeting UK Brexit Secretary Davids in 9 Downing Street

European Parliament's Brexit representative Guy Verhofstadt is meeting UK Brexit Secretary David Davids in 9 Downing Street today. Verhofstadt will also meet Cabinet Office minister David Lidington and Home Secretary Amber Rudd at 10 Downing Street where Prime Minister Theresa May would stop by. Verhofstadt urged May to move beyond "vague aspirations" and give "credible proposals" after her Mansion House speech last Friday

May called for a system of "mutual recognition " on the trade deal with EU after Brexit. That is, the two trading partners should recognize each other rule, yet they're free to adopt their own ways. The system is to be overseen by a joint UK-EU court. EU negotiator Michel Barnier's chief adviser Stefaan de Rynck blasted it as a "failed" system. He said "there was a time we thought it would lead to market efficiency, but with the financial crisis we have gone for an approach of more harmonization and centralization and more EU bodies overseeing that and stronger powers for those bodies." And, "if you are in a very integrated market with a third country but you don't have the joint enforcement structures, then you can see the potential for all kinds of difficult situations.

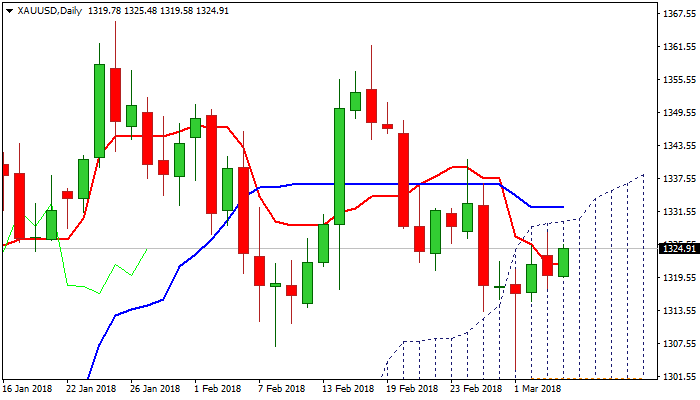

Technical Outlook: Spot Gold: Fresh Attempts Higher As Sentiment Sours On Renewed Fears About Trade War

Spot Gold moved higher on Tuesday, probing again above initial barrier at $1323 (10SMA), as uncertainty on US tariffs keeps dollar's sentiment sensitive. Traders remain cautious as fears of possible trade war remain alive, as pressure rises on President Trump to pull back from proposed tariffs plan. Investors are returning to risk-off mode on persisting uncertainty and could push gold price higher if sentiment sours further. Fresh upside pressures cracked pivot at $1326 (Fibo 61.8% of $1340/$1302 bear-leg), firm break of which would generate bullish signal and open way for test of next pivot at $1329 (daily cloud top). Technical picture remains mixed as bearish momentum is building, MA's are in mixed mode while slow stochastic heads north and showing space for further advance. Lift above $1326/29 pivots is needed to improve the picture and signal further advance. Cracked 10SMA marks immediate support at $1323, while return below $1322 (rising 55SMA) would generate negative signal.

Res: 1326, 1329, 1333, 1336

Sup: 1324, 1322, 1315, 1307