Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

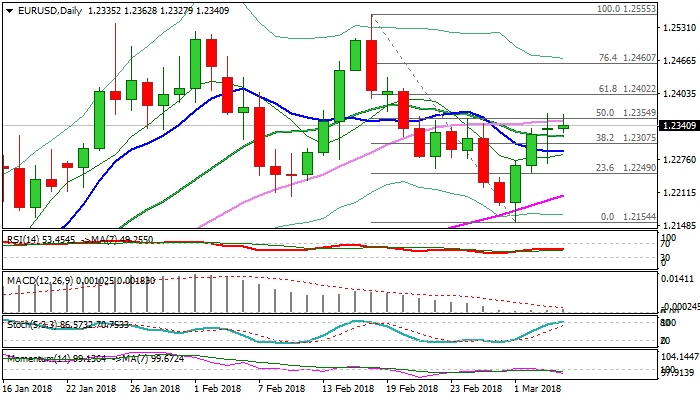

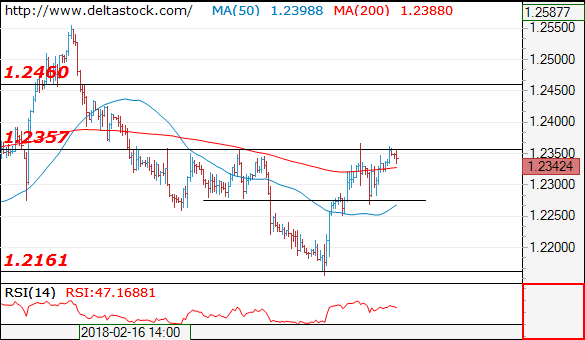

EUR/USD

Current level - 1.2342

The resistance at 1.2360 is still intact, so intraday allow a downswing to 1.2280 support. A break through 1.2360 will target 1.2460.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2360 | 1.2460 | 1.2280 | 1.2160 |

| 1.2460 | 1.2560 | 1.2160 | 1.2090 |

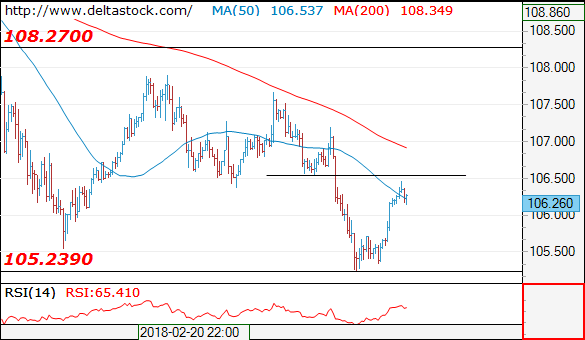

USD/JPY

USD/JPY

Current level - 106.26

The resistance at 106.50 should cap the upside, for a downswing to 105.20 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 106.50 | 108.30 | 105.70 | 105.40 |

| 107.60 | 110.40 | 105.20 | 102.40 |

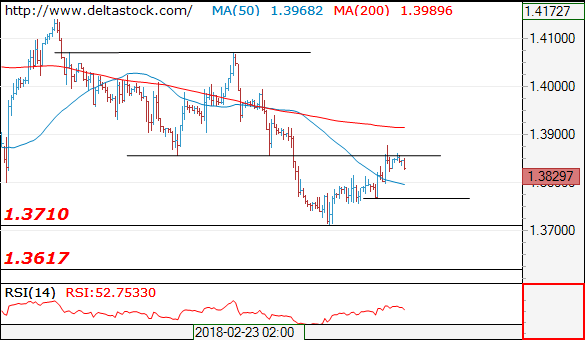

GBP/USD

Current level - 1.3829

The corrective rebound reached 1.3850 resistance and a break through 1.3765 will unleash a sell-off towards 1.3620 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3850 | 1.4280 | 1.3765 | 1.3620 |

| 1.4070 | 1.4340 | 1.3620 | 1.3620 |

Fundamentals: Gold And Oil

- Gold holding on to gains

- US Oil production makes headwinds strronger

Gold

Softness in the dollar index is helping the precious metal- gold. The dollar weakness is triggered because of the worries around the global trade war. Donald Trump, the US president, is facing strong political pressure to soften his stance towards his announcements of trade tariffs.

If the new form of NAFTA deal is signed and becomes a reality, he may change his mind towards these tariffs. Investors will also be looking to learn more from FOMC member Brainard about his stance on the interest rate hikes.

Oil

Investors piled their bets by buying crude oil which helped the crude. The IEA fuelled the rally in the oil price by saying global oil demand is expected to grow. The oil price has been consolidating for the past few days and this was the break which the market needed.

However, the surge in the US crude oil production remains the threat and this is weighing on the price.

Forex, Gold, Oil And Cryptocurrencies

- Risk appetite returns

- Gold back in demand

- Growing demand helping oil

Forex

Traders’ appetite for risk returns as trade war worries ease, restoring faith in the dollar. USD ISM Services data beating analyst expectations added a fresh impetus for investors to long the dollar sending it 0.5% higher against the yen. Its gains weren’t so prosperous against the dollar however, up only 0.1% after Italian election results strengthened the case to back the euro. A major determinant for EUR/USD will be Thursday’s ECB interest rate decisions. Although a rate rise is virtually ruled out at this stage, it will nonetheless be important to gauge hawkishness to provide an indication of when QE will be wrapped back. Elsewhere, positive UK PMI data succeeded in pushing the pound higher against the dollar.

Gold

With Wall Street extending Friday’s late rally and the dollar rising 0.1% against a weighted basket of currencies, Gold dropped down to $1320/ounce. The precious metal is now trading in a historical area of support and resistance but if risk appetite continues to strengthen, the safe haven asset could drop a bit further than anticipated.

Oil

Oil prices gained ground amidst report of further stockpile declines at the key US storage and delivery point of Cushing, with Crude Oil jumping to $62.5. However, if the US equity markets continue to weaken, we may not be through the worst yet.

Cryptocurrency

The market cap for this new asset class continues to creep higher as crypto fundamentals strengthen even further. China’s CPPCC conference confirms that while China has already clamped down on ICOs and fiat to crypto trading, the government will step up its support for turning block chain technology into real-life applications. Adoption is already well underway in Europe with European Banks completing their first live securities transfer on R3’s block chain platform, strengthening the bullish case.

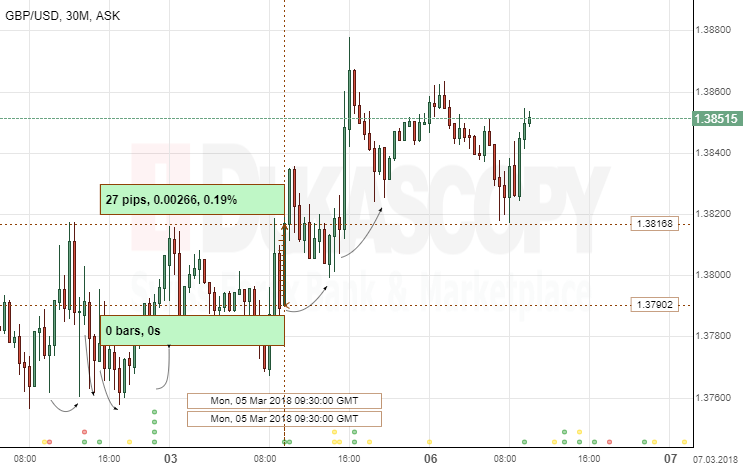

GBP/USD: UK Services PMI

The Sterling rallied against the US Dollar in the wake ofthe report by Markit on the UK services industry. The GBP/USD exchange rate gained 27 base points or 0.19% to the 1.3816 mark to continue fluctuating in the 1.3810 area.

Britain's economy notably strenghtened its growth pace in February, following the prior month, ending the weakest period since the recession of 2009. According to the IHS Markit report, the UK Services PMI rate grew to 54.5, compared to 53.0 in the previous month, topping the estimate of 53.3. Economists believe Britain is likely to sustain its growth rate as of late 2017. However, the resistance from weak consumer spending and cautious investors could persist.

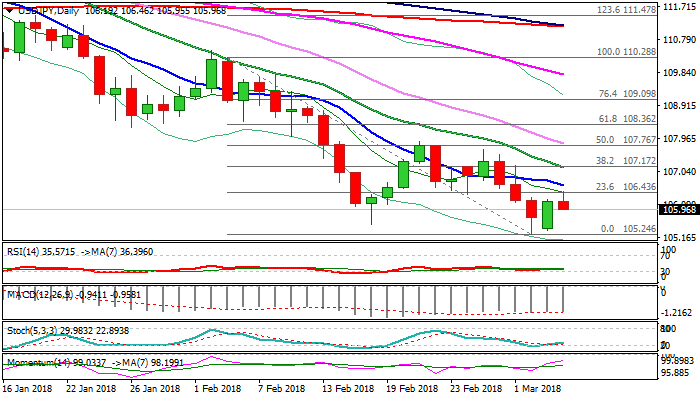

Technical Outlook: USDJPY – Limited Recovery But Immediate Downside Risk Is Sidelined

The pair eased from session high at 106.44, where Fibo 23.6% of 110.28/105.24 fall capped the extension of Monday's strong rally.

Bounce from new 16-month low at 105.24 sidelined immediate downside risk, however, daily techs remain in full bearish setup and keep the pair under strong pressure.

Near-term action may hold in extended consolidation as slow stochastic emerged from oversold territory, with stronger upticks to be capped at 107 zone (Fibo 38.2% of 110.28/105.24 / falling 20SMA) ahead of release of US NFP data which could provide stronger signal.

Res: 106.44, 106.63, 107.15, 107.52

Sup: 105.95, 105.54, 105.24, 105.00

Dollar Little Changed As Equities Rebound, Trade Considerations Still In Focus

Here are the latest developments in global markets:

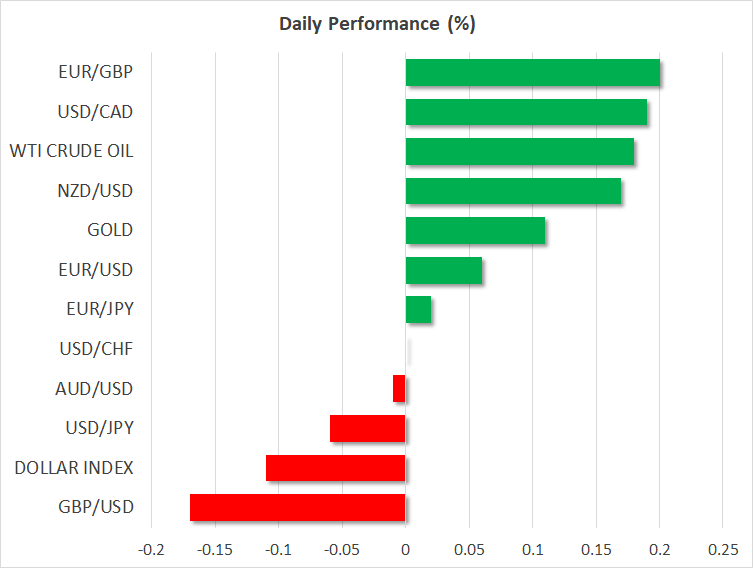

FOREX: The dollar index was slightly down on Tuesday after gaining less than 0.2% on Monday, in an environment where concerns for a trade war following the Trump administration’s decision to impose tariffs on imported steel and aluminum were easing.

STOCKS: US markets closed markedly higher yesterday, recovering some of their latest losses, as concerns over a potential trade war receded somewhat. The gains came after US House Speaker Paul Ryan urged the President to reconsider his tariffs, sending the message that not even the Republicans are comfortable with such measures. The Dow Jones led the charge, gaining nearly 1.4%. The S&P 500 rose by 1.1%, while the Nasdaq Composite followed in its track, up by 1.0%. Futures tracking the Dow, S&P, and Nasdaq 100 are all flashing green as well. Asian markets took their cue from the US and surged. In Japan, the Nikkei 225 and the Topix finished higher by 1.8% and 1.3% respectively, while in Hong Kong, the Hang Seng trade higher by 2.3%. Europe was a similar story. Futures tracking all the major indices were a sea of green today, pointing to a higher open for these benchmarks.

COMMODITIES: In energy markets, oil prices staged a comeback yesterday, as risk sentiment recovered. Commodities like oil are considered relatively risky and are thus quite sensitive to changes in investors’ risk appetite. Both WTI and Brent crude are higher by 0.2% today, extending the gains from yesterday. Today, traders will look to the release of the private API inventory data, which tend to set the tone for what to expect from the official EIA data, due out tomorrow. In precious metals, gold was higher but only by 0.1%, last seen near the $1320 per ounce mark. Gold traded lower yesterday, as diminishing concerns over a trade war likely decreased the yellow metal’s allure, a reaction seen in other safe havens as well, such as the Japanese yen and the Swiss franc.

Major movers: Dollar little changed as trade fears recede; loonie under pressure

Major movers: Dollar little changed as trade fears recede; loonie under pressure

The dollar’s index against a basket of currencies was 0.1% down amid receding worries for a trade war following last week’s decision on tariffs by US President Donald Trump. Pressure on Trump – coming from House Speaker Paul Ryan as well – to reconsider his decision, may have acted as a catalyst for market concerns to ease.

Equity markets gaining is also an indication that market participants are becoming less worried of the situation. Still, with things looking fluid, it should be said that markets may be running ahead of themselves.

Dollar/yen was little changed at 106.13 after rising on Monday. This compares to Friday’s 16-month low of 105.23 when the yen was attracting safe-haven flows on the back of uncertainty over trade. Also yen-related, the currency didn’t react much after Bank of Japan Governor Haruhiko Kuroda said on Tuesday that there were downside risks to the central bank’s forecast that inflation would reach its 2% target around the fiscal year ending in March 2020.

In other closely watched pairs: euro/dollar was not much changed at 1.2335, with the pair recording a two-week high of 1.2365 on Monday, a day during which uncertainty following Sunday’s Italian elections was dominating attention. Brexit-sensitive sterling was 0.15% down versus the greenback at 1.3830.

Dollar/loonie has been a pair that has been attracting additional interest lately, as Canada is the largest exporter of steel to the US. The Canadian dollar has come under increased pressure on the tariffs story, with dollar/loonie rising to 1.30 on Monday, this being an eight-month high. The pair was 0.2% up at 0731 GMT, trading close to the aforementioned peak. Trump’s intention to use the proposed tariffs on steel and aluminum to gain leverage in NAFTA talks is not helping the Canadian currency either. It should also be noted that the Bank of Canada meets tomorrow, and some of the recent softness in the CAD likely reflects expectations that policymakers may strike a concerned tone, amid heightened trade risks.

The Australian dollar was roughly flat at $0.7762, with minimal reaction to the Reserve Bank of Australia’s decision to keep interest rates steady at the record low of 1.5%, though there were some concerns as the central bank was cautious on the outlook for growth. Kiwi/dollar was higher by around 0.2%, at 0.7237.

Day ahead: Trade considerations to remain at the forefront on quiet calendar day

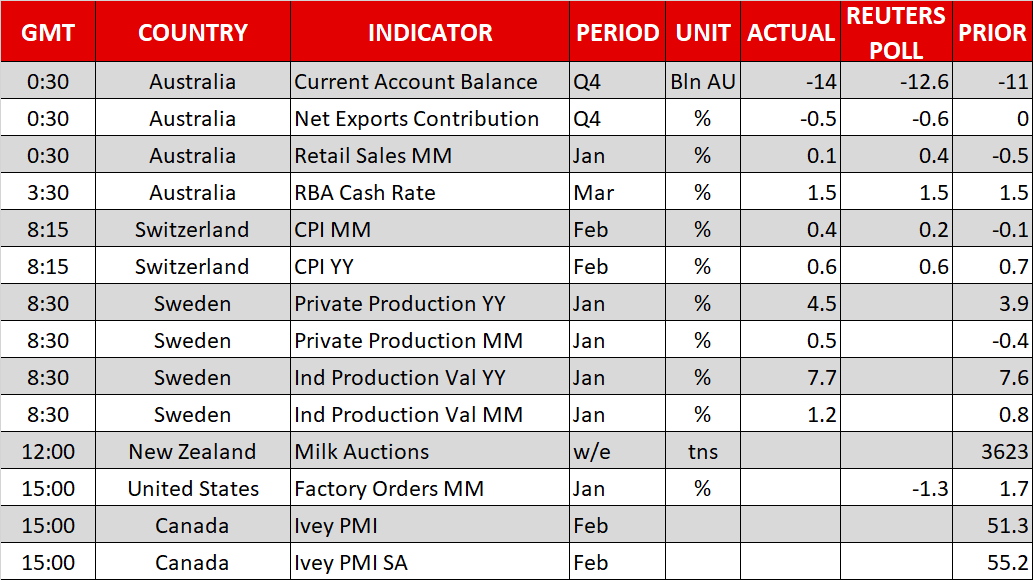

The economic calendar is relatively light today, with only second-tier releases on the agenda. In the US, factory orders for January are due out at 1500 GMT, and the forecast is for the figure to have dropped by 1.3% in monthly terms, a turnaround following a 1.7% rise previously.

In Canada, the Ivey PMI for February will be in focus (1500 GMT), ahead of the Bank of Canada’s rate decision tomorrow.

Elsewhere, NZD traders will keep their eyes on the bi-weekly milk auction. The release is tentative, lacking a specific time, but most economic calendars have it marked for 1200 GMT. While there is no forecast available for the figure, it tends to be a market mover for the kiwi dollar, considering New Zealand’s status as a major dairy exporter.

On the Brexit front, the EU is anticipated to publish its draft guidelines for a post-Brexit trade deal, though media reports suggest these are likely to be relatively short and vague, allowing room for the UK to clarify what it wants in the coming weeks.

In energy markets, oil traders will turn their sights to the private API weekly inventory data that will be released at 2130 GMT.

Equity investors will probably remain focused on any comments regarding tariffs and global trade, as they try to gauge the probability of a trade war materializing. While price action yesterday was driven by expectations that Congress will serve as a hurdle to tariffs, it’s important to note that a few hours later, President Trump said he is not backing down on the issue. Over the coming days, markets will be looking for fresh clues as to whether this rhetoric is simply posturing in complex trade negotiations, similar to the “fire and fury” remarks, or whether the US President will stick to his guns and risk a tit-for-tat retaliation by other nations.

Regarding policymakers’ appearances, we will hear from New York Fed President William Dudley (a permanent FOMC voting member) at 1230 GMT. Next in line will be the Bank of England’s chief economist and MPC member Andy Haldane, who will deliver remarks at 1800 GMT. While neither Dudley’s, nor Haldane’s topics of discussion are related to monetary policy directly, comments on the subject are always a possibility from these highly-influential policymakers. The Governor of the Reserve Bank of Australia, Philip Lowe, will also step up to the rostrum at 2135 GMT.

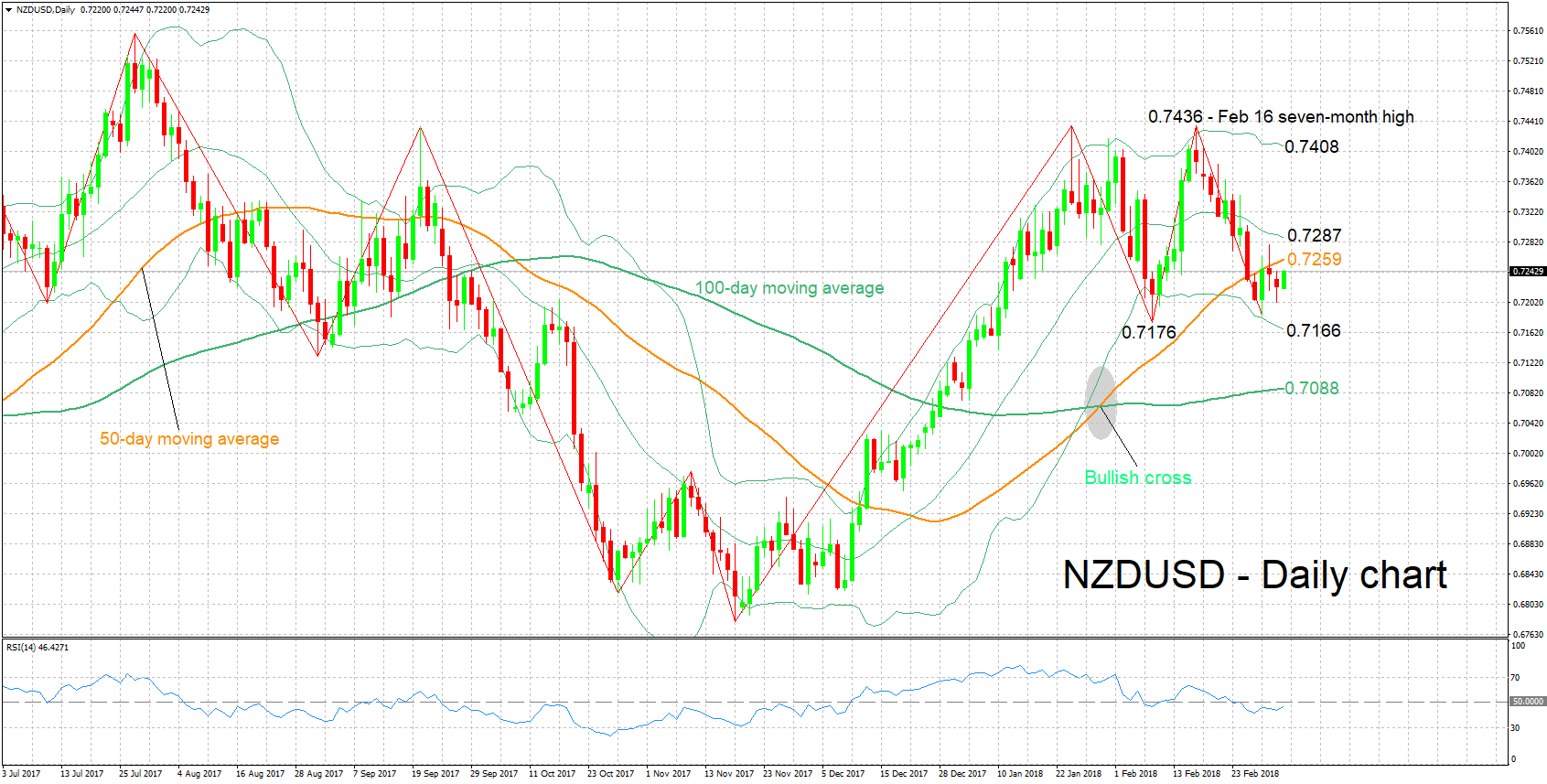

Technical Analysis: NZDUSD looking neutral ahead of milk auction

NZDUSD has distanced itself to the upside from the one-month low of 0.7185 hit last Thursday. The RSI has halted its decline and has been moving sideways for the most part in recent days, pointing to a neutral picture in the short-term.

Should today’s bi-weekly milk auction show a rise in prices, then the pair might receive a boost; New Zealand is a major dairy exporter. Resistance in this case might come around the 50-day moving average at 0.7259, with stronger gains shifting the focus to the middle Bollinger line – a 20-day moving average line – at 0.7287.

If on the other hand milk prices surprise to the downside, NZDUSD could record losses. In this scenario, support could come around the lower Bollinger band at 0.7166. The area around this level also includes last week’s one-month low of 0.7185, as well as the two-month low of 0.7176 that was recorded on February 8.

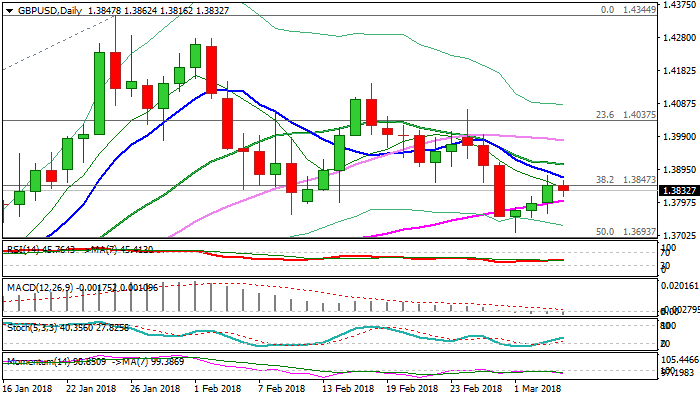

Technical Outlook: GBPUSD Holds In Narrowing Range Between 55 And 10SMA, But Negatively Aligned Techs Keep The Downside Vulnerable

Cable showed little action in Asia / early Europe on Tuesday but holding in red for now after upside attempts stalled on approach to descending 10SMA (1.3871).

The pair is trading in the middle of thick daily cloud, with today's action holding within narrowing range, defined by falling 10 SMA and ascending 55SMA (1.3804).

Initial signs of stall of recovery leg from 1.3711 (01 Mar trough) are developing but need reversal and close below 55SMA for stronger negative signal.

Bearish momentum studies on daily chart support negative scenario, along with falling 10/20/30 SMA's in firm bearish setup.

At the upside, falling 10SMA marks initial barrier, break of which would look for confirmation of bullish signal on lift above 20SMA (1.3908) to expose pivotal barrier at 1.3944 (daily cloud top).

With no releases from the UK scheduled for today, the pair is expected to be driven by techs and news.

Res: 1.3871, 1.3908, 1.3944, 1.3979

Sup: 1.3862, 1.3804, 1.3766, 1.3740

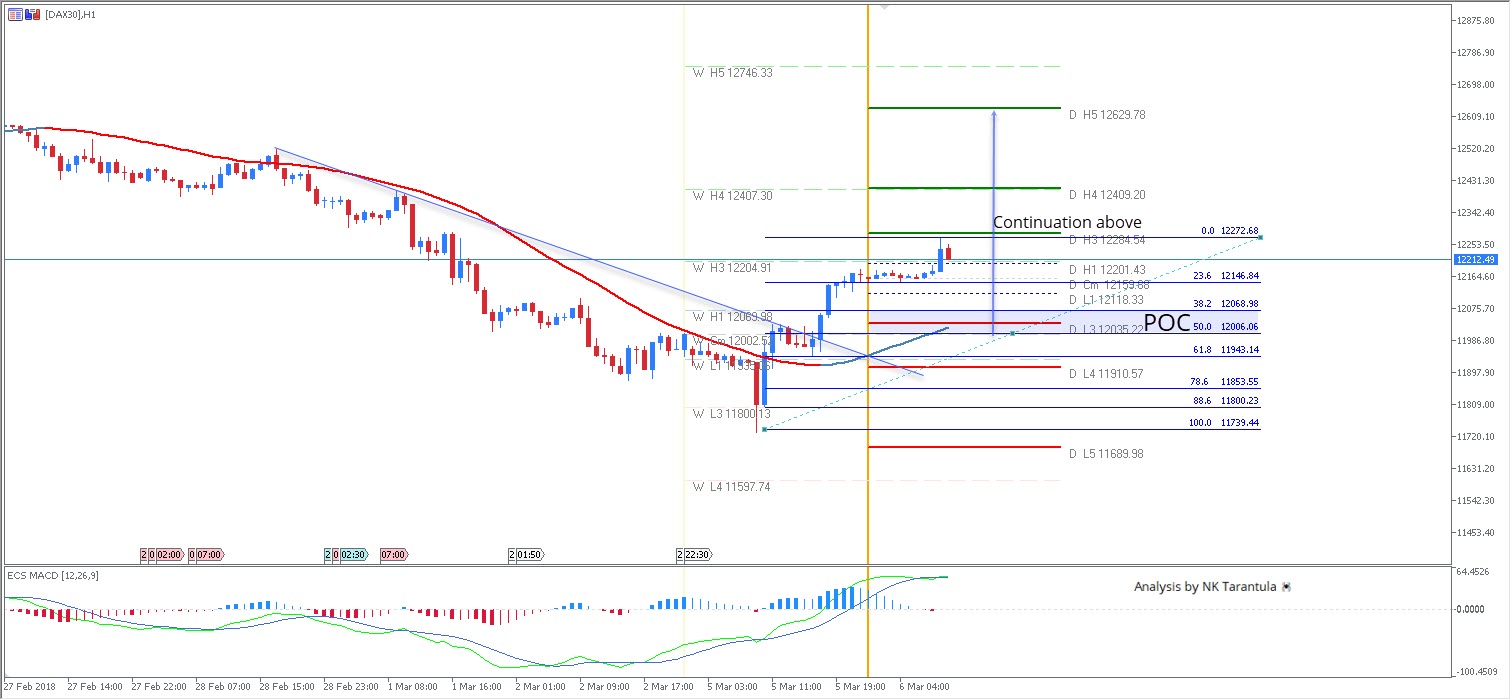

DAX30 Bouncing After The Trend Line Break

The DAX30 made a break above the trend line and EMA89 and currently it's above W H3 level that further confirms its bullishness. The retracement into the POC zone 12005-12070could show fresh buyers, and the price might spike towards W H3 again. Further continuation above the W H3 pivot is targeting W H4/ D H4 confluence -12409 with the final target at 12629 but only if there is an apparent 4h close or strong 1h breakout above 12410.

- W H3 -Weekly Camarilla Pivot (Weekly Interim Resistance)

- W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

- W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 – Daily Camarilla Pivot (Daily Support)

- D L4 – Daily H4 Camarilla (Very Strong Daily Support)

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Eurozone retail PMI rose to 52.3 in Feb, up from Jan’s 50.8

Eurozone retail PMI rose to 52.3 in Feb, up from Jan's 50.8.

Key points from release

- Headline Retail PMI rises to 52.3 from 50.8 in January

- Sales broadly unchanged on annual basis

- Gross margins remain under pressure

Quote:

"The latest data highlight another positive month for the eurozone retail sector, with sales up at a quicker pace on a monthly basis. In turn, this contributed to a renewed bout of optimism, with the survey's measure of business confidence among the highest over the last year. Further expansions in purchasing activity and employment underscore retailers' positive outlook. Nevertheless, gross margins continued to be squeezed, suggesting business conditions remain challenging."

Technical Outlook: EURUSD – Directionless Near-Term Action Looks For Fresh Signal, ECB And EU GDP Data Eyed

The Euro holds in tight range in early hours of the European session, showing no clear direction after Monday’s trading ended in long-legged Doji, signaling strong indecision.

Three-day recovery from 1.2154 (01 Mar low) faced strong headwinds at 1.2350 zone, where 30SMA and the mid-point of 1.2555/1.2154 downleg continue to cap the advance.

Repeated probes above 30SMa were so far unsuccessful, with fears reversal after repeated upside rejections remaining in play.

Fresh bearish momentum is building on daily chart and along with overbought slow stochastic, keeping the downside vulnerable.

On the other side, thickening daily cloud continues to underpin after Monday’s dip was contained by cloud top which currently lies at 1.2264.

The pair is in near-term directionless mode and looking for a catalyst for fresh direction. Releases of EU Q4 GDP on Wednesday and ECB rate decision on Thursday are focused for stronger signals.

Firm break above 30SMA is needed to generate fresh bullish signal for continuation of recovery leg from 1.2154 towards next strong barrier at 1.2400 (Fibo 61.8% of 1.2555/1.2154 downleg.

Conversely, initial bearish signal could be expected on break below 20SMA (1.2320) with extension through daily cloud top needed to generate stronger bearish signal and shift near-term focus lower.

Res: 1.2350, 1.2364, 1.2400, 1.2435

Sup: 1.2320, 1.2307, 1.2291, 1.2264