Sample Category Title

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8878; (P) 0.8913; (R1) 0.8941; More...

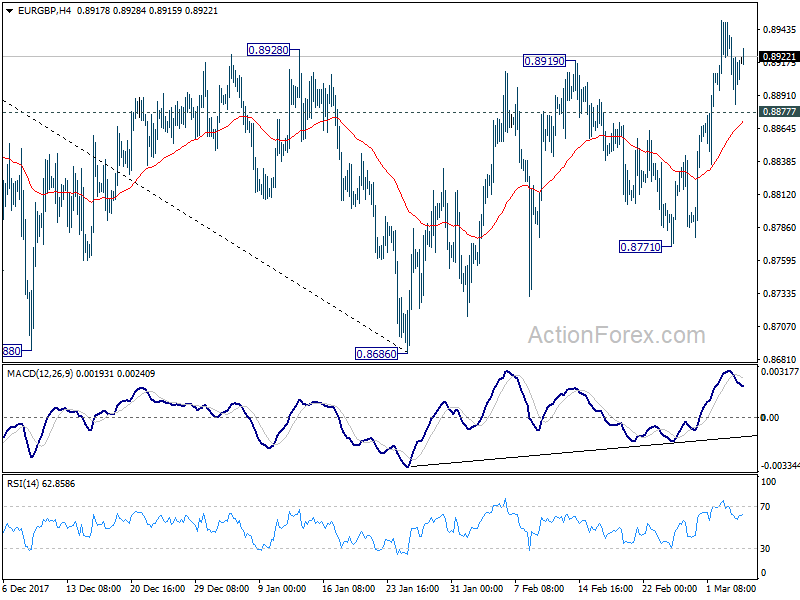

At this point, further rise is still expected in EUR/GBP. Prior break of 0.8928 resistance indicates near term trend reversal. Decline from 0.9305 has completed at 0.8686 after hitting 61.8% retracement of 0.8312 to 0.9305. Further rise should be seen back to 61.8% retracement of 0.9305 to 0.8686 at 0.9069. Firm break there will target retest of 0.9305 high. On the downside, below 0.8877 minor support will dampen this bullish view and target 0.8771 support instead.

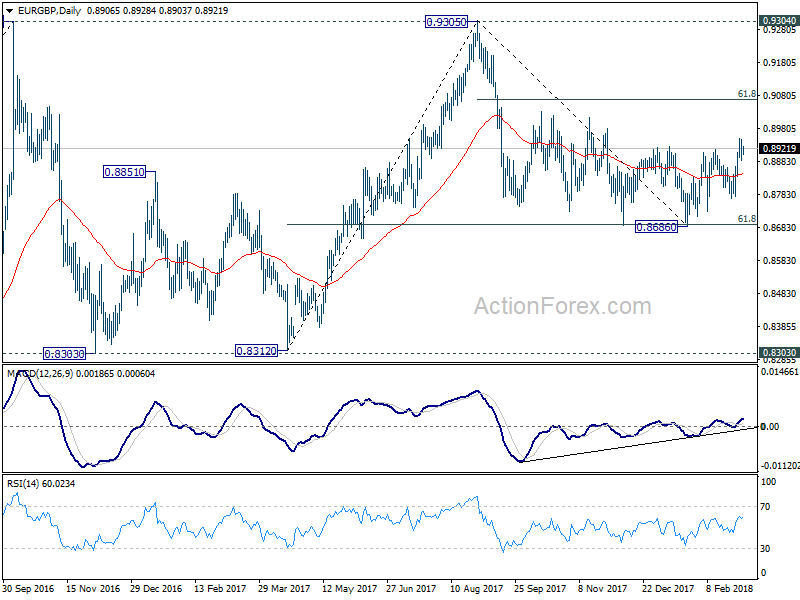

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to conf

irm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

irm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Market Update – Asian Session: Equities Track Higher Following US

Headlines/Economic Data

General Trend: Asian equity markets rise amid rebound in steel makers and earlier gains in the US

Asian automakers also trade generally higher

Energy producers gain after rise in oil prices on Monday

RBA expects faster economic growth in 2018 vs 2017; notes wage growth ‘appears to have troughed’

Weaker yen boosts Japanese exporters, especially auto makers

Australia Q4 Net Exports expected to subtract from GDP; Q4 GDP data due on Wednesday’s session

Korean Won (KRW) gains over 0.5% versus US dollar as talks between the two Koreas in focus

Australia/New Zealand

ASX 200 opened +0.3: closed +1.1%

ASX 200 Energy Index +2%, Utilities +1.8%, Telecom +1.6% Resources +1.5%, Consumer Discretionary +1.1%, Financials +1%

NZM.NZ Terminates merger agreement with Fairfax’s Stuff Limited, will continue with appeal

(AU) Australia Q4 Current Account (A$): -14.0B v -12.2Be; Net Exports of GDP: -0.5% v -0.6%e

(AU) AUSTRALIA JAN RETAIL SALES M/M: 0.1% V 0.4%e

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED

Looking ahead: Australia Q4 GDP data due to be released on Wed, RBA Gov Lowe scheduled to speak (topic: ‘The Changing Nature of Investment’)

China/Hong Kong

Shanghai Composite opened flat, Hang Seng -0.2%

Hang Seng Energy Index +2.7%, Info Tech +2.6%, Materials +1.8%, Services +1.3%, Consumer Goods +1.2%, Financials +1.2%

(CN) China PBoC monetary policy expected to be more flexible this year; Should cut RRR to prevent risks from slower growth - China Securities Journal

(CN) According Financial Stability Board (FSB) stats China shadow banks account for 15% of global market, with ~$7T of the global $45.2T global shadow banking assets

(CN) China PBoC Open Market Operation (OMO): Skips reverse repo operations for the 2nd consecutive session; Net drain nil v CNY100B prior

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3386 V 6.3431 PRIOR

Japan

Nikkei225 opened +1.7%; closed: +1.8%

TOPIX Iron & Steel +2.4% Index, Electric Appliances +2.3%

Cosmetics company Shisheido [4911.JP] gains over 4% following release of FY18-20 corporate strategy

(JP) Barclays pushes back forecast for BoJ policy changes to 2019 – US financial press

(JP) Top analysts say a worsening in trade concerns could weigh on foreign demand for Japanese equities – US financial press

(JP) Japan Trade Min Seko: Japanese products contribute to US growth and jobs

(JP) Japan's Persol, Recruit, and other major human resource firms to start providing commutation allowances for temporary workers in administrative positions from April this year as labor shortages become an increasingly serious issue - Nikkei

(JP) Japan Cabinet approves plan to improve the accuracy of prelim GDP data - financial press

(JP) Japan Govt approves signing of TPP FTA without the US - Nikkei (to happen later this week in Chile)

(JP) Japan MoF sells ¥800B v ¥800B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.75% v 0.820% prior; Bid to cover: 4.24x v 4.27x prior

(JP) BoJ Gov Kuroda: BOJ is keeping policy very accomodative, takes time to get rid of deflationary mindset - Confirmation Hearings

Looking Ahead: Additional confirmation hearings for the BoJ Dep Gov Nominees (Amamiya, Wakatabe) set for Wed, March 7th

Korea

Kospi opens +1.1%

Shares of Samsung Electronics gain over 3% (declined ~1.8% on Monday’s session)

LG Display’s shares underperform amid cautious broker commentary

(KR) North Korea and South Korea hold high level talks today, North Korea has a "firm will" to advance relations with South Korea. Kim Jung Un has agreed to meet with South Korea President Moon after successful talks.

(KR) SOUTH KOREA FEB CPI M/M: 0.8% V 0.5%E; Y/Y: 1.4% V 1.2%E

(KR) South Korea Jan Current Account: $2.68B v $4.1B prior; Balance of Goods (BOP): $8.11B v $8.2B prior

(KR) South Korea to talk about revision of property holding tax - Korean press

(KR) South Korea to challenge US steel tariffs in G20 - Korean press

(KR) South Korea to announce scale and date of military drills with US after the 18th (were delayed due to Olympics)

(KR) South Korea sells 30-yr bonds; avg yield 2.735%

Other Asia

(PH) Philippines Feb CPI M/M: 0.8% v 1.0% prior; Y/Y: 4.5% v 4.1%e (Highest annual pace since 2014)

Punjab National Bank [PNB.IN] Foreign banks said to stop sales of gold to the bank - Indian Press

North America

US equity markets ended broadly higher: Dow +0.7%, S&P500 +0.8%, Nasdaq +0.7%, Russell 2000 +0.7%

S&P500 Utilities +2%, Financials +1.4%, Real Estate +1.4%

(US) On Thursday (Mar 8th), US President Trump expected to discuss impact of planned tariffs with US companies that use aluminum and steel - US financial press

(US) President Trump: Will not back down on trade; I don't think we will have a trade war; Reiterates threat to raise tax on car imports

LOGI Guides initial FY19 Rev growth in 'high single-digit'; Op $310-320M; affirms FY18 Rev +12-14% y/y; Op $270-280M

Looking ahead: US Weekly API Crude Oil Inventories due for release

Europe

(UK) Reportedly the EU's initial offer on trade will not be very detailed; The lack of detail in the offer would leave the UK having to renegotiate large parts of its trade agreement with the EU during the post-Brexit period. The UK has been seeking to have the entire trade accord squared away before the March 2019 Brexit – press

(UK) Senior EU Brexit negotiator Rynck: not likely that there will be certainty about future ties to the EU by this fall [*Note: previously EU had sought to wrap up trade negotiations by Nov]

(UK) Feb BRC Sales LFL y/y: 0.6% v 0.5%e

OPEC Sec Gen Barkindo: Demand has not been this solid and positive since before the financial crisis; Have to wait on a decision about whether production cuts will be extended into 2019; Shale producers are interested in a dialogue with OPEC, but will not be discussion production cuts or prices

Telecom Italia [TIT.IT]: Elliott said to build stake in the company - US financial press

Levels as of 01:00ET

Hang Seng +1.7%; Shanghai Composite +0.8%; Kospi +1.5%

Equity Futures: S&P500 +0.0%; Nasdaq 100 +0.2%, Dax +0.1%; FTSE100 -0.1%

EUR 1.2332-1.2363; JPY 106.16-106.47; AUD 0.7761-0.7792 ; NZD 0.7203-0.7245

Apr Gold +0.3% at $1,324/oz; Apr Crude Oil +0.2% at $62.70/brl; Mar Copper +0.5% at $3.14/lb

Asian Equity Indices Have Followed Their US Counterparts Into Green Territory

Market movers today

In terms of data there are no global market movers in today's session and markets will continue to focus on Trump's protectionist measures and possible counter -measures from countries hurt by the announced tariffs. The political situation in Italy will also be on the radar.

The EU is expected to publish its draft guidelines for the future relationship between the UK and EU today. According to the press, we should not expect very detailed guidelines, as the EU wants the UK to concretise the relationship it wants.

The Fed's Vice-Chairman Bill Dudley is set to participate in a roundtable discussion on St . Thomas, but the subject is the effect of the hurricanes on the Virgin Islands and Puerto Rico. Therefore, it is unlikely he will address the out look for monetary policy.

Meanwhile, in the Scandies, the big event of the day is Norges Bank's Regional Network Survey, which is t he cent ral bank's preferred indicator of the economic out look. In Sweden, we will follow Riksbank Governor Stefan Ingves and Deputy Governor Henry Ohlsson at tending a parliamentary hearing as well as the release of industrial product ion data. For more information, see page 2.

Selected market news

Global risk appetite has improved at the beginning of the week as concerns of a global trade war stemming from more protectionist US policies have eased amid Republican lawmakers and influential investors publicly questioning Trump's intended tariffs on steel and aluminium. This morning, most Asian equity indices have followed their US counterparts into green territory, the USD has stabilised and US 10Y Treasury yields have risen 9bp from Friday's low.

Following the defeat of the Democratic Party (DP) at the Italian election, former Italian Prime Minister Matteo Renzi has resigned as DP leader. Meanwhile, Renzi will head t he part y's talks in the at tempt to create a new government and has re-emphasised that the DP will not enter a coalition with either the League or the Five Star – the two ant i-establishment parties that stand as winners following Sunday's vote. Going forward, the negotiations remain messy and the next important date will be 23 March when both houses of Parliament are due to come together for the first time. In our view, it remains unlikely that we will have an Italian government in place before May or June and at this stage we cannot rule out new elect ions in H2 this year.

The monthly house price sta istics from Real Estate Norway showed that house prices in Norway rose by a seasonally-adjusted 0.4% m/m in February, see chart. In addition, the details showed a further improvement in the sales-to-stock ratio, suggesting that house prices are very close to fully bottoming out . This reduces the downside risk of the economic out look ahead of today's Regional Network Survey an d next week's Norges Bank monetary policy meeting.

This morning, the Reserve Bank of Australia has as expected kept the cash rate unchanged at 1.5%. The accompanied statement was fairly neutral and AUD/USD is little changed post the announcement . Going forward, we st ill pencil in one rate hike over the coming 12M.

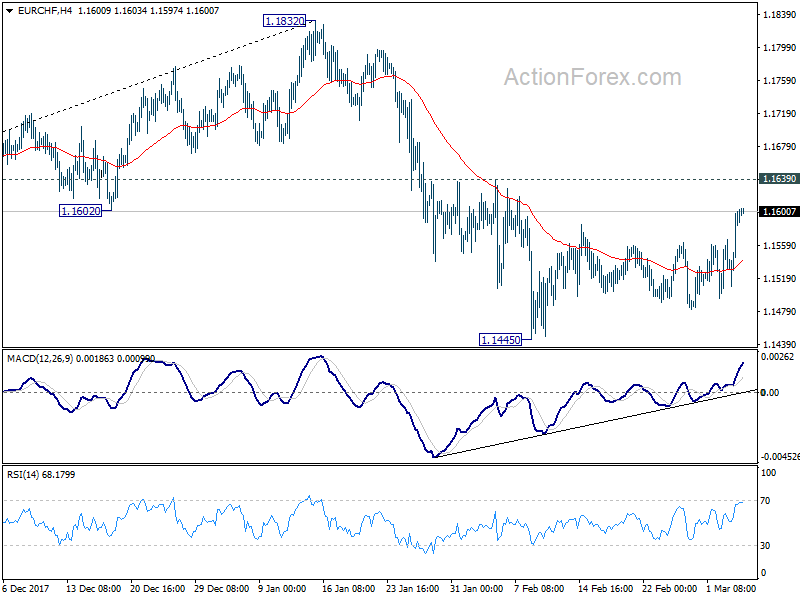

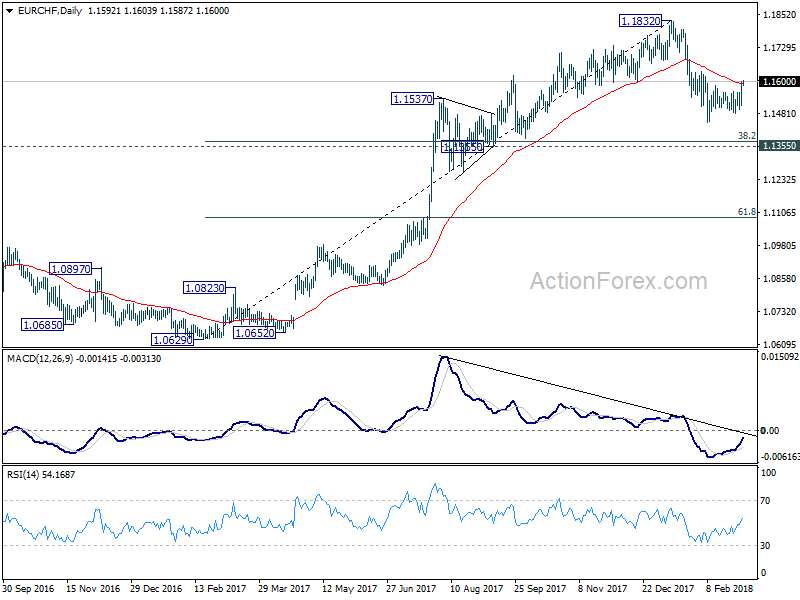

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1535; (P) 1.1567; (R1) 1.1626; More...

EUR/CHF reaches as high as 1.1603 so far as rebound from 1.1445 extends. However, price actions from 1.1445 are viewed as a corrective pattern. Hence, intraday bias remains neutral. Also, near term outlook will remain bearish as long as 1.1639 resistance holds. On the downside, break of will resume the corrective fall from 1.1832 and target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound. Nevertheless, break of 1.1639 will suggest short term reversal and turn bias back to the upside for 1.1832 high.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

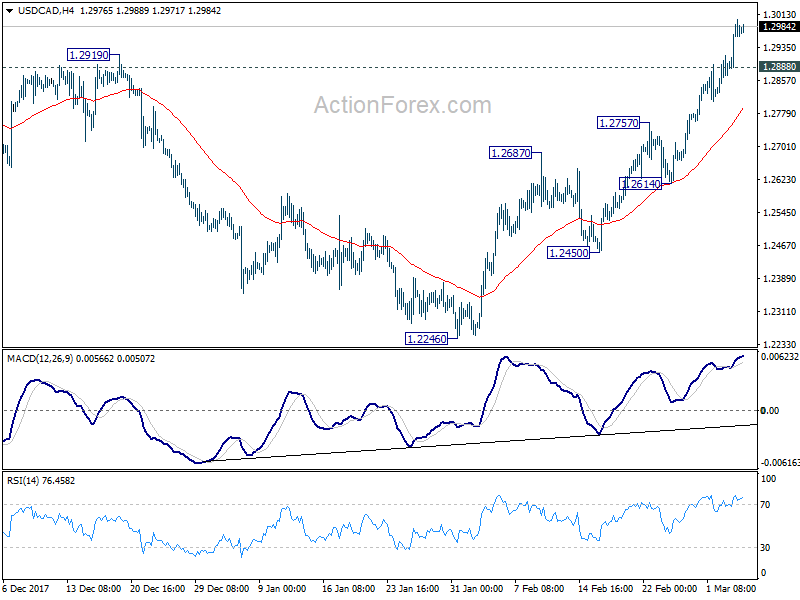

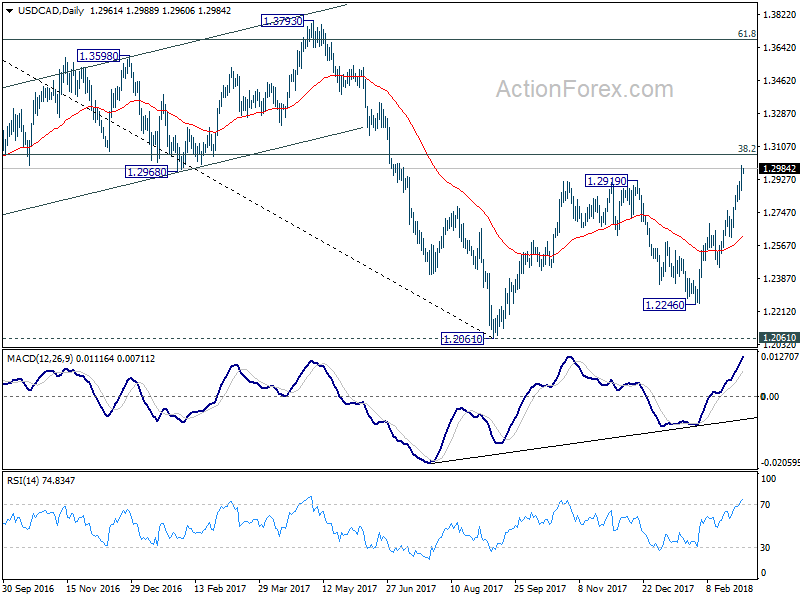

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2881; (P) 1.2941; (R1) 1.3023; More....

USD/CAD's rally is still in progress and intraday bias stays on the upside. Medium term rebound from 1.2061 is now extended to target 1.3065 fibonacci level next. On the downside, below 1.2888 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 1.2757 resistance turned support holds.

In the bigger picture, strong break of 1.2919 resistance adds much credence to the bullish case. That is larger down trend from 1.4589 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

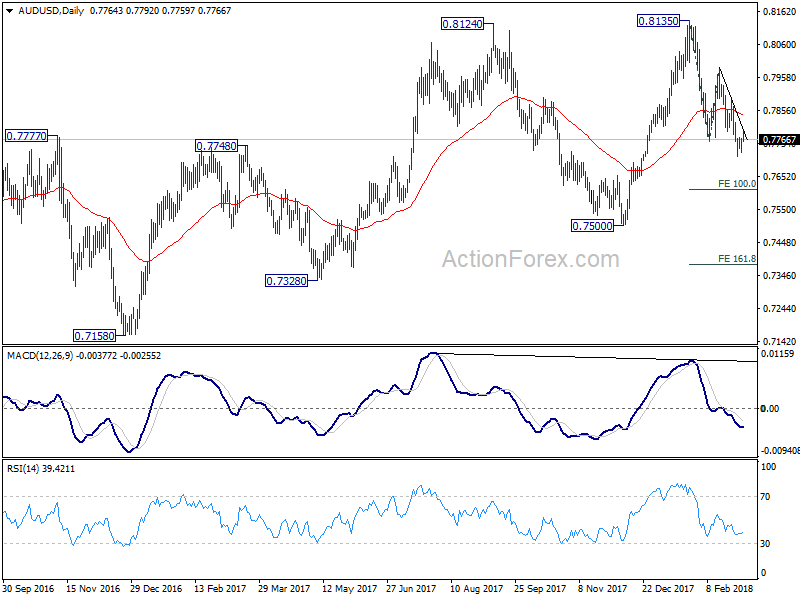

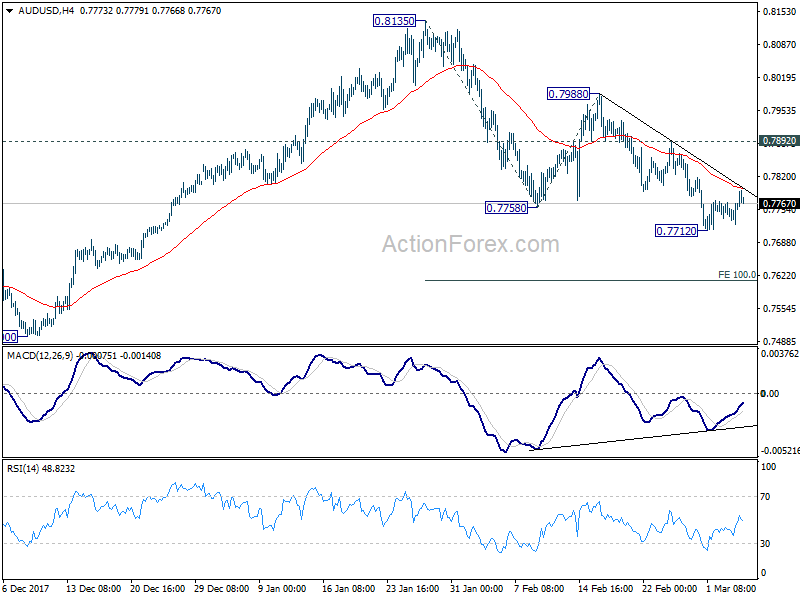

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7737; (P) 0.7754; (R1) 0.7782; More...

AUD/USD's consolidation from 0.7712 is still in progress and intraday bias remains neutral. Also with 0.7892 resistance intact, near term outlook remains mildly bearish. Break of 0.7712 will resume the decline from 0.8135 and target 100% projection of 0.8135 to 0.7758 from 0.7988 at 0.7611. Break there will put 0.7500 key support into focus.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

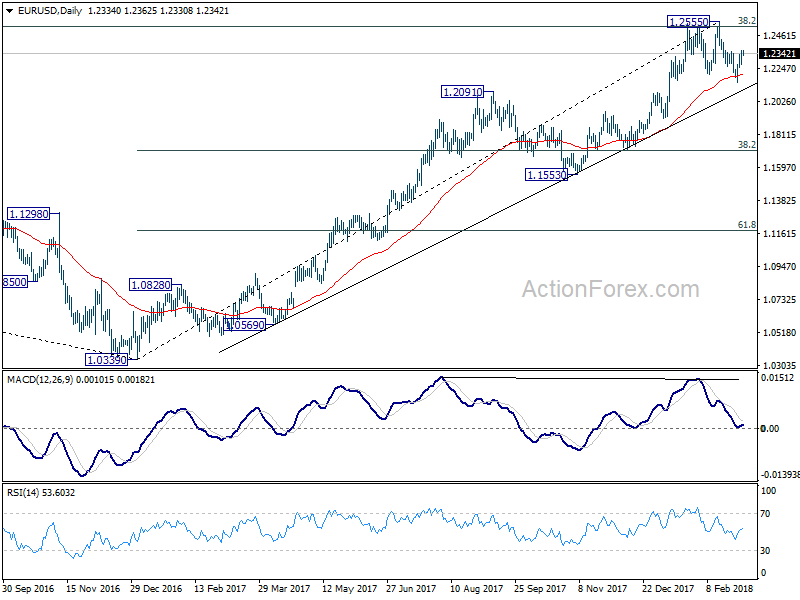

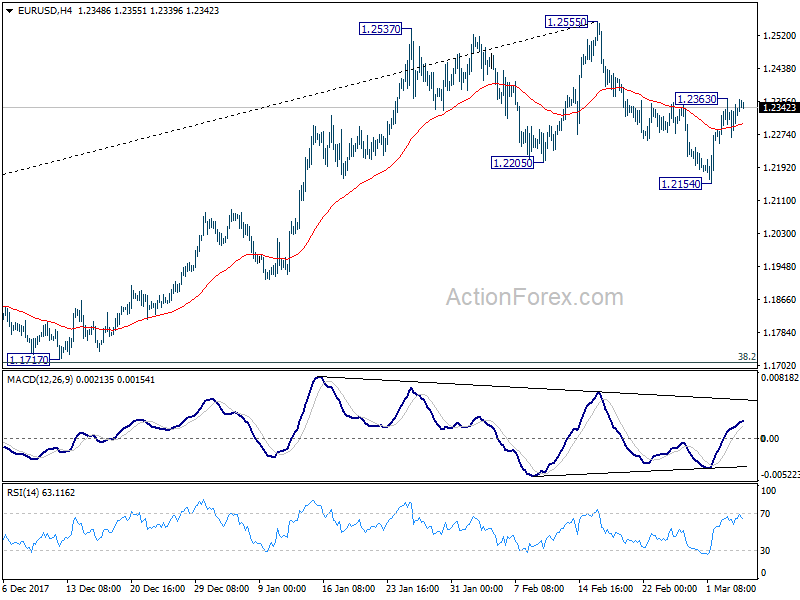

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2281; (P) 1.2323 (R1) 1.2376; More....

Despite the rally attempt, EUR/USD staying below 1.2363 minor resistance. Intraday bias remains neutral first. Break of 1.2363 should extend the rebound from 1.2154 to retest 1.2555 high. Firm break there will carry larger bullish implication. On the downside, break of 1.2154 would revive the case of rejection by 1.2516 key fibonacci level and trend reversal. Outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2555 at 1.1708.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

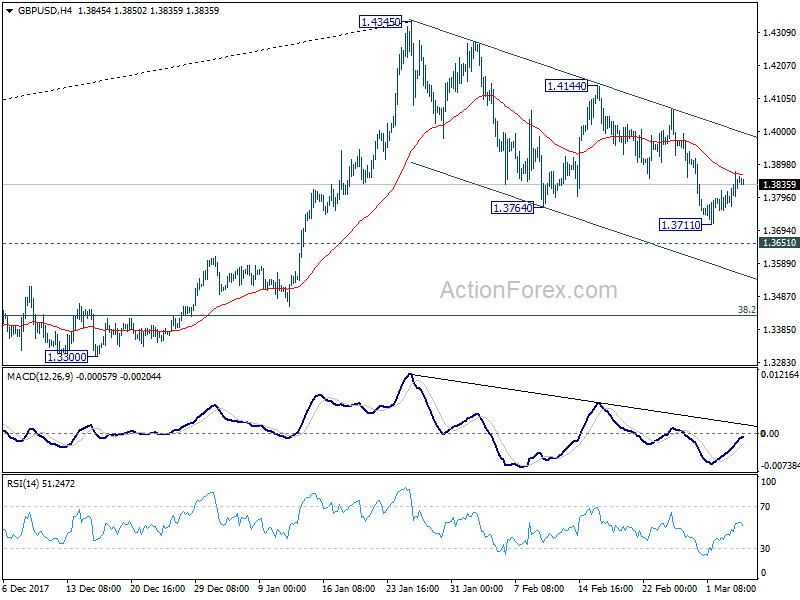

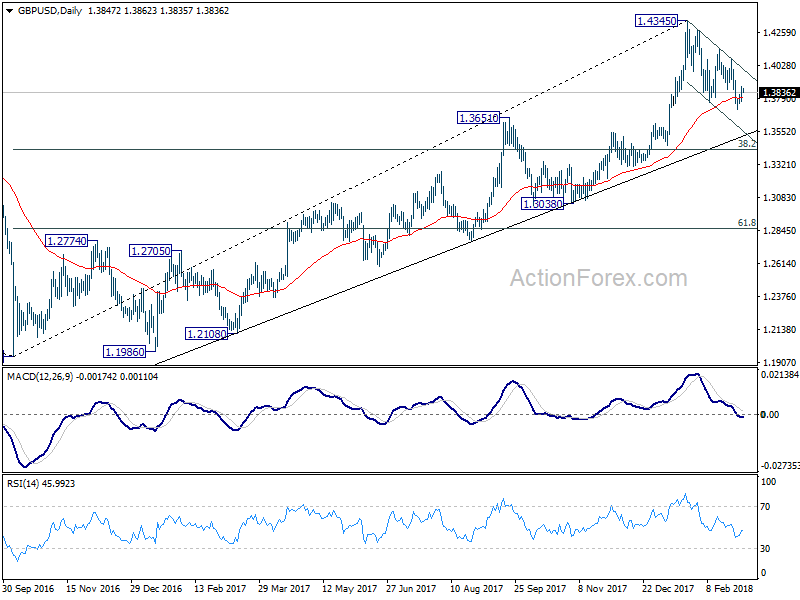

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3763; (P) 1.3789; (R1) 1.3824; More....

GBP/USD's corrective recovery from 1.3711 is still in progress and is pressing 4 hour 55 EMA. Intraday bias stays neutral at this point. And, near term outlook is still mildly bearish with 1.4144 resistance intact. Correction from 1.4345 would extend to 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

QE Details: More Of The Same In Volume Terms – Yet, Increasingly Distorted WAM

As expected, the QE figures for February showed PSPP share remained around 70% of the new purchase rate of EUR30bn. This is in line with expectations of the new purchase rate as of January this year. We continue to expect around 70% of the total APP will be allocated to the PSPP.

The major countries were bought close to the capital key, as there was no change in the cumulated capital key deviations among the major countries compared to January.

The weighted average maturity of German PSPP purchases increased significantly from 6.8 to 12.2 years. However, we emphasise that with an increasing amount of redemptions, one should be cautious when reading these estimates. If there were any PSPP redemptions in the ECB's holdings (for example, the OBL Feb-18 (org. 5Y bond) matured in February), this could 'distort' our average monthly maturity estimates. Hence, redemptions could add volatility to these figures going forward. We assign the significantly higher WAM to this.

The additional redemption details covering Feb-2019 underscore the presence of redemptions, with total QE redemptions in Feb-19 amounting to EUR11.8bn, of which EUR8.8bn is in PSPP. Total PSPP redemptions through to Feb-19 are EUR141bn

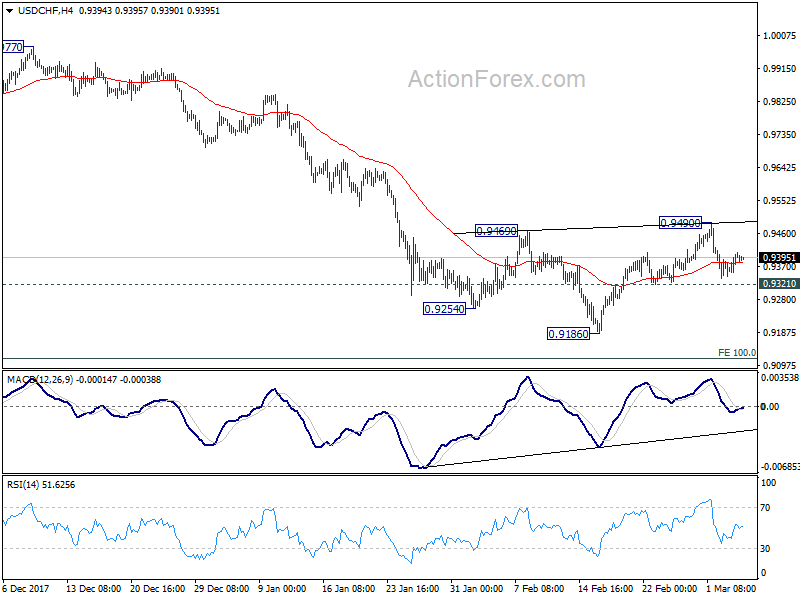

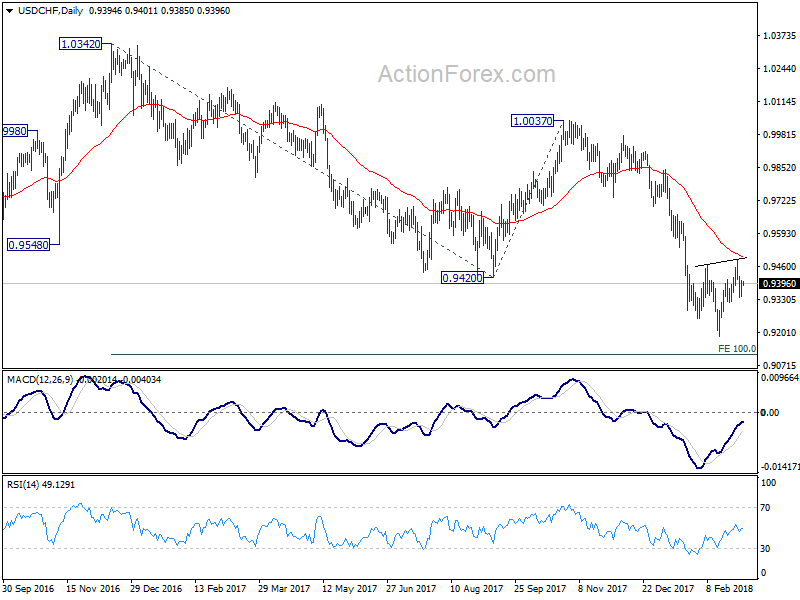

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9357; (P) 0.9382; (R1) 0.9423; More...

USD/CHF recovered ahead of 0.9321 minor support. But upside is limited below 0.9490 resistance. Intraday bias remains neutral first. On the downside, break of 0.9321 will indicate completion of the rebound from 0.9186. Intraday bias will be turned back to the downside for 0.9186 first. Break will resume larger down trend to 0.9115 projection level. On the upside, break of 0.9490 will revive the case of near term reversal, on bullish convergence condition in 4 hour MACD. In that case, outlook will be turned bullish.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.