Sample Category Title

Japanese Yen Pauses After Strong Week

The Japanese yen has edged lower in the Monday session. In North American trade, USD/JPY is trading at 105.96, up 0.20% on the day. On the release front, the sole Japanese event is the 30-year bond yield. In the US, the ISM Non-Manufacturing PMI slowed to 59.5, but managed to beat the estimate of 58.9 points.

It was a good week for the Japanese yen, which improved 1.3% on the week. The currency received a boost after Bank of Japan governor Haruhiko Kuroda said that the BoJ would consider exiting from its ultra-accommodative monetary policy if its inflation target of around 2020 was reached in early 2020. Kuroda’s remarks were unusual in that they mentioned a possible “exit” from its stimulus program, and this caught the markets off guard. The BoJ has been lagging behind the Fed and other central banks in winding up stimulus, but Kuroda added that the Bank would normalize policy if “economic conditions become favorable and our price target is achieved”. Although inflation remains well below target, any further hints at normalization could strengthen the yen.

The US dollar was broadly lower last week, after President Trump sent shock waves through the markets when he announced stiff tariffs on steel and aluminum, in order to protect domestic producers. Under the new scheme, foreign steel will be taxed at 25% and aluminum at 10%. The response to the move was overwhelmingly negative, both abroad and in the US. China and the EU immediately denounced the move. US auto makers and oil and gas producers also condemned the tariffs, saying they could get caught in the middle of a nasty trade war if other countries retaliate. In imposing the tariffs, Trump relied on a provision which allows such measures for national security, but clearly, US trading partners will not quietly accept these protectionist measures.

DOW correcting fall from 25800

DOW sees some solid buying today, up 200 pts at the time of writing. But it's more like a recovery that corrects the fall from 25800.35 to 24217.47. For now, the recovery could extend to 55 H EMA an or above. but strong resistance is likely between 25000/25200. Another fall to 23360.29 is still in favor for the near term.

CAD worst performing, threatened by Trump

CAD is clearly the worst performing one today threatened by Trump. He tweeted:

CAD is clearly the worst performing one today threatened by Trump. He tweeted:

- "NAFTA, which is under renegotiation right now, has been a bad deal for U.S.A. Massive relocation of companies & jobs,"

- "Tariffs on Steel and Aluminum will only come off if new & fair NAFTA agreement is signed."

A recap on top steel importers to the US in 2017

- Canada (16%)

- Brazil (13%)

- South Korea (10%)

- Mexico (9%)

- Russia (9%)

- Turkey (7%)

- Japan (5%)

- Taiwan (4%)

- Germany (3%)

- India (2%)

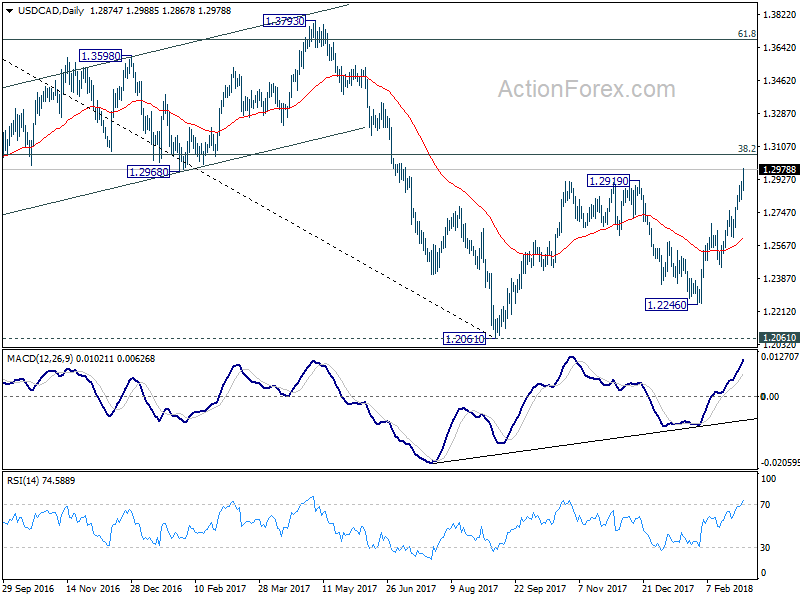

USD/CAD now heading to 1.3065 fibonacci level.

US: Non-Manufacturing Activity Largely Holds on to Last Month’sGain

The Institute for Supply Management's (ISM) non-manufacturing index fell by 0.4 points to 59.5 in February, after rising by an impressive 3.9 points in the month prior. The headline print came in better than expected, with market consensus anticipating a slightly larger decline of 0.9 points.

Movements among the main subcomponents were mixed. Business activity and new orders continued to build on last month's impressive gains, extending the two-month advance by 5.0 and 10.3 points respectively to 62.8 and 64.8. The level of the new orders in fact marked a new cyclical peak, rising to the highest level since-2005.

On the other hand, the employment sub-index fell by 6.6 points and settled around mid-2017 levels – giving back all of the progress made in the prior two months. Meanwhile, the supplier deliveries sub-index held steady for the third consecutive month at 55.5 points.

The performance among the remaining indicators was broadly positive, with the backlog of orders, new export orders and inventories all improving. The prices paid sub-index pulled back slightly but remained elevated at 61 points – suggesting continued price pressures.

Comments from survey contacts maintained a positive tilt with respect to business conditions and the economic outlook. Meanwhile, the vast majority of industries reported growth on the month, with arts, entertainment & recreation and accommodation & food services being the only two exceptions.

Key Implications

Today's report suggests that after a brief lull in at the end of 2017, the U.S. nonmanufacturing sector is resuming a healthier level of activity at the start of 2018, with the index largely holding onto last month's gain. Broad strength among a few of the main sub-indicators, particularly business activity and new orders – with the latter reaching a new cyclical peak – along with a broadly positive outlook among survey contacts, add further credence to this narrative.

The pullback in the employment index is not surprising, given the all-time high reached last month, but is its magnitude is disappointing. The decline suggests that hiring wasn't as strong in February, with this Friday's payrolls likely to be softer than previously expected.

Current levels of the ISM nonmanufacturing index, alongside its manufacturing cousin, suggest that the U.S. economy should be growing near 2% (ann.) during the quarter. However, the hard data has been coming in weaker, with our latest nowcast suggesting the pace of growth is closer to 1.6%. Nonetheless, we believe that residual seasonality may be behind some of the weakness, with the pace of growth likely to accelerate in subsequent quarters.

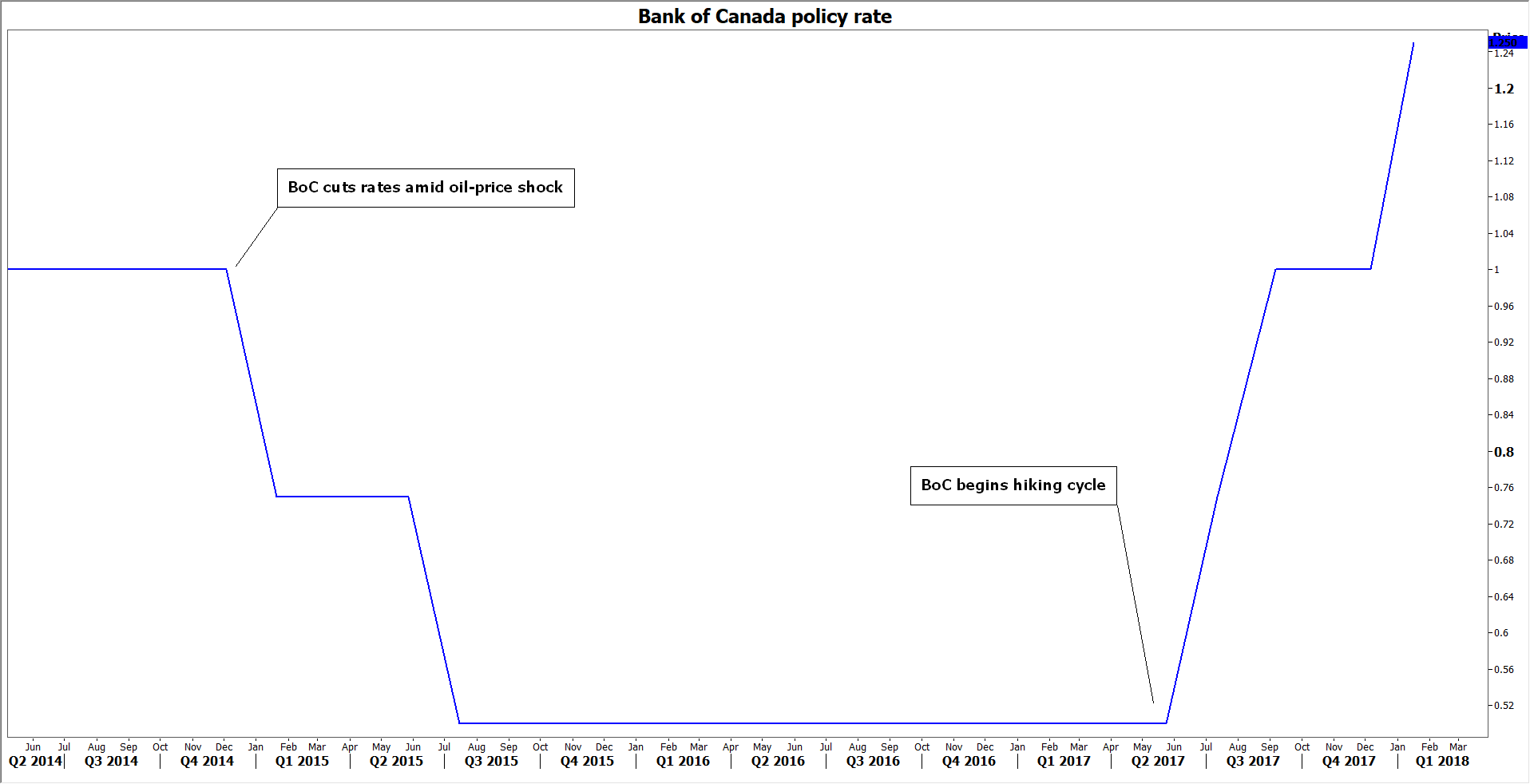

Bank of Canada to Stand Pat, May Appear Cautious Amid Trade Risks

The Bank of Canada (BoC) is due to announce its policy decision on Wednesday at 1500 GMT, and expectations are for the Bank to stand pat having raised interest rates at its previous meeting. While markets continue to expect two more hikes by the BoC this year, it will be interesting to see whether officials adopt a more cautious stance, in an environment where recent economic data have softened and the US has announced tariffs that will adversely impact the Canadian economy.

Even as it raised interest rates in January, the BoC appeared quite concerned with trade developments, ending the first paragraph of the statement accompanying that decision with "uncertainty surrounding the future of NAFTA is clouding the economy's outlook". The outlook for free trade has worsened significantly since then, as the US recently announced it plans to introduce heavy tariffs on steel and aluminum imports. This is a particularly discouraging development for Canada, which exports nearly 90% of its steel to the US, and accounts for 16% of all US steel imports, the highest of any country.

Meanwhile, Canadian economic data have softened ever since the BoC's January meeting. On the inflation front, both the headline and the core CPI rates have declined. In terms of economic growth, the economy grew by less than projected in the final quarter of 2017 as consumer spending waned, while third quarter growth was revised lower. As for employment, the labor market posted a particularly soft month in February, but some moderation in jobs appears only natural following several months of robust gains. As for oil prices – Canada being a major oil exporter – those have eased from January's highs, but not by much.

Where does market pricing stand? At the time of writing, investors have fully priced in one more rate hike by the BoC this year, and also see a 70% probability for a second one after that, according to Canada's overnight index swaps. In case the Bank strikes a cautious tone, and expresses increased concerns on trade risks and the economy's lackluster performance, then the probability for a second hike could decline further. The Canadian dollar may come under renewed selling interest, with dollar/loonie likely to surge and aim for a test of the psychological 1.3130 territory, which is the 61.8% Fibonacci retracement of the May 2017 – September 2017 collapse, with a high at 1.3793 and a low at 1.2057. A decisive break above that hurdle could open the way for the 1.3220 zone, marked by the lows of April 2017.

On the other hand though, there is a possibility that the BoC does not jump to any conclusions about trade risks and thus, does not appear particularly nervous for now. NAFTA negotiations are ongoing, and there is a likelihood (albeit a small one) that Canada manages to secure an exemption from such tariffs. Moreover, considering that the market may already be anticipating a concerned tone by the BoC in light of these events, even a neutral stance by the Bank could prove cause for a rebound in the loonie. In this scenario, dollar/loonie could fall back down for a test of the 1.2925 support area, which is the 50% retracement of the aforementioned Fibonacci at 1.2720. A downside violation of this area could set the stage for declines towards the round figure of 1.2800, which was congested in the recent past.

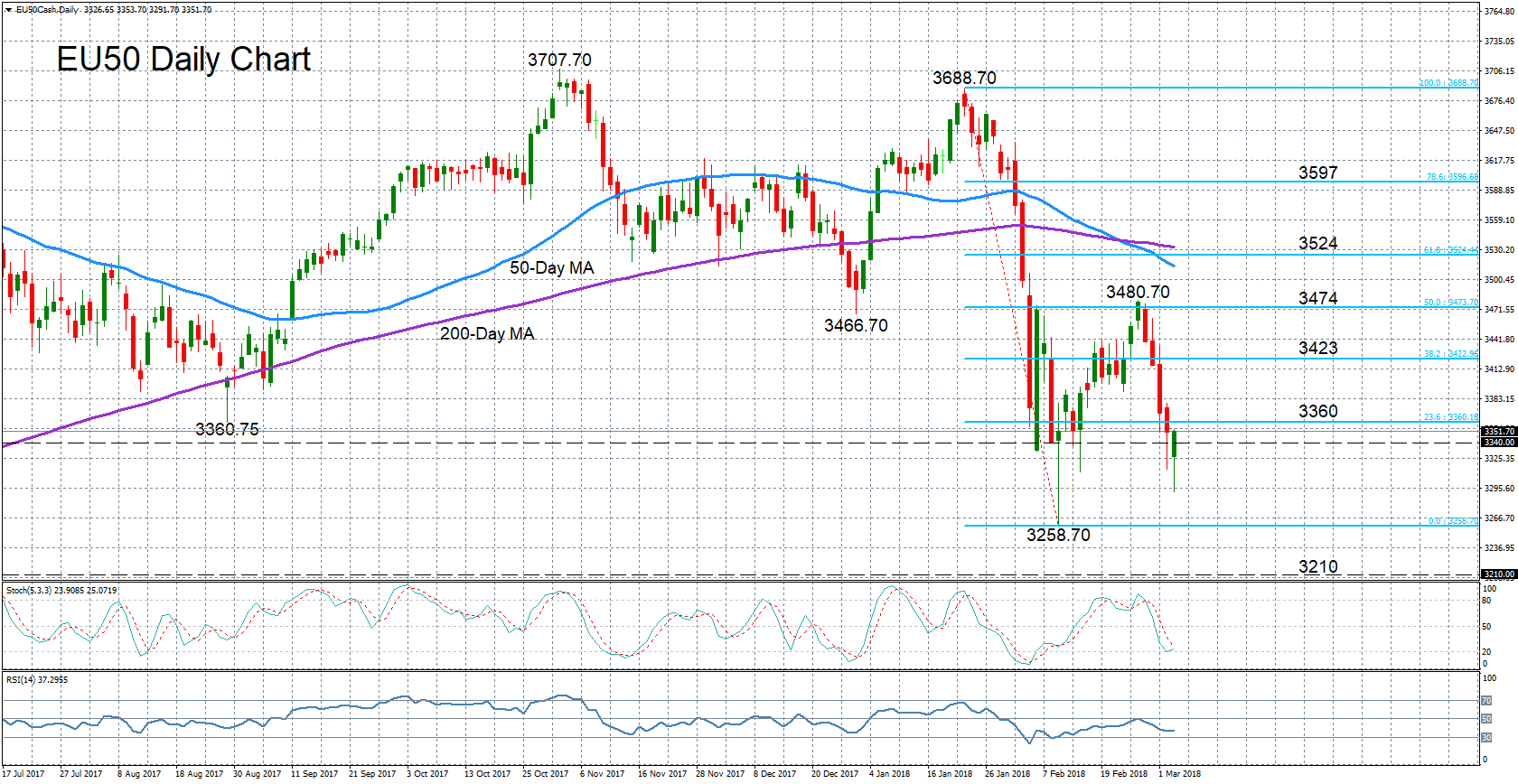

EU 50 Stock Index Looking Increasingly Bearish Below Moving Averages

The EU 50 stock index remains stuck in bearish territory as the recent upswing failed to lift the price above its moving averages. The index has now turned lower again after the rebound was halted at the 50% Fibonacci retracement of the downleg from 3688.70 to 3258.70, and is heading towards February’s one-year lows.

Momentum indicators point to further weakness in the short term, with both the RSI and the stochastics moving closer to oversold territory. However, there are signs that the downside momentum may be easing as the RSI appears to be flatlining and the %K line of the stochastic oscillator is attempting to reverse upwards.

Further losses could see the index revisiting the one-year low of 3258.70. A breach of this level could see the 3210 level (a support barrier from February 2017) coming into focus and would also underscore the increasingly bearish outlook in the medium term.

However, if today’s upside moves pick up further momentum, the index could meet resistance at the 23.6% Fibonacci retracement at 3360. A break above that level could see further resistance at the 38.2% Fibonacci level at 3423 before having another go at the critical 50% Fibonacci level around 3475.

Italian Election Results in Hung Parliament

As widely anticipated, yesterday's general election in Italy resulted in a hung parliament. The incumbent, centre-left government of Paolo Gentiloni lost ground to centre-right populist parties. The populist and eurosceptic Five Star Movement (M5S) earned the greatest share of the popular vote in the lower chamber at 32.5%, but is unlikely to form part of a new coalition government. Instead, a coalition of four centre-right, soft eurosceptic parties that altogether earned about 37% of the popular vote, is favoured to form government after negotiations conclude in the coming weeks or even months.

With 65 governments elected in the last 72 years, political uncertainty is not new to Italy. As such, businesses and the economy more broadly have adapted to operate in an environment of elevated political uncertainty. Overall, the potential for a long process of forming a new coalition government coupled with a likely election within the next year is not expected to have a material negative impact on the Italian or Euro Area economy.

With the election turning out as expected, financial markets largely shrugged off the news, with the only indication of concern registering in a 1.1% decline in Italian equities (FTSE MIB). In the three weeks leading up to Sunday's election, the spread between Italian 10-yr bonds and German bunds rose to about 140 bps from a 16 month low of 126 bps. As of the time of writing, the bond spread is still roughly at 140bps. Moreover, the euro exchange rate with the U.S. dollar has held steady, a sharp contrast to moves preceding and following Dutch and French elections last year when there was fear that anti-EU candidates might form government.

Italian Economy Slowly Improving, Budget Finance a Key Priority for next Government

Italy's economy continues to recover from the 2009 Great Recession and the Euro Crisis that followed. Indeed, 2017 recorded the fourth consecutive year of well-above trend growth. Unemployment rates continue to fall, but at 11% remain about four percentage points above the pre-2009 average. Further structural challenges include the need to better integrate the young, women, and immigrants into the labour force. More progress is also required on the resolution of non-performing loans in the banking sector, which is impairing the flow of credit into the economy.

Chronic general budget deficits have driven Italy's debt-to-GDP ratio to 140%, the second highest in the Euro Area after Greece. General government expenditures have posted strong deficits equivalent to over 4% of GDP on average over the past few years, reflecting legacy debt service payments amongst other factors. In contrast, but similar to its fiscally distressed neighbours, Italy's cyclically adjusted primary budget balance as a percentage of GDP has been strongly positive over the past decade.

Despite positive primary budget surpluses, weak underlying economic growth makes it difficult for governments to raise revenues to pay off legacy debts. Add the challenge posed by tight fiscal rules set by the European Union, and fiscal policy since the 2009 financial crisis has left policymakers with little room to maneuver to aid the Italian economic recovery.

Long-term Challenges Need to be Addressed

As with much of the Euro Area, an aging labour force is putting pressure on government finances through rising old-age dependency ratios. However, with low fertility rates and the election of a centre-right coalition that includes parties that strongly oppose migrant labour, the demographic situation is unlikely to see much improvement in the near-term.

Productivity growth has been notoriously weak in peripheral Europe, and Italy is no exception. With negligible productivity growth since the introduction of the euro in the early 2000s, there is a sense of urgency for Italy to undertake structural labour and product market reforms that should boost trend productivity growth. However, the lack of a strong government mandate will make reforms difficult to achieve in the near-term.

Overall, these headwinds combine to hold the trend pace of growth near zero percent, all but ensuring that Italy will continue to find it a challenge to bring down its debt-to-GDP ratio. And, with planned fiscal spending by a centre-right coalition to the tune of €161 billion, it may not be long before financial markets once again start to panic about peripheral European debt.

Sunset Market Commentary

US and European bonds opened higher this morning. Sentiment in Asia turned risk-off as investors pondered the impact of an indecisive outcome of the Italian election. Investors were also uncertain on potential next protectionist steps after US president Trump declared he will impose import tariffs on steel and aluminum. However, the safe haven bid for core bonds eased soon. The Bund and the US 10-y Note future soon returned most of the earlier gains. The final EMU PMI was revised lower to 57.1 (from 58. 8 in January). There was no noticeable impact on the Bund. Contrary to what was the case last week, European equities hardly suffered from political uncertainty. Most indices (ex Italy) soon returned into positive territory, preventing further bond gains. The US yield curve declines about 2/3 bps with the 5-year outperforming (-3.2 bp). German yields decline between 0.5 bp (2-year) and 3 bp (10-y). 10-year yield spreads versus Germany are mostly little changed. Italy underperforms (+8bp).

Overnight, the euro faced conflicting signals. EUR/USD jumped temporary to the mid 1.23 area as German SPD agreed to join a coalition with Angela Merkel’s CDU/CSU. However, the indecisive outcome of the Italian election caused the euro the reverse its early gains. EUR/USD dropped temporary below the 1.23 handle at the start of the European session, but there were no follow-through losses. A weaker than expected EMU PMI caused no additional losses for the euro. EUR/USD found a new equilibrium near 1.23. The headlines were not supportive for the euro, but the debate on US import tariffs is weighing on the dollar, too. Call it a balance of weaknesses. EUR/USD trades currently around 1.2310. USD/JPY gained a few ticks, trading in the 106.80 area. The US non-manufacturing ISM will be published after the redaction this report. Last week, after the positive eco comments from Fed’s Powell, it looked that eco data could again become more important for markets/the dollar. However, with the focus on import tariffs/protectionism, a big data surprise is probably needed to have a lasting impact on the dollar.

Sterling traded with a slight positive bias today. Brexit moved temporary to the background and the UK services PMI rebounded more than expected from 53.0 to 54.5. The report kept the door open for a next BoE rate hike in May. EUR/GBP declined from the mid 0.89 area to the 0.89 area. This was partly GBP strength. Euro softness in the wake of the Italian election result also played a (minor) role. Last week’s attempt of EUR/GBP to break beyond the 0.8930/50 intermediate resistance is again rejected. Cable returned to the 1.38 area.

News Headlines

Italy faces a period of political instability as Sunday’s election resulted in a hung parliament. None of the three main groups in Parliament will probably secure a majority . Five Star leader Luigi Di Maio claimed the right to form a government as he said: “The consensus we have gathered across the country paves way for us to govern”.

The EMU IHS markit final Composite PMI declined to 57.1 in February from 58.8. (flash estimate 57.5). The data suggest that the European growth momentum might have peaked. However, the IHS markit chief business economist said the level still indicates growth of 0.8% to 0.9% in Q1. The German composite PMI also declined to 57.6 from 59.0, a three-month low. The UK Markit/CIPS services PMI rose to 54.4 from 53.3. The consensus only expected 53.3. The report leaves to door open for the BoE to raise rates again at the May policy meeting.

Ministers from the United States, Canada and Mexico meet on Monday to wrap up the latest round of NAFTA talks as US President Donald Trump prepares to announce tariffs on steel and aluminum. Trump apparently ties possible exemptions for the United States' two neighbors to a "new" NAFTA deal as well as other steps. The trade tensions are putting the Canadian dollar under heavy pressure. USD/CAD is near the 1.30 barrier.

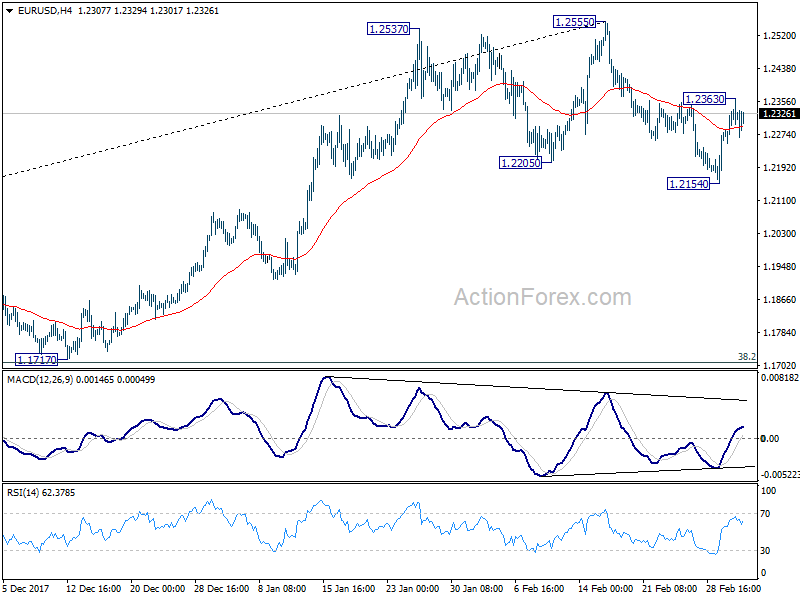

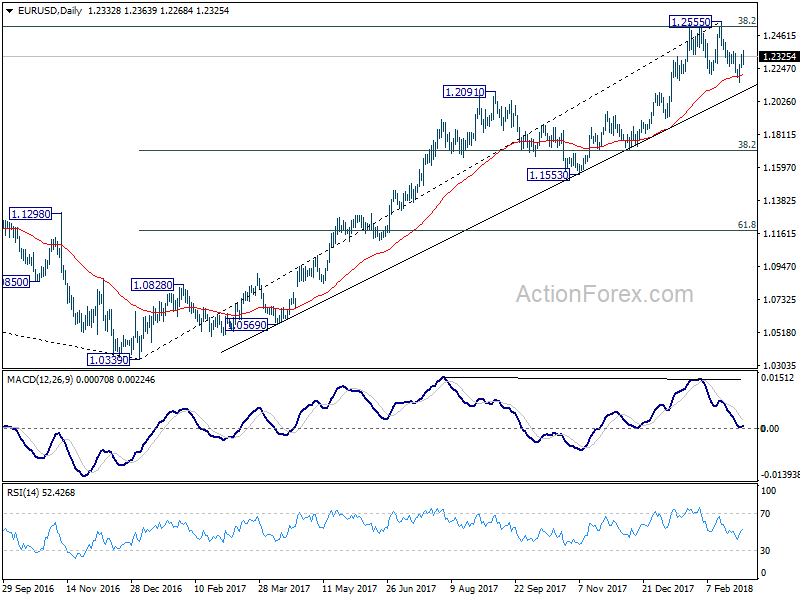

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2267; (P) 1.2301 (R1) 1.2351; More....

Intraday bias in EUR/USD remains neutral at this point. On the upside, above 1.2363 should extend the rebound from 1.2154 to retest 1.2555 high. Firm break there will carry larger bullish implication. On the downside, break of 1.2154 would revive the case of rejection by 1.2516 key fibonacci level and trend reversal. Outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2555 at 1.1708.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

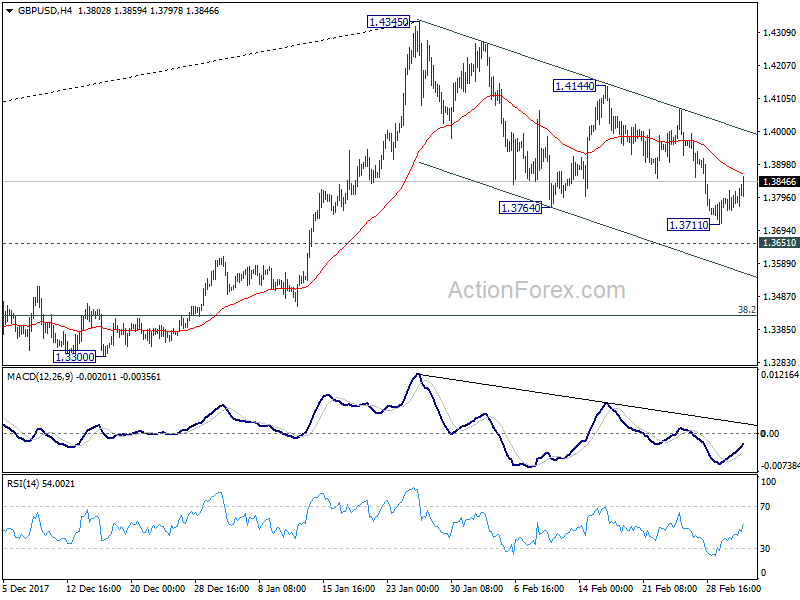

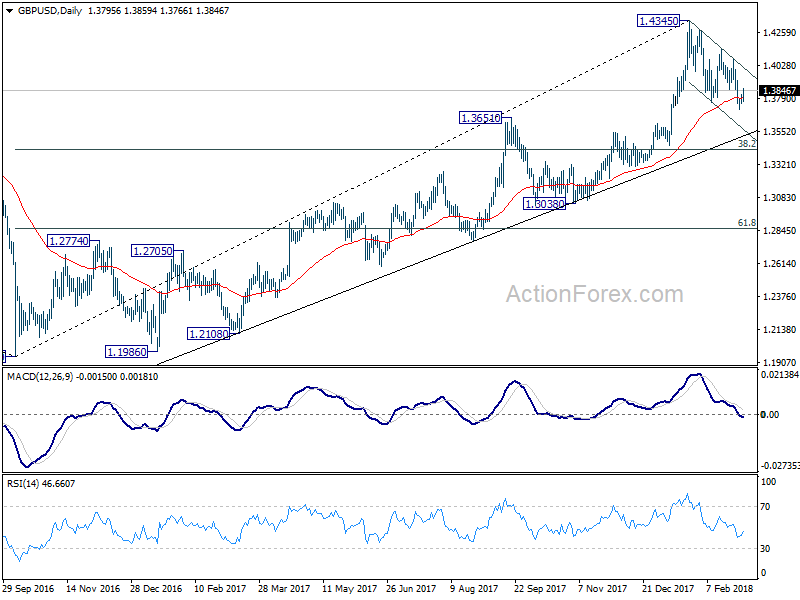

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3763; (P) 1.3789; (R1) 1.3824; More....

GBP/USD recovers mildly today but it's considered staying in consolidation from 1.3711 temporary low. Intraday bias stays neutral at this point. And, near term outlook is still mildly bearish with 1.4144 resistance intact. Correction from 1.4345 would extend to 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.