Sample Category Title

RBA: Wage growth have troughed, AUD ticks mildly higher

Aussie trades mildly higher after RBA kept the cash rate unchanged at 1.50% as widely expected. The statement is almost likely a carbon copy of the prior one. Nonetheless, RBA sounded more optimistic on wage growth as it said that "the rate of wage growth appears to have troughed". Regarding the economy, Australian economy is expected to grow fast in 2018 than in 2018. Regarding inflation RBA maintained that "the central forecast is for CPI inflation to be a bit above 2 per cent in 2018." The statement concluded by maintaining "holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time."

Released earlier in Australia retail sales rose 0.1% mom in January, below expectation of 0.4% mom. Current account deficit widened to AUD -14.0b in Q4.

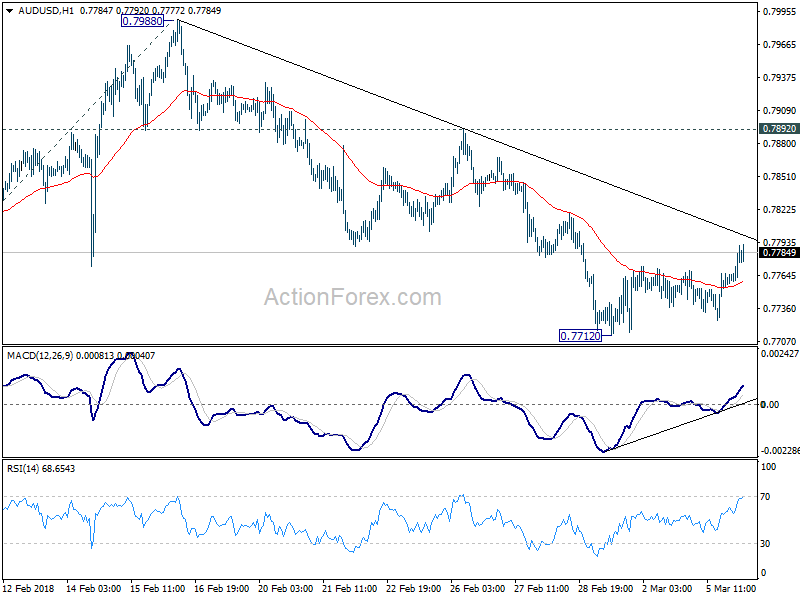

AUD/USD mildly higher but first hurdle of near term reversal is trend line resistance at 0.78.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth picked up in the Asian economies in 2017, partly supported by increased international trade. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth.

The pick-up in the global economy has contributed to a rise in oil and other commodity prices over the past year. Even so, Australia's terms of trade are expected to decline over the next few years, but remain at a relatively high level.

Globally, inflation remains low, although higher commodity prices and tight labour markets are likely to see inflation increase over the next couple of years. Long-term bond yields have risen but are still low. Market volatility has increased from the very low levels of last year. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus. Financial conditions remain expansionary, with credit spreads narrow.

The Bank's central forecast is for the Australian economy to grow faster in 2018 than it did in 2017. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Further growth in exports is expected after temporary weakness at the end of 2017. One continuing source of uncertainty is the outlook for household consumption. Household incomes are growing slowly and debt levels are high.

Employment grew strongly over the past year and the unemployment rate declined. Employment has been rising in all states and has been accompanied by a significant rise in labour force participation. The various forward-looking indicators continue to point to solid growth in employment over the period ahead, with a further gradual reduction in the unemployment rate expected. Notwithstanding the improving labour market, wage growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wage growth over time. Consistent with this, the rate of wage growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation remains low, with both CPI and underlying inflation running a little below 2 per cent. Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

On a trade-weighted basis, the Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. APRA's supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Market Morning Briefing: The Euro Has Broken Above The Immediate Resistance

STOCKS

Dow (24874.76, +1.37%) moved up from the immediate support on the daily candles instead of moving down to test lower supports near 24000-23600. Upside could be limited to 25000-25200 levels in the medium term and an eventual test of 24000 is possible in the longer term. While the support on the daily candles hold, the index may rise towards 25000-25200.

Dax (12090.87, +1.49%) bounced slightly after the recent fall to levels below 12000. Currently trading just above 12000, the index could attempt a test of 12200-12300 on the upside from where another short dip is possible. The horizontal support on the weekly seems to be holding just now as mentioned yesterday but need to see if the current bounce is short lived or moves higher towards 12500 and above.

Nikkei (21487.16, +2.12%) is trading just along the support on the 3-day candle charts and while that holds, a bounce towards 22000-22500 looks possible.

Shanghai (3247.79, +0.28%) has immediate resistance as visible on the daily candle chartand while that holds, there could be a decent fall towards 3230-3200 in the next 1-2 sessions.

Nifty (10358.85, -0.95%) tested a low of 10323 yesterday, breaking our mentioned 10380 support. If the index does not bounce back immediately, it could indicate upcoming bearishness towards 10200-10000 levels in the near term. Else a bounce back from current levels could take it higher towards 10500-10800 levels.

Sensex (33746.78, -0.88%) show a clear break of the immediate support which is yet not visible on the Nifty. This could be indicateive of an upcoming bearishness. Current levels are crucial to keep an eye on.

COMMODITIES

Brent (65.66) and WTI (62.63) have moved up and could target 66.0-66.5 and 63.0-63.4 today. Thereafter a small dip is possible back towards 64.30 and 62-61 respectively.

Gold (1321.91) has paused near current levels and could trade sideways in the 1310-1330 region just now. Slight rejection from 1330 is possible in the next couple of sessions. Near term looks stable.

Copper (3.1315) is also in a pause mode just now and is likely to remain stable for sometime in the 3.15-3.07 region before trying to move towards 3.20 or higher in the longer run.

FOREX

The Dollar Index (89.966), seems to be getting some immediate support near 90 by the 13 days and 21 days moving average lines on daily line chart and also by the 5 weeks moving average line on the weekly line chart. However these supports might not hold for long as the Dollar Index might attempt to move further down towards support near 89.5 on daily candles. 89.0-89.5 is seen as crucial long term support level on the weekly line charts, which if broken, might lead to sustained bearishness for the Dollar.

The Euro (1.2350) has broken above the immediate resistance, which was being provided by the 21 days moving average line on the daily line chart near 1.232-1.233. There might be some resistance provided by earlier support line on 3 day candles near 1.235, but this resistance should be breached soon for an attempt of higher levels near 1.245-1.250 later this week.

Dollar-Yen (106.41) against our expectation has risen from levels near 105.4-105.5 seen yesterday and might now attempt a test of resistance near 106.5-106.75 on the daily candles before dipping again. Medium term looks bearish for Dollar Yen with the next target on the downside being levels close to 104.0-104.5, seen as support on daily and 3 day candles.

The Euro-Yen (131.43) tested support on daily candles near 129.5 (it saw a low of 129.36) earlier than expected and has now bounced. There is resistance near 131.5 on the daily candles and near 132 on the 3 day candles which should keep the Euro Yen’s upmove restricted.

Pound (1.3845) is bouncing from support near 1.3775 on the daily candles and might move back up towards 1.395 over the coming sessions, which is seen as immediate resistance on daily candles.

Dollar-Rupee (65.11): Bit of a two-way market possible today - watch if either Resistance at 65.3075 or Support at 65.00 breaks.

INTEREST RATES

The German 10 Yr – US 10 Yr yield differential (-2.24%) is hovering near crucial long term support level of -2.25%, which might hold. A hold of the support would imply either a drop in US 10 yr yield or a rise in the German 10 yr yield. The German 10 Yr yield (0.64%) recently dropped below support near 0.7 on the medium term chart and dipped from resistance near 0.75 on the long term chart. Moreover, the ECB is expected to not indicate much tightening in their next meeting on 8th March, which might thereby imply that a rise in German 10 Yr yield might be difficult. Hence, for support on the German-US spread to hold, US yields might need to drop, which also look unlikely immediately. For now, the 8th march ECB meeting and 21st March US Fed meeting become extremely vital to the course of yields and forex rates.

US 10 Year Yield (2.88), US 30 year Yield (3.1547), US 5 year yield (2.65), US 2 year yield (2.237) : US Yields continue their oscillation near respective long term resistances

The first half of March might just see muted movement in US yields. As the 21st March Fed meeting comes closer, there could be a rise in yields in anticipation of a rate hike.

(Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen in March 2nd half.)

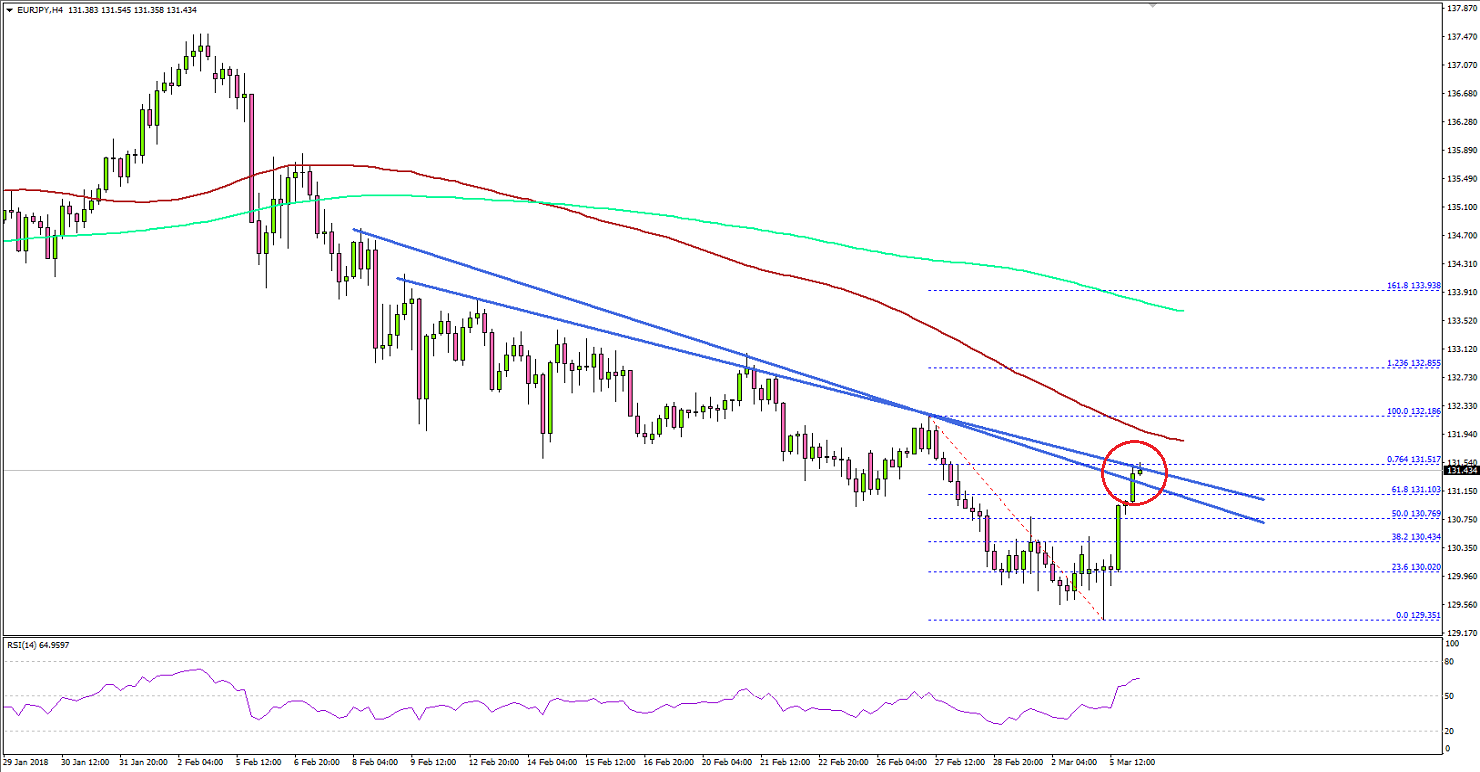

EUR/JPY About To Break Downtrend At 131.50

Key Highlights

- The Euro is in a major downtrend with a key resistance at 131.50 against the Japanese Yen.

- There are two important bearish trend lines forming with resistance near 131.30-50 on the 4-hours chart of EUR/JPY.

- The Euro Zone Services PMI for Feb 2018 posted a decline from the last reading of 56.7 to 56.2.

- The US Factory orders figure for Jan 2018 will be released today, which is forecasted to decline by 1.3% (MoM).

EURJPY Technical Analysis

The Euro declined heavily during the past few days and moved below the 132.00 support against the Japanese Yen. The EUR/JPY pair is currently attempting a recovery, and it must break 131.50 to move into a positive zone.

The pair recently traded as low as 129.35 and is currently correcting higher. It already corrected higher substantially, but it is facing sellers on the upside near the 131.40 and 131.50 levels.

Looking at the 4-hours chart, there is a clear downtrend in place from the 137.00 swing high. The pair broke a couple of important support levels such as 135.00 and 132.00.

On the upside, there are two important bearish trend lines forming with resistance near 131.30-50 on the 4-hours chart. Moreover, the pair is well below the 100 simple moving average (red, 4-hour) and 132.00.

There can be an upside correction, but the pair may face resistance near the trend lines and the 76.4% Fib retracement level of the last decline from the 132.18 high to 129.35 low. Once there is a close above 131.50, the pair may move into a bullish zone.

On the downside, a break below the recent low of 129.35 could ignite further declines toward the 128.50 level.

Recently, the Euro Zone saw the release of the Services PMI for Feb 2018. The market was looking for no change in the PMI from 56.7. However, there was a minor decline from the last reading of 56.7 to 56.2.

Commenting on the report, the Chief Business Economist at IHS Markit, Chris Williamson, stated:

The eurozone economy looks to have hit a speed bump in February after a stellar start to the year. It’s too early to read too much into the February fall in the PMI, and some pull-back from January’s high was always on the cards.

It seems like the recent gains in the Japanese Yen may continue to weigh on EUR/JPY. Only a close above the 131.50 resistance could clear the path for a recovery.

I Won’t Back Down

While the markets get distracted by Central Bank discourse and Friday’s crucial NFP report, the tariff story continues to linger over the market like the foul smell of rotten eggs as the day of reckoning nears for the release of the official tariff details. Given the overwhelmingly negative response from industry leaders, international financial markets and even the furious backlash from loyal members of Trumps administration, there is growing optimism that perhaps significant exemptions will be forthcoming. The ink has not dried on the tariff bill, so investors remain guardedly optimistic.

US equity market rose Monday as investors apprehension about the impending global trade war has tempered hoping for a diplomatic solution, and at the minimum, a process would be in place for businesses to get exemptions from the White House. However, expecting for cooler heads to prevail, might be far too optimistic given that President Trump promoted reforms of U.S. trade policies as a cornerstone of his election campaign, and it’s challenging to envision him back down.

With traders eyeing NAFTA headlines and extrapolating possibility of steel tariff, the latest round of talks made little progress and negotiations remain fractured as political headwinds build.

Oil Markets

Oil prices moved the significantly higher overnight following reports of a drop in crude inventories at the prominent US Cushing Oklahoma storage facility with WTI chalking up its most significant days since Feb 14.

Also, lingering optimism that the CERAWeek by IHS Market conference could generate some production consensus, but with the trade war rhetoric filling the air suggesting little compliance from the Shale elements, the risk will be a two-way street subject to the outcome of the meeting.

Still, the upswing in US Shale production estimates continues to soar as the International Energy Agency suggested that the U.S. would become the world’s top crude producer by 2023 with production hitting a record of 12.1 million barrels a day.

Gold Market

Gold market continues to run hot and cold on the back of fast money.

With higher headline risk comes waves of fast short-term money plays that can leave a sizable imprint on the daily charts. Again, price momentum becomes headline challenged at the principal $ 1330 level as investors reduce risk hedges as global trade ware rhetoric tempers. Price action will remain choppy within near-term ranges until the prospect of higher US inflation receives increased attention. But even in the near term, given the unpredictable nature of current market sentiment, investors will continue to buy gold on dips to hedge the growing tail risk from Trump’s controversial policies.

Currency Markets

The Euro

The Euro has traded positively in the wake of the Italian election aftermath despite the growing wave of anti-establishment populism.

But the Euro has a convincing history story of reversing EU political negatives. And with the main political risk for Germany behind us, with compelling headlines, the Euro could punch higher. But the sentiment is predictably muted ahead of the ECB given the recent soft run of data as traders are erring on the side of caution. But even if the ECB play their cards close to their chest, it’s as sure of a bet as one can get in FX markets that the ECB will continue to march towards policy normalisation and the EUR will move higher in this weak US dollar environment.

The Japanese Yen

The risk was a bit overextend, and traders found themselves far to stretched heading into the Tariff announcement while simultaneously positioning for a possible upgraded inflation expectation ahead of this week’s NFP’s wage data.

US yields moved higher overnight, and USDJPY caught a bit of a tailwind, helping USDJPY move towards crucial resistance levels ( 106.35-50 )

But looking at a broader class of riks assets they too are trading more favourably this morning assisting USDJPY sentiment. But given this could be little more than a short-term reprieve , the market will continue to look lower for USDJPY from both a short-term risk perspective and longer-term BoJ policy implications.

The Malaysian Ringgit

For now, the downside surprise in Jan’s headline inflation and tepid core give MPC ample room to hold policy steady on Wednesday, with the BNM preference for a stronger MYR to act as the cantilever for tightening monetary conditions as the Malaysian economy will continue to overperform through 2018

The BNM well telegraphed January’s rate hike intention so traders will be looking for forwarding guidance, mainly the BNM’s in inflation outlook, to gauge if they could move the dial one more time in 2018. AS such traders will keep a close watch for any hawkish nuances. Overall the statement should be very favourable for the local economy and will be supportive of the local bond markets. However, given the current currency malaise in the regional market, it could be less favourable in that regards.

In the meantime, OPEC compliance continues to support oil prices which play favourably for the Ringgit fortunes. And as far as the regional basket is concerned the MYR should remain in favour given is a strong external position, the lack of dependency on US trade and improving current account balance.

Pound Continues To Gains Ground

The British pound has posted gains to start off the week. In Monday’s North American trade, GBP/USD is trading at 1.3852, up 0.37% on the day. In economic news, British Services PMI improved to 54.5, above the estimate of 53.3 points. In the US, the ISM Non-Manufacturing PMI slowed to 59.5, but managed to beat the estimate of 58.9 points.

The pound has started the week with gains, despite growing concerns over tensions between London and Brussels over Brexit. On Friday, Prime Minister May outlined her vision of relations between the EU and Britain after Brexit. May sought to lower the recent sharp rhetoric surrounding Brexit, saying that both sides needed to show flexibility in order to reach an agreement. May said that she was seeking a free trade agreement with the EU that included financial services. The response from Brussels has been lukewarm, with some policymakers saying that Britain continues to operate under the illusion that it can leave the club but still enjoy the benefits. Last week, there were sharp exchanges between the two sides after the EU releases a draft of the legal framework of the Brexit agreement.

The US dollar was broadly lower last week, after President Trump sent shock waves through the markets when he announced stiff tariffs on steel and aluminum, in order to protect domestic producers. Under the new scheme, foreign steel will be taxed at 25% and aluminum at 10%. The response to the move was overwhelmingly negative, both abroad and in the US. China and the EU immediately denounced the move. US auto makers and oil and gas producers also condemned the tariffs, saying they could get caught in the middle of a nasty trade war if other countries retaliate. In imposing the tariffs, Trump relied on a provision which allows such measures for national security, but clearly, US trading partners will not quietly accept these protectionist measures.

Trade Risks Crystalize

White House comments to start the week tied tariffs to NAFTA and were seen as a sign that the President has a strategy. The pound was the top performer while the Canadian dollar lagged. The RBA decision is up next.

Global stock markets bounced and the yen slipped on Monday as rhetoric shifted on steel tariffs. What looked like a hasty decision to put on global tariffs may have been part of a strategy to leverage a better NAFTA deal. Trump and US NAFTA negotiator Lighthizer both said Canada and Mexico would win exemptions from the tariffs if they made a NAFTA agreement.

It's entirely unclear what kind of agreement Trump wants or if US NAFTA partners can accept it but for now, markets were comforted by signs of a plan.

One pocket of weakness was the Canadian dollar as mounting risks pushed USD/CAD above the technically-critical 1.2920 level to the highest since June. That fear ties into Wednesday's BOC decision and a growing likelihood of a more-neutral stance because of greater trade and economic risks.

Yet, it remains unclear if Trump has a bigger plan for tariffs outside of NAFTA. Many leaders want to see the text of what Trump is proposing before taking a step towards retaliation.

Looking ahead, it's a big day for AUD traders with current account and retail sales at 0030 GMT followed by the RBA decision three hours later. Retail sales are forecast to rise 0.4% after a 0.5% decline in December. It's been volatile time for the numbers but consumer confidence has been rising.Trade, meanwhile is expected to show next exports pulling GDP 0.6 pp lower and the current accounts in a deficit of A$12.2B.

Whatever the numbers, the market will be reluctant to make a move before the RBA weighs in. Lowe has been more optimistic lately and expects GDP to accelerate to 3.25% y/y by the end of 2018 but recent wage numbers have been soft.

Elliott wave Analysis: USD Index Update

USD Index is trading impulsively lower from the high, suggesting that a bigger corrective wave 4 had ended. If so, then we now expect price to unfold a five-wave drop, with red wave i) being already completed. Current minor rally can be wave ii), which can see limited upside near the 90.45/90.50 area.

USD Index, 1H

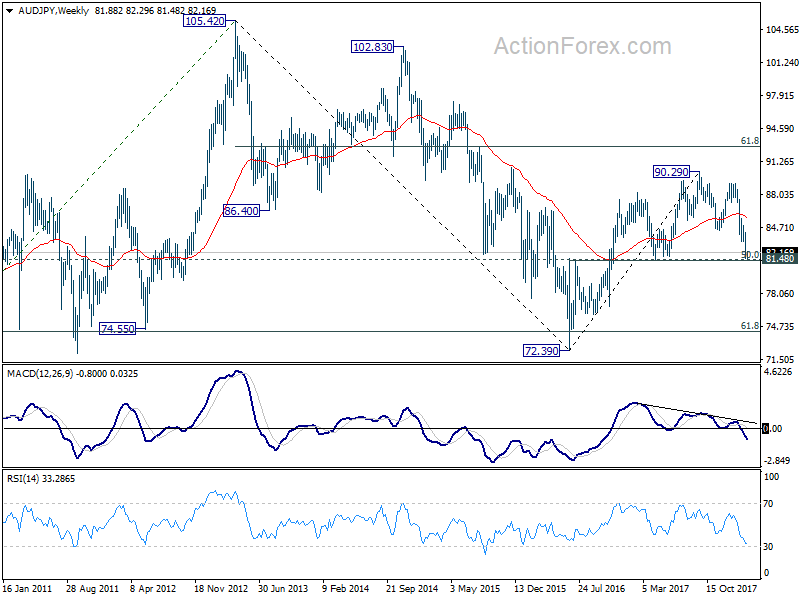

RBA to hold. AUD/JPY drawing support from 81.48.

RBA up next in Asian session. OCR is widely expected to be kept unchanged at 1.50%. RBA will also maintain a neutral stance. Movements in Aussie is more likely tied to risk appetite/aversion than RBA. Australia will also release current account and retail sales.

More on RBA

- RBA Expected to Stand Pat; Other Key Data Out of Australia on the Agenda

- Australia & New Zealand Weekly: RBA on Hold, AUD to Weaken through 2018 and 2019

AUD/JPY is a pair that's worth watching. It's pressing key long term cluster level at 81.48, close to 50% retracement of 72.39 to 90.29. Return of risk appetite could trigger a rebound through 83.17 resistance. And that would in turn trigger a near term reversal.