Sample Category Title

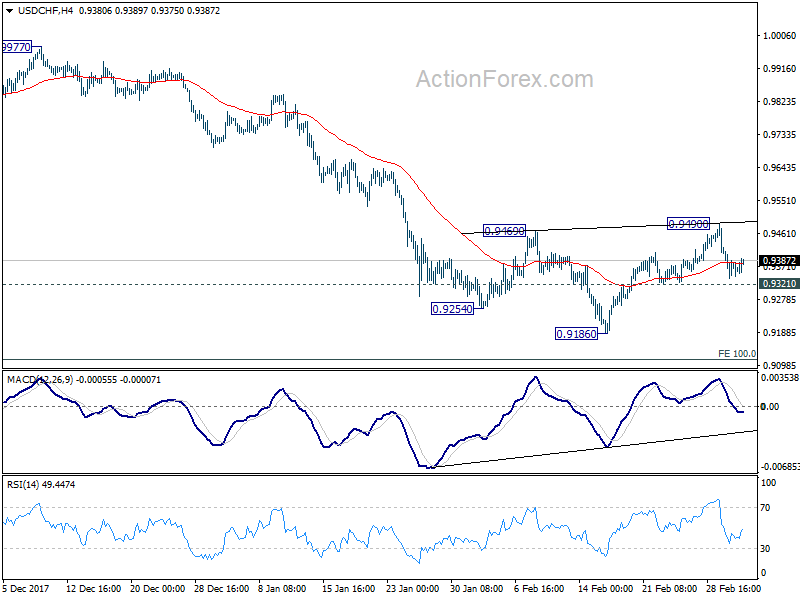

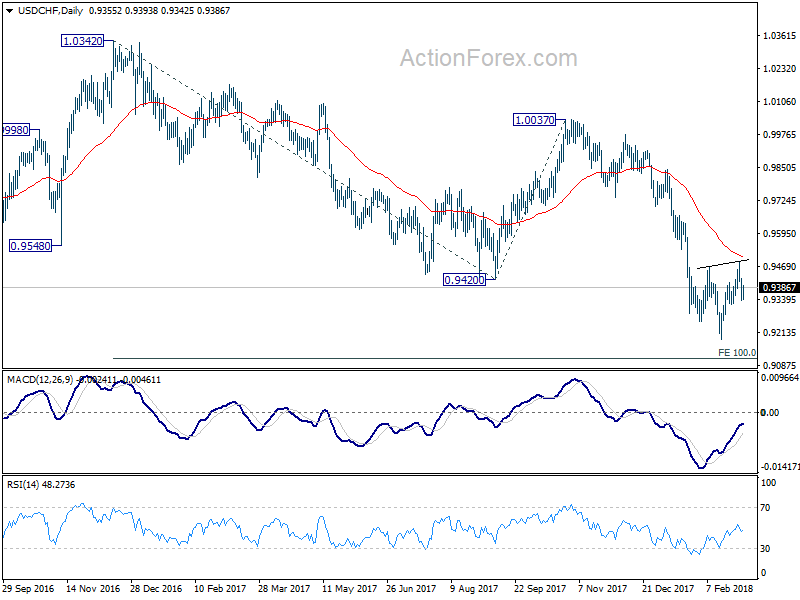

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9333; (P) 0.9378; (R1) 0.9419; More...

Intraday bias in USD/CHF remains neutral with focus on 0.9321 minor support. On the downside, break of 0.9321 will indicate completion of the rebound from 0.9186. Intraday bias will be turned back to the downside for 0.9186 first. Break will resume larger down trend to 0.9115 projection level. On the upside, break of 0.9490 will revive the case of near term reversal, on bullish convergence condition in 4 hour MACD. In that case, outlook will be turned bullish.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

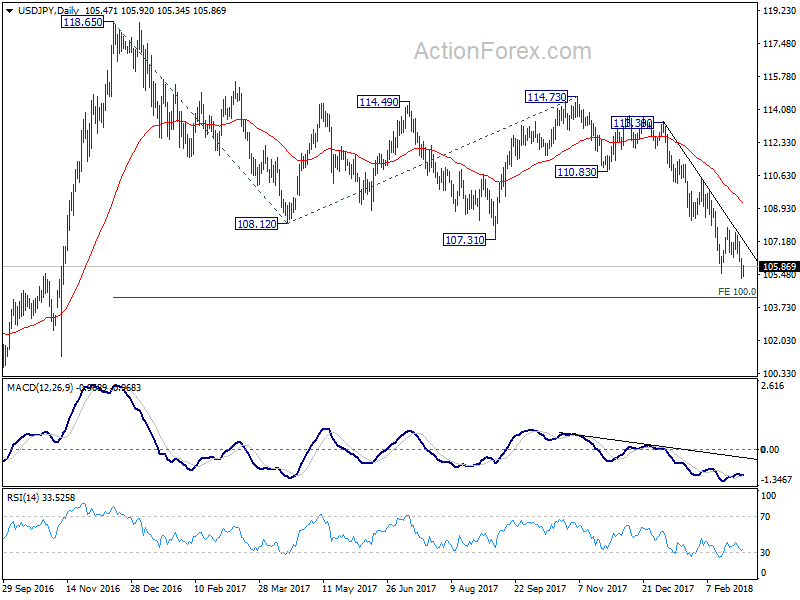

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.20; (P) 105.75; (R1) 106.25; More...

USD/JPY recovers today but stays well below 106.37 minor resistance. Intraday bias remains on the downside for the moment. As noted before, down trend from 118.65 has just resumed and should target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

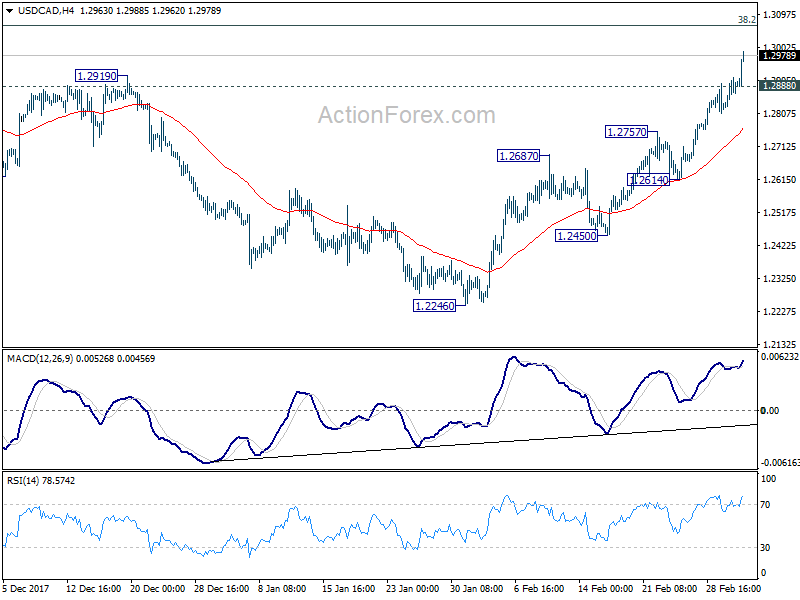

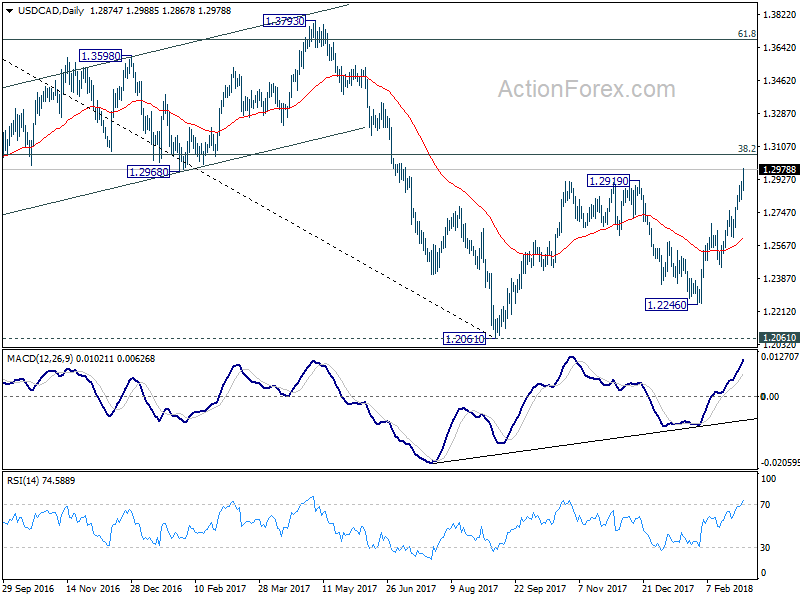

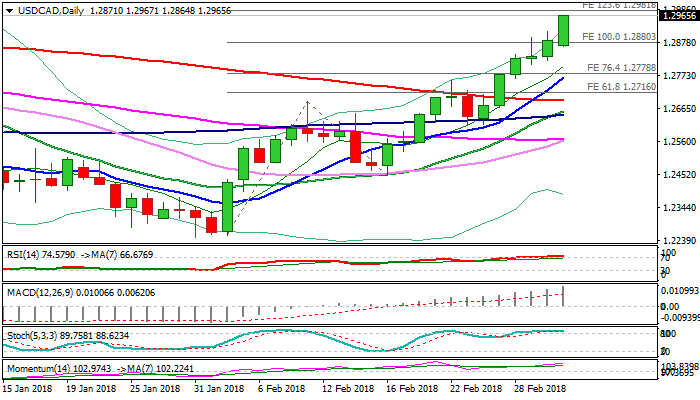

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2828; (P) 1.2871; (R1) 1.2924; More....

USD/CAD surges to as high as 1.2988 today and the firm break of 1.2919 resistance confirms resumption of whole medium term rise from 1.2061. Intraday bias is back on the upside for 1.3065 fibonacci level next. On the downside, below 1.2888 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 1.2757 resistance turned support holds.

In the bigger picture, strong break of 1.2919 resistance adds much credence to the bullish case. That is larger down trend from 1.4589 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

Canadian Dollar Dives as Trump Plays Tariff Card in NAFTA Negotiations

Canadian Dollar suffers steep selling today as US President Donald Trump singles out Canada and Mexico in his trade war rhetorics. He said in a tweet that "NAFTA, which is under renegotiation right now, has been a bad deal for U.S.A. Massive relocation of companies & jobs." And, "tariffs on Steel and Aluminum will only come off if new & fair NAFTA agreement is signed." It should be noted that again that Canada (16%) and Mexico (9%) were the first and fourth steel importers to US in 2017. Technically, USD/CAD took out a key resistance level at 1.2919 and which confirmed resumption of medium term rise from 1.2061.

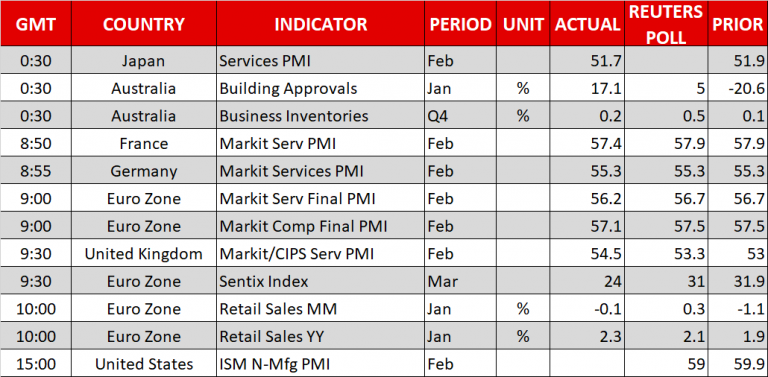

Released from US, ISM non-manufacturing composite dropped to 59.9, down from 59.9 but beat expectation of 59.0.

UK PMI services: May BoE hike very much in place

Pound regains some footing today as supported by services data. UK PMI services rose to 54.5 in February, up from 53.0 and beat expectation of 53.3. Markit noted in the release that "business activity rises at fastest pace for four months" with "strongest upturn in new work since May 2017". Chief Business Economist Chris Williamson said that "the service sector overtook manufacturing as the fastest growing part of the economy for only the second time since the referendum in February, thanks to the combination of the largest rise in services activity for four months and waning growth of factory output."

Regarding interest rate outlook, Williamson noted that "with Bank of England policymakers sounding hawkish even following the January fall in the PMI to a one-and-a-half year low, the February upturn in the surveys surely leaves a May rate hike very much in play. The Bank seems keen to normalize interest rates even if output growth is below levels it would usually like to see when tightening policy."

Eurozone Sentix: Economic turnaround is in the air

Euro is also firm, after initial selling. Eurozone Sentix investor confidence dropped to 24.0 in March, down from 31.9, much worse than expectation of 30.9. Sentix noted the index "fell significantly" and "expectations are clearly losing ground. "Deterioration in Germany" is one of the main reasons. And, "international environment is also deteriorating." In particular, "the US expectations are close to zero. Trump's comments on punitive tariffs give investors a great deal of thought." Sentix warned that "an economic turnaround is in the air!"

Also from Eurozone, retail sales dropped -0.1% mom in January. PMI services was revised down to 56.2 in February, from initial reading of 56.7.

Elsewhere

China Caixin PMI services dropped 0.5 to 54.2 in February. Australia TD securities inflation dropped -0.1% mom in February. Australia building approvals rose 17.1% mom in January.

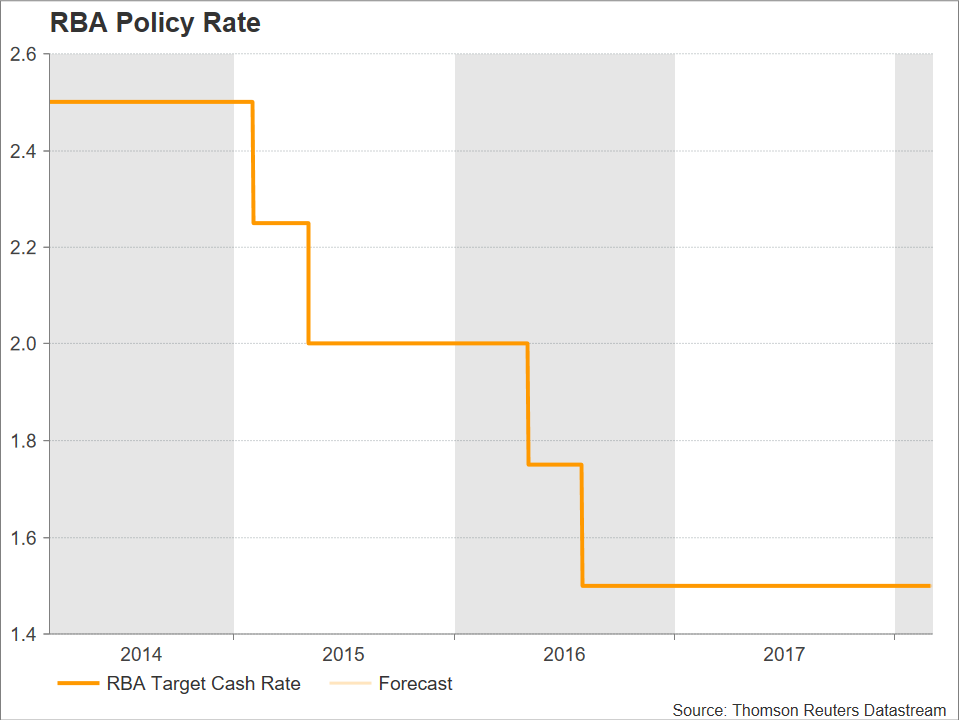

RBA to stand pat

RBA rate decision is the main focus in the upcoming Asian session. RBA is widely expected to keep interest rate unchanged at 0.50%. Governor Philip Lowe and other policymakers have been clear in their neutral stance. RBA is not going to follow other global central banks for tightening. NAB recently adjusted their expectation to just one RBA hike this year, not two. Westpac maintained their forecast that RBA will be on hold throughout this year.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2828; (P) 1.2871; (R1) 1.2924; More....

USD/CAD surges to as high as 1.2988 today and the firm break of 1.2919 resistance confirms resumption of whole medium term rise from 1.2061. Intraday bias is back on the upside for 1.3065 fibonacci level next. On the downside, below 1.2888 minor support will turn intraday bias neutral first. But outlook will now stay bullish as long as 1.2757 resistance turned support holds.

In the bigger picture, strong break of 1.2919 resistance adds much credence to the bullish case. That is larger down trend from 1.4589 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Feb | -0.10% | 0.30% | ||

| 00:30 | AUD | Building Approvals M/M Jan | 17.10% | 5.00% | -20.00% | |

| 01:45 | CNY | Caixin PMI Services Feb | 54.2 | 54.3 | 54.7 | |

| 08:45 | EUR | Italy Services PMI Feb | 55 | 57 | 57.7 | |

| 08:50 | EUR | France Services PMI Feb F | 57.4 | 57.9 | 57.9 | |

| 08:55 | EUR | Germany Services PMI Feb F | 55.3 | 55.3 | 55.3 | |

| 09:00 | EUR | Eurozone Services PMI Feb F | 56.2 | 56.7 | 56.7 | |

| 09:30 | GBP | Services PMI Feb | 54.5 | 53.3 | 53 | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Mar | 24 | 30.9 | 31.9 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -0.10% | -0.10% | -1.10% | -1.00% |

| 14:45 | USD | US Services PMI Feb F | 55.9 | 55.9 | 55.9 | |

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Feb | 59.5 | 59 | 59.9 |

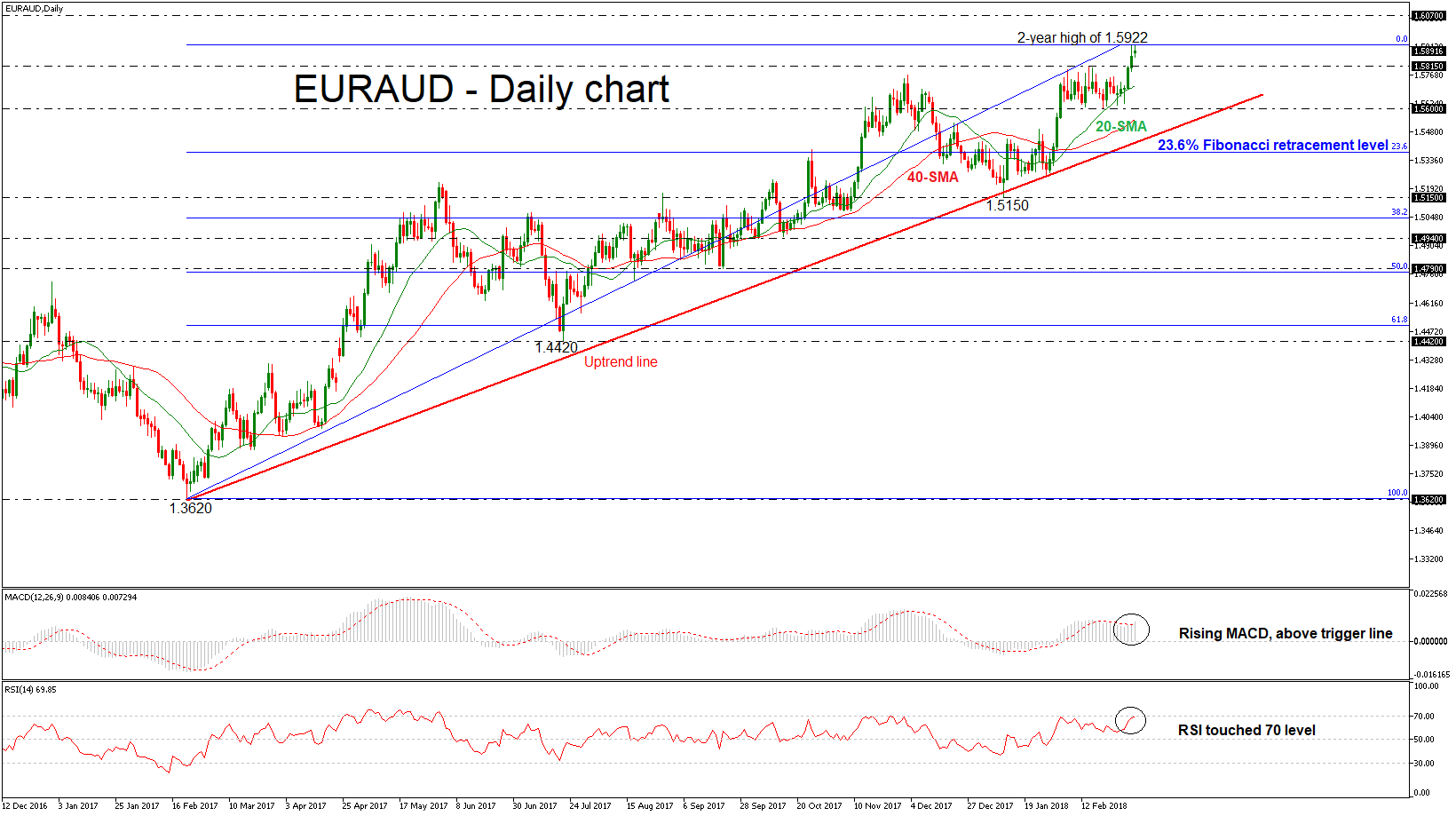

EURAUD Extends its Gains; Reaches a New 2-Year High

EURAUD surged to a fresh 2-year high of 1.5922 during today’s European session after it successfully surpassed the 1.5815 key level. The pair recorded the fifth straight green day and the bullish picture in the short-term is further supported by the technical indicators. It is worth to mention that the price has been developing in an uptrend since February 2017.

From the technical point of view, in the daily chart, the MACD oscillator jumped above its trigger line in the bullish territory, indicating further gains. Also, the RSI indicator touched the 70 level and is ready to enter the overbought area.

If price action remains above 1.5922, it could push the price higher towards the 1.6070 resistance level, taken from the peak in January 2016.

An alternative scenario is a downside tendency below the 1.5815 barrier. Then the focus could shift to the 1.5600 psychological level, painting a bearish picture. If the aforementioned level breached, it could increase the decline and bring about a reversal of the trend towards the 23.6% Fibonacci retracement level of 1.5380 of the upleg from 1.3620 to 1.5922.

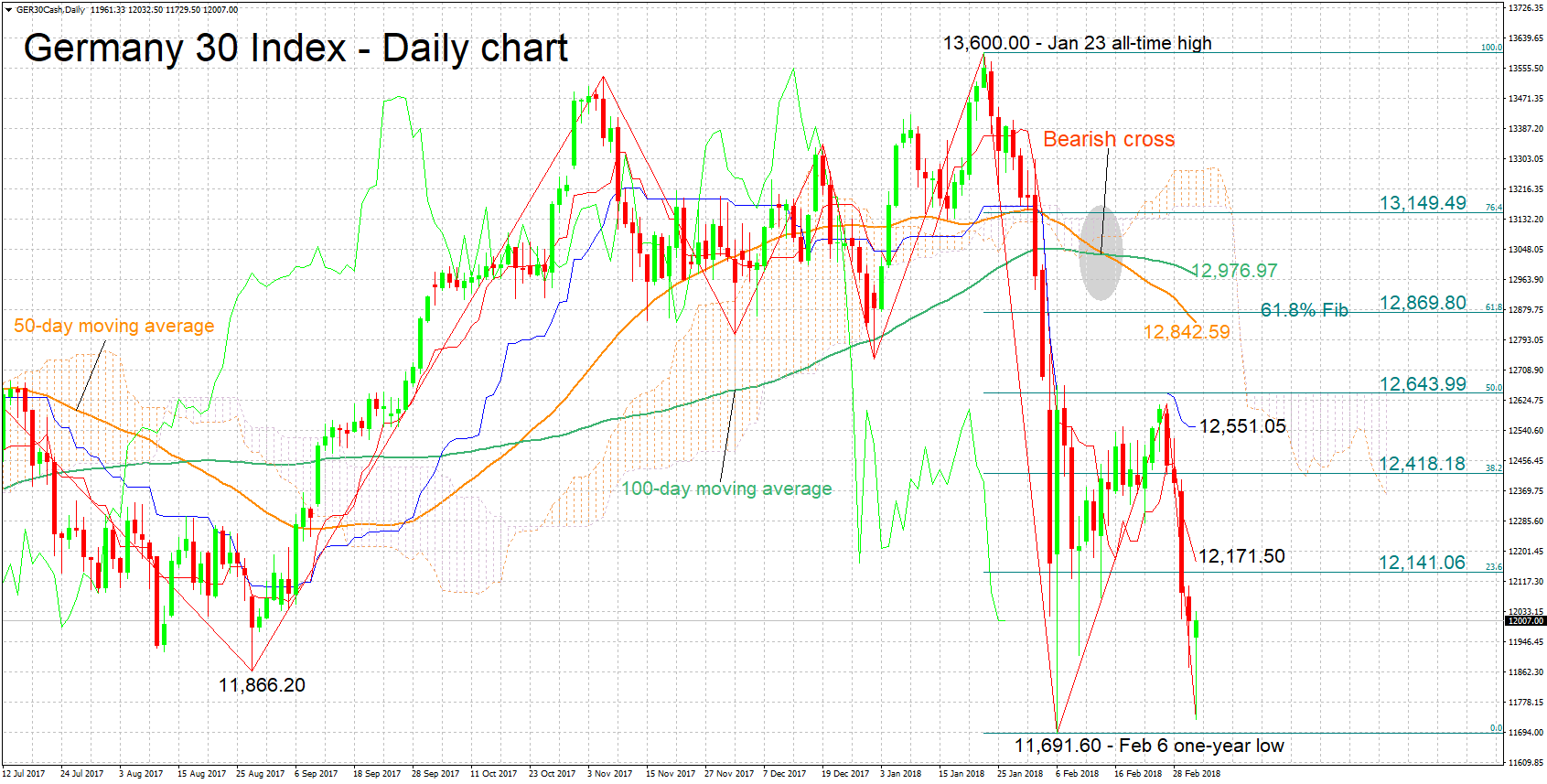

GER 30 Index Possibly Oversold in Near-Term; Looking Bearish in Medium-Term

The Germany 30 index has managed to cross above the 12,000 handle – a level that may be of psychological importance – after previously falling as low as 11,729.50 during Monday’s trading and coming close to the one-year low of 11,691.60 that was recorded in early February.

The bias in the short-term is looking bearish as indicated by the negatively aligned Tenkan- and Kijun-sen lines. The Chikou Span however might be pointing to an oversold market, rendering a rebound in the near-term a possibility.

Index advancing could meet resistance around the 23.6% Fibonacci mark of the January 23 to February 6 downleg at 12,141.06. The area around this barrier also includes the current level of the Tenkan-sen at 12,171.50, with an upside break bringing into view the 38.2% Fibonacci level at 12,418.18.

On the downside, support might come around 11,866.20, this being a previous low with the range around it encapsulating a few bottoms from further back in time as well. Steeper declines would shift the focus to the one-year low of 11,691.60 for additional support.

In terms of the medium-term picture, it is looking bearish at the moment: Price action is taking place below the 50- and 100-day moving average lines, as well as below the Ichimokou cloud. In addition, a bearish cross was recorded in mid-February when the 50-day MA moved below the 100-day one.

Overall, both the short- and medium-term outlooks are looking bearish, with the caveat that an overextended selloff might have taken place in the short-term, something which keeps the possibility for a near-term price recovery open.

RBA Expected to Stand Pat; Other Key Data Out of Australia on the Agenda

The Reserve Bank of Australia will be completing its meeting on monetary policy on Tuesday, with a decision on the Bank's policy rate being made public at 0330 GMT. Markets widely expect the central bank to keep rates unchanged, with the market's focus falling on the RBA's remarks on the outlook for the economy and inflation which could offer hints as regards its monetary policy plans moving forward.

RBA policymakers are expected to support maintaining the cash rate, the central bank's policy rate, at the record low of 1.5% upon completion of the Bank's monthly policy meeting next week.

Given that no change in rates is expected, attention would fall on the Bank's optimism – or lack thereof – on the Australian economy moving forward. The RBA has in the past expressed concern on wage growth – that has the capacity to spur inflationary pressures, pushing annual inflation within the Bank's target of 2-3% – which has been dismal despite an overall improving business investment and labor market. Comments on this front will be eagerly anticipated by market participants. It is noteworthy as well though that in its previous assessment, despite the not so upbeat views on workers pay, the Bank said it expects economic growth to accelerate, exceeding 3% over the next couple of years.

Any remarks on the threats posed by household debt, which has been hovering around record-high levels and constituting yet another reason for the RBA's reluctance to deliver a rate increase in the past, will also be attracting attention; the household debt issue is also linked to real estate prices reaching "bubbly" levels, at least according to analysts, in certain cities.

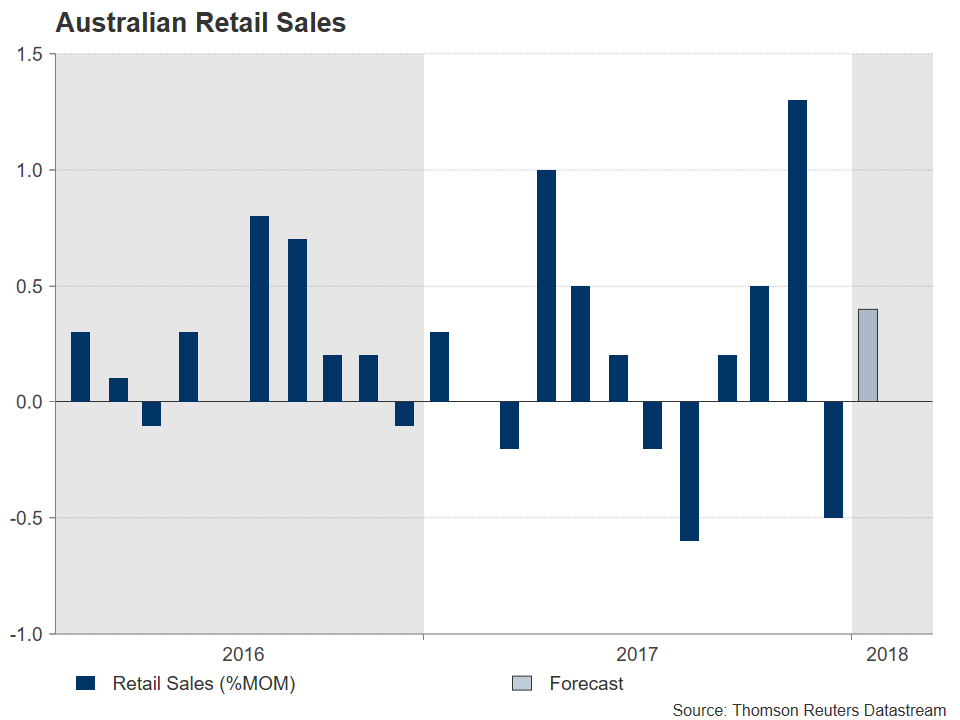

Earlier in the day (at 0030 GMT), retail sales for the month of January, as well as Q4 2017 current account and net exports contribution to growth data will also be attracting interest out of Australia. Retail sales, which can be used as a gauge for household spending that makes up more than 50% of the Australian economy's annual GDP, are expected to rise by 0.4% after contracting by 0.5% in December. It should be mentioned though that overall Q4 2017 retail sales numbers were upbeat despite the fall during the last month of 2017, pointing to an improving outlook for economic activity.

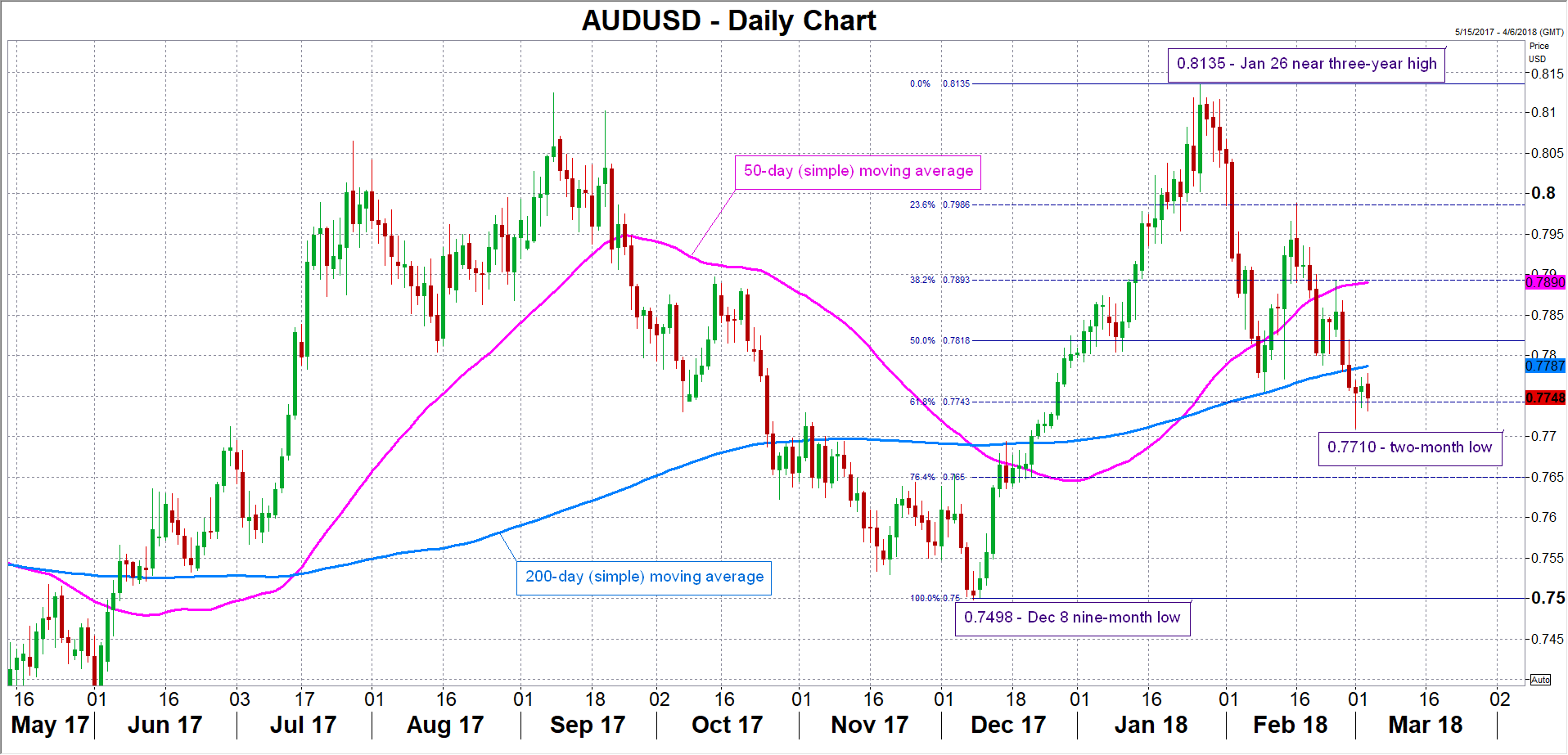

An optimistic tune by the RBA, one that kindles expectations for tightening sooner than previously anticipated, and stronger-than-anticipated data out of Australia are likely to push aussie/dollar higher. The current level of the 200-day moving average at 0.7787, in combination with the 50% Fibonacci mark of the December 8 to January 26 upleg at 0.7818, could act as a resistance zone to price advancing. Further above, the focus would shift to the range around the 38.2% Fibonacci level at 0.7893, with the area around it also encapsulating the 50-day MA at 0.7890 and the 0.79 handle that may hold psychological significance.

On the other hand, should the RBA sound concerned on the economy's outlook, or the data out of the country disappoint, then aussie/dollar is expected to decline. The pair is under pressure, falling considerably after reaching a near three-year high of 0.8135 in late January. A continuation of the declines might meet support around the 61.8% Fibonacci level at 0.7743. Price action is taking place close to this level, with a downside violation bringing into view the 76.4% Fibonacci mark at 0.7650, while the area around last Thursday's two-month low of 0.7710 could also provide support.

Year-to-date, the Australian currency is down by around 0.7% versus its US counterpart. In 2017, it advanced by 8.1%, spurring policymakers' unease as an appreciating currency is seen a weighing on the country's exports – and thus the growth outlook – as well as on inflationary pressures. This year's underperformance might translate into the absence of a currency talk-down by RBA policymakers.

At the moment, the majority of analysts supplying their forecasts to Reuters project that the RBA will not deliver an interest rate increase before Q3 2018, but 14 out of 27 anticipate at least one quarter percentage point hike by the end of the year.

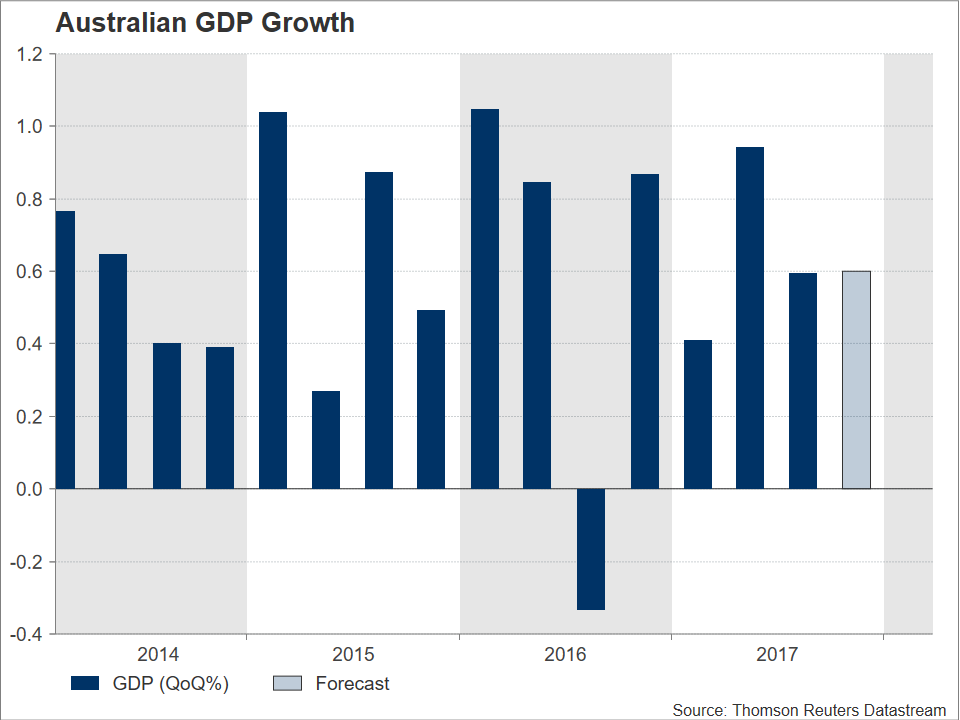

The country's Q4 2017 GDP figures are due on Wednesday at 0030 GMT. Quarter-on-quarter and year-on-year, the pace of expansion is projected to stand at 0.6% (same pace as in Q3) and 2.5% (versus 2.8% in Q3) respectively. It is perhaps important to mention within the context of growth figures, that last week's data on Q4 capital expenditure surprised to the downside, with private capex recording a fall by 0.2% rather than the 0.9% expansion that was forecast by analysts. The data were met with a selloff in the Australian currency.

Euro Continues to Struggle amid Italian Political Risks; European StocksRise

Here are the latest developments in global markets

FOREX: The euro remained under pressure during early European afternoon as Sunday's elections in Italy which ended to a hung parliament, undermined Eurozone's prospects, with Eurosceptic parties gaining some ground. However, investors' confidence on the bloc's economic performance and an expected grand coalition deal between Merkel's Conservatives and their previous partners, the SPD, provided some support to the currency, with euro/dollar rising back to 1.2332 before it inched lower to 1.2295 (-0.16%). Euro/yen and euro/pound were down at 129.93 (-0.23%) and 0.8900 respectively (-0.21%). Pound/dollar managed to edge up to a fresh five-day high of 1.3834 (+0.09%) following stronger than expected services PMI readings for the month of February but sentiment on the currency remained weak as investors were waiting for the EU to clarify its Brexit position this week after the UK Prime Minister, Theresa May asked the EU to use a more flexible stance on future negotiations. The dollar index stood at 90.07 and dollar/yen traded lower at 105.62 as investors turned their focus on safer assets amid a potential escalation in trade tensions) between the US trade and the rest of the world. Dollar/loonie gained positive momentum, rallying near to an eight-month high of 1.2928 as Trump's proposed import tariffs on aluminum and steel were said to complicate NAFTA talks. The US president, Donald Trump tweeted on Monday that "tariffs will only come off if new and fair NAFTA agreement is signed". Note that the seventh round of NAFTA negotiations concludes today.

STOCKS: European stocks opened higher on Monday after posting losses for four consecutive days. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.66% and 0.54% respectively at 1100 GMT with all sectors being in the green as the political gridlock in Germany came to an end, offsetting losses arising from disappointing Italian elections and Trump's proposed hefty import tariffs. The German DAX 30 surged by 0.93%, the French CAC 40 rose by 0.50%, and the Spanish IBEX 35 climbed by 0.56%. On the other hand, the Italian FTSE MIB tumbled by 0.58% to six-month lows in the wake of political risks, with the banking sector being set to print its biggest daily loss since May 2017. The UK's FTSE 100 increased by 0.34%. US stock futures were mixed.

COMMODITIES: Oil prices were moving to the upside but fears of rising US output continued to hold investors cautious, with the International Energy Agency revising the US oil output upwards significantly on Monday and claiming that the US could steal part of OPEC's market share by 2023. Meanwhile, operations at Libya's El Sharara oilfield resumed today after a shut down on Sunday due to environmental protests, according to Reuters. WTI crude and Brent were last trading at $61.41.(+0.26%) and $64.40 (+0.06%) respectively. In precious metals, gold held onto gains, fluctuating around $1324/ounce.

Day ahead: Italian political developments in focus; RBA decides on interest rates during the Asian session

Day ahead: Italian political developments in focus; RBA decides on interest rates during the Asian session

Political updates in Europe will be in the spotlight during the coming days following an inconclusive election in Italy which increased Eurosceptic voices, despite an expected coalition deal in Germany.

On Sunday, Italian exit polls showed that no party had enough votes to form a majority government as anticipated but gave a lead to anti-EU parties, pointing to a period of political instability in the third largest EU economy. The anti-establishment Five Star Movement (M5S) gained 29-32%, above the 20.5% won by the pro-EU center-left Democratic party, while Berlusconi's center-right Forza Italia and the anti-immigration League party were said to attract only 13-16% of the votes, leaving room to the M5S to negotiate a position in the government. According to the media, the Italian Parliament will meet on March 23, while formal talks are not expected to start until early April. The Italian constitution does not specify any time limit for the parties to deal an agreement or settle new elections.

Brexit uncertainties are also back on the cards and are expected to weigh on market sentiment as the gap between the EU and the UK doesn't seem to be getting narrower after the UK Prime Minister backed Brexiteers last week, rejecting EU proposals to retain custom union rules in Northern Ireland. However, during her speech on Friday, she expressed some ideas on how to maintain a softer border with the Irish Republic.

Central bank meetings will be of greater interest this week, with the Reserve Bank of Australia being the first in line to decide on interest rates early on Tuesday (0330 GMT). However, for once again policymakers have no intention to tighten monetary policy, keeping rates at a record low of 1.5% given the sluggish inflation and the overloaded household debt. The Bank of Canada, the European Central Bank and the Bank of Japan will announce their own decisions later in the week ahead of the famous US nonfarm payrolls due on Friday.

Concerns over a potential trade war between the US and the rest of the world, triggered by Trump's announcement of punitive import tariffs on aluminum and steel last week, may continue to restrict any stock market gains. China, the world's biggest exporter, has already claimed that it doesn't want a trade war with the US, but it will respond accordingly if the measures harm its interests.

Looking at today's economic calendar, data releases will be relatively light, with the US reporting ISM non-manufacturing PMI for the month Of February at 1500 GMT. Forecasts are for the index to decline by 0.9 points to 59.0, remaining safely above the threshold of 50 which separates growth from contraction.

As for the speakers, Fed Board member Randal Quarles (voter) is due to deliver remarks at 1815 GMT. In the UK, Finance Minister Philip Hammond will appear before Parliament to discuss the government's plans for leaving the EU.

In energy markets, a meeting between major US shale firms and OPEC oil ministers will be closely eyed, amid expectations that the two sides could coordinate in order to prevent another oversupply crisis.

Loonie Remains Under Strong Pressure on NAFTA, US Tariffs; Psychological 1.30 Barrier in Focus

The USDCAD maintains firm bullish sentiment and broke above strong barriers at 1.2920 (former triple top/2018 high), extending the upleg from 1.2610 (23 Feb trough) into sixth straight day. Canadian dollar remains under increased pressure, driven lower by rising concerns about NAFTA talks which are at their finals, as President Trump characterized it as bad deal for the USA and being overshadowed by US tariffs on imported steel and aluminum.

United States are the biggest market for Canada's metals, with stronger negative impact to be expected if tariffs will be fully imposed to Canada and NAFTA talks end without desired result. The pair is in uninterrupted ascend from 31 Jan trough at 1.2248 and is riding on the third wave of five-wave sequence from 1.2248.

The wave broke above its FE100% at 1.2880, to validate the wave principles and is eyeing next targets at 1.2981 (FE123.6%) and psychological 1.3000 barrier.

Strong bearish signal was generated on break above lower base/triple-top at 1.2920, with close above it needed to confirm and open way for extension broader recovery phase from 1.2061 (08 Sep low) for further retracement of 1.3793/1.2061 (May-Sep 2017 fall).

Firm break above 1.30 barrier would open way towards next key barriers at 1.3131 (Fibo 61.8% of 1.3793/1.2061) and 1.3146 (FE 161.8% of the wave C from 1.2450 (16 Feb trough). Daily MA's in full bullish setup, formed several bear-crosses, to further underpin the rally, as momentum continues to trend higher.

A breather in recent strong rally could be anticipated in coming sessions as daily RSI and slow stochastic entered overbought territory, but so far did not create firmer bearish signal.

Res: 1.2981; 1.3000; 1.3044; 1.3146

Sup: 1.2920; 1.2865; 1.2820; 1.2765

Canadian Dollar Slide Continues After Weak GDP

The Canadian dollar has posted losses in the Monday session. Early in the North American session, USD/CAD is trading at 1.2959, up 0.58% on the day. On the release front, there are no Canadian events. In the US, today’s key indicator is Non-Manufacturing PMI, which is expected to dip to 58.9 points. On Tuesday, Canada releases Ivey PMI.

Canada’s economy slowed down in January, as GDP posted a weak gain of 0.1%, matching the estimate. On an annualized basis, growth in the fourth quarter was 1.7%, considerably lower than the Bank of Canada’s most recent projection of 2.5%. With the Fed expected to raise rates up to four times in 2018, the BoC will be pressed to match rate hikes with its southern neighbor, or risk having the Canadian currency head lower. Currently, the BoC is projecting only two rate hikes in 2018. Strong growth has propelled the BoC to raise rates three times since July, but there are some factors weighing against a rate hike before May. First, fourth quarter expansion may fall short of the BoC’s forecast of 2.5%. As well, the future of NAFTA remains unclear, as negotiations between Canada, Mexico and the US have floundered. If the US decides to pull out of NAFTA, the repercussions on the Canadian economy could be significant, and the BoC will have to delay any plans to raise rates.

Canadian policymakers continue to look with growing alarm at protectionist moves by the Trump administration. Negotiations on NAFTA have not shown much progress, as a seventh and final round of talks are underway in Mexico City. As if the headache of a possible blowup of NAFTA wasn’t bad enough, the Canadian government now has to deal with the stiff imports that President Trump is set to apply to steel and aluminum imports. With some 80% of Canadian exports heading south to the US, Canada can ill afford a trade war with its giant neighbor. Still, the government will be under pressure to respond forcefully and stand up for its domestic steel industry.