Sample Category Title

DAX Moves Higher After Rough Week

The DAX index has started the week with considerable gains. In the Monday session, the index is trading at 11,998.58, up 0.70% since the Friday close. On the release front, Eurozone indicators were a disappointment. German and Eurozone Services PMIs dropped in February and missed their estimates. Still, both indicators continue to point to expansion. Elsewhere, Sentix Investor Confidence dropped to 24.0, well off the estimate of 31.1 points. This was its weakest reading since April 2017. Retail Sales declined 0.1%, shy of the estimate of +0.3%. This marked a third decline in the past four months, raising concerns about consumer spending in the eurozone.

It was a dreadful week for the DAX, which slipped 4.6% if its value. European stock markets reacted negatively following US President Trump’s decision to impose stiff tariffs on steel and aluminum imports in order to protect domestic producers. Under the new scheme, foreign steel will be taxed at 25% and aluminum at 10%. The response to the move was overwhelmingly negative, both abroad and in the US. China and the EU immediately denounced the move and US auto makers and oil and gas producers also condemned the tariffs. In imposing the tariffs, Trump relied on a provision which allows such measures for national security, but clearly, US trading partners will not quietly accept these protectionist measures. If these countries retaliate, a nasty trade war could ensue, which would likely unnerve investors and send the markets even lower.

The Federal Reserve was in the spotlight last week, as Jerome Powell delivered his maiden speeches to Congress last week. Next up is the ECB, as policymakers meet on Thursday. Will Draghi & Co. deliver more of the same? The markets will be paying close attention to the language used by ECB, as there is a possibility of removing the easing bias regarding bond purchases. A removal of the easing bias would likely be interpreted as a plan to tighten policy and could impact on the stock markets. Inflation remains weak, so there is little pressure on the ECB to tighten policy anytime soon. Recent indicators show that inflation in the eurozone is steady, but remains well below the ECB target of around 2 percent. Eurozone CPI dipped to 1.2% in February, down from 1.3% in January.

Futures Steady as Trump Tariff Stance Hardens

Stocks Rebound After Trump Tariffs Rattle Markets

US equity markets are on course to open relatively unchanged at the start of the week after bouncing back from early losses on Friday, which came as Donald Trump announced tariffs on steel and aluminium.

With the US President threatening tariffs on car imports should the EU retaliate, there is a real possibility that a trade war could unfold which doesn't work to anyone's benefit. The prospect of this rattled markets on Friday but this didn't last long and US equities quickly bounced back, with the S&P 500 ending the day half a percentage point higher. European stocks have been playing catch up at the start of the week, although automakers continue to struggle after Trump's threats.

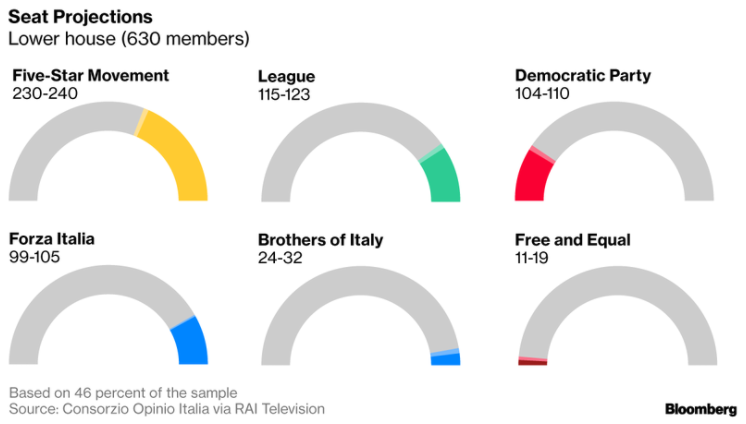

FTSE MIB Under Pressure as Projections Show Strong Performance of Populist Parties in Election

The Italian election over the weekend likely failed to produce a majority government, with projections showing the Five Star Movement was the largest single party and the centre-right block received the most votes. Negotiations will now commence to form a government which is likely to take months and could yield a coalition of the League and Five Star Movement, which could be very problematic for Italy's partners in the European Union.

Source – Bloomberg

Source – Bloomberg

While European stock indices have largely shrugged off the Italian election result, the FTSE MIB was down more than 1% in early trade as investors worry that prolonged coalition talks and the possibility of an anti-establishment majority could harm the economy. The last 12 months has seen a number of anti-establishment parties defeated in elections across the EU, which was celebrated as a victory over the populists and an endorsement for the EU project. This result suggests people aren't as supportive as European leaders would have us believe.

Mixed PMIs Seen Across Europe

The euro has also been unaffected by the result, and trades only marginally lower on the day. The PMI data for the region won't be helping the currency, with the final readings being revised a little lower, although they still remain comfortably in growth territory. Retail Sales data also suggested that January wasn't a great month for the region compared with December, although gradual progress is being seen year on year.

EURUSD Daily Chart

OANDA fxTrade Advanced Charting Platform

OANDA fxTrade Advanced Charting Platform

The UK services PMI was more encouraging though, jumping to 54.5 in February, its highest since October. The services sector is incredibly important to the UK, covering more than three quarters of total output, so movements in the PMI tend to be monitored very closely and can give a strong indication about how the economy is managing, particularly during challenging periods like this. Still to come we have US final services and ISM non-manufacturing PMIs and we'll also hear from FOMC voter Randal Quarles.

Euro Subdued, Shrugs Off Soft Services PMIs

It's a quiet start for the euro in the Monday session. Currently, EUR/USD is trading at 1.2306, down 0.10% on the day. On the release front, eurozone numbers disappointed, as services PMI, retail sales and consumer confidence all missed their estimates. In the US, today's key indicator is Non-Manufacturing PMI, which is expected to dip to 58.9 points. On Sunday, Italians went to the polls, and the euro-skeptic parties did quite well, as the country appears headed to political deadlock.

The euro gained 1.0% late last week, after US President Trump announced that he would be imposing stiff tariffs on steel and aluminum, in order to protect domestic producers. Under the new scheme, foreign steel will be taxed at 25% and aluminum at 10%. The response to the move was overwhelmingly negative, both abroad and in the US. China and the EU immediately denounced the move. US auto makers and oil and gas producers also condemned the tariffs, saying they could get caught in the middle of a nasty trade war if other countries retaliate. In imposing the tariffs, Trump relied on a provision which allows such measures for national security, but clearly, US trading partners will not quietly accept these protectionist measures.

The Federal Reserve has been in the spotlight in recent weeks, but market attention shifts to the ECB this week, as policymakers meet on Thursday. No major changes are expected, but members could discuss the possibility of removing the Bank's easing bias towards increasing bond purchases if needed. A removal of the easing bias would likely be interpreted as a plan to tighten policy and would be bullish for the euro. Inflation remains weak, so there is little pressure on the ECB to tighten policy anytime soon. Recent indicators show that inflation in the eurozone is steady, but remains well below the ECB target of around 2 percent. Eurozone CPI dipped to 1.2% in February, down from 1.3% in January.

Euro Falls On Uncertainty Over Italy, Equities Remain Under Pressure On Trade Concerns

Here are the latest developments in global markets:

FOREX: The dollar index was gaining ground, while the euro was on the defensive following a cloud of uncertainty after Sunday’s elections in Italy. The aussie and the kiwi were also recording notable losses versus the greenback on the back of rising trade tensions.

STOCKS: US markets closed mostly higher on Friday, even despite the rising probability of a tit-for-tat trade war between the US and its major partners. The Nasdaq Composite surged 1.1%, while the S&P 500 rose 0.5%. The Dow Jones, on the other hand, declined 0.3%. The turbulence in equity markets seems to be far from over, as futures tracking the Dow, S&P and Nasdaq 100 are all currently well into negative territory, signaling a negative open today. Asian markets continued to underperform amid heightened trade concerns. In Japan, the Nikkei 225 and the Topix pulled back by 0.7% and 0.8% respectively, while in Hong Kong, the Hang Seng plunged 2.2%. In Europe, futures tracking most of the major benchmarks were flashing red today, indicating that these indices may extend the losses they posted on

COMMODITIES: In energy markets, oil prices were trading a little higher on Monday, with WTI and Brent crude both rising a little more than 0.1%. The gains are being attributed to supply disruptions in Libya, as well as optimism that a meeting between OPEC ministers and US shale firms later today will help to address oversupply concerns. In precious metals, gold was 0.3% higher on Monday, last seen near the $1326/ounce mark. The precious metal has managed to regain some ground lately as investors focused on the prospect of a retaliatory trade war hurting the global economy, and could well extend its gains if such worries intensify further.

Major movers: Euro declines on Italian political uncertainty; yen continues to gain; antipodeans retreat, hurt by trade concerns

The eurozone’s common currency was losing ground after initial results from Sunday’s Italian elections showed no clear winner, pointing to a hung parliament. Populist-perceived parties did have a strong showing though, and this is perhaps another reason – besides the uncertainty – for the euro’s decline.

The German Social Democratic Party’s (SPD) decision to support a “grand coalition” with Chancellor Merkel’s conservative bloc is seen as euro-supportive, but still it wasn’t enough to prevent the currency from recording losses.

Euro/dollar was 0.3% down at 1.2282, while the single currency extended its losses versus the yen following considerable declines during the week that preceded. Euro/yen was 0.6% down, trading not far above a fresh six-month low of 129.33.

Meanwhile, American tariffs continue to weigh on sentiment and this is particularly evident in equity markets. On this front, it is interesting that China said it will host US officials for a new round of talks on trade issues.

Turning to the greenback, the dollar index was 0.25% higher at 90.14, gaining mostly on the back of a weaker euro as the US currency kept retreating versus the yen. Dollar/yen was 0.35% down at 105.36, close to the near 16-month low of 105.23 hit on Friday. The Japanese currency benefitted last week as BoJ Governor Haruhiko Kuroda made talk of an exit from ultra-easy monetary policies. Despite that being dependent on the Japanese central bank meeting its inflation target, still markets interpreted it as paving the way for policy normalization.

Pound/dollar was 0.1% down with Brexit developments remaining in focus following last week’s speech by UK PM Theresa May on the future relationship between the Britain and the EU.

The antipodeans were recording losses versus the US dollar, with aussie/dollar and kiwi/dollar trading lower by 0.3% and 0.4% respectively. Both Australia and New Zealand rely on commodity exports and it is thus natural for rising trade tensions to act as a drag on their currencies. Australia saw the release of some strong numbers, including on building approvals, earlier on Monday, but still they weren’t enough to halt the currency’s decline.

Day ahead: Italian election results awaited; UK and US PMIs in focus ahead of a busy week

The euro was trading on a softer tone on Monday, as the positive coalition outcome in Germany was not enough to offset the political concerns emanating from Italy. The results of the Italian election are still not official yet, though exit polls and projections point to a hung parliament, i.e. no single party or coalition having gained enough votes to establish a majority. While this should come as little surprise considering that opinion polls suggested as much, what probably caught the market off-guard is the surge in popularity for Eurosceptic parties like the Five Star Movement (M5S) and the Northern League.

Once the results are finalized, attention will shift to the coalition-making process, which promises to be a lengthy one considering that the M5S (that is now the largest single party) previously said it wouldn’t participate in any coalition. Although the euro could remain under some pressure as markets digest the commotion in Italy, the currency’s short-term bias may be decided primarily on Thursday, when the European Central Bank (ECB) meets.

Turning to economic data, in the UK, traders will turn their sights to the release of the services PMI for February, at 0930 GMT. The index is expected to have risen to 53.3 from 53.0 previously, which would signal that the UK’s largest sector gained some momentum during the month. At the time of writing, markets have priced in a 70% probability for the Bank of England to hike rates in May, and a strong services PMI today could push that number higher, potentially helping sterling to recover some of its latest Brexit-related losses.

In the Eurozone, retail sales (1000 GMT) for January are anticipated to have rebounded in monthly terms, and to have accelerated somewhat on a yearly basis.

Out of the US, the ISM non-manufacturing PMI for February is due out at 1500 GMT. The index is projected to decline to 59.0, from 59.9 in the previous month. Interestingly enough, the manufacturing print for the month beat a similar forecast for a decline and instead surged to reach a high last seen in 2004. Thus, investors may look to the non-manufacturing print in order to gauge whether that was an isolated phenomenon, or whether the broader economy indeed picked up some speed in February.

As for the speakers, Fed Board member Randal Quarles (voter) is due to deliver remarks at 1815 GMT. In the UK, Finance Minister Philip Hammond will appear before Parliament to discuss the government’s plans for leaving the EU.

In energy markets, a meeting between major US shale firms and OPEC oil ministers will be closely eyed, amid expectations that the two sides could coordinate in order to prevent another oversupply crisis.

Elsewhere, this will be a particularly calendar-heavy week, packed with central bank meetings. The week begins with a Reserve Bank of Australia gathering on Tuesday, following by a Bank of Canada decision on Wednesday. On Thursday, the ECB gathering will be in the spotlight, while on Friday, the Bank of Japan will announce its own decision a few hours before the US releases its all-important nonfarm payrolls report for February. In China, the annual National People’s Congress kicked off today, with Premier Li Keqiang announcing that the nation’s growth target for 2018 will be 6.5%.

Technical Analysis: Gold looking bullish in short-term as it records 6-day high

Gold has advanced considerably after hitting a two-month low of 1,302.70 on March 1. Earlier on Monday it rose to 1,327.66, this being a 6-day high, while it is currently trading not far below this level.

Technical indicators are pointing to a bullish picture in the short-term: the Tenkan-sen line has crossed above the Kijun-sen, while the RSI indicator is heading higher, having crossed above the 50 neutral-perceived level.

More uncertainty, either on the political front or on trade, is likely to boost the safe-haven perceived asset. In this case, resistance might occur around the current level of the 100-period moving average at 1,330.17.

On the other hand, should political and trade considerations ease, the precious metal could lose part of its allure and record losses. In this case, support could come around the 50-period moving average at 1,324.46. Price action is taking place close to this level with further declines shifting the focus to the Tenkan-sen at 1,321.41.

Technical Outlook: EURUSD – Uncertainty From Italy Election Was Partially Offset By German SPD Vote, Daily Cloud Top Holds...

The Euro stands at the back foot at the beginning of European session on Monday and returned below 1.23 handle, after upside attempts in early Asian trading were rejected at 1.2364.

Fresh easing pressures the top of rising daily cloud (1.2264) which contained pullback from 1.2555 peak and underpinned recovery rally on Thu/Fri.

Recovery stalled on initial attack at important resistances at 1.2350/55 zone (30SMA / daily Kijun-sen / 50% retracement of 1.2555/1.2154 pullback), lacking for now stronger bullish signal expected on break.

Daily MA's are in mixed setup, but 14-d momentum is returning to negative territory and signaling existing downside risk.

Daily cloud top marks key near-term support, firm break of which would weaken near-term structure and turn bias into negative mode, risking further weakness and possible retest of correction low at 1.2154, posted on 01 Mar.

On the other side, hopes for fresh attempts higher would remain in play while cloud top contains dips, however, close above cracked 30SMA (1.2348) is seen as minimum requirement to signal further recovery and expose next target at 1.2400 (Fibo 61.8% of 1.2555/1.2154 bear-leg).

Initial outcome from highly anticipated Italian election show no major blocs winning an outright majority, but negative signal came from stronger than expected showing from euro-skeptic bloc, which could undermine the single currency.

Final results are expected later today and should be generally in line with expectations, with markets turning focus on coalitions that will be formed after the election as none of parties and blocs won an absolute majority.

Initial worries on the outcome of Italian election was partially offset by vote of German SPD party to back another coalition with Chancellor Angela Merkel's conservative, which would provide Merkel another term as German chancellor.

Series of Services PMI data from Eurozone countries are in focus today, with forecasts showing no changes from the previous release.

EU retail sales are expected to rise in Jan according to forecasts at 0.3% m/m vs -1.1% in Dec and 2.1% y/y in Jan vs 1.9% in Dec, which could inflate the Euro on stronger upside surprise.

Res: 1.2335, 1.2364, 1.2400, 1.2435

Sup: 1.2287, 1.2264, 1.2251, 1.2205

Italy Services PMI down to 55.0 vs exp 57.3, Slower growth compared to January recorded

Italy Services PMI down to 55.0, vs exp 57.3, from prior 57.7.

Key findings:

- Slower growth compared to January recorded

- Activity and new business nonetheless still increase at marked rates

- Further jobs added as workloads continue to

increase

Paul Smith, Director at IHS Markit which compiles the Italy Services PMI survey, said:

"Following a stellar start to the year, the Italian service sector saw growth weaken in February but sustained at a decent clip. Midway through the first quarter of 2018 the economy is firmly on course to deliver a similar sized level of quarterly GDP growth to those seen over the past year or so.

"Demand conditions remain favourable, and rising workloads mean that companies continue to take on additional workers, albeit in a relatively careful and considered manner.

"Recruitment is also being supported by positive expectations for growth, with service providers retaining an optimistic outlook and indicating plans to raise investment levels over the coming 12 months."

Investors Focus On German And Italian Political Outcomes

Italy will remain under the control of the present caretaker government and Paolo Gentiloni, the current Prime Minister, will continue his job. The Italian election results have produced a very predictable outcome- no party has a clear majority. In other words, we have a hung parliament and in Italy, there is no pressure or time limit to form a government. So, basically we have a prolong period of political uncertainty which would weigh on country's economic condition.

We do know that the negotiations process to form a government would take several rounds of talk and months in terms of time period. However, if the discussions turns really sour and situation starts to look like out of control, there are strong chances that Italians may have to go back to the polling stations to vote again

Nonetheless, for now, the reaction from the markets is more subtle. Initially, the Euro popped to the upside as investors celebrated that the worst outcome didn't become a reality- the Five Star movement party, coming into the power. But, it is not all glory for the Euro, because in Germany, the leadership of German Chancellor, Angela Merkel, has weakened and she has a lot to deal with. The combination of hung parliament, Angela Merkel losing some control over in Germany and fears of trade war are going to weigh on the euro.

Moving away from this, the trade war is the major focal point for investors. We do see a full scale trade war coming as other countries would not stay reticent and watch the show. The full blown trade war would hurt the global economy and the risk sentiment would only spur further.

Trade War Fears Keep Investors On The Defensive

Global equities are likely to slide on Monday as concerns about a global trade war continue to weigh on investor sentiment. The E.U. was fast to respond to Donald Trump’s threatening tariff talk by calling a meeting this week to discuss protective measures, in case the U.S. proceeds with imposing tariffs on steel and aluminium. European Commission President, Jean-Claude Juncker, is expected to hit back by proposing countermeasures against the U.S. and similarly, Canada and China are wowing to retaliate.

I expect that this trade fight will be messy and cause more volatility in equities, fixed income and currency markets in the short run. However, I believe this may end up with the E.U. and China taking a less protectionist stance, rather than the U.S. taking a stronger one. After all, there is no winner from a trade war in the long term, and policymakers know that very well. Until this scenario fully plays out, I expect to see a further selloff in equities and even fixed income markets, with the primary beneficiaries being the Japanese Yen and gold.

The Euro found no support after Germany’s Social Democratic party voted for a coalition deal with Angela Merkel’s CDU party. The muted Euro reaction is mainly due to worries that the Italian elections delivered a hung parliament. The European Union would have a new headache to deal with if Italy formed a Eurosceptic coalition which would undoubtedly challenge E.U. budget rules. Expect to see a sharp fall in Italian equities today.

On the data front, eurozone services PMIs are likely to show a little bit of a slowdown later today, similar to what we saw in the manufacturing sector last week, but the figures are unlikely to have a significant impact on the Euro.

Investors have lot of news to digest this week.

Monetary policy meetings

The European Central Bank meeting on Wednesday is not expected to result in any change to the asset purchase program or interest rates. Traders will be focusing mainly on the language of the statement, particularly on any changes in the forward guidance. Given the strong performance in the Eurozone’s economic recovery, many investors are waiting for signals for when the ECB will quit buying bonds. At this stage I think no clear signal will be given. However, the potential of upscaling of QE is likely to be removed from the statement. Thus, the meeting is likely to be slightly positive for the EUR.

Bank of Canada and Reserve Bank of Australia are also meeting this week. Given the slight slowdown in recent economic data, I expect both central banks to keep policy unchanged and the meetings are likely to be a non-event for currency traders.

U.S. Jobs Report

Traders will closely watch the U.S. non-farm payrolls reports. Although hiring is expected to have picked up slightly in February and employment to remain at 4.1%, both these figures will be ignored. Investors are mainly concerned about the average hourly earnings figure. After increasing at the fastest pace in almost a decade, wage growth is expected to fall 0.4% YoY. If this materializes, then previous inflation fears which caused the steep drop in equities beginning of February, will likely ease.

Forex Analysis: PMI Data To Be Released Today As The Steel Tariff Fallout Continues

German Retail Sales (YoY) (Jan) was released coming in at 2.3% v an expected 3.3%, from -1.9% previously, which was revised to -0.2%. Retail Sales (MoM) (Jan) was -0.7% v an expected 0.8%, from -1.9% previously, which was revised to -1.1%. This data is usually volatile but on this occasion, it has surprised to the downside marginally. EURUSD moved lower to eventually test 1.22512.

UK PM May gave a prepared speech on Friday on Brexit progress and ongoing negotiations with the EU. Of particular interest was her policy on trade regulations and the Northern Irish border. In that regard, one of the takeaways from her statements was that there is an option for a customs partnership between the EU and the UK. She said that to avoid a hard border, an agreement on customs was needed. The best option involved a highly streamlined customs arrangement with simple requirements for the movement of goods. She promised that the UK would maintain the high standards of the EU including maintaining environmental standards to a level at least as high but also wanted flexibility on this and the fisheries policy. In her speech, she made it clear that the level and type of market access of some services will not be the same as pre-Brexit. Her key tests for Brexit success were:

1. Implementing the decision of the British people

2. Reaching an enduring solution

3. Protecting security and prosperity

4. Delivering an outcome consistent with the kind of country we want to be

5. Strengthening the Union

'I want to be straight with people – we all need to face up to some hard facts' – ‘in certain ways our access to markets will be less than it is now' – we can't have all the benefits without all the obligations'.

Market reaction to her speech was indecisive with GBPUSD moving higher to 1.38017, then selling to 1.37604, before recovering to starting levels around1.37880. EURGBP moved lower to 0.89155 but then rallied to 0.89488. FTSE traded around 7088.00.

UK Construction PMI (Feb) was released and came in at 51.4 v an expected 50.5, with a prior number of 50.2. This data is based on a survey of purchasing managers, with a reading above 50 indicating expansion and below 50 indicating contraction. This number has been trending down since a high of 64.7 in February 2014. GBPUSD moved lower from 1.37876 to 1.37606 upon this data breaking. It can see a seasonal pick up around this time, heading into summer and due to increased construction activity but like-wise, any failure for this to take place could indicate a downturn in the sector.

Eurozone Producer Price Index (YoY) (Feb) was 1.5% v an expected 1.6%, from 2.2% previously. This data represents the change in the price of finished goods and services sold by producers. A number lower than the consensus shows that the value of goods has decreased but represents a saving for consumers. EURUSD moved higher after this release from 1.22741 to 1.22979.

Canadian Gross Domestic Product (MoM) (Dec) was as expected at 0.1% from a prior reading of 0.4%. The range of this data point since 2010 has been between +0.6% and -0.6% and a reading outside of this range would result in a larger market reaction. Gross Domestic Product Annualized (QoQ) (Q4) was 1.7% v an expected 2.1%, with a prior reading of 1.7%, which was revised down to 1.5%. USDCAD initially moved up to 1.23180 but then sold off to 1.22937 after this data was released, as the headline number was in-line with expectations.

Baker Hughes US Rig Count numbers were released, with the headline number coming in at 800. The prior number last Friday showed that there were 799 Oil rigs in operation. WTI Oil traders pay close attention to this number as they look to the week ahead, with an increase from the prior week showing an expansion and indicating an increase in the volume of crude oil drilled. In the context of supply and demand, this would mean an increase in supply. The Number of operational rigs has not been at the 800 level since 2015.

EURUSD is down -0.20% overnight, trading around 1.22917.

USDJPY is down -0.16% in early session trading at around 105.543.

GBPUSD is down -0.13% this morning, trading around 1.37816.

Gold is up 0.24% in early morning trading at around $1,325.50.

WTI is up 0.16% this morning, trading around $61.28.

Major data releases for today:

PMI – Purchasing Managers Index Data will be released for various economies around the world today. The Index is used to gauge the level of business conditions including employment, production, new orders, prices, supplier deliveries, and inventories, by compiling surveyed data from purchasing managers. A reading below 50 indicates contraction in the industry while above 50 indicates growth. This data is important due to the link with interest rates. In the current stage of the economic cycle, it can be a warning for inflation increasing, which has caused selling in risk assets recently.

At 08:15 GMT, Spanish Markit Services PMI (Feb) is expected to be 56.5, from a previous reading of 56.9.

At 08:55 GMT, German Markit Services PMI (Feb) is expected to be unchanged at 55.3. Markit PMI Composite (Feb) is expected unchanged at 57.4. EUR crosses could be affected by this data.

At 09:00 GMT, Eurozone Markit Services PMI (Feb) is expected to be unchanged at 56.7. Markit PMI Composite (Feb) is expected to be unchanged at 57.5. EUR crosses could be moved by this data.

At 14:45 GMT, US Markit Services PMI (Feb) is expected to be unchanged at 55.9. Markit PMI Composite (Feb) is also expected to be unchanged at 55.9. USD crosses could be moved by this data.

At 15:00 GMT, US ISM Non-Manufacturing PMI (Feb) will be out with a consensus of 58.9 expected, against a prior reading of 59.9.

Major data releases for the week ahead:

On Tuesday at 03:30 GMT, the RBA will release Australian Rate Statement and Interest Rate Decision.

On Wednesday at 10:00 GMT, Eurozone GDP data will be released.

Later at 15:00 GMT, the BOC will release the Canadian Rate Statement and Interest Rate Decision.

On Thursday at 12:45 GMT, the ECB will release the Eurozone Interest Rate Decision and Deposit Rate Decision with a press conference and the Monetary Policy Statement at 13:30 GMT.

On Friday at 04:00 GMT, the BOJ will release the Japanese Interest Rate Decision and Monetary Policy Statement. They will also hold a press conference.

At 13:30 GMT, US Jobs data will be released for February.

RBA Preview – Westpac: RBA to hold

RBA will announce rate decision tomorrow.

Exerpts from the Westpac report:

- The Reserve Bank Board meets next week on March 6. Of course we expect there will be no change in the overnight cash rate.

- We also do not expect to see any significant change in the Governor's rhetoric from last month.

- Overall, we are expecting a cumulative fall (in USD's) in Australia's Commodity Price Index of around 25% between June 2018 and December 2019.

- Readers will be aware that Westpac expects a considerable widening in the negative Australia/US interest rate differential as the FEDERAL RESERVE continues to raise rates and the RBA remains on hold.

- Readers should be aware that Westpac has reviewed its currency forecasts and, while continuing to see an AUD low of USD 0.70 in 2019, has pushed out the timing to September 2019 from March.

Details in Australia & New Zealand Weekly: RBA on Hold, AUD to Weaken through 2018 and 2019