Sample Category Title

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2267; (P) 1.2301 (R1) 1.2351; More....

EUR/USD edged higher to 1.2363 earlier today but fails to sustain above 1.2354 resistance so far. Intraday bias remains neutral first. On the upside, above 1.2363 should extend the rebound from 1.2154 to retest 1.2555 high. Firm break there will carry larger bullish implication. On the downside, break of 1.2154 would revive the case of rejection by 1.2516 key fibonacci level and trend reversal. Outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2555 at 1.1708.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Eurozone Data The Talk Of Monday

A steady stream of Eurozone data will make its way through the markets on Monday. In political news, investors are still evaluating the outcome of Italy’s national election, which delivered a hung parliament with the anti-establishment Five Star Movement set to take top place.

IHS Markit will deliver a deluge of PMI data beginning at 08:15 GMT with reports on Spanish, Italian, French, German and euro-wide services activity. Eurozone services PMI is forecast to come in at 56.7; the Composite indication, which tracks services and manufacturing, is expected to come in at a solid 57.5.

On the PMI scale, anything above 50 signals expansion in economic activity.

At 09:30 GMT, Sentix will report on Eurozone investor confidence for the month of March.

The European Commission’s statistical agency will issue its monthly retail sales report at 10:00 GMT. Receipts at retail stores are forecast to rise 0.3% in January, which translates into a year-over-year gain of 2.2%.

Shifting gears to North America, Markit and the Institute for Supply Management (ISM) will each issue respective PMI reports for the month of February. ISM’s non-manufacturing PMI is forecast to ease slightly to 59.4 from 59.9 the previous month.

Earlier in the day, Caixin China’s services PMI showed a slight drop in the country’s non-manufacturing industries. The services PMI slipped to 54.2 from 54.7 in January.

EUR/USD

Europe’s common currency snapped back to health on Friday, rising more than 50 pips against the dollar to reclaim the 1.2300 handle. The EUR/USD exchange rate was last seen trading at 1.2323 for a daily gain of 0.1%. The pair is trading right around the 20-day moving average and faces immediate support at the psychological 1.2300 level. Economic data throughout the week will influence the direction of this pair, culminating in a report on US nonfarm payrolls on Friday.

GBP/USD

Cable extended losses at the end of last week, falling below 1.3800 for the first time in three weeks. GBP/USD was last seen hovering at 1.3789, where it was down around 0.1% from the Friday close. Cable is currently trading within a bearish channel marked by Brexit risks and a rebounding US dollar. In terms of technical levels, immediate support is located at 1.3750.

USD/JPY

The dollar-yen exchange rate opened the week in negative territory, extending last Friday’s sharp decline. The USD/JPY was down 0.2% at 105.48, its lowest since 2015. In terms of technical levels, the USD/JPY faces immediate support at 105.20, followed by 104.75. On the opposite side of the ledger, key resistance levels include 105.85 and 106.30. In addition to US data this week, the Japanese government will report on GDP and household spending. On Friday, the Bank of Japan will also deliver a rate verdict.

Market Update – Asian Session: China Sets 2018 GDP Growth Forecast In Line With Market Speculation

Headlines/Economic Data

General Trend: Asian equities trade mostly lower as steel makers remain weaker

Euro rises then pares gains amid release of Italy election results: No majority is expected (in line with prior market speculation), while support for Five Star Party rises

Precious metals outperform in the commodities space: Silver gains over 1%

Tuesday is a busy day for Australia: Q4 Current Account and Net Export Contribution expected to be released, along with Jan Retail sales and RBA decision

Japan bond yields decline amid drop in Treasury yields and rise seen on Friday after BoJ Gov Kuroda’s remarks

USD/JPY declines ahead of upcoming BoJ confirmation hearings

US Feb Nonfarm Payrolls and Avg Hourly Earnings data due for release on Friday, March 9th

Australia/New Zealand

ASX 200 opened flat: closed -0.7%

ASX 200 Utilities Index -2.3%, Materials -1.2%, Resources -1.1%, Financials -1%

Retail Food Good [RFG.AU]: Drops over 35% after reporting H1 impairment losses and declining to provide FY outlook

(AU) Australia Jan Building Approvals M/M: 17.1% v 5.0%e; Y/Y +12.0% v -0.6%e

(AU) Australia Q4 Company Operating Profit Q/Q: 2.2% v 1.5%e; Inventories Q/Q: 0.2% v 0.5%e

(NZ) New Zealand Treasury: Expects jobless rate to be broadly flat in 2018; evaluating several ways to estimate natural rate of unemployment

China/Hong Kong

Shanghai Composite opened flat, Hang Seng -0.2%

Hang Seng Telecom Index -1.8%, Financials -1.2%, Services -1.1%

Shanghai Composite Property Index rises over 1%, then pares some of gain

China Mobile [941.HK]: Declines over 2% as China announced plans to cut mobile internet rates and cancel mobile internet roaming fees.

(CN) China Feb Caixin PMI Services: 54.2 v 54.3e (first m/m decline since Sept); Composite: 53.3 v 53.7 prior

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3431 V 6.3334 PRIOR

(CN) China PBoC Open Market Operation (OMO): Skips v CNY90B injected combined in 7-day, 28-day and 63-day reverse repos prior: Net drain CNY100B v CNY20B drain prior

(CN) China sets 2018 GDP growth target around 6.5% v 6.9% growth rate in 2017 (as speculated); to maintain 'prudent and neutral' monetary policy and 'proactive' fiscal policy in 2018 – Xinhua

(CN) China commented on fiscal policy measures for 2018: To adjust minimum wage reasonably; To reduce tax in manufacturing and transportation industries; To cut taxes for enterprises and individuals by CNY800B; To cap end of 2018 outstanding sovereign bonds at CNY15.7T.

(CN) China commented on plans for property market in 2018: To push forward property tax legislation.

(CN) China comments on trade policy for 2018: Expects trade to show good trend amid stable development; To lower import tariffs on vehicles and consumer goods

Japan

Nikkei225 opened -0.6%; closed: -0.7%

TOPIX Iron & Steel Index -2.2%, Real Estate -2.1%, Electric Appliances -1.8%, Securities -1.6%

Japan mega-banks trade broadly lower

Steel and Auto Manufacturers extend losses amid trade protectionism concerns

Nikkei weighted Fast Retailing gains over 1% after reporting Feb domestic SSS +5.1% y/y

Japan Feb Services PMI: 51.7 v 51.9 prior; Composite: 52.2v 52.8 prior

Bank of Japan (BoJ) Dep Gov Nominee Wakatabe: Expects continued monetary easing to push up real wages; notes inflation is distant from 2% target and that Japan not fully out of deflation

BoJ Dep Gov Nominee Amamiya: Domestic economy making steady progress toward hitting BoJ's price goal; financial conditions have maintained stability

Looking Ahead: BoJ Gov Kuroda Upper House confirmation hearings set for Tuesday March 6th; The confirmation hearings for the Dep Gov Nominees (Amamiya and Wakatabe) set for March 7th

Korea

Kospi opens +0.2%

South Korea Finance Min: Reiterates not appropriate for government to intervene into Bank of Korea (BoK) interest rate decisions

In related news, Bank of Korea (BoK) Gov Lee-Ju-yeol is said to be reappointed for another term as central bank gov, according to a report released on Friday, March 2nd; If Lee is reappointed it would be the first time since the 1970s that a BoK governor was appointed to a 2nd term.

South Korea Special Envoy Chung: To deliver President Moon's strong will for denuclearization to North Korea [**Note: South Korea's President Moon is expected to send a special envoy to North Korea 'soon', said a local press report from March 1st]

South Korea sells 3-year government bond: avg yield 2.34% v 2.275% prior

Other Asia

(HK) Hong Kong Feb PMI: 51.7 v 51.1 prior

(IN) India Feb PMI Services: 47.8 v 51.7 prior (1st contraction in 3 months)

(SG) Singapore Feb PMI: 55.3 v 53.6 prior

North America

XL Group [XL]: Reportedly Axa is in late stage talks to acquire XL Group – press

Qualcomm [QCOM]: US Dept of Treasury CFIUS issues interim order to the company to postpone its March 6th annual stock holders meeting and postpone election of directors by 30 days

Looking Ahead: OPEC reportedly schedules meeting with US shale producers in Houston on Monday, March 5th - press

Europe

(IT) Italy Berlusconi led Centre-Right bloc seen leading 5-star in the Italian elections; suggests hung parliament (in line with final poll ahead of the elections from Feb 16th); Support rises for 5-Star party - exit poll

(EU) EC Pres Juncker: we are preparing import duties on US products; Confirms preparing import duties on Levi's jeans, Harley Davidson motorcycles, and bourbon

UAE Oil Min Al Mazrouei: No talks yet about extending OPEC production cut into 2019

Levels as of 01:00ET

Hang Seng -1.4%; Shanghai Composite -0.2%; Kospi -0.9%

Equity Futures: S&P500 -0.6%; Nasdaq 100 -0.5%, Dax -0.6%; FTSE100 -0.6%%

EUR 1.2299-1.2365; JPY 105.41-105.69; AUD 0.7740-0.7776 ; NZD 0.7206-0.7251

Feb Gold +0.3% at $1,327/oz; Feb Crude Oil +0.4% at $61.48/brl; Mar Copper -0.2% at $3.127/lb

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3763; (P) 1.3789; (R1) 1.3824; More....

Intraday bias in GBP/USD remains neutral for consolidation above 1.3711 temporary low. Near term outlook is still mildly bearish with 1.4144 resistance intact. Correction from 1.4345 would extend to 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9333; (P) 0.9378; (R1) 0.9419; More...

At this point, USD/CHF is still staying above 0.9321 support and intraday bias remains neutral first. On the downside, On the downside, break of 0.9321 will indicate completion of the rebound from 0.9186. Intraday bias will be turned back to the downside for 0.9186 first. Break will resume larger down trend to 0.9115 projection level. On the upside, break of 0.9490 will revive the case of near term reversal, on bullish convergence condition in 4 hour MACD. In that case, outlook will be turned bullish.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

Daily Wave Analysis: EUR/USD Awaits Bearish Pullback And Bullish Bounce At 1.2250

EURUSD

The EUR/USD bullish breakout above resistance (orange/red) could restart the old uptrend whereas a bearish break below support makes a wave 4 (pink) less likely and a downtrend more probable.

The EUR/USD seems to have completed 5 bullish waves (blue) which could be a wave 1 (purple). The alternative is a wave A-B rather than 1-2. Price cannot break below the 100% Fib level otherwise it would invalidate the wave 2.

GBPUSD

The GBP/USD is testing the support at the 61.8% Fibonacci level, which is a new bounce or break spot.A bearish break and close below 1.37 and the support line (blue)makes the wave 4 (green) pattern less likely.

The GBP/USD could be in a wave 4 (blue), unless price breaks above the bottom of the wave 1 (red line).

USDJPY

The USD/JPY made a new lower low as part of a wave 5 (blue) pattern and has now reached a key support at the 105 round level.

On the lower 1 hour time frame, the USD/JPY could be building a bullish wave 4 (green) correction, which could indicate the potential for one more bearish wave 5 (green).

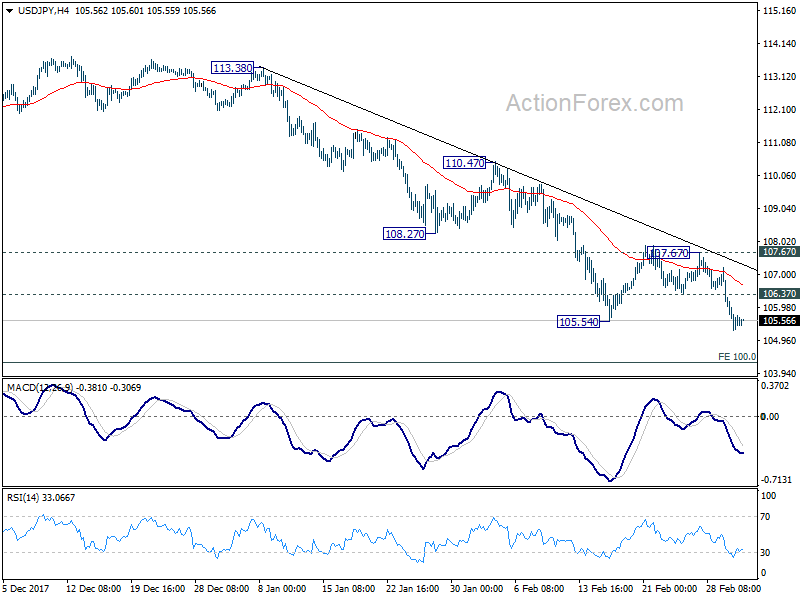

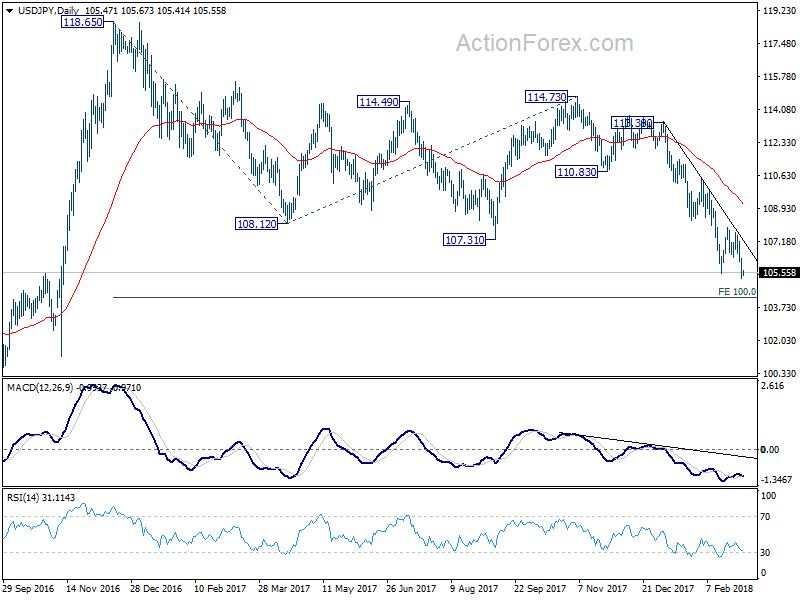

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.20; (P) 105.75; (R1) 106.25; More...

Intraday bias in USD/JPY remains on the downside for the moment. Down trend from 118.65 has just resumed and should target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Markets Stay Defensive as Trump Steps Up His Words on Trade Wars

The forex markets are pretty steady in Asian session as an extremely busy week starts. Reactions to Italy election and Germany SPD vote on grand coalition were muted. Euro remains steady so far, staying as the second strongest major currency for the month after Yen. Canadian Dollar and Australian Dollar remain the weakest ones for the month. Asian stocks are weak, however, with Nikkei trading down -0.8%, HK HSI down -1.3% at the time of writing. Investors are cautious and US President Trump continued to step up his words on trade wars.

Trump: EU has been brutal to us

Trump counter-attacked on EU's criticism on his steel and aluminum tariff. He tweeted again during the weekend that the European Union has been "brutal to us". And he warned that "if the E.U. wants to further increase their already massive tariffs and barriers on U.S. companies doing business there, we will simply apply a Tax on their Cars which freely pour into the U.S."

That was in reaction to European Commission President Jean-Claude Juncker's statement that "we will not sit idly while our industry is hit with unfair measures that put thousands of European jobs at risk.

Trump's advisor Navarro: Tariffs exemption possible, but no exclusion

White House Director of the National Trade Council, Peter Navarro commented on Trumps' tariffs on Sunday: He said exemptions and exclusions are different. And, "there'll be an exemption procedure for particular cases where you need to have exemptions so that business can move forward." However, "at this point in time, there'll be no country exclusions." Navarro added that "As soon as he (Trump) starts exempting countries, he has to raise the tariff on everybody else." And, "as soon as he exempts one country, his phone starts ringing with the heads of state of other countries."

Trump is expected to formally sign an order for the 25% tariff on steel and 10% on aluminum this week, or next week latest.

No clear winner in Italy election

In Italy, based on the early vote counts, there will be no clear winner in the election. Center-right coalition of former Primer Minister Silvio Berlusconi is heading for a win in the election, but falls short of a majority. That means, it will take weeks of negotiations before a government could be formed. Anti-establishment Five Star movements to come in second place. Center-left coalition by the governing Democratic Party will come in third.

SPD approved grand coalition, Merkel secured fourth term

Angela Merkel secured her fourth term as Chancellor of Germany. Members of the Social Democrats voted for the coalition deal with Merkels' CDU/CSU. Months of political uncertainty has now ended. The SPD's vote results were overwhelming, with 66% supporting, and only 34% rejecting.

On the data front

China Caixin PMI services dropped 0.5 to 54.2 in February. Australia TD securities inflation dropped -0.1% mom in February. Australia building approvals rose 17.1% mom in January. Main focuses in European session is on UK PMI services. Eurozone will also release Sentix investor confidence, retail sales and PMI services revisions. Later in the day, US will release ISM non-manufacturing composite.

The week ahead

For the week ahead, RBA, BOC, ECB and BoJ would have monetary policy meetings, scheduled on Tuesday, Wednesday and Thursday, Friday respectively. RBA is widely expected to keep interest rate unchanged at 0.50%. Governor Philip Lowe and other policymakers have been clear in their neutral stance. RBA is not going to follow other global central banks for tightening. NAB recently adjusted their expectation to just one RBA hike this year, not two. Westpac maintained their forecast that RBA will be on hold throughout this year.

For BOC, the biggest uncertainty on the economic outlook is undoubtedly future trade relations with the US, in particulate NAFTA negotiations. Also, it should be noted again that Canada is the biggest steel importer to the US. And the newly to be imposed tariff could give the country's economy another blow. BoC is not expected to hike again until the picture becomes clear.

As such, the central bank would be cautious over rate hike decisions. ECB would also maintain its rates and QE program unchanged. However, the focus is the timing for changing the forward guidance. The language in the accompanying statement and President Mario Draghi's comments at the press conference would be closely watched. For now, it's expected that ECB officials will discuss tweaking the languages, but hold it for June meeting. So Euro bulls could be disappointed out of the meeting.

On the dataflow, the focus is on US employment report due Friday. Non-farm payrolls probably increased 205K in February, up modestly from January's 200K. The unemployment rate probably slid -0.1 percentage point to a new low of 4%. Average hourly earnings might have grown 0.2% m/m in February, easing from 0.3% in the prior month. Scheduled for release on the same day is Canada's employment situation. The number of employment probably increased 21K in February, after contracting -88K a month ago. The unemployment rate might have stayed unchanged at 5.9%.

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.20; (P) 105.75; (R1) 106.25; More...

Intraday bias in USD/JPY remains on the downside for the moment. Down trend from 118.65 has just resumed and should target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will target 98.97 key support level. On the upside, above 106.37 minor resistance will turn bias neutral first. But outlook will remain bearish as long as 107.67 resistance holds.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | TD Securities Inflation M/M Feb | -0.10% | 0.30% | ||

| 0:30 | AUD | Building Approvals M/M Jan | 17.10% | 5.00% | -20.00% | -20.60% |

| 1:45 | CNY | Caixin PMI Services Feb | 54.2 | 54.3 | 54.7 | |

| 8:45 | EUR | Italy Services PMI Feb | 57 | 57.7 | ||

| 8:50 | EUR | France Services PMI Feb F | 57.9 | 57.9 | ||

| 8:55 | EUR | Germany Services PMI Feb F | 55.3 | 55.3 | ||

| 9:00 | EUR | Eurozone Services PMI Feb F | 56.7 | 56.7 | ||

| 9:30 | GBP | Services PMI Feb | 53.3 | 53 | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Mar | 30.9 | 31.9 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | -0.10% | -1.10% | ||

| 14:45 | USD | US Services PMI Feb F | 55.9 | 55.9 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Feb | 59 | 59.9 |

Australia’s Services Sector Growth Cooled In February

For the 24 hours to 23:00 GMT, the AUD marginally declined against the USD and closed at 0.7754 on Friday.

LME Copper prices rose 0.5% or $31.0/MT to $6883.0/MT. Aluminium prices rose 0.1% or $1.0/MT to $2144.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7751, with the AUD trading slightly lower against the USD from Friday’s close, after overnight data indicated that Australia’s AiG performance of services index eased to a level of 54.0 in February. In the prior month, the index had recorded a reading of 54.9.

On the contrary, the nation’s seasonally adjusted building approvals climbed 17.1% on a monthly basis in January, exceeding market expectations for a rise of 5.0%. In the previous month, building approvals had dropped by a revised 20.6%.

Elsewhere in China, Australia’s largest trading partner, the Caixin/Markit services PMI fell more-than-expected to a level of 54.2 in February, after recording a nearly 6-year high level of 54.7 in the prior month. Markets were expecting the PMI to drop to a level of 54.3.

The pair is expected to find support at 0.7735, and a fall through could take it to the next support level of 0.7720. The pair is expected to find its first resistance at 0.7769, and a rise through could take it to the next resistance level of 0.7788.

Moving ahead, investors would closely monitor the Reserve Bank of Australia’s interest rate decision, due tomorrow.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

German Retail Sales Surprisingly Dipped In January

For the 24 hours to 23:00 GMT, the EUR rose 0.43% against the USD and closed at 1.2329 on Friday.

In economic news, data showed that the Euro-zone’s producer price index (PPI) climbed less-than-anticipated by 1.5% on an annual basis in January, compared to an advance of 2.2% in the previous month, while markets were anticipating the PPI to increase 1.6%.

Separately, Germany’s retail sales registered an unexpected drop of 0.7% on a monthly basis in January, confounding market expectations for a gain of 0.7% and dampening hopes that private consumption will propel growth in Euro-bloc’s largest economy this year. In the previous month, retail sales had registered a revised drop of 1.1%.

The greenback declined against a basket of major currencies on Friday, pressured by continuous fears over trade wars following the US President, Donald Trump’s proposal to impose hefty tariffs on steel and aluminium imports.

On the macro front, the US final Reuters/Michigan consumer sentiment index climbed less than initially estimated to a level of 99.7 in February, compared to a preliminary print indicating a rise to a level of 99.9. In the previous month, the index had recorded a level of 95.7.

In the Asian session, at GMT0400, the pair is trading at 1.2325, with the EUR trading a tad lower against the USD from Friday’s close.

The pair is expected to find support at 1.2263, and a fall through could take it to the next support level of 1.2201. The pair is expected to find its first resistance at 1.2376, and a rise through could take it to the next resistance level of 1.2427.

Moving forward, traders would focus on the final Markit services PMIs for February, slated to release across the Euro-zone in a few hours. Also, the Euro-zone’s Sentix investor confidence for March and retail sales data for January, will be on investors’ radar. Later in the day, the US ISM non-manufacturing and the final Markit services PMIs for February, will be keenly eyed by market participants.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.