Sample Category Title

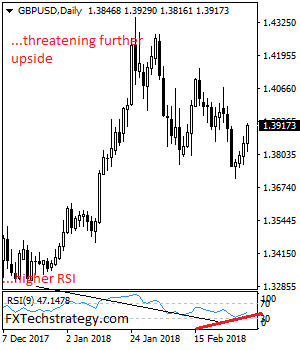

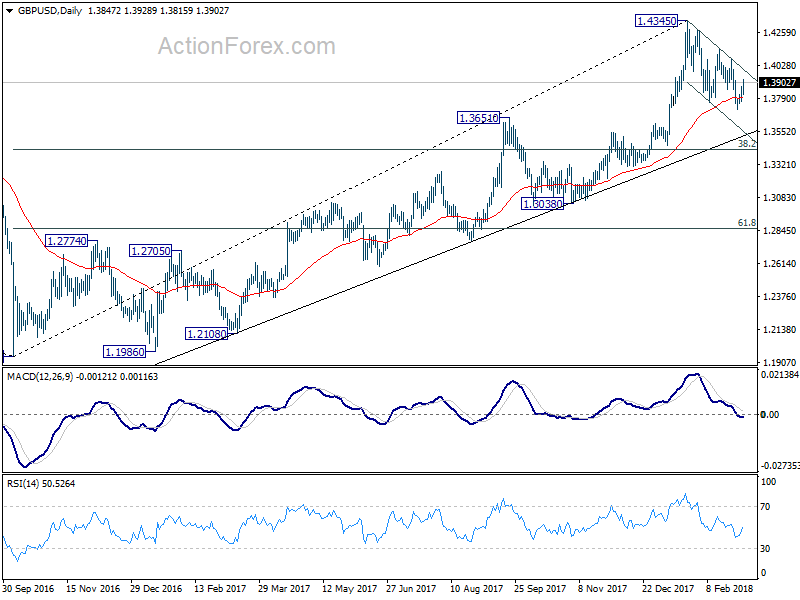

GBPUSD: Retains Its Upside Offensive

GBPUSD: The pair extended its upside pressure on Tuesday leaving risk of more strength on the cards. Support lies at the 1.3850 level where a break will turn attention to the 1.3800 level. Further down, support lies at the 1.3700 level. Below here will set the stage for more weakness towards the 1.3650 level. Conversely, resistance stands at the 1.3950 levels with a turn above here allowing more strength to build up towards the 1.4000 level. Further out, resistance resides at the 1.4050 level followed by the 1.4100 level. On the whole, GBPUSD looks to correct further higher.

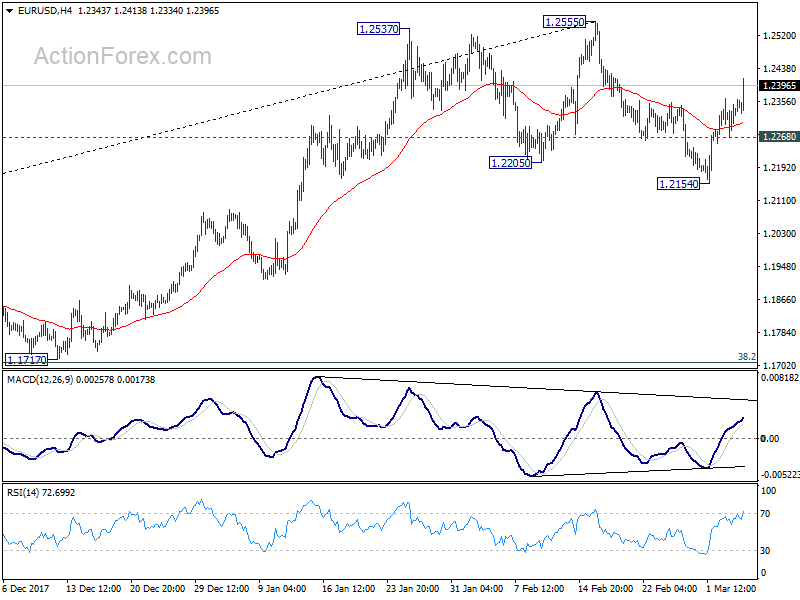

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2281; (P) 1.2323 (R1) 1.2376; More....

EUR/USD's rebound resumed and intraday bias is back on the upside. Further rally should be seen to 1.2555 high. The corrective structure of the fall from 1.2555 to 1.2154 argues that larger rally is not finished. More importantly, firm break of 1.2555 and 1.2516 long term fibonacci level will carry larger bullish implications. On the downside, below 1.2268 minor support will turn bias back to the downside for 1.2154 instead.

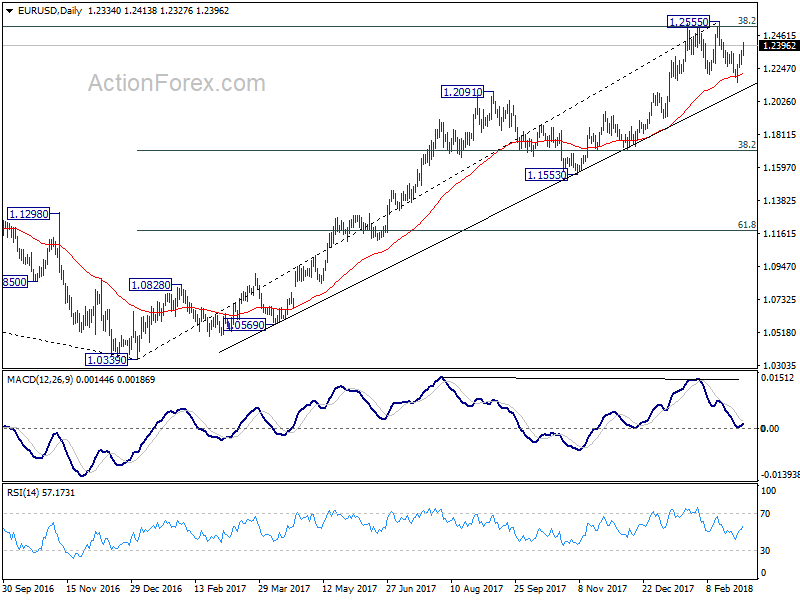

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

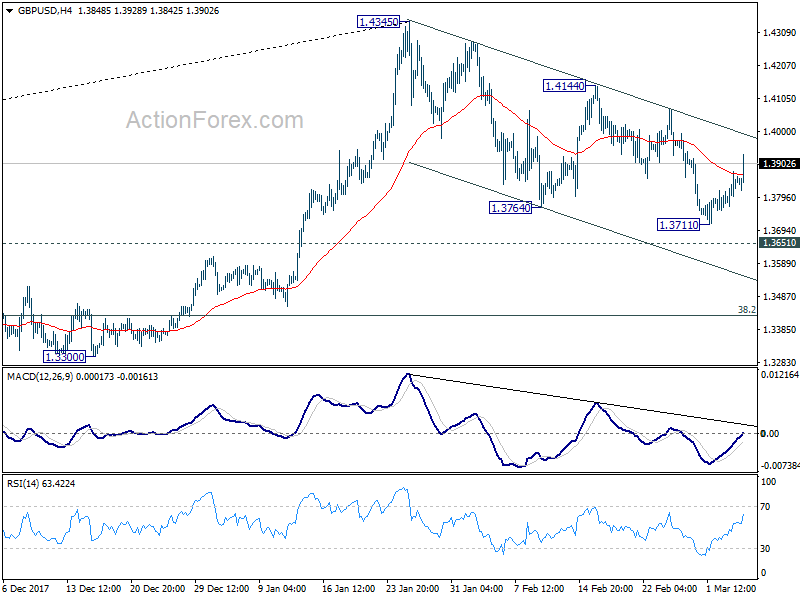

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3763; (P) 1.3789; (R1) 1.3824; More....

GBP/USD rebounds further today but still it's staying well below 1.4144 resistance. Intraday bias remains neutral, with mild bearish near term outlook. Correction from 1.4345 would extend and break of 1.3711 will target 1.3651 resistance turned support and below. At this point, such fall is viewed as a corrective move. Hence, we'll look for strong support from 38.2% retracement of 1.1946 to 1.4345 at 1.3429 to contain downside and bring rebound.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

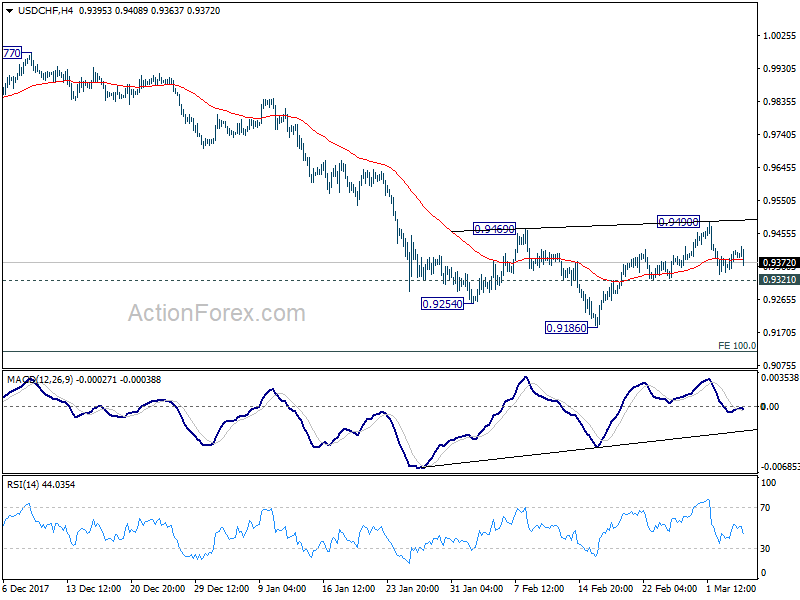

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9357; (P) 0.9382; (R1) 0.9423; More...

Intraday bias in USD/CHF remains neutral at this point. On the downside, break of 0.9321 will indicate completion of the rebound from 0.9186. Intraday bias will be turned back to the downside for 0.9186 first. Break will resume larger down trend to 0.9115 projection level. On the upside, break of 0.9490 will revive the case of near term reversal, on bullish convergence condition in 4 hour MACD. In that case, outlook will be turned bullish.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

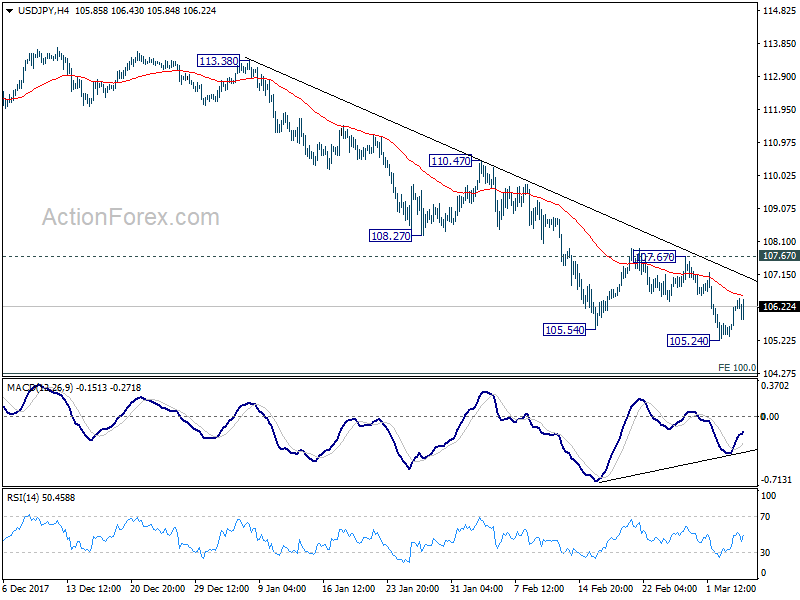

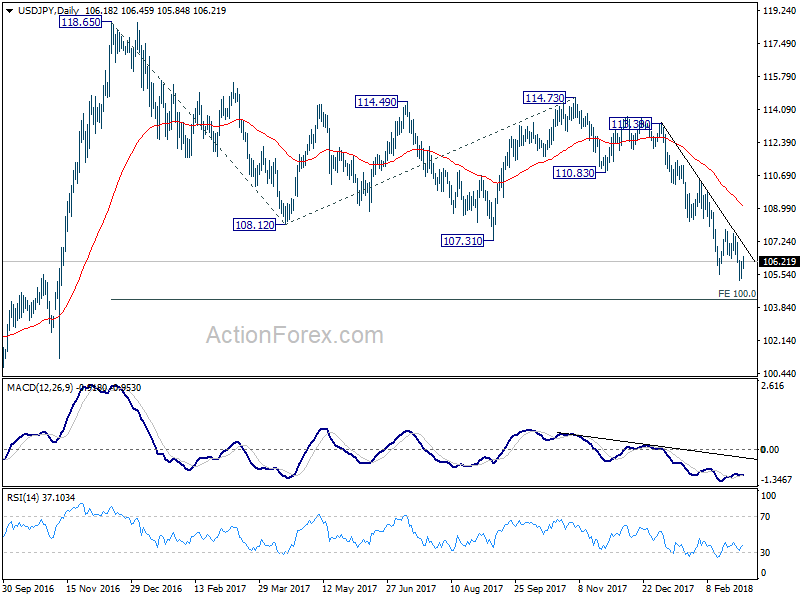

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 105.61; (P) 105.92; (R1) 106.50; More...

Intraday bias in USD/JPY remains neutral as consolidation from 105.24 temporary low continues. As long as 107.67 resistance holds, near term outlook will remain bearish. Break of 105.24 will resume larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Firm break there will pave the way to 98.97 key support level and below. However, break of 107.67 will indicate short term bottoming, on bullish convergence condition in 4 hour MACD. In such case, stronger rebound would be seen back to 55 day EMA (now at 109.05) first.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Canadian Dollar Rebounds, Ivey PMI Next

The Canadian dollar has edged lower on Tuesday. Currently, USD/CAD is trading at 1.2870, down 0.73% on the day. On the release front, there are no major US indicators. Canada will release Ivey PMI. On Wednesday, the US releases ADP nonfarm payrolls. Canada publishes trade balance and the Bank of Canada will set the benchmark rate.

The Canadian government is seeing red after President Trump has threatened to impose stiff tariffs on Canadian steel imports. Canada is the top exporter of steel to the US, accounting for some 16% of US steel imports. The “tariff tussle” could prove to be a major irritant in US-Canada relations, and has weakened the Canadian dollar, as USD/CAD broke above the 1.30 line on Monday, for the first time since late June. Trump is facing strong opposition to the move from Republican lawmakers, and has held our a carrot to Mexico and Canada – if a new NAFTA deal is reached, both countries would be exempted from the tariffs. Canada’s steel industry is a crucial backbone of the economy, and if the US does slap on the tariffs, it could ignite a trade war with Canada and other US trading partners.

Canada’s economy slowed down in January, as GDP posted a weak gain of 0.1%, matching the estimate. On an annualized basis, growth in the fourth quarter was 1.7%, considerably lower than the Bank of Canada’s most recent projection of 2.5%. With the Fed expected to raise rates up to four times in 2018, the BoC will be pressed to match rate hikes with its southern neighbor, or risk having the Canadian currency head lower. Currently, the BoC is projecting only two rate hikes in 2018. Strong growth has propelled the BoC to raise rates three times since July, but there are some factors weighing against a rate hike before May. First, fourth quarter expansion may fall short of the BoC’s forecast of 2.5%. As well, the future of NAFTA remains unclear, as negotiations between Canada, Mexico and the US have floundered. If the US decides to pull out of NAFTA, the repercussions on the Canadian economy could be significant, and the BoC will have to delay any plans to raise rates.

Dollar Climbs as North Korea Considers Denuclearization; European Stocks Rise Further

Here are the latest developments in global markets:

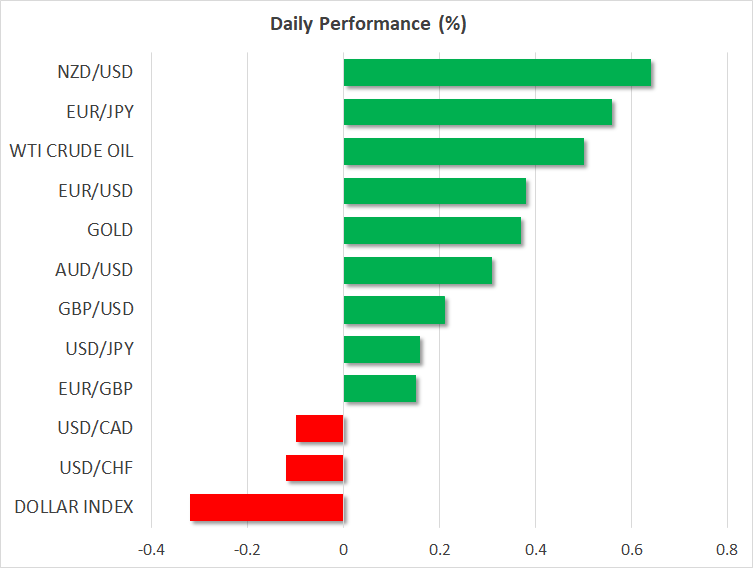

FOREX: Dollar/yen rallied significantly towards 106.34 (+0.13%) during early European afternoon, reversing earlier losses on news that North Korea was willing to begin negotiations with the US and abandon its nuclear program if regime’s safety is guaranteed according to South Korean officials. Sources also stated that the South and North Korean leaders will meet for a summit at the end of April along the border. The dollar index, though, dived to 89.72 (-0.45%) as other major currencies strengthened as well. Euro/dollar surged to 1.2396 (+0.59%) despite the EU’s threats to impose tariffs on US products in response to Trump’s trade protection measures announced on Friday. Investors, though, were less worried about a trade war after calls by US officials to reconsider the import restrictions. Political uncertainties in Italy were also somewhat offset by Germany’s successful efforts to reach a grand coalition agreement, providing some support to the common currency. Pound/dollar rallied to 1.3903 (+0.40%) ignoring comments by the French Finance Minister who said today that financial services “cannot be in a free trade agreement after Brexit”. Aussie/dollar and Kiwi/dollar spiked higher to 0.7818 (+0.70%) and 0.7286 (+0.89%) respectively, while dollar/loonie tumbled to 1.2926 (-0.25%).

STOCKS: European stocks gained positive momentum on Tuesday as the focus turned back to the corporate news. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.77% and 0.60% respectively at 1100 GMT with telecommunications and utilities driving the markets. The German DAX 30 climbed by 1.11% as auto stocks rebounded, the French CAC 40 jumped by 0.40%, while the Italian FTSE MIB was the biggest winner, surging by 1.43%, above six-month lows hit yesterday. This came after news that activist investor Elliott Management is building a stake in Italian telecom operator Telecom Italia to counter how its largest investor Vivendi SA runs the company. The UK’s FTSE 100 rose by 0.95%. US stock futures were in the green.

COMMODITIES: Oil prices retained earlier gains, with WTI crude and Brent last trading at $62.86 (+0.46%) and $65.73 (+0.29%) per barrel respectively. Yesterday the International Energy Agency revised its growth prospects on global oil demand upwards but warned that OPEC’S market share could weaken in the face of rising production in the US. In precious metals, gold was recovering yesterday’s losses, last seen at 1325.22 (+0.41%).

Day ahead: Trump’s trade strategy under speculation; Australia’s Q4 GDP growth pending in the Asian session

Day ahead: Trump’s trade strategy under speculation; Australia’s Q4 GDP growth pending in the Asian session

Looking forward to the day, there will be few economic releases to drive the markets, while trade headlines will continue to attract interest although concerns of a potential trade war have somewhat eased today.

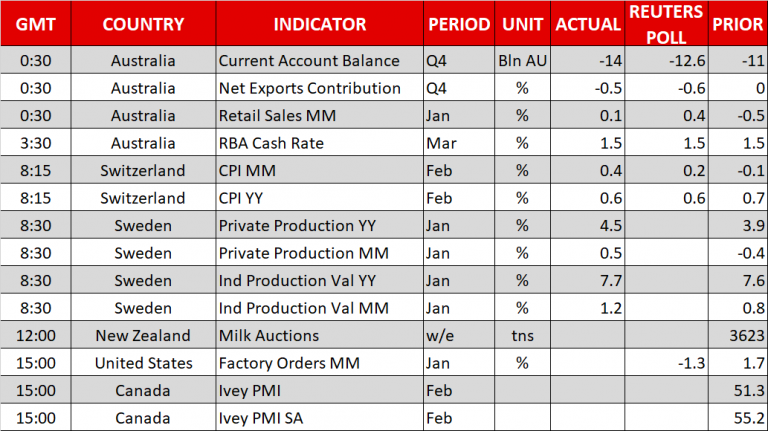

At 1500 GMT, the US will report readings on factory orders for the month of January, with analysts anticipating the number of purchase orders placed by manufacturers to decline for the first time in five months, falling by 1.3% on a monthly basis. This compares with a growth of 1.7% seen in December. At the same time, Canada will deliver February’s Ivey PMI which fell to the lowest level since June in January.

Milk auctions will be in focus in New Zealand as dairy products dominate the country’s exports. The release, though, is tentative, lacking a specific time, but most economic calendars have it marked for 1200 GMT.

Elsewhere, the EU will present its draft guidelines for a post-Brexit trade deal on Wednesday. However, the document is expected to be short of details since discussions on the issue have not developed substantially yet, probably forcing the UK Prime Minister to form her position on the trade front.

In energy markets, investors will be waiting for the API weekly oil report due at 2130 GMT.

Turning to today’s public appearances, the New York Fed President William Dudley (permanent voter) will be speaking at 1230 GMT ahead of the Bank of England’s chief economist and MPC member Andy Haldane, who will deliver remarks at 1800 GMT. The policymakers are not expected to comment on monetary policy directly but any reference to the topic is always a possibility from these highly-influential policymakers. Later in the day, the Governor of the Reserve Bank of Australia, Philip Lowe, will give a speech at the AFR Business Survey in Sydney at 2135 GMT, a few hours before Australia Statistics report GDP growth figures for the final quarter of 2017 early on Wednesday (0030 GMT).

Trump’s potential protectionism measures regarding aluminum and steel imports announced on Friday will continue to keep traders cautious but probably to a less extent following calls by the House Speaker Ryan Paul to reconsider the matter, while the House economic adviser Gary Cohn advised US companies dependent on the metal to meet the US President this week in an effort to prevent the order. However, the EU has already started preparing its position in response to Trump’s tariffs. According to Bloomberg news, the EU plans to impose bans on US brand imports including Harley Davidson motorcycles, jeans, and whiskey as well as agricultural and steel products.

Global Stocks Bounce Back… But for How Long?

It’s remarkable and somewhat alarming to see how the risk-off sentiment last Friday was swiftly replaced with a risk-on mood today, as fears eased over a looming global trade war.

Global stocks ventured higher during Tuesday’s trading session with Asian equities regaining ground, following Wall Street’s rebound overnight. European stocks were elevated by the renewed appetite for risk, and this positive momentum has the ability to support Wall Street this afternoon. There is a suspicion that the mounting pressure Trump is facing from political allies to reconsider the steep tariffs, has somewhat supported risk sentiment. With Trump also signaling that the tariffs on steel and aluminum would be scrapped if the U.S negotiates a “new & fair” NAFTA agreement, investors may be prompted to re-evaluate the chances of a global trade war. While the current market relief could push stocks higher, upside gains are likely to face headwinds in the form of uncertainty.

Currency spotlight – GBPUSD

The Pound received a boost on Monday, thanks to market optimism over the United Kingdom potentially securing a transitional deal with the European Union.

Although Sterling extended gains on Tuesday, many feel this had nothing to do with a change of sentiment towards the currency but rather Dollar weakness. With the Pound still gripped by the ongoing Brexit uncertainty, further losses remain on the cards. Technical traders will continue to closely observe how the currency reacts around the 1.3850 level. Sustained weakness below 1.3850 could encourage a decline lower towards 1.3750. Alternatively, a breakout and daily close above 1.3850 may invite an incline higher towards 1.3920 and 1.4000, respectively.

Commodity spotlight – Gold

Commodity spotlight – Gold

It is interesting how Gold prices appreciated during Tuesday’s trading session, despite stock markets across the globe rebounding.

While Dollar weakness could have played a small role in Gold’s appreciation, market uncertainty over a potential global trade war remains the driving factor. Although the yellow metal has scope to venture higher, investors must not overlook U.S interest hike expectations which could limit upside gains. Taking a look at the technical picture, prices remain pressured below the $1324.15 level. A failure for bulls to break above this level could encourage a decline back towards $1310 and $1300, respectively. A scenario where bulls conquer $1324.15 could result in an incline back towards $1340.

USDJPY Intraday Bullish Above 106.00 Level

The U.S dollar has moved sharply higher against the Japanese yen during the European trading session, hitting 106.40, as risk-on sentiment returns to financial markets. The USDJPY pair has quickly recovered upside momentum, following news that North Korea is willing to enter discussions on denuclearization with the United States. Moving into Tuesday’s U.S session, traders look towards the release of U.S Factory orders and today’s strong decline below the 90.00 level in the U.S dollar index.

The USDJPY pair is intraday bullish above the 106.00 level, further gains towards the 106.81 and 107.19 levels appear likely.

Should the USDJPY pair move above the 106.00 level, a deeper decline towards the 105.50 and 105.22 support levels seems possible.

EURUSD Buyers Take Control Above 1.2364 Level

The euro has moved to the highest trading levels of the week against the U.S dollar, hitting 1.2380, as financial markets look past U.S Tariff fears and the recent Italian election result. The EURUSD has broken above the key 1.2364 resistance level, as investors speculate that President Trump will not impose Trade Tariffs on the European Union. Moving into the U.S trading session, investors await the release of U.S Factory Orders and any new comments from President Trump that effect the U.S dollar index.

The EURUSD is strongly bullish above the 1.2364 level, with buyers pushing towards the key 1.2430 and 1.2550 resistance levels.

If the EURUSD now moves back below the 1.2364 level, sellers may push the pair back towards the 1.2305 and 1.2259 support levels.