Sample Category Title

USD/CAD Daily Outlook

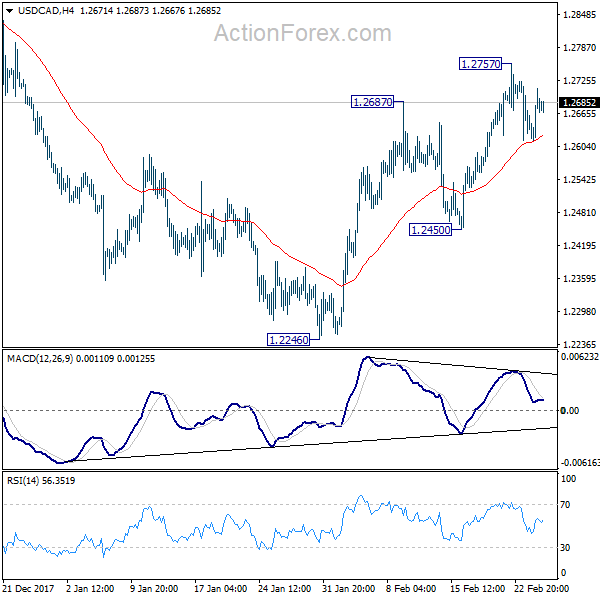

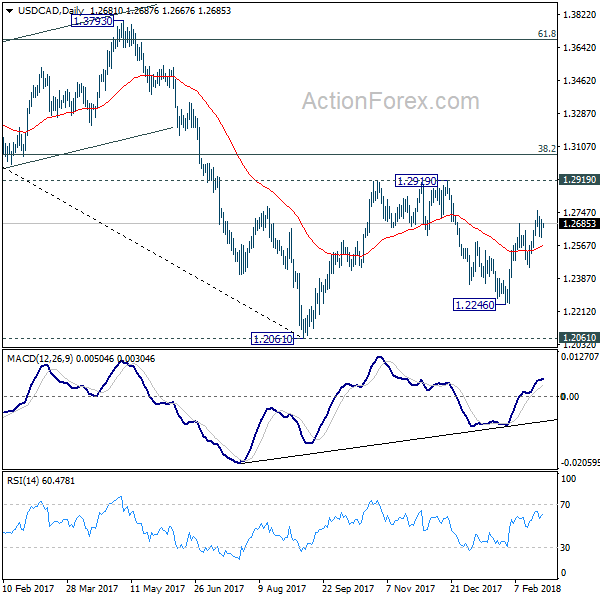

Daily Pivots: (S1) 1.2628; (P) 1.2670; (R1) 1.2725; More....

USD/CAD is staying in tight range below 1.2757 and intraday bias remains neutral first. On the upside, above 1.2757 will resume the rebound from 1.2246 and target a test on 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2450 will turn bias back to the downside for 1.2246 support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Stocks Heading Back to Record Highs as Sentiments Improved, Forex Mixed, Fed Powell Watched

Risk sentiments are generally positive this week so far. DOW gained 399.28 pts or 1.58% to close at 25709.27 overnight. The rebound from 23360.29 resumed with solid momentum and is set to extend to retest 26616.71 record high. Comparatively, NASADAQ was even strongly, up 11.15% to 7421.46, just inches below 7500.61 record high. Asian markets follow with Nikkei trading up over 300 pts, or 1.4%, at the time of writing. Pull back in treasury yields was a factor helping stocks as 10 year yield dipped -0.012 to 2.859 after recent rally lost momentum. The currency markets are mixed though, with major pairs and crosses stuck in range. Euro is mildly firmly against the others but there is no clear momentum.

Things to watch in Fed Powell's testimony

Fed Chair Jerome Powell's first Congressional testimony will be the major focus today. While Powell is not expected to deviate much from Fed's FOMC minutes and Monetary Policy Report last week, there are still a few points of interest to note. Firstly, the January FOMC meeting was held before the Congress passed the two year budget with USD 300b increase in federal outlays. Powell might offer his view on how the fiscal stimulus would give another boost to the economy.

Secondly, one of the key arguments of Fed doves against tightening is that after a few hikes, policy rate would be closer to neutral rates. And by then, policy will be restrictive. The markets would like to know Powell's view on where the neutral rate stands, and whether the neutral rate has moved up again after sustained recovery in the economy. Thirdly, there have been talks about so called price-level targeting in recent markets. The markets would like to know more about the discussion within Fed on this topic.

But after all, for now, the markets should be firmly expecting three Fed hikes this year. The question is on whether there will be a fourth hike. If Powell doesn't offer any clue, we'll have to wait for new economic projections to be published at the March FOMC meeting before having a conclusive expectation.

Fed Quarles offered upbeat outlook

Fed Governor Randal Quarles offered an optimistic view on the economic outlook of the US. He said that "Some of the factors that have been holding back growth in recent years could shift, moving the economy onto a higher growth trajectory." He also pointed to the tax cuts and said they "will also likely boost investment and increase the capital stock." He supported gradual removal of monetary policy accommodation. And he added that "this higher policy path would be motivated by sustained stronger growth and improved economic conditions, not a greater desire to slow the economy."

On the other hand, Fed dove St. Louis Fed President James Bullard warned again that "if the Committee raises the policy rate substantially from here without other changes in the data, the policy setting could become restrictive." And he's concerned that FOMC "goes too far too fast" in tightening.

ECB Draghi sounded cautious again

ECB President Mario Draghi sounded cautious again in his comments yesterday. He warned that "given the uncertainty surrounding the measurement of economic slack, the true amount may be larger than estimated, which could slow down the emergence of price pressures." And therefore, the "right blend" of stimulus measures is still needed.

Nonetheless, he said "these factors should wane as the economic expansion continues and unemployment further declines." "The relationship between growth and inflation remains largely intact, even if it has temporarily weakened in recent years to the extent that the speed of adjustment in inflation towards our aim has been affected." But he remained confident that " headline inflation will resume its gradual upward adjustment, supported by our monetary policy measures."

Draghi's comments suggested that ECB is still in no rush to exit stimulus. And the comments echoed the January meeting minutes that "changes in communication were generally seen to be premature at this juncture, as inflation developments remained subdued despite the robust pace of economic expansion." ECB is not even ready to change its forward guidance yet.

EU to publish draft Brexit treaty

The EU is set to publish 100-page draft Brexit treaty this Wednesday, detailing how it expects Brexit to happen and the terms of the transition period. That will come just two days before UK Prime Minister Theresa May's speech on future trade relationship with EU. It's believed the EU's document will be sole from EU's perspective for the negotiation ahead. Meanwhile, it draws criticism from UK that EU is only trying to push its agenda, rather than producing something that reflects the positions of both sides.

On the data front

New Zealand trade balance showed NZD -566m deficit in January. Eurozone M3 and confidence indicators will be released in European session. German CPI will also be featured. US will release trade balance, wholesale inventories, durable goods orders, house price indices and consumer confidence.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2628; (P) 1.2670; (R1) 1.2725; More....

USD/CAD is staying in tight range below 1.2757 and intraday bias remains neutral first. On the upside, above 1.2757 will resume the rebound from 1.2246 and target a test on 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2450 will turn bias back to the downside for 1.2246 support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Jan | -566M | -2710M | 640M | 596M |

| 9:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 4.60% | 4.60% | ||

| 10:00 | EUR | Eurozone Business Climate Indicator Feb | 1.47 | 1.54 | ||

| 10:00 | EUR | Eurozone Economic Confidence Feb | 114 | 114.7 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Feb | 8 | 8.8 | ||

| 10:00 | EUR | Eurozone Services Confidence Feb | 16.3 | 16.7 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | 0.1 | 0.1 | ||

| 13:00 | EUR | German CPI M/M Feb P | 0.50% | -0.70% | ||

| 13:00 | EUR | German CPI Y/Y Feb P | 1.50% | 1.60% | ||

| 13:30 | USD | Fed Powell's Congressional Testimony | ||||

| 13:30 | USD | Advance Goods Trade Balance Jan | -72.3B | -72.3B | ||

| 13:30 | USD | Wholesale Inventories M/M Jan P | 0.30% | 0.40% | ||

| 13:30 | USD | Durable Goods Orders Jan P | -2.50% | 2.80% | ||

| 14:00 | USD | House Price Index M/M Dec | 0.40% | 0.40% | ||

| 14:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Dec | 6.30% | 6.40% | ||

| 15:00 | USD | Consumer Confidence Index Feb | 126 | 125.4 |

AUD/USD Is Approaching A Crucial Break

Key Highlights

- The Aussie Dollar traded lower recently and moved below the 0.7900 support against the US Dollar.

- There is a crucial contracting triangle forming with support at 0.7805 on the 4-hours chart of EUR/USD.

- The Chicago Fed National Activity Index (CFNAI) declined to 0.12 in Jan 2018.

- Today, the US Durable Goods Orders for Jan 2018 will be released, which is forecasted to decline 2.2%.

AUDUSD Technical Analysis

The Aussie Dollar declined below the 0.7950 and 0.7900 support levels recently against the US Dollar. The AUD/USD pair tested the 0.7790 level and is currently trading in a range.

Looking at the 4-hours chart, it seems like the pair may make the next move. A push above the 0.7900-0.7910 resistance could take the pair towards 0.8000. On the other hand, a break below the 0.7800 support may initiate a fresh downside wave.

The chart points that there is a crucial contracting triangle forming with support at 0.7805. On the upside, the triangle resistance is at 0.7910. Therefore, the 0.7800 and 0.7900 are breakout levels.

The 0.7910 level is significant since it is near the 50% Fib retracement level of the last decline from the 0.7988 high to 0.7790 low. A successful close above the 0.7900 and 0.7910 levels could kick start a fresh rally in AUD/USD in the near term.

Recently in the US, the Chicago Fed National Activity Index (CFNAI) for Jan 2018 was released by Federal Reserve Bank of Chicago. The market was looking the index to rise to 0.15.

The actual result was a bit lower as there was a decline in the index to 0.12 from 0.14. However, there was no negative impact on the US Dollar.

Major pairs such as EUR/USD and GBP/USD traded lower and are currently in a bearish zone. On the other hand, USD/JPY is moving higher towards a major resistance area near 107.10-20.

Economic Releases to Watch Today

Euro Zone Services Sentiment Feb 2018 – Forecast 114.0, versus 114.7 previous.

German Consumer Price Index for Feb 2018 (Prelim) (YoY) – Forecast +1.5%, versus +1.6% previous.

German Consumer Price Index for Feb 2018 (Prelim) (MoM) – Forecast +0.5%, versus -0.7% previous.

US Durable Goods Orders for Jan 2018 – Forecast -2.2% versus +2.8% previous.

Market Morning Briefing: Dollar-Yen Saw A Low Of 106.38 Yesterday

STOCKS

Dow (25709.27,+1.58%) moved up breaking above 25500 and may eventually recover to levels near 26500 in the coming sessions. Near term looks bullish just now with a possibility of a test of previous highs near 26700.

Dax (12527.04, +0.35%) tested 12600 on the upside and if that holds, the index could fall back towards 12400 in the next few sessions. Near term could be bearish while below 12600. A break above 12600 if seen just now, could negate an immediate fall towards 12400 and instead take it higher towards 12800.

Nikkei (22460.85, +1.39%) rose in line with our expectation of a rise towards 22500. There is scope on the upside towards 23000 or aye even higher while support near 21000 holds on the weekly charts. Near to medium term looks bullish.

Shanghai (3295.65, -1.02%) came off from 3335 as expected and may come off towards 3275-3250 levels again in the coming sessions. While immediate resistance on the 3-day candles holds, near term looks bearish.

Nifty (10582.60, +0.87%) has risen from levels near 10400, the support as seen on the 3-day candles. While that holds, a near term rise towards 10800 looks likely in the medium term. Sensex (34445.75, +0.89%) also has similar support and may rise towards 35000 in the near to medium term.

COMMODITIES

WTI (63.87) and Brent (67.50) are almost stable and is likely to move up towards 65 and 68-69 respectively.

Gold (1335.40) looks poised and may rise towards 1360-1370 again in the coming sessions. Near term looks bullish.

Copper (3.2275) is likely to head towards 3.30, the medium term resistance from where another sharp rejection could be expected. Near term is bullish towards 3.30.

FOREX

Some immediate support might be provided to the Dollar Index (89.73) on the daily line chart by 13 days and 21 days moving average lines. Moreover, earlier resistance trend line on the daily line chart could also provide some support near 89.0-89.5. Our earlier projection of ranging between 88.5-90.0 for this week would be incorrect if the above mentioned supports hold.

Euro (1.2338) did see a high near 1.2355 yesterday but closed lower near 1.2317 and is currently trading around 1.233-1.234. Much like the Dollar index, the 21 days moving average line on the daily line chart could provide some resistance near 1.236 to the Euro’s upmove.

Dollar-Yen (106.93) saw a low of 106.38 yesterday, but, as mentioned yesterday, might have found some support near 106.25-106.5 on the 3 day line chart and the weekly candles. It might now test resistance near 107.25 on the daily candles again before dipping further.

The Euro-Yen (131.95), as expected, has bounced from support on daily candles near 131. If resistances for the Dollar Yen (near 107.25) and for Euro (near 1.236) hold (as mentioned above), then the Euro Yen’s upside could be restricted till 132.5-132.6.

As per expectation, Pound (1.3971) did test resistance on daily candles yesterday (at 1.407) and is now dipping towards support near 1.39, from where a bounce could be expected.

Dollar-Rupee (64.7950): Increased chances of fresh rally targeting 65.40.

INTEREST RATES

US 10 Year Yield (2.866), US 30 year Yield (3.1563), US 5 year yield (2.6082), US 2 year yield (2.2179) : Longer term US yields are consolidating around levels seen yesterday while the 2 Year yield has come further down from the 2.25-2.26 levels seen last week. The 10 Yr, 30 Yr and 5 Yr could see another upmove towards 2.9%, 3.2% and 2.65% in this week. US GDP data which would be released tomorrow could be important for how investors react. Decent GDP growth could see investors shift to stock markets, thereby leading to a rise in yields.

(Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

Spotlight On Powell

Spotlight on Powell

Outside of equity markets where the US stock indexes clocked in gains of 1 %, most asset classes remain parked in neutral as all eyes are on Jay Powell.

After yesterday's wave of broader USD weakness during the APAC session, led by USDJPY on the back of mushy US yields, the DXY ended nearly flat on the day, as pre-Humphrey Hawkins position adjustments dominated the NY session.

Investor focus also remains on China after the ruling party will pave the way for President Xi to extend his rule in office, with a proposal to remove the constitutional clause limiting presidents service to two five year terms. And also of significance, Chinese President Xi Jinping's top economic adviser, Liu He, will be visiting the US from Tuesday through Saturday

Removing Xi's term limits is a boon to regional economic sentiment as it guarantees continued market reforms and staying the course on the trade-and-infrastructure program called the Belt and Road Initiative.

Investors will be eying Liu He USA visit where the discussion will centre on Bilateral trade. It comes at a time when the trade tensions are broadening. Liu He is expected to be the next central bank chief so all eyes will be on these trade discussion. In the past high-level talks tackling their enormous trade imbalances produce few if any significant results so while discussion moves forward and the market hopes for some level of cooperation, it is worth preparing for the worst.

Equity Markets

S&P500 powered higher overnight and chalked up it's strongest close for the month as a positive uptrend is reemerging. Investor feel less threatened by US rate hikes as those that were on the road to 3 % US 10 Year yields have temporarily parked at the roadside rest stop.

Investors appear less concerned by US rate hikes than at any point this month, which is what is providing the positive tone in global equity markets

Oil Markets

The confluence of bullish signals has WTI moving above 64.00.But It's the dwindling Cushing inventories that continue to resonate with oil traders while another supply disruption in Libya has provided that extra fillip. Given last weeks Cushing collapse in oil stockpiles, traders are keenly awaiting this week's US inventories data. Keeping in mind, with oil prices trading in backwardation there is less incentive for oil producers to warehouse supply.

Gold Markets

Upbeat equity market and the DXY returning to this weeks opening levels have erased most of yesterday's market gains ( on a weaker USD) as the Gold hedge remains exceptionally correlated to the USD and a lesser degree to US equity markets.

But given the Fed has struggled to surpass their 2 % inflation target it's possible the Fed's could opt to run the economy hotter than expected by keeping interest rates lower for longer. If the market perceives any hint that the Fed will remain behind the curve, Gold could bounce considerably higher.

With that said, the market will trade very neutral ahead of Jay Powell's testimony,

Currency Markets

The Japanese Yen

USDJPY, as expected continues to be the go-to vehicle for G-10 traders. A bit of a topsy-turvy day yesterday as what seemed to be decent dollar demand into the 9:55 Tokyo Fix on the back of active equity markets and a dovish sounding Kuroda turned lower on huge volumes. While US yields were soggy, traders should be cognisant of exporter supply entering the picture for both month and year-end selling. Also, it looks like the market was caught a bit long and wrong at higher levels, and there was a bit of panicked rush for the exits.

Well, that's my view on yesterday, but for today I suspect it will be the case of wait and see. But even dollar bears like me after years dealing with arguably the most dovish sitting Fed Chair of all times; it might be worth positioning for a hawkish surprise after all Powell is highly unlikely to match Yellen on the dovish scale or is he?

The Australian Dollar

The Aussie dollar turned gangbusters yesterday as Iron ore futures in Asia rallied to a 10 month high on news that steel supply curbs in China could go beyond the winter season but have come off overnight highs as the market is prepping for Powell.

The Yuan

Predictably the RMB traders have embraced the Xi' news as the announcement removes any political uncertainty of Xi's successor, and provides a stable political scrim.But it also guarantees that deeper market reforms remain a priority as to does the Belt and Road initiative.

The Malaysian Ringgit

The Ringgit has been trading favourable due to some front.

Oil prices continue to move higher on collapsing US inventories.

Bond and equity inflows picked up as US yields fell and risk on returned to Global equity markets

The positive tone in yesterday local bond market suggests today auction will be fully subscribed and should provide a bounce to the MYR sentiment.

Removing presidential term limits in China not only provides political continuity in the region but guarantees the continuation of the Belt and Road initiative of which Malaysia will be a huge benefactor for decades to come

Gold Steady, Investors Await Powell Testimony To Congress

Gold has stated the week with slight gains. In Monday's North American session, the spot price for an ounce of gold is $1331.69, up 0.16% on the day. On the release front, New Home Sales dropped to 593 thousand, well off the estimate of 655 thousand. This marked the smallest gain since August. Traders should be prepared for a busier Tuesday. The US releases durable goods and consumer confidence reports. As well, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

Gold continues to show volatility. The base metal lost 1.5% last week, after climbing 2.2% a week earlier. Concerns that strong US numbers could stoke inflation and more rate hikes sparked the recent turbulence in global stock markets. This has triggered volatility in gold, as gold prices are sensitive to moves (or expected moves) in interest rates. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, the Fed could press the rate trigger four, or even five times in 2018. If the Fed does revise its rate hike projection upwards, gold prices would likely move downwards.

It hasn't been a smooth ride for Jerome Powell, who took over as chair of the Federal Reserve from Janet Yellen earlier this month. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation. Powell will be on center stage this week, when he makes separate appearances before the House of Representatives and the Senate. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

Pound Ticks Lower, Markets Eye Durable Goods, Powell Testimony

The British pound has posted slight losses in the Monday session. In North American trade, GBP/USD is trading at 1.3958, down 0.08% on the day. On the release front, there are no key British indicators. In the US, New Home Sales dropped to 593 thousand, well off the estimate of 655 thousand. This marked the smallest gain since August. Tuesday will be much busier, with the US releasing durable goods and consumer confidence reports. As well, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

It hasn't been a smooth ride for Jerome Powell, who took over as chair of the Federal Reserve from Janet Yellen earlier this month. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation. Powell will be on center stage this week, when he makes separate appearances before the House of Representatives and the Senate. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

Brexit negotiations have been bumpy from the start, but matters seem to be deteriorating almost daily. Prime Minister May is in a tough spot, with the Europeans dismissing her latest proposals on a trade deal after Brexit, and many members of her party supporting playing hard with Europe. May has proposed that a trade deal would allow some divergence with EU regulations in certain industries, but the Europeans have dismissed this as ‘cherry picking', which they say is a non-starter. May will lay out her post-Brexit vision of relations with the EU in a speech on Friday and if the Europeans pour cold water on her plan, the markets could react negatively.

British GDP for Q4 was a disappointment last week, but the pound has managed to hold its own against the dollar. GDP was revised downwards to 0.4%, down from 0.5% in the initial estimate. Looking at growth for all of 2017, GDP was revised lower from 1.8% to 1.7%, its worst showing since 2012. The weak readings are being attributed to lower production and weaker consumer spending. Consumers are being squeezed by a weaker British pound as well as high inflation, which is running at a 3% clip, compared to the BoE target of 2%.

USD/JPY – Japanese Yen Subdued Ahead Of Powell Testimony

The Japanese yen is almost unchanged in the Monday session. In North American trade, USD/JPY is trading at 106.84, down 0.03% on the day. On the release front, it’s a quiet start to the week. US New Home Sales dropped to 593 thousand, well off the estimate of 655 thousand. This marked the smallest gain since August. Tuesday will be much busier, with the US releasing durable goods and consumer confidence reports. As well, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

It hasn’t been a smooth ride for Jerome Powell, who took over as chair of the Federal Reserve from Janet Yellen earlier this month. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation. Powell will be on center stage this week, when he makes separate appearances before the House of Representatives and the Senate. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

Bank of Japan Governor Harohiko Kuroda was recently reward with a second 5-year term, and has lost no time in defending his monetary policy. Speaking in parliament on Monday, Kuroda said he had no plans to conduct a review as to why the Bank’s massive stimulus program had failed to raise inflation to the target of just under 2 percent. Kuroda said it was “unfortunate” that the target had not been met, but argued that the BoJ’s “powerful” monetary easing had eliminated deflation. Kuroda’s comments were another clear message that the BoJ will not be reducing its massive stimulus program anytime soon. The Japanese economy has rebounded, but inflation has not kept pace, with core consumer inflation climbing just 0.9% in January.

Looming Balance Of Payments Problem

The market is abuzz with talk about the twin US deficits but one part of the equation is overlooked. The euro was the top performer Monday while the Canadian dollar lagged. German CPI is next and Fed chair Powell will testify to the House Finance Committee in US trading at 10:00 ET (15:00 London/GMT) but the text of the Powell's speech is due for release at 8:30 ET 13:30 London/GMT. The Dow30 trade was stopped out, leaving 2 other indices in progress.

Here's the issue: The US economy is strong. Unemployment is near all-time lows, corporate profits are soaring, house prices are back at the highs, consumers are in good shape… and yet the government just delivered a gigantic tax cut, among the biggest ever.

What happens to that money? One argument is that it finds its way abroad.

Elaborating further: A US company wants to fill a large order. The US factory is running at capacity and management is unable to find good workers without overpaying, so they forego on filling the order. As a result, the buyer seeks an economy that's relatively slower, such an example is a factory in Mexico that's running at half capacity and eager to complete the order, willing to discount and can deliver ASAP.

That's an oversimplification but that might be what's beginning to happen. It's early but the US trade deficit has grown to $70B/month from $60B/month in two months. That's a big drag on growth. Other drawbacks include debt financing at higher rates, but getting into that would be dancing on thin ice.

Secondly -- and no one is talking about this – is that Trump's tax cut will exacerbate the US twin deficits, making them a larger problem than they already are --a political disaster and an acute economic imbalance.

The Republican brand is tied to fiscal discipline and Trump's brand is tied to balancing trade deficits. So markets haven't particularly cared about the twin deficits for a long time but Washington does care. Markets are increasingly worried about what's coming to solve those problems. Trump will want action on the fiscal deficit, while pressing for action on the trade deficit and on Monday he railed against the WTO so everything is on the table.

Given the ideology of Washington, we could be months away from a trade war and from some harsh cuts to US social spending. In the shorter term, the focus will be on German CPI and Powell's Humphrey Hawkins testimony on Tuesday.

EURGBP Rallies on Weaker Pound; Daily Cloud Twist also Attracts

The cross accelerated from 2 1/2 week low at 0.8771, posted earlier today and broke above 0.88 handle after highly-anticipated speech of opposition leader Jeremy Corbyn today. Corbyn explicitly supported customs union with EU after Brexit, despite Labour party also being split over Brexit case. Sterling was deflated after Corbyn's speech as opposition's view of Brexit further collides with strategy of British PM May. The EURGBP cross bounced from dangerous zone (the weakness earlier today cracked pivotal support at 0.8775 (Fibo 61.8% of 0.8686/0.8919 upleg), reducing immediate downside risk. Technical studies are bearish overall (daily MA's are in firm bearish setup/14-d momentum heads south, deeply in negative territory), but reversal of slow stochastic from oversold zone signals correction, with daily cloud twisting today (0.8854) and attracting rallies. Initial pivotal barrier lies at 0.8830 zone (Fibo 38.2% of 0.8919/0.8771 bear-leg/55SMA), guarding (100SMA/daily cloud top (0.8853) break of which would generate stronger bullish signal. However, daily cloud is widening after twist and may produce stronger pressure which would keep the downside vulnerable, while daily cloud limits recovery attempts.

Res: 0.8815; 0.8830; 0.8854; 0.8870

Sup: 0.8800; 0.8771; 0.8732; 0.8716