Sample Category Title

Sunset Market Commentary

Markets

Global core bond markets took a slow start to the trading week, eking out small gains in line with last week. US Treasuries slightly outperform Bunds. The Bund is close to 159.75 resistance (which corresponds with 0.62% in the 10y German yield), but a test didn't occur. The eco calendar couldn't inspire trading. St. Louis Fed Bullard kept his role as one of the most dovish members on the FOMC board. Inflation readings (EMU and US) and Fed chair Powell's testimony before Congress are keeping many investors sidelined. US yields decline by 1.2 bps (2-yr) to 2.7 bps (10-yr) at the time of writing. The German yield curve bull flattens with yields 0.1 bp (2-yr) to 2.2 bps (30-yr) lower. 10-yr yield spread changes versus Germany are nearly unchanged with Italy (-5 bps), Spain (-4 bps) and Portugal (-3 bps) outperforming. Next weekend's Italian election, which risks producing a political stalemate; doesn't seem to bother investors. The Kingdom of Belgium launched its debut green OLO via syndication. The 15-yr bond (€4.5bn Apr2033) was priced to yield MS -14 bps, compared to initial price takings in the MS -11 bps area. The green bond printed spot on the regular OLO-curve. Orderbooks closed above €12.7bn.

The dollar started the week on a soft footing in Asia and early in European dealings this morning. There was no high profile news to explain the move. A positive risk/equity sentiment coincided with USD weakness as was often the case of late. Interest rate differentials narrowed slightly against the dollar/in favor of the euro, but we doubt that this was a factor. Whatever, dollar softness eased/was reversed during the afternoon session, despite soft comments from Fed's Bullard. FX Markets are looking forward to tomorrow's hearing of Fed Chairman Powell on the Hill tomorrow. There are also plenty of (EMU and US) eco data later this week. Markets apparently don't want to be too much short dollar going into these events. USD/JPY rebounded back to the high 107 area., EUR/USD reversed this morning's gains and trades again in the low 1.23 area, awaiting the events to come.

Hawkish comments from BoE's Ramsden this weekend supported sterling early this morning. At the same time, the UK Labour Party had signaled that its leader would reveal his support for the UK to stay in a customs union with EU after Brexit. This was seen as putting pressure on UK PM May and raising chances on a softer Brexit. EUR/GBP dropped to the 0.8775 area. Jeremy Corbyn's speech was more or less as expected. The Labour leader said he doesn't want a new referendum on Brexit, but advocated that a customs union could serve the party's priority to get the best deal for jobs, living standards and the economy. The sterling rally stalled as the speech didn't bring any high profile news anymore. The reaction of pro-EMU conservative party members is still highly uncertain and so remains the overall UK roadmap to Brexit. EUR/GBP trades again near the 0.88 barrier. Cable hovers near 1.40.

News Headlines

Labour leader Corbyn in a speech on Monday backed a customs union with the EU after Britain leaves the EU next year, setting the stage for Labour lawmakers to join Conservative rebels in supporting the necessary amendments to trade legislation.

An era of low productivity growth and high world demand for safe assets may be anchoring appropriate central bank policy rates at a low level, St. Louis Fed Bullard said.

US, Mexican and Canadian negotiators seek to narrow disagreements on how to overhaul the NAFTA trade deal despite renewed signs of tension between Mexico and US President Trump over his planned border wall.

Gold Eases after Sharp Upward Move Earlier in the Day

Gold is heading south over the last couple of hours, while it started the day in green. In the 4-hour chart, the precious metal is developing within the 50.0% and 61.8% Fibonacci retracement levels of the downleg with the high of 1366 and the low of 1307. The price struggled within 1336 and 1343 after the aggressive jump towards 1340.90 during today's European session.

Gold is heading south over the last couple of hours, while it started the day in green. In the 4-hour chart, the precious metal is developing within the 50.0% and 61.8% Fibonacci retracement levels of the downleg with the high of 1366 and the low of 1307. The price struggled within 1336 and 1343 after the aggressive jump towards 1340.90 during today's European session.

In the near-term, the technical indicators suggest that negative movements are more likely to occur given that the RSI is sloping downwards in the positive zone, while stochastic is on track to post a bearish crossover in the overbought area above 80. Moreover, the price has slipped below the 40-simple moving average, suggesting further losses.

If the precious metal drops below the 50.0% Fibonacci mark of 1336, it could hit the 38.2% Fibonacci level of 1329, which holds near the 20-day SMA.

Conversely, upside moves are likely to find resistance around the 61.8% Fibonacci level of 1343. Moreover, a bullish rally could extend gains towards the 1361.40 resistance barrier.

Ruble, Sterling and Yuan Advance as Dollar Struggles ahead of Powell Testimony

The Dollar is under threat to losses once again, with the Greenback at time of writing currently trending lower against all of its G10 counterparts, with the exception of the Canadian Dollar. The Dollar is also weaker against many emerging market currencies, as investors take some Dollar exposure away from the table ahead of Fed Chair Jerome Powell's Congress testimony later in the week. The new Fed Chair is expected to be heavily quizzed on policy, with congress likely to be particularly interested in Powell's US interest rate outlook. If Powell suggests that the Federal Reserve could raise US interest rates four times in 2018, it could be seen as a positive sign for the US Dollar.

Away from the highly anticipated testimony of the new Fed Chair, one of the major stories making the rounds are reports that President Xi Jinping is set to tighten his grip on leadership in China by scrapping the two-term presidency rule. Premier Xi remaining in power past his set term is likely to lead to an opportunity to drive through his policy agenda, and appears to have been warmly received by investors. The Shanghai Composite Index advanced by 1.2% on Monday, while the Chinese Renminbi climbed around 0.5% against the USD. Centralizing power under Premier Xi should also lead to China making further reforms and progress towards liberalizing its financial markets, which should provide another reason to expect a stronger Chinese Yuan.

Another currency to have started the week positively against the USD is the Russian Ruble, with the USDRUB down by 0.35% at time of writing and 1% since Friday. S&P Global Ratings raising Russia's credit rating to investment grade BBB-/A-3 on Friday has increased momentum for the Russian Ruble. The Russian economy has withstood a variety of different obstacles over the past couple of years, including international sanctions following the Crimea conflict and declining commodity prices. The economy does, however, appear to have weathered the storm with the outlook for the economy now being more stable. The upgrade should continue to lift sentiment towards the Ruble, as investors receive encouragement to hold capital in Russia.

A hawkish shift in tone from Bank of England (BoE) Deputy Governor Dave Ramsden towards higher UK interest rates has encouraged the Sterling to climb against the Dollar. Ramsden has previously voted against raising UK interest rates, but his comments over the weekend signal that another member of the Monetary Policy Committee (MPC) is becoming upbeat on the UK interest rate outlook. This has also encouraged the market to be more optimistic over a potential UK interest rate rise before the second half of 2018. The expectations that UK Labour leader, Jeremy Corbyn, will support staying in a customs union with the EU after Brexit will also help investor sentiment, as it complements the view that the United Kingdom is heading for a 'softer' Brexit.

The GBPUSD is currently trading 0.4% higher against the Dollar for the day and, as long as the GBPUSD manages to remain above the psychological 1.40 level, the outlook will be that the Pound can trade higher as the week continues.

GBPUSD: Strengthens, Remains On The Offensive

GBPUSD - The pair followed through higher on the back of its Friday gain on Monday. Support lies at the 1.4000 level where a break will turn attention to the 1.3950 level. Further down, support lies at the 1.3900 level. Below here will set the stage for more weakness towards the 1.3850 level. Conversely, resistance stands at the 1.4100 levels with a turn above here allowing more strength to build up towards the 1.4150 level. Further out, resistance resides at the 1.4200 level followed by the 1.4250 level. On the whole, GBPUSD looks to correct further higher.

Xi Jinping Set to Secure China’s Reform Path

China's news agency Xinhua yesterday reported that the Central Committee of the Communist Party has made a proposal to change the Constitution and remove the phrase that says the President can sit for only two terms (each of five years). This paves the way for Xi Jinping to be able to stay as President when his current term expires in 2023. With Xi Jinping most likely to stay in power for another 10 years – and possibly more, it should secure the current Chinese economic reform path for a long time. We expect economic policy to continue focusing on the upgrading of China into the areas of technology and innovation, opening the economy up further alongside reducing poverty, fighting financial risks and reducing pollution. The Chinese markets responded positively to the news.

Next step is a formal approval by the NPC

In our view, the Chinese legislative session the National People's Congress, which opens next week, is likely to approve the Central Committee's proposal. With approval, there would no longer be a limit to how long a President could sit and Xi Jinping could, in principle, sit for life if he has support from the Communist Party.

Xi Jinping to be longest sitting leader since Deng Xiaoping

It has been clear for some time that Xi Jinping is the strongest leader since Mao. Xi Jinping was lifted to 'core leader' of the Communist Party in 2016, something his predecessor Hu Jintao did not achieve, and his name was written into the Constitution as the first sitting leader since Mao. Deng Xiaoping's name is also in the Constitution but got there after his death.

Now we also know why there was no designated successor in the new Standing Committee of the Communist Party when it was presented in October 2017. The Party had probably already decided back then that Xi Jinping could stay on as President for longer than the two terms, although it needed a change to the Constitution. Xi Jinping will thus be the longest serving leader since Deng Xiaoping, who was China's 'paramount leader' for around 15 years from 1978 until the early 1990s. Although he stopped having any formal leadership roles in 1989, he was China's de facto leader until Jiang Zemin became President in 1993.

Xi Jinping a powerful leader but necessary to fight vested interests that block reforms

There is no doubt that Xi Jinping has amassed power during his first five years as President and driven a centralisation move. The Party has strengthened its' role and tightened controls. However, it has to be seen in the light of the country Xi Jinping took over in 2013. While economic growth had been high for many years, extensive corruption and crony capitalism was widespread in many spheres of the economy as well documented in the book China's Crony Capitalism by Minxin Pei. For China to get to the next stage of development and not get caught in the so-called 'middle-income trap', it had to deal with this problem. Many countries have become stuck in the 'middle income trap' because the existing leaders did not deal with – or were part of – the crony capitalism that is normal at the middleincome stage of development.

Vested interests block reform and efficiency gains because the people gaining from crony capitalism would lose out due to reforms and a fight against corruption. China's leader from 2003-12 Hu Jintao was generally seen as a weak leader and he failed to deal with the significant growth in corruption that occurred under his watch.

China has a proverb that says 'the mountains are high and the emperor is far away', illustrating the problems for China's leadership in getting local regions to follow orders. The proverb is said to be centuries old, illustrating that this is not a new challenge. The often popular belief that everyone follows orders from the top of the Party has been quite far from the truth. Collusion between local governments, local state-owned banks and local state-owned enterprises (SOEs) has been a widespread problem and also a factor behind the bad debts that have piled up in China.

For Xi Jinping, the fight against corruption was also a matter of securing the legitimacy of the Communist Party among a population where corruption is very unpopular. He has spoken extensively in many speeches about how to secure the legitimacy among the Chinese people. In combination with high inflation, anger over corruption was the main culprit behind the big protests at Tiananmen Square in 1989.

Xi Jinping set to secure the reform path and push for efficiency

While China has broadly managed to stay on a reform path throughout the 40-year period since the reform and opening policy began in 1978, Chinese leaders have been constantly challenged by a more conservative left-wing faction of the Communist Party. Following the crisis in 1989, conservatives in the Communist Party argued it happened due to the reforms. However, following a three-year reform vacuum, Deng Xiaoping gave a clear signal of continued reform with his 'southern tour' in 1992, when he visited the export areas of Shenzen, Guanzhou and Zhuhai. After that, foreign investment started to pour in again and the way was paved for the biggest push of economic reforms in China's history under Zhu Rongji, who was China's strong economic tsar of the 1990s (became premier 1998-2003). Interestingly, this was also a period of strong centralisation. Under President Hu Jintao (2003- 2013) the reform pace slowed down and the rapid growth during his period was due partly to the reforms done in the late 1990s and the entry into WTO in 2001 engineered by Zhu Rongji.

Although reforms in China have happened in ebbs and flows, we believe Xi Jinping is likely to be a guarantor of a continued steady reform path for many years to come. Xi Jinping launched a very ambitious reform agenda at the 3rd Plenum in 2013 and in 2015 he pushed for a deepening of supply-side reforms by reducing overcapacity, improving the efficiency of SOEs, closing zombie companies and fostering public-private partnerships. As already mentioned, the significant hindrance to making local SOEs more efficient is vested interests. However, it is becoming increasingly difficult for the local regions not to 'follow orders' from Beijing. Refraining from taking the necessary reform steps and fighting financial risks is likely to have bigger consequences for local leaders in the future.

The balance of not becoming too powerful

While the power of Xi Jinping is probably good for fighting vested interests, there is a delicate balance of not becoming too powerful and intervening in too many things. There is no doubt that companies are under closer scrutiny these days, causing some concern that this will inhibit the innovation and entrepreneurship for which China aims. China's government has stepped in when it has deemed the activities of private companies unhealthy for the Chinese economy. The most recent case was last week when China took over control of the insurance company Anbang Insurance Group and prosecuted the former Chairman Wu Xiaohui for alleged 'economic crimes'.

The China Insurance Regulatory Commission (CIRC) said on its website that it aimed to protect consumer interests, as the company's unlawful practices may endanger Anbang's solvency. In 2017, China also implemented measures to limit and restrict what it calls extensive overseas investments. The State Council released guidelines for foreign investments 'to promote healthy growth of overseas investments and prevent risks'. It put restrictions on foreign investments in real estate, hotels, entertainment, sport clubs and outdated industries. China promotes what it sees as 'patriotic' investments but not investments that do not benefit the overall Chinese economy but instead could put it at risk.

The surveillance of activities and uncertainty over potential government intervention has created some anxiety in business circles, which works against the aim of fostering an entrepreneurial spirit. China thus has to tread carefully here and strike the right balance. The 'new era' is a Xi Jinping era

To sum up, it is now clear that 'Socialism with Chinese Characteristics in a New Era' is set to be an era with Xi Jinping at the helm for a long time. We believe it will be an era with continued tight control but also a strong hand in fighting vested interests and reinforcing that the Chinese economy can continue on a path of economic reform and take the next step on its development path. At the top of the current political agenda is what China has called the 'three tough battles', which are fighting financial risks, reducing pollution and eradicating poverty. Supply-side reforms and investment in technology are also high on the agenda.

If China manages to stay on this path of reform, the size of the Chinese economy is likely to double over the next 10-15 years and become the world's biggest economy. A constant challenge for China will be to navigate on the global scene with a world that has become increasingly anxious as China grows in size. Not least, dealing with the US response to China's growing role will be an important part of China's foreign policy. It seems Xi Jinping is well aware of this as reports suggest Xi will give Wang Qishan, his most trusted ally, an important role in foreign affairs. Wang stepped down from the Standing Committee of the Politbureau in October, as he fell foul of the informal age limit rule as he was older than 67 years (see South China Morning Post: Will China's new foreign policy dream team be the key to achieving its global ambitions?, 25 January). Wang is one of the most respected Chinese politicians and dealt with the US a lot when he was Governor of China Construction Bank in the 1990s and later when he was in charge of the Chinese side of the US-China Strategic and Economic Dialogue.

Canadian Dollar Edges Higher, US Housing Report Next

The Canadian dollar has recorded slight gains in the Monday session. Currently, USD/CAD is trading at 1.2663, up 0.22% on the day. On the release front, it's a quiet start to the week. There are no Canadian releases on the schedule. The US releases New Home Sales, which is expected to jump to 655 thousand. On Tuesday, Canada releases the annual budget. The US will release durable goods and consumer confidence reports. As well, Federal Chair Jerome Powell will testify before the House Financial Services Committee.

Canada releases its annual budget on Tuesday. In October, the Trudeau government revised downwards the deficit for the 2017-2018 fiscal year to C$19.9 billion. The Canadian economy was steady in the fourth quarter, so the deficit could be even lower. The budget is not expected to show any major spending, so it's likely that the release will not shake up the Canadian dollar. The Canadian currency lost ground last week, and touched its lowest level since late December.

Jerome Powell took over from Janet Yellen earlier this month, and will be on center stage this week, when he testifies before the House of Representatives and the Senate. After the recent stock markets volatility, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.53; (P) 106.83; (R1) 107.15; More...

Outlook in USD/JPY is unchanged and intraday bias remains neutral. Outlook also remains bearish with 108.27 resistance intact. On the downside, break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

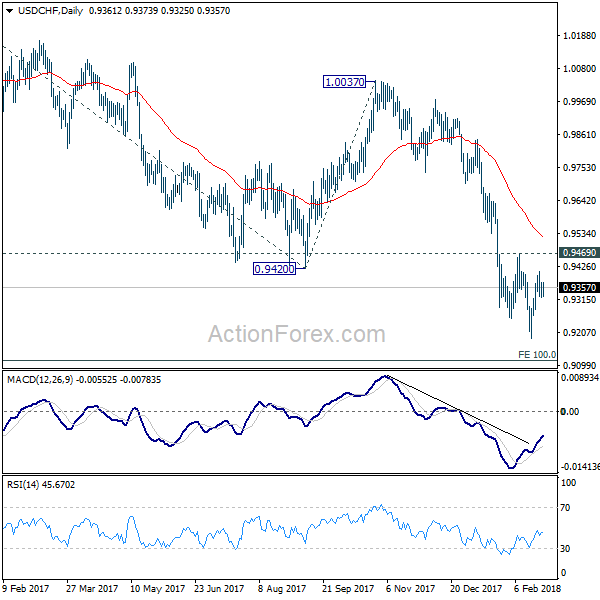

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9325; (P) 0.9349; (R1) 0.9379; More...

Outlook in USD/CHF is unchanged and intraday bias remains neutral. With 0.9469 resistance intact, deeper fall is still expected. On the downside, break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9520) and above.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

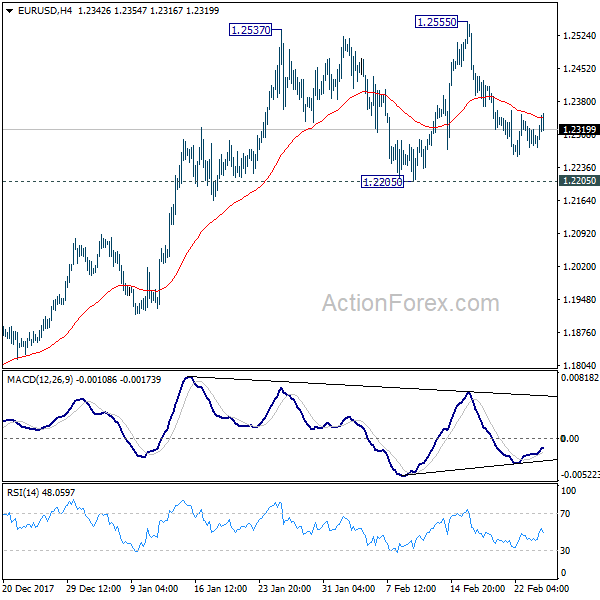

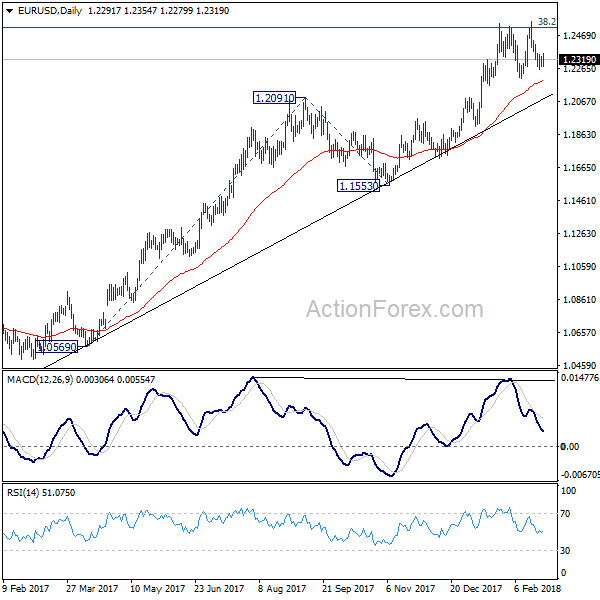

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2269; (P) 1.2303 (R1) 1.2327; More....

No change in EUR/USD's outlook and intraday bias remains neutral. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

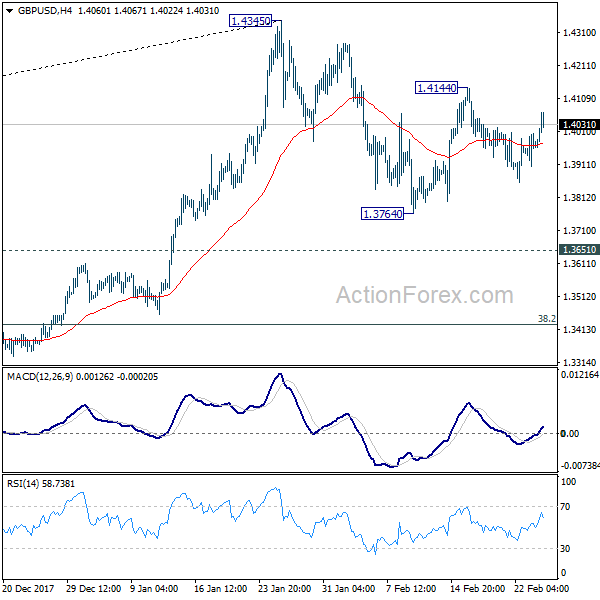

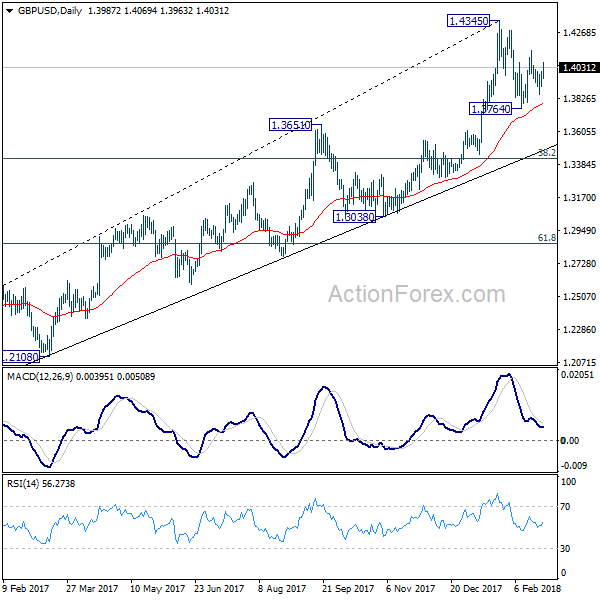

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3912; (P) 1.3958; (R1) 1.4014; More....

GBP/USD rebounds today but upside is limited below 1.4144 minor resistance. Intraday bias neutral first. On the upside, break of 1.4144 will extend the rise from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.