Sample Category Title

Will Canada’s Inflation Data Reverse The Loonie’s Losing Trend?

Early today, Statistics New Zealand released retail sales data that beat analysts' forecast. Data from the agency showed that core retail sales grew by 1.8% against the expected 0.7% while the retail for Q4 rose by 1.7% compared to the forecasts of 1.4%. Following the release, the kiwi fell 0.35% against the dollar, continuing a downward trend that started yesterday when the pair hit a three-day high of 0.7632. Today, no major dollar economic data will be released. As such, the pair could continue its downward momentum, pushing it to below 0.7240.

Today, we will receive inflation data from Canada, which will be very important for the Canadian Dollar. A disappointing number could see a sharp decrease in the Canadian dollar. Traders expect the annualized CPI to grow by 1.4%, down from the previously reported 1.9%. They expect the monthly CPI to grow by 0.4% compared to last month's -0.4%. Other data to be released are the Common CPI and Core CPI.

In Europe, we will receive GDP data from Germany, the largest economy in the region. Traders expect the data to show that the economy expanded by an annualized rate of 2.3%. They also expect the data to show that the economy expanded by 0.6%, down from last month's 0.8%. We will also receive inflation data from the EU. Traders expect the core CPI to grow by 1.0% while the annualized CPI to remain at 1.3%. A surprise beat to the upside will lead the EUR to more gains as traders anticipate a rate increase before the end of the year.

EUR/USD

Today, the EUR/USD is little moved following yesterday's sharp fall from the 1.2556 level. Traders are waiting for the inflation data from the EU and the GDP numbers from Germany. The first scenario today is where the pair reverses its downward trend and reaches the important resistance area of 1.2420. The alternative scenario is where the pair continues to fall and reaches the 1.2205 level.

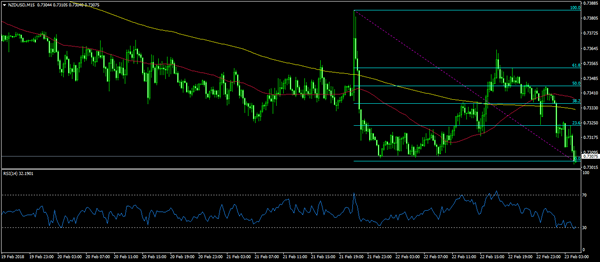

NZD/USD

The pair fell to a new weekly low of 0.7032, even as the retail data showed significant improvements. Using the Relative Strength Index, there is a likelihood that the pair could reverse as traders take profits. The likely scenario is where the pair tests the 0.7323 resistance level.

USD/CAD

The Canadian dollar has weakened significantly against the dollar. It is now trading at a near two-month low. The upward trend in the pair could change today when Canada releases its inflation data. Bullish data could see the pair reverse to the 1.2450 level while bearish data could see the pair's momentum continue to rise to 1.2925.

Forex Analysis: US Secretary Of Defence Supports Commerce Department On Steel

The US Secretary of Defence says he supports the Commerce Department’s actions on steel and aluminium trade. He also said that targeted tariffs are preferable to a global quota or a global tariff. This would impact EU based steel companies as well as those based in China.

French Consumer Price Index (EU norm) (YoY) (Feb) came in as expected, unchanged at 1.5%.

German IFO – Current Assessment (Feb) was 126.3 v an expected 127.0, from 127.7 previously, which was revised up to 127.8. IFO – Business Climate (Feb) was 115.4 v an expected 117.0, from 117.6 previously. IFO – Expectations (Feb) were 105.4 v an expected 107.9, from 108.4 prior, which was revised down to 108.3. EURUSD found support at 1.22751 before moving higher to 1.22990 after the data was released.

UK Gross Domestic Product (YoY) (Q4) was 1.4% v an expected 1.5%, from 1.5% previously. Gross Domestic Product (QoQ) (Q4) was 0.4% v an expected 0.5%, from 0.5% previously. GBPUSD went to a low of 1.38735 before recovering to a high of 1.39018.

US Continuing Jobless Claims (Feb 9) was 1.875M v an expected 1.930M, from a previous number of 1.942M, which was revised up to 1.948M. Initial Jobless Claims (Feb 16) was 222K v an expected 230K, with the prior reading of 230K, which was revised down to 229K. EURUSD moved higher from 1.22900 to a high of 1.23345 after this data release.

Canadian Retail Sales Ex Autos (MoM) (Dec) was -1.8% v an expected 0.3%, from 1.6% previously, which was revised up to 1.7%. Retail Sales (MoM) (Dec) was -0.8% v an expected 0.2%, from 0.2% previously, which was revised up to 0.3%. USDCAD moved higher from 1.26989 to 1.27525 following this release.

US FOMC Member Bostic spoke at the Banking Outlook Conference hosted by the Federal Reserve Bank of Atlanta. He made the following comments: The Fed is carefully calibrating a return to more normal policy and things continue to look up, citing the Atlanta GDP tracker.

US FOMC Member Kaplan’s speech was closely followed by traders for any hints on future policy. He said that he sees US GDP growth around 2.5%-2.75% in 2018 and he would give the economy a B+ or an A-, with a weaker grade next year. He says that the labour market is getting very tight but he has not seen it fan higher wages yet. Inflation will firm up this year but won’t be a hockey stick shape. Businesses still show a lack of pricing power and some progress will be made this year on inflation.

Japanese National Consumer Price Index (YoY) (Jan) was 1.4% v an expected 1.3%, from a prior 1.0% in December. National Consumer Price Index Ex-Fresh Food (YoY) (Jan) was 0.9% v an expected 0.8%, from a prior 0.9% in December. USDJPY moved higher from 106.681 to 106.990 following this release.

EURUSD is down -0.25% overnight, trading around 1.22991.

USDJPY is up 0.31% in early session trading at around 107.068.

GBPUSD is down -0.07% to trade around 1.39416.

Gold is down -0.39% in early morning trading at around $1,326.88.

WTI is up 0.21% this morning, trading around $62.76

Major data releases for today:

EU European Council Meetings will take place today and may impact on moves in EUR crosses.

At 07:00 GMT, German Gross Domestic Product w.d.a (YoY) (Q4) is expected to come in unchanged at 2.9%. Gross Domestic Product (QoQ) (Q4) is also expected unchanged at 0.6%. Gross Domestic Product (YoY) (Q4) is expected to be unchanged at 2.3%. EUR crosses could see a spike in volatility should the data released differ from the expected consensus.

At 10:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Jan) will be released. The consensus is for an unchanged value of 1%. Consumer Price Index (MoM) (Jan) is expected to be -0.9% from 0.4% previously. Consumer Price Index (YoY) (Jan) is expected to be unchanged at 1.3%. Consumer Price Index – Core (MoM) (Jan) is expected at -1.6% from 0.5% prior. EUR pairs can see volatility pick up due to this data.

At 12:00 GMT, UK BOE Ramsden is scheduled to participate in a panel discussion titled “Tackling the UK’s Productivity Challenge” at the East of England Confederation of British Industry event, in Cambridge. This may impact on moves in GBP crosses.

At 13:30 GMT, Canadian Consumer Price Index (MoM) (Jan) is expected to be 0.4% from -0.4% previously. BOC Consumer Price Index Core (YoY) (Jan) is expected to be unchanged at 1.2%. BOC Consumer Price Index Core (MoM) (Jan) is expected at 0.7% v a prior -0.5%. Consumer Price Index (YoY) (Jan) is expected to be 1.4% from 1.9% previously. Consumer Price Index – Core (MoM) (Jan) was 0.1% previously. CAD crosses could be affected by this release.

At 15:15 GMT, US Fed’s Dudley is due to participate in a panel discussion about the Fed’s balance sheet at the United States Monetary Policy Forum, in New York, with comments having the potential to move USD pairs.

At 18:00 GMT, Baker Hughes US Rig Count numbers will be released. The prior number last Friday showed that there were 798 Oil rigs in operation. WTI traders will be paying close attention to this number as they look to the week ahead.

At 18:30 GMT, US FOMC Member Mester is due to participate in a panel discussion about monetary policy objectives at the United States Monetary Policy Forum, in New York. This event may impact USD crosses and assets.

At 20:40 GMT, US FOMC Member Williams is scheduled to speak about economic and monetary policy at the City Club of Los Angeles. Audience questions are expected to follow, and his comments will be followed by traders for any hints on future US FOMC policy.The US Secretary of Defence says he supports the Commerce Department’s actions on steel and aluminium trade. He also said that targeted tariffs are preferable to a global quota or a global tariff. This would impact EU based steel companies as well as those based in China.

French Consumer Price Index (EU norm) (YoY) (Feb) came in as expected, unchanged at 1.5%.

German IFO – Current Assessment (Feb) was 126.3 v an expected 127.0, from 127.7 previously, which was revised up to 127.8. IFO – Business Climate (Feb) was 115.4 v an expected 117.0, from 117.6 previously. IFO – Expectations (Feb) were 105.4 v an expected 107.9, from 108.4 prior, which was revised down to 108.3. EURUSD found support at 1.22751 before moving higher to 1.22990 after the data was released.

UK Gross Domestic Product (YoY) (Q4) was 1.4% v an expected 1.5%, from 1.5% previously. Gross Domestic Product (QoQ) (Q4) was 0.4% v an expected 0.5%, from 0.5% previously. GBPUSD went to a low of 1.38735 before recovering to a high of 1.39018.

US Continuing Jobless Claims (Feb 9) was 1.875M v an expected 1.930M, from a previous number of 1.942M, which was revised up to 1.948M. Initial Jobless Claims (Feb 16) was 222K v an expected 230K, with the prior reading of 230K, which was revised down to 229K. EURUSD moved higher from 1.22900 to a high of 1.23345 after this data release.

Canadian Retail Sales Ex Autos (MoM) (Dec) was -1.8% v an expected 0.3%, from 1.6% previously, which was revised up to 1.7%. Retail Sales (MoM) (Dec) was -0.8% v an expected 0.2%, from 0.2% previously, which was revised up to 0.3%. USDCAD moved higher from 1.26989 to 1.27525 following this release.

US FOMC Member Bostic spoke at the Banking Outlook Conference hosted by the Federal Reserve Bank of Atlanta. He made the following comments: The Fed is carefully calibrating a return to more normal policy and things continue to look up, citing the Atlanta GDP tracker.

US FOMC Member Kaplan’s speech was closely followed by traders for any hints on future policy. He said that he sees US GDP growth around 2.5%-2.75% in 2018 and he would give the economy a B+ or an A-, with a weaker grade next year. He says that the labour market is getting very tight but he has not seen it fan higher wages yet. Inflation will firm up this year but won’t be a hockey stick shape. Businesses still show a lack of pricing power and some progress will be made this year on inflation.

Japanese National Consumer Price Index (YoY) (Jan) was 1.4% v an expected 1.3%, from a prior 1.0% in December. National Consumer Price Index Ex-Fresh Food (YoY) (Jan) was 0.9% v an expected 0.8%, from a prior 0.9% in December. USDJPY moved higher from 106.681 to 106.990 following this release.

EURUSD is down -0.25% overnight, trading around 1.22991.

USDJPY is up 0.31% in early session trading at around 107.068.

GBPUSD is down -0.07% to trade around 1.39416.

Gold is down -0.39% in early morning trading at around $1,326.88.

WTI is up 0.21% this morning, trading around $62.76

Major data releases for today:

EU European Council Meetings will take place today and may impact on moves in EUR crosses.

At 07:00 GMT, German Gross Domestic Product w.d.a (YoY) (Q4) is expected to come in unchanged at 2.9%. Gross Domestic Product (QoQ) (Q4) is also expected unchanged at 0.6%. Gross Domestic Product (YoY) (Q4) is expected to be unchanged at 2.3%. EUR crosses could see a spike in volatility should the data released differ from the expected consensus.

At 10:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Jan) will be released. The consensus is for an unchanged value of 1%. Consumer Price Index (MoM) (Jan) is expected to be -0.9% from 0.4% previously. Consumer Price Index (YoY) (Jan) is expected to be unchanged at 1.3%. Consumer Price Index – Core (MoM) (Jan) is expected at -1.6% from 0.5% prior. EUR pairs can see volatility pick up due to this data.

At 12:00 GMT, UK BOE Ramsden is scheduled to participate in a panel discussion titled “Tackling the UK’s Productivity Challenge” at the East of England Confederation of British Industry event, in Cambridge. This may impact on moves in GBP crosses.

At 13:30 GMT, Canadian Consumer Price Index (MoM) (Jan) is expected to be 0.4% from -0.4% previously. BOC Consumer Price Index Core (YoY) (Jan) is expected to be unchanged at 1.2%. BOC Consumer Price Index Core (MoM) (Jan) is expected at 0.7% v a prior -0.5%. Consumer Price Index (YoY) (Jan) is expected to be 1.4% from 1.9% previously. Consumer Price Index – Core (MoM) (Jan) was 0.1% previously. CAD crosses could be affected by this release.

At 15:15 GMT, US Fed’s Dudley is due to participate in a panel discussion about the Fed’s balance sheet at the United States Monetary Policy Forum, in New York, with comments having the potential to move USD pairs.

At 18:00 GMT, Baker Hughes US Rig Count numbers will be released. The prior number last Friday showed that there were 798 Oil rigs in operation. WTI traders will be paying close attention to this number as they look to the week ahead.

At 18:30 GMT, US FOMC Member Mester is due to participate in a panel discussion about monetary policy objectives at the United States Monetary Policy Forum, in New York. This event may impact USD crosses and assets.

At 20:40 GMT, US FOMC Member Williams is scheduled to speak about economic and monetary policy at the City Club of Los Angeles. Audience questions are expected to follow, and his comments will be followed by traders for any hints on future US FOMC policy.

Elliott Wave View: Gold Ended Correction

We revise our Gold Short Term Elliott Wave view to a more aggressive one and call the decline to 2.8.2018 at $1306.8 ending Intermediate wave (X). For this view to get validity however, the yellow metal needs to break above Intermediate wave (W) at $1366.06. Until then, the alternate view can’t be ruled out that the yellow metal can do a double correction in Intermediate wave (X) towards $1228.27 – $1302.28 before the rally resumes.

Up from $1306.8, the rally is proposed to be unfolding as a zigzag Elliott Wave structure where Minute wave ((a)) ended at $1361.72 and Minute wave ((b)) is proposed complete at $1320.60. Near term, while pullbacks stay above there, and more importantly above $1306.8, expect Gold to extend higher. We don’t like selling the yellow metal. If Gold breaks below $1306.8, then the yellow metal is doing a double correction in Intermediate wave (X) and opens extension lower towards $1228.27 – $1302.28 where buyers should appear for at least a 3 waves bounce.

Gold 1 Hour Elliott Wave Chart

Market Update – Asian Session: Asian Equity Markets Open Broadly Higher After Mixed US Session

Headlines/Economic Data

General Trend:

Japan Jan Core CPI holds steady, while headline inflation hits highest level since March 2015 (highest since July 2014 excluding impact of sales tax hike)

China takes temporary control of Anbang Insurance

China said to speak with banks about support for conglomerate HNA Group

Kiwi (NZD) under performs

South Korea confirms to resume sales of 50-year bonds

Australia/New Zealand

ASX 200 opened +0.4%; closed +0.8%

ASX 200 Resources Index +1.6%, REIT +1.2%, Financials +0.6%

(AU) Australia sells A$400M v A$400M in May 2021 bonds, avg yield 2.1289% , bid to cover 6.12x

(NZ) New Zealand Q4 Retail Sales (Ex Inflation) Q/Q: 1.7% v 1.4%e

(AU) Fitch affirms Australia 4 major banks (Commonwealth Bank, ANZ, NAB, Westpac)

(AU) Australia Deputy PM Joyce resigns as leader of National Party, remains in parliament

China/Hong Kong

Shanghai Composite opened +0.2%, Hang Seng opened +1%

Hang Seng Property/Construction Index +1.3%, Energy+1.1%, Materials +1%, Services +1%, Info Tech +0.9%, Financials +0.9%

Shanghai Property index rises over 2% then pares gain

Aluminum producer Rusal [486.HK] declines over 1% as Q4 adj EBITDA missed estimates

(CN) China regulators take over Anbang Insurance for 1-year from Feb 23rd; company to'remain private' - US financial press

(CN) China to notify banks about supporting HNA Group - US financial press

(CN) China revises Jan Trade Surplus higher to $20.35B v $20.34B prelim; US dollar (USD) denominated imports revised to +36.8%v +36.9% prelim – Customs

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3482 V 6.3530 PRIOR

(CN) China PBoC OMO: Injects CNY230B v CNY350B injected in 7-day, 28-day and 63-day reverse repos prior

Japan

Nikkei 225 opened +0.3%: closed +0.7%

TOPIX Iron & Steel Index +1.8%, Real Estate+1.5%, Securities +1.5%

JAPAN JAN NATIONAL CPI Y/Y: 1.4% V 1.3%E(Highest since March 2015*); CPI EX-FRESH FOOD (CORE) Y/Y: 0.9% V 0.8%E[*Note: According to Japan government data, the overall Jan CPI rose at the fastest pace since July 2014 (ex impact of sales tax hike)]

Japan Finance Min Aso: Want to raise nationwide sales tax as scheduled in Oct 2019; Reiterates important for BoJ to maintain current policy framework

Korea

Kospi opened +0.5%

Samsung Electronics [005930.KR]: To spend $6.0B by 2020 to expand Hwaseong chip plant, could expand investment after the production line begins operations

South Korea Vice Finance Min: To resume sale of 50-year Treasury bonds in mid-March; the specific date and amount has not been set as of yet

South Korea Q4 Short-term External Debt:$115.9B v $118.9B prior

US said to announce new sanctions on North Korea on Friday - financial press

Other Asia

(SG) Singapore Jan CPI M/M: -0.2% v +0.2%e; Y/Y: 0.0% v 0.4%e; CPI Core Y/Y: 1.4% v 1.5%e

NorthAmerica

US equity markets ended mixed: Dow +0.7%,S&P500 +0.1%, Nasdaq -0.1%, Russell 2000 -0.1%

S&P500 Energy +1.1%, Real Estate +1.1%; Financials -0.8%

(US) Fed's Bullard (dove, non-voter): Not behind view for 4 rate hikes in 2018 "unless everything goes perfect"; idea that rates have to rise 100bp in 2018 "seems like a lot to me."– CNBC

(US) Fed's Kaplan (non-voter, dove): Still believes three 2018 hikes is a good base case

(US) Fed's Bostic (2018 voter, dove): Fed is carefully calibrating a return to more normal policy - comments in Atlanta

(US) Fed's Dudley (dove, FOMC voter): Does not comment on monetary policy in prepared remarks

(US) NY Fed Jan primary dealer survey: median dealer saw 3 hikes in 2018 before Jan FOMC meeting

(US) TREASURY $28B 7-YEAR NOTE AUCTION RESULTS:DRAWS 2.839% (highest yield since March 2011); BID-TO-COVER: 2.49 V 2.73 PRIOR AND 2.54 AVG OVER LAST 12 AUCTIONS (lowest BTC since Nov 2017)

(US) US Treasury Sec Mnuchin: President Trump's policies will raise wages without inflation

(US) US Defense Secretary Mattis: Supports Commerce Dept's actions on steel and aluminum; targeted tariffs are preferable to global quota or global tariff

(US) DOE CRUDE: -1.6M V +2ME

Europe

(EU) ECB's Smets (Belgium):has full confidence ECB will reach inflation goal; Euro strength and volatility is not yet a concern

Levels as of 01:00ET

Hang Seng +0.9%; Shanghai Composite +0.1%; Kospi +1.2%

Equity Futures:S&P500 +0.3%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 +0.3%

EUR 1.2295-1.2338 ; JPY 106.65-107.05; AUD 0.7816-0.7849 ;NZD 0.7289-0.7346

Feb Gold -0.3% at $1,329/oz;Feb Crude Oil -0.1% at $62.70/brl; Mar Copper -0.6% at $3.217/lb

The ECB Minutes Yesterday Were Slightly On The Dovish Side

Market movers today

On a day with few important data releases, the financial markets will be looking to signs from the Fed on the outlook for the economy and monetary policy, when US Fed chair William's speaks . The minutes from the January meeting showed that the Fed has become more upbeat on the US economy following the tax reform, which has since then been supplemented by more expansionary fiscal spending out look. Hence financial markets will closely watch for Fed speakers giving signs of a fourth rate hike being in play this year.

In Norway, the oil investment survey is due, where we expect a solid upward revision of the estimate for 2018 given that a large number of field development plans have been submitted since the previous survey. However, this would still be in line with our relatively optimistic forecast for investment activity in the Norwegian oil sector (for more details, see the Scandi section next page).

In Sweden, the Riksbank Minutes due for release at 09:30 will be scrutinized for indications as to how sensitive the Board is to further inflation disappointments (like the one earlier this week, for more details see Scandi section).

Selected market news

Asian equity markets are generally higher this morning, mirroring higher US markets yesterday. At the same time, US 10 year yields remained near their highest since 2014. Dallas Fed President Robert Kaplan spoke yesterday at an event in Vancouver, saying that FED policy is accommodative, but the rate path to a neutral monetary stance may be flatter and not as far away as the market may think, reiterating that he sees three rate hikes this year as appropriate, although evidence of rising inflation would affect his rate view.

In our view, the ECB minutes yesterday were slightly on the dovish side, but we keep our call on the revisit forward guidance in March: the Minutes said on the issue that ‘language pertaining to the monetary policy stance could be revisited early this year as part of the regular reassessment at the forthcoming monetary policy meetings. ' As we pointed to earlier, the QE flexibility is first in line with the minutes saying ‘some members expressed a preference for dropping the easing bias regarding the APP'. In line with our view, the ECB board members are not concerned about the exchange rate path through to inflation for now.

On Brexit, Prime Minister Theresa May yesterday gathered her top ministers for an eighthour session to get them to back her Brexit strategy. One of the key elements that appears to be on the table from the UK side is a " three basket approach", which would allow the UK to apply varying degrees of EU rules. The European Commission yesterday pre-empted the out come of Theresa May's meeting by saying that such plan would be the same as a ‘cherry picking' approach that the EU wants to avoid to preserve the integrity of the EU single market.. Theresa May is due to deliver a speech next week on how she sees the future trading relationship between the UK and EU post -Brexit . Trade talks with the EU are due to begin next month, which are set to be challenging.

Aussie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.56% against the USD and closed at 0.7843.

LME Copper prices rose 0.4% or $29.0/MT to $7032.0/MT. Aluminium prices rose 0.2% or $4.0/MT to $2194.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7827, with the AUD trading 0.2% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7795, and a fall through could take it to the next support level of 0.7762. The pair is expected to find its first resistance at 0.7860, and a rise through could take it to the next resistance level of 0.7892.

Next week, market participants would keep a close watch on Australia’s AiG performance of manufacturing index and private sector credit data.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Governing Council Could Revisit Policy Guidance Soon: ECB Minutes

For the 24 hours to 23:00 GMT, the EUR rose 0.45% against the USD and closed at 1.2335, after minutes of the European Central Bank's (ECB) January meeting hinted that policymakers could soon indicate that it is mulling an earlier end to its stimulus programme.

Minutes showed that some policymakers pushed for considering a revision in the language pertaining to the monetary policy stance early this year. However, it was concluded that such an adjustment would be premature at this juncture, as inflation is still not moving decisively higher despite the robust pace of economic expansion. Further, officials broadly agreed that the perceived volatility in the Euro represents a source of uncertainty and need to be monitored.

On the economic front, Germany's Ifo business climate index fell to a 5-month low level of 115.4 in February, on the back of growing concerns over political uncertainty and recent market turmoil. The index had recorded a level of 117.6 in the prior month, while market participants had envisaged for a drop to a level of 117.0. Moreover, the nation's Ifo business expectations index eased to a level of 105.4 in February, hitting its lowest level in 10 months. The index had registered a reading of 108.4 in the prior month, while markets were expecting for a fall to a level of 107.9.

Also, the nation's Ifo current assessment index eased more-than-expected to a level of 126.3 in February, compared to market consensus for a drop to a level of 127.0 and following a level of 127.7 in the prior month.

Macroeconomic data revealed that first time claims for the US unemployment benefits unexpectedly eased to a level of 222.0K in the week ended 17 February, hitting its lowest level in nearly 45 years and pointing to a strong growth in the labour market. Initial jobless claims had recorded a revised reading of 229.0K in the previous week, while markets were anticipating for a rise to a level of 230.0K. Additionally, the nation's leading indicator registered a rise of 1.0% on a monthly basis in January, beating market expectations for an advance of 0.7%. In the previous month, leading indicator had registered a rise of 0.6%.

In the Asian session, at GMT0400, the pair is trading at 1.2306, with the EUR trading 0.24% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2260, and a fall through could take it to the next support level of 1.2214. The pair is expected to find its first resistance at 1.2352, and a rise through could take it to the next resistance level of 1.2398.

Going ahead, traders would look forward to the Euro-zone's final inflation numbers for January as well as Germany's final 4Q GDP data, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

UK’s Economy Grew Less Than Initially Estimated In The Final Three Months Of 2017

For the 24 hours to 23:00 GMT, the GBP rose 0.35% against the USD and closed at 1.3960, shrugging off disappointing GDP report from the UK.

In economic news, the second estimate of Britain's gross domestic product (GDP) was revised lower to 0.4% on a quarterly basis in the three months to December 2017, as household spending and business investment tailed off, thus offering latest sign of the growing hit to the economy from rising inflation. The nation's GDP had registered a similar rise in the previous quarter, while the preliminary print had indicated a rise of 0.5%.

In other economic news, the flash total business investment in the UK remained flat on a quarterly basis in 4Q 2017, compared to an advance of 0.5% in the prior quarter, while markets were anticipating for a gain of 0.4%.

In the Asian session, at GMT0400, the pair is trading at 1.3948, with the GBP trading 0.09% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3874, and a fall through could take it to the next support level of 1.3799. The pair is expected to find its first resistance at 1.4006, and a rise through could take it to the next resistance level of 1.4063.

Amid no macroeconomic releases in the UK today, investors would focus on Britain's Markit manufacturing as well as construction PMs, GfK consumer confidence index, mortgage approvals and net consumer credit data, all set to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Annual Inflation Jumped To Its Strongest Level In Nearly 4 Years In January

For the 24 hours to 23:00 GMT, the USD declined 0.6% against the JPY and closed at 106.70.

In the Asian session, at GMT0400, the pair is trading at 106.90, with the USD trading 0.19% higher against the JPY from yesterday's close.

Overnight data revealed that Japan's national consumer price index (CPI) accelerated 1.4% YoY in January, surging to its highest level since July 2014. Market participants had envisaged the CPI to climb 1.3%, after recording a rise of 1.0% in the previous month.

The pair is expected to find support at 106.46, and a fall through could take it to the next support level of 106.03. The pair is expected to find its first resistance at 107.47, and a rise through could take it to the next resistance level of 108.05.

Moving ahead, Japan's jobless rate, retail trade and consumer confidence index, all due to release next week, would keep investors' on their toes.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Switzerland’s Industrial Output Climbed In 4Q 2017

For the 24 hours to 23:00 GMT, the USD declined 0.67% against the CHF and closed at 0.9326.

In economic news, Switzerland's industrial production grew 8.7% on an annual basis in the October-December 2017 period. In the previous quarter, industrial production had recorded a revised gain of 9.2%.

In the Asian session, at GMT0400, the pair is trading at 0.9345, with the USD trading 0.2% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9310, and a fall through could take it to the next support level of 0.9276. The pair is expected to find its first resistance at 0.9394, and a rise through could take it to the next resistance level of 0.9444.

Looking forward, market participants would eye Switzerland's 4Q GDP, ZEW economic sentiment index, real retail sales and manufacturing PMI, all slated to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.