Sample Category Title

GBP/USD Drifting Down

GBP/USD is decreasing below 1.39, trading between hourly support and resistance and 1.3742 (16/01/2018 low) and 1.4151 (05/02/2018 high). The technical structure suggests further short-term decline.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Bearish Bias

EUR/USD is decreasing further, breaking hourly support at 1.2276 (14/02/2018 low) and heading to further resistance at 1.2165 (17/01/2018 low). Hourly resistance at 1.2510 (15/02/2018 high) is distanced. The technical structure suggests further downside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Technical Outlook: WTI OIL – Bears Cracked Key Supports, Weekly Crude Stocks Report Eyed For Fresh Signals

WTI oil price fell further on Thursday, driven by stronger dollar and probed below pivotal support at $60.93 (Fibo 38.2% of $58.19/$62.63 upleg).

Today's dip was contained by 10SMA ($60.75) with subsequent bounce signaling hesitation at strong $60.93/75 support zone.

However, the price remains within daily cloud which was penetrate yesterday with bearishly aligned daily techs keeping negative near-term outlook.

EIA weekly crude stocks report will be released today and expected to show another build in oil inventories which could have negative impact on oil price.

Firm break below cracked $60.93/75 supports would signal fresh bearish extension towards $60.71 (daily Tenkan-sen) and key supports at $59.89/84 (Fibo 61.8% of $58.19/$62.63 / daily cloud base).

Daily cloud top marks significant resistance at $61.73 which is expected to cap extended upticks.

Only break and close above cloud would sideline near-term bears and shift focus higher.

Res: 61.38, 61.73, 62.00, 62.35

Sup: 60.93, 60.75, 60.41, 59.89

Forex Analysis: US30 And GBPUSD

The reaction to the FOMC Minutes in the US30 index was to initially rally on the positive tones coming from the Fed. However, as we have seen recently, fears about inflation took hold, sending the price tumbling lower through strong support around 25000.00 and 24876.70. The low created so far is 24589.00. A break lower to the 24500.00 level can still be regarded as constructive for bulls but should this level be breached there is a danger that the higher low formed on the 14th of February at 24312.6 is tested. Moving below this level hands control over to the bears, who will attempt to move price down to 24000.00 and the rising blue trend line. A loss of this trend line would be a deeper correction to test the 2018 lows and the 23000.00 level.

But until then, those holding a bullish view have an opportunity to buy any dip created above 24000.00. The area between the current price level and yesterday’s high contains important levels and moving averages that can become increasingly resistive the longer we stay below them. As we have seen with V-shaped recoveries in the past, the sooner the price retraces the move lower, the less chance there is of previous support levels becoming strong resistance levels. The most immediate level to contest is 24876.70, followed by the 50 and 55-period moving averages around 24963.00. The 100-period MA is located at 25079.00 and the 200-period MA at 25143.00. The falling red trend line comes in at 25240.00, with 25436.00 the next resistance overhead. A break to this area can see bearish positions come under pressure, which would lead towards the area around 26000.00.

GBPUSD

The BOE Monetary Policy Committee were in Parliament yesterday for the Inflation Report Hearings. The reaction to this event saw the GBPUSD pair move from 1.39348 to a high for the European session of 1.39898, before slipping back to the start line following US PMI data. With the release of the FOMC Minutes, the pair reached a high of 1.40076 but was unable to sustain this level as the USD strengthened and the pair reached a daily low an hour later at 1.39062. Further selling this morning has seen the 200-period MA broken and price reach 1.38695. The next level of support is found at 1.38354, with 1.37644 below. Should price fail to rally at these levels, there is little in the way of support until 1.36000.

Resistance can be found at the 100-period MA, currently at 1.39667. The Blue resistance trend line, at 1.39830, appears to be part of a bull flag but until this line is tested and broken, price will remain below 1.40000. The Red resistance trend line has been used multiple times now and is located at 1.40910, just below the 1.41000 level. A break above that resistive area can lead to a push for the highs at 1.43450.

USD Takes A Breather Amid FOMC Minutes

FOMC minutes: investors are left waiting for March meeting

The publication of the January FOMC minutes did not affect much the FX market in the absence of any significant news. Market participants were still trying to determine whether “further gradual increase” has to be interpreted in the sense of faster pace of rate hike or whether it will just mean that the Fed will continue on this path and at this pace for years to come. We believe that the latter is more likely, especially in the short-term, as there is no reason for the Fed to accelerate tightening. Inflation is under control. Moreover, in our opinion, it is risky to draw to many conclusions from those minutes as Jerome Powell took over as Fed Chair in the meantime. Indeed, the January FOMC meeting was done under Janet Yellen, and even though Powell will not fundamentally change the Fed thinking, one could expect some small adjustments.

Initially, the greenback had an acute reaction as it fell slightly against most of its peers. However, the mini sell-off was short-lived. This morning, in the absence of a clear driver the buck is performing unevenly. USD/JPY is down 0.40% to 107.30, EUR/USD stabilised at around 1.2280, while USD/CHF maintains a bullish momentum. Given the lack of global driver, investors will remain focus on the Fed and anything that could influence its tightening path. More specifically, the January’s PCE figures that will be released next week and the February’s CPI report, which will be publish on March 13th, will be scrutinized by investors as it could influence the outcome of the FOMC March meeting. We remain positive USD; however it seems that the market remains cautious regarding the buck and do not expect further upside.

South African inflation is under control

Since Cyril Ramaphosa took office as South African President last week, economic data and reform on VAT came out yesterday, in an attempt to shake South African investors, but in vain: South African JSE 40 gained 707 points, ending at 51’727 (+1.39% intraday) and heading for its historical highs along 54’000, supported by Financials (+18.72%), Real Estate (+17.26%), Consumer Staples (+4%) while Consumer Discretionary lagged behind (-5.16%). On forex side, the ZAR continues to gain strength, gaining ground against the USD and EUR, valued at 11.66 (-0.56%) and 14.33 (-1%) respectively.

Published data concerned January Consumer Price Index, given at 4.4% Y/Y and 0.30% M/M (in line with both consensus) against 4.70% and 0.50% for the previous month, confirming our stance that inflation remains under control and is decreasing at an accommodative pace. President Ramaphosa also confirmed an increase of current VAT by 1% (from 14% to 15%) in order to tackle growing debt and improve credit rating. The change in VAT rate is supposed to take immediate affect as of April 1st 2018, keeping in mind that the country owns one of the lowest rate among emerging markets (e.g. China: 17%, Russia: 18% - 10%, Brazil: 25% - 17% or India: 28% - 0%).

Market Update – European Session: Germany IFO Survey Moves Off Record Highs, UK Q4 GDP Revised Lower

Notes/Observations

German IFO sentiment moves off record highs - UK Q4 GDP revised lower in its 2nd reading for its slowest annual pace since 2012 (YoY: 1.4% v 1.5%e)

Asia:

Shanghai Composite reopens after 1-week Lunar New Year break; ends +2.0%

PBoC injected cash in its Open Market Operation (OMO) for its 1st injection after 16 consecutive skips

Europe:

German Finance Ministry Feb Report: No end in sight for German economic expansion; forecasts 2018 GDP growth of 2.4%

German SPD party said to support nomination of Bundesbank's Weidmann as next ECB President (later refuted)

PM May's Cabinet did not agree to her negotiating strategy for the Brexit transition period before it was sent to the EU. The proposal sent to EU nations "prompted a furious backlash after raising the prospect of an open-ended transition period after Brexit." Cabinet ministers were told about the position paper less than 24 hours before it was published. UK PM May and her senior Cabinet minister to meet at Chequers on Thursday, Feb 22nd to try and hammer out a deal over the Govt’s approach to Brexit

Moody's raised Greece sovereign rating two notches to B3 from Caa2; outlook Positive

Americas:

FOMC Jan Minutes saw the majority members view that stronger economic growth would raise the likelihood of further rate hikes. Saw appreciable risk inflation to lag target with almost all Fed officials seeing inflation rising to 2% goal. Number of Fed officials saw upside risks to growth from tax cut - Fed's Quarles (hawk, FOMC voter): Economy was performing well; current policy remained accommodative, gradual rate increases were appropriate

Fed's Kashkari (dove, non-voter): Want to see clear signs of inflation rising to 2% before supporting more rate hikes

Treasury undersecretary Malpass accused China of “patently non-market behavior”; US needs a stronger response to counter it

Energy:

Weekly API Oil Inventories: Crude: -0.9M v +3.9M prior

Economic Data:

(FR) France Jan Final CPI M/M: -0.1% v -0.1%e; Y/Y: 1.3% v 1.4%e

(FR) France Jan Final CPI EU Harmonized M/M: -0.1% v -0.1%e; Y/Y: 1.5% v 1.5%e

(FR) France Feb Business Confidence: 109 v 110e, Manufacturing Confidence: 112 v 113e, Production Outlook Indicator: 30 v 33e, Own-Company Production Outlook: 16 v 15e

(CH) Swiss Q4 Industrial Output WDA Y/Y: 8.7 v 9.2% prior, Industry & Construction Output WDA Y/Y: 8.5% v 8.0% prior

(HK) Hong Kong Jan CPI Composite Y/Y: 1.7% v 1.8%e

(HK) Hong Kong Jan Unemployment Rate: 2.9% v 2.9%e (matched lowest level since Feb 1998)

(SE) Sweden Q4 Total Number of Employees Y/Y: 2.4% v 3.0% prior

(DE) German Feb IFO Business Climate: 115.4 v 117.0e; Current Assessment: 126.3 v 127.0e, Expectations Survey: 105.4 v 107.9

(IT) Italy Dec Industrial Orders M/M: 2.5 v 0.4% prior; Y/Y: 7.2 v 8.9% prior

(IT) Italy Dec Industrial Sales M/M: 6.5 v 1.4% prior; Y/Y: 6.9 v 5.1% prior

(UK) Q4 Preliminary GDP (2nd reading) Q/Q: 0.4% v 0.5%e; Y/Y: 1.4% v 1.5%e (slowest annual pace since 2012)

(UK) Q4 Preliminary Private Consumption Q/Q: 0.3% v 0.4%e, Government Spending Q/Q: 0.6% v 0.3%e, Gross Fixed Capital Formation Q/Q: 1.1% v 0.5%e, Exports Q/Q: -0.2% v +0.5%e, Imports Q/Q: 1.5% v 1.0%e

(UK) Q4 Preliminary Total Business Investment Q/Q: 0.0% v 0.4%e; Y/Y: 2.1% v 2.4%e

(UK) Dec Index of Services M/M: 0.0% v 0.0%e; 3M/3M: 0.6% v 0.5%e

(IT) Italy Jan Final CPI M/M: 0.3% v 0.2% prelim; Y/Y: 0.9% v 0.8% prelim

(IT) Italy Jan Final CPI EU Harmonized M/M: -1.5% v -1.6% prelim; Y/Y: 1.2% v 1.1%e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.8% at 378.0, FTSE -1.0% at 7207, DAX -1.0% at 12349, CAC-40 -0.5% at 5276 , IBEX-35 -0.1% at 9814, FTSE MIB -0.6% at 22526 , SMI -0.7% at 8930, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European Indices trade lower across the board following on from a lower close in Wallstreet overnight and weaker futures this morning following the FOMC minutes yesterday. This morning also saw another swath of earnings with Barclays bucking the oveall market following results with shares higher by over 5%. Positive results from French names Axa, Veolia and Arkema and Bouygues help the CAC marginally outperform, with positive results from Telefonica helping the Spanish Ibex. To the downisde, BATS, Anglo American, Kaz minerals and BAE systems weigh on the FTSE, while Deutsche Telekom trades lower in Germany following earnings miss. Looking ahead notable earners include Sprouts, Hormel and Orbital ATK.

Movers

Consumer Discretionary [BATs [BATS.UK] -5.1% (Earnings)]

Utilities [Veolia [VIE.FR] +0.6% (Earnings)]

Materials [ Anglo American [AAL.UK] -3.8% (Earnings), Kaz Minerals [KAZ.UK] -2.4% (Earnings), Arkema [AKE.FR] +2.8% (Earnings)]

Industrials [BAE Systems [BA.UK] -2.5% (Earnings)]

Telecom [ Bouygues [EN.FR] +2.6% (Earnings), Deutsche Telekom [DTE.DE] -2.9% (Earnings), Telefonica [TEF.ES] +2.6% (Earnings)]

Financial [ Barclays [BARC.UK] +5.2% (Earnings), Axa [CS.FR] +1.0% (Earnings), RSA [RSA.UK] +3.4% (Earnings)]

Speakers

German Chancellor Merkel commented in Bundestag Parliament ahead of Friday’s EU Leader Summit that Each Euro member must undertake ambitious reforms. Must remain competitive; embrace digitization. Stability-growth pact remained the compass of Euro policy

EU official expressed doubts that Brexit transition would hit the March deadline

IFO Economists: Domestic economy and exports were slightly less euphoric. Coalition deal not a cause for jubilation but rather sobriety

Japan Currency Head Asakawa reiterated govt view that BOJ easing was not aimed at weakening the JPY currency (Yen)

Indonesia Finance Ministry: Maintaining planned issuance for 2018; viewed rise in yields as temporary

Currencies

USD maintaining its firm tone in the aftermath of the release of Jan FOMC minutes which help to push Treasury yield higher. Greenback rallied after Jan Minutes saw the majority members of FOMC view that stronger economic growth would raise the likelihood of further rate hikes

GBP/USD continued its soft tone for the 5th straight session as UK Q4 GDP was revised lower in its 2nd reading for its slowest annual pace since 2012 (YoY: 1.4% v 1.5%e). Dealers noted that overall Brexit headlines the past few session were not showing any meaningful progress yet in the transition phase

EUR/USD steady by holding below the 1.23 level but in the middle part of its 2018 400 pip trading range. Focus on ECB Jan minutes for clarity and timeline on potential forward language change. On Wednesday reports circulated that ECB would look to gradually amend its forward guidance before it ended its asset purchase program

Fixed Income

Bund Futures trades up 32 ticks at 158.54 extending its gains after German IFO disappoints across the board. Upside targets159.25, while a return lower targets the157.75 level.

Gilt futures trade at 121.66 up 6 ticks after Q4 UK GDP is revised lower. Support continues to stand at 120.75 then 120.15, with upside resistance at 121.75 then 122.25.

Thursday's liquidity report showed Wednesday's excess liquidity fell to €1.827T from €1.835T prior. Use of the marginal lending facility rose to €119M from €76M prior.

Corporate issuance saw 5 issuers raise $4.5B in the primary market

Looking Ahead

(CA) Canada Feb CFIB Business Barometer: No est v 62.7 prior

(BR) Brazil Feb CNI Industrial Confidence: No est v 59.0 prior

(AR) Argentina Feb Consumer Confidence index: No est v 45.2 prior

05:30 (HU) Hungary Debt Agency (AKK) to sell in 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

05:30 (UK) DMO to sell £950M in 0.125% I/L Nov 2036 Gilts

05:30 (PL) Poland to sell Bonds

06:00 (UK) Feb CBI Retailing Reports Sales: 14e v 12 prior; Total Distribution: No est v 14 prior

06:00 (IE) Ireland Jan PPI M/M: No est v 0.4% prior; Y/Y: No est v -3.6% prior

06:00 (CZ) Czech Republic to sell 3-month Bills

06:00 (RO) Romania to sell Bonds

06:30 (IS) Iceland to sell 6-month Bills - 06:45 (US) Daily Libor Fixing

06:30 (TR) Turkey Feb Capacity Utilization: No est v 78.2 prior

06:30 (TR) Turkey Feb Real Sector Confidence (Seasonally Adj): No est v 110.9 prior; Real Sector Confidence (unadj): No est v 108.3 prior

07:30 (EU) ECB account of Jan 24-25th policy meeting (Jan Minutes)

08:00 (PL) Poland Jan M3 Money Supply M/M: -1.1%e v +2.2% prior; Y/Y: 4.9%e v 4.6% prior

08:00 (RU) Russia Gold and Forex Reserve w/e Feb 16th: No est v $447.4B prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Initial Jobless Claims: 230Ke v 230K prior; Continuing Claims: 1.94Me v 1.942M prior

08:30 (CA) Canada Dec Retail Sales M/M: 0.0%e v +0.2% prior Retail Sales Ex Auto M/M: 0.3%e v 1.6% prior

09:00 (BE) Belgium Feb Business Confidence: 1.5e v 1.8 prior

10:00 (US) Leading Index: 0.7%e v 0.6% prior

10:00 (MX) Mexico Central Bank (Banxico) Feb Minutes

10:00 (US) Fed's Dudley (dove, FOMC voter) to speak at New York Fed Briefing on Puerto Rico

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Weekly DOE Crude Oil Inventories

11:00 (US) Feb Kansas City Fed Manufacturing Activity: 18e v 16 prior

(IT) Italy Debt Agency (Tesoro) announcement for BTP and Floating Rate Note (CCTeu)

12:10 (US) Fed's Bostic (2018 voter, dove) speaks at Banking Conference in Atlanta

13:00 (US) Treasury to sell 7-Year Notes

15:30 (US) Fed's Kaplan (non-voter, dove) on panel

Technical Outlook: AUDUSD – Bears Show Hesitation Ahead Of Key Supports

The pair entered consolidation phase on Thursday, following strong fall the previous day, after Fed minutes inflated the greenback.

Near-term action is moving within daily cloud, which was penetrated on Wednesday's strong bearish acceleration.

Break through cloud top and close in the cloud was bearish signal, reinforcing negative outlook on bearish setup of daily techs for further extension of bear-leg from 0.7988 (16 Feb high) towards key supports, converged 100/200SMA's (0.7773), 09 Feb low (0.7758) and Fibo 61.8% of 0.7500/0.8135 ascend (0.7742).

Bears may show stronger hesitation on approach to these supports which could result in slowing bearish momentum and stronger corrective upticks.

Broken cloud top, reinforced by 55SMA marks initial resistance at 0.7839, with extended rallies to be capped by 10SMA (0.7872) to keep bears intact for fresh attempts lower.

Res: 0.7839, 0.7872, 0.7900, 0.7920

Sup: 0.7790, 0.7773, 0.7758, 0.7742

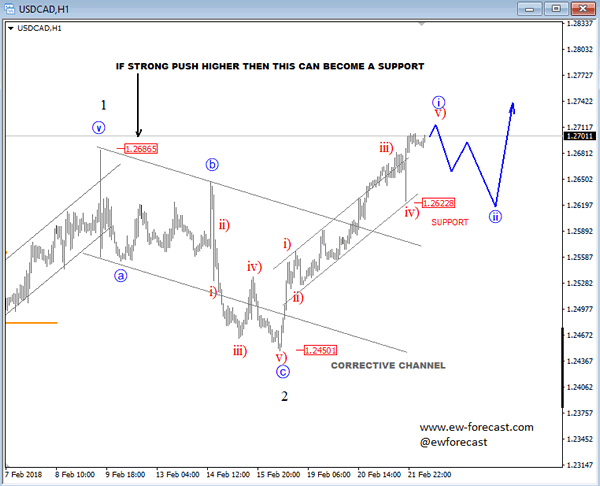

Elliott Wave Analysis: USDCAD And BTCUSD Update

USDCAD bounced perfectly yesterday from that channel support where wave four bottomed so we see pair now in wave five testing that old swing high at 1.2686. If there will be a decisive break through this level with a daily close above it then this old high can become a new support later. If break would be unsuccessful in the next 12 hours then support to keep an eye on for a pullback is at 1.2622.

USDCAD, 1H

BTCUSD is turning south, now falling below the trendline support so we assume that new a-b-c pullback is in play, ideally for 9k.

BTCUSD, 2H

EUR/USD: US Existing Home Sales

The Greenback weakened versus the Euro following the release of US existing home sales report. The EUR/USD pair increased 11 base points, or 0.09%, to hit the 1.2334 level, reflecting the decline in the resales of American homes.

The US National Association of Realtors reported that in January the existing home sales slumped for the second month in a row. Contrary to economists' expectations for the number to have surged 0.9%, existing home sales declined 3.2% in the reported month. It was the largest drop on year-to-year basis over the three-year period. Yet, the demand for housing is increasing due to the boosting labor market, which results as a shortage of buying opportunities for some potential first-time buyers.

GBP/NZD 4H Chart: Set For A Breakout

The Pound Sterling has continued to surge against the New Zealand Dollar since the last time the pair was reviewed. However, there has been some negative development during this period.

The currency pair has been trading in a large-scale triangle after it hit the lower boundary on January 11. Also, the exchange rate has formed a new junior channel during this period.

Given that the GBP/NZD pair is currently trading sideways, traders should expect a breakout in either direction in near future. In addition, technical indicators favour a breakout south.