Sample Category Title

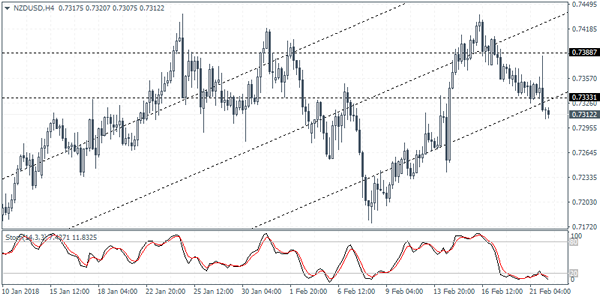

NZDUSD Intraday Analysis

NZDUSD (0.7312): The New Zealand dollar broke past the 0.7333 level of support and this could signal a decline towards 0.7160. However, given the consolidation above 0.7333, there is scope for NZDUSD to likely retrace back above the support level. This could keep NZDUSD to remain range bound in the near term within 0.7387 and 0.7333 region. A breakout from this level will establish the trend direction. To the upside, NZDUSD could be seen posting further gains if price manages to close above the previously established higher. However, we expect to see the corrective decline towards 0.7160 in the near term.

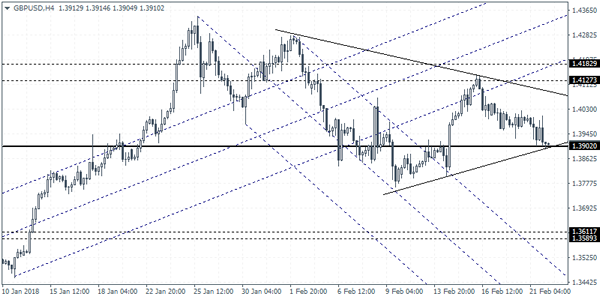

GBPUSD Intraday Analysis

GBPUSD (1.3910): The British pound was seen testing the support level at 1.3902 earlier today. The currency pair was seen falling after a disappointing labor market data and the FOMC minutes which sent the USD higher on the day. While price action could consolidate near the support level, in the event of a breakdown below this support, the declines could push GBPUSD down towards 1.3611 - 1.3589 level of support. Price action is also forming a triangle pattern and this could suggest some near term retracement to the upside. A breakout from the triangle pattern is required to establish further trend direction

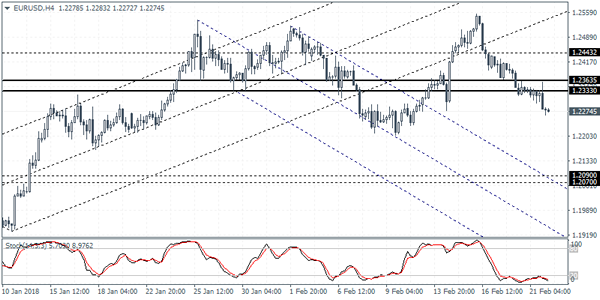

EURUSD Intraday Analysis

EURUSD (1.2274): The EURUSD was seen extending declines for four consecutive days as price action nears the monthly low. From the 4-hour chart, the breakdown below the support level of 1.2365 - 1.2333 signals further decline in price. We now expect to see EURUSD continue towards the lower support level targeting 1.2090 - 1.2070 level. In the short term, any rebound in price is likely to stall near the breached support level which could act as resistance. The downside bias of course changes if EURUSD can break past 1.2365 which could keep price action biased to the upside or potentially turn sideways.

USD Edges Higher On Fed Minutes

The FOMC meeting minutes released yesterday sent the U.S. dollar to close higher on the day as investors brace for a March rate hike. Although the Fed minutes did not reveal anything new, the upbeat tone of the minutes saw the markets pricing three rate hikes this year, with the first rate hike expected as early as March.

Data from the UK showed that the unemployment rate increased to 4.4%. This was higher than the forecasts that indicated no change to the unemployment rate. However, the rise in the unemployment rate was offset by wage growth coming out stable at 2.5% on an annual basis.

In the Eurozone, the flash manufacturing and services PMI showed that economic activity in the bloc continued to rise but the momentum was seen declining after it touched a 12-year high in January.

Looking ahead, the economic calendar today will see investors focusing on the UK's second revised GDP estimates for the fourth quarter of 2017. Data from ONS previously showed that the UK's GDP grew at a pace of 0.5% during the quarter. No changes are expected at today's revised GDP.

In the Eurozone, the ECB will be releasing the monetary policy meeting minutes from January. The ECB had kept interest rates and monetary policy unchanged at its meeting in January. However, investors will brace for any potential hawkish follow through from the minutes.

Later in the evening, the retail sales figures for the fourth quarter of 2017 will be coming out for New Zealand. Economists are optimistic that retail sales might have increased 1.4% on the quarter, accelerating from the 0.2% increase previously.

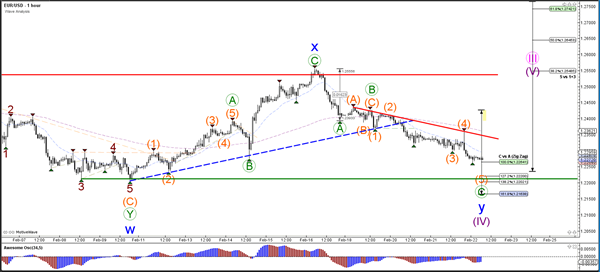

Daily Wave Analysis: GBP/USD Reaches Key Decision Zone For Uptrend Or Downtrend

Currency pair GBP/USD

The GBP/USD broke below the previous top (dotted green) which indicates that the bullish wave pattern is invalidated. Price could either be building a larger WXY (blue) correction within wave 4 (green) or starting a new downtrend.

The GBP/USD is challenging the support trend line and Fibonacci levels of wave W vs Y (blue).

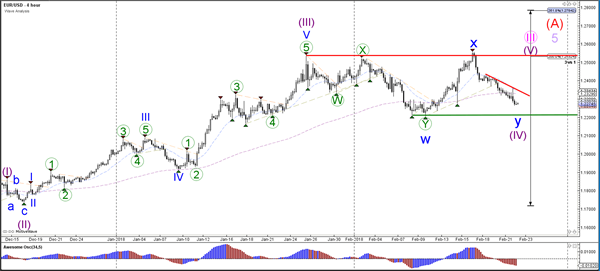

Currency pair EUR/USD

The EUR/USD is testing the support zone of the previous wave W (blue) bottom. A bullish bounce confirms a WXY pattern within wave 4 (purple).

The EUR/USD seems to be in wave 5 (orange) of larger wave C (green).

Currency pair USD/JPY

The USD/JPY is testing a strong resistance zonewhich includes a trend line and the previous bottoms.

The USD/JPY broke below support (dotted blue) but price action has been quite choppy so far.

Elliott Wave View: Gold Can Do A Double Correction

Gold Short Term Elliott Wave view suggests that the yellow metal is still correcting cycle from 12.13.2017 low ($1236.30) as a double three Elliott Wave structure. Down from 1.25.2018 high ($1366.06), the decline is unfolding as a double three where Minor wave W ended at $1306.96 and Minor wave X bounce ended at $1361.81.

Minor wave Y is in progress and the subdivision is also unfolding as a double there where Minute wave ((w)) ended at $1324.75 and Minute wave ((x)) ended at $1336.21. Near term, while bounces stay below $1336.21, but more importantly below $1361.81, the yellow metal has scope to extend lower towards $1288.27 – $1302.28 to end Minor wave Y. Afterwards, expect Gold to resume the rally higher or at least bounce in larger 3 waves to correct cycle from 1.25.2018 high. We don’t like selling the proposed pullback

For this view to be gain more validity, Gold needs to break below Minor wave W at $1306.96. Until then, there is no guarantee Gold will extend lower and the right side remains higher as the yellow metal still has 5 swing bullish sequence from 12.15.2016 low. We do not like selling the proposed pullback and expect buyers to appear at $1228.27 – $1302.28 (if reached) for a 3 waves bounce at least.

Gold 1 Hour Elliott Wave Chart

The US Stock Market Reversed Gains And Bond Yields

Market movers today

In the euro area, a key release is the ECB minutes from the January meeting. No changes were announced at the meeting but we will look for the attention the (in hindsight ) small sell-off and exchange rate volatility had at the time of the meeting. Also, we will be looking for any indications of when the ECB could revisit forward guidance.

In Germany, we will get numbers for the IFO expectations, which we believe will show a further decline to 107.9, possibly influenced by some turbulent weeks in the stock markets.

In the UK, we will get more details about what drove economic growth in Q4 with the second release of GDP growth.

Also in the UK, Theresa May and her most senior cabinet ministers will meet to try and agree on a Brexit trade deal that they want with the EU in the post -Brexit future. This will be a litmus test for the UK Prime Minister as her cabinet still appears to be divided between those who want a soft and a hard Brexit .

Overnight , we will get January inflation figures for Japan. Inflation has been ticking upwards over the past year but it has been driven primarily by energy prices. The underlying price pressure in Japan remains very low. Recently, according to IHS Markit data, prices charged by both the service and the manufacturing sector have risen. It will be interesting to see whether these figures will also induce higher consumer prices.

Selected market news

The Fed minutes of the January FOMC meeting released last night have set the tone in financial markets over night. The minutes revealed that the FOMC has become more upbeat on near-term growth compared to December, seeing bigger potential for the tax reform to boost growth than estimated previously and the strong rises in equity prices at the beginning of the year (the meeting took place before the equity market correction began in early February). However, FOMC members expected inflation to rise this year, despite the still muted inflation and wage growth. In our view, the minutes did not suggest the Fed will be inclined to raise its rate hike expectations to four from three hikes this year. We expect the Fed to hike the interest rate at the next meeting in March. At this meeting it will be interesting to see how the Fed factors in the additional fiscal loosening from the budget deal and higher wage and inflation data. We may already get some signals when new Fed Chair Jerome Powell testifies on the central bank's semi-annual report on monetary policy and the economy in the US congress on 28 February.

On the back of the minutes, the US stock market reversed gains and bond yields . The S&P 500 Index ended the day down 0.6% after being up as much as 1.2% earlier. The yield on 10- year Treasuries rose to 2.94%, which is the highest in four years. This morning, Asian markets are following suit , with the Nikkei down over 1%. The only exception is the Chinese stock markets, which is reopening after a five-day break for the Chinese Lunar New Year. Most Asian currencies are also losing ground against the USD, except for the Japanese yen, which is seeing support from the higher risk aversion in the market .

Market Update – Asian Session: Regional Currencies Weaker On USD Strength

Headlines/Economic Data

General Trend:

Asian equity markets trade mixed after earlier weakness in US markets

Shanghai Composite opens higher upon return from Lunar New Year break

Chinese cobalt producers rise as Apple is speculated to consider direct purchases from miners

Qantas and Air New Zealand rise after earnings reports

Yen trades broadly higher: USD/JPY declines amid selling in the Yen crosses

PBoC injects cash in first OMO since before the Lunar New Year break

Japan

Nikkei 225 opened -0.8%; closed -1.1%

Topix Iron& Steel Index -2.3%, Securities -1.5%, Electric Appliances -1.3%, Real Estate -1.3%

Japanese automakers trade generally lower as the Yen strengthened

Ricoh [7752.JP]:Declines over 4% amid press speculation related to possible impairment loss

(JP) Japan PM Adviser Hamada: Reiterates BoJ should consider buying foreign bonds - US financial press

(JP) Japan Cabinet Office (Gov’t) Monthly Economic Report for February:Maintains its overall assessment , economy is recovering gradually(yesterday after close)

(JP) Japan MoF sells ¥1.0T v ¥1.0T indicated in 0.60% (prior 0.60%) 20-yr bonds; avg yield 0.5610% v 0.592% prior; bid to cover 4.44x v 4.17x prior

Looking Ahead: Japan Jan CPI data due to be released on Friday

Korea

Kospi opened -0.5%

(KR) South Korean brokerages expect Bank of Korea(BOK) rate hike in May and leave rate unchanged next week - Korean press

(KR) South Korea Q4 Household Credit (KRW): 1.45T v 1.42T prior; Household Debt y/y: 8.1% v 9.5% prior

(KR) North Korea to have official visit to the South On Feb 25th - Korean press

China/Hong Kong

Hang Seng opened -1.1%, Shanghai Composite +1.2%

Shanghai Property Index rises over 1%

Hang Seng Financials Index -1.3%, Energy -1.1%, Information Tech -0.9%, Property/Construction-0.9%

(CN) China Jan Swift GlobalPayments (CNY) 1.7% v 1.5% prior

(CN) China PBOC OMO: Injects CNY350B in 7,28 and 63-day reverse repos v skipsprior (1st injection after 16 consecutive skips)

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3530 V 6.3428 PRIOR

(US) Treasury undersecretary Malpass accuses China of “patently non-market behavior”; US needs a stronger response to counter it - press

(CN) According to China National Tourism Administration (CNTA) Lunar New year tourism totaled CNY475B, +12.6% y/y - Xinhua

(CN) Chinese companies are being forced to halt trading as their owners attempt to unwind loans collateralized with stocks - FT

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.1%

ASX 200 Utilities Index -2.4%, REIT -1.3%, Financials -0.2%; Consumer Discretionary +1.1%

Qantas, QAN.AU Reports H1 (A$)Net 607M v 515M y/y, Pretax 976M v 852M y/y; Rev 8.66B v 8.18B y/y;Announces On-market share buy-back of up to A$378M

CrownResorts, CWN.AU Reports H1 (A$) Net 192.4M v 175Me; EBITDA 447.7M v 448Me; Rev 1.80B v1.7Be; to buyback 29.3M shares

Viralytics [+175.2%], VLA.AU To be acquired by Merck forA$1.75/shr valued at A$502M

Air New Zealand [+4%],AIR.NZ Reports H2 (NZ$) NPAT 232M v 229Me, Rev 2.7B v 2.7Be; raisesdividend

(NZ) New Zealand sells NZ$150M in 3.5% 2033 bonds; avg yield 3.3421%

(AU) Australia sells A$500M v A$500M indicated in June 2018 notes, avg yield1.6924%, bid to cover 6.06x

(NZ) New Zealand Jan Credit Card Spending M/M: -0.6% v 0.6% prior; Y/Y: 4.6% v6.3% prior

Looking Ahead: New Zealand Q4 Retail Sales data due for release on Friday

Other Asia

(PH) Philippines updates CPI base year to 2012 from 2006

(TH) Thailand Central Bank Gov Veerathai: The economy can weather volatile capital flows, economic fundamentals are strong; no need to rush to raise rates

North America

US equity markets ended mostly lower: Dow -0.7%, S&P500 -0.6%, Nasdaq -0.2%, Russell 2000 +0.1%

S&P500 Real Estate -1.8%, Energy -1.7%

(US) Chair of the Council of Economic advisers Kevin Hassert: Sees 2018 GDP at 3% of which 0.8% per year of growth to the president's policies - US media

ROKU Reports Q4 +$0.06 v -$0.11e,Rev $188.3M v $183Me;-22% after hours

MLNX Guides Q1 Rev $240-250M v$227Me; Non-GAAP gm's 68.5-69.5%; CFO resigns; +11% after hours

(US) FOMC MINUTES FROM JAN 31 MEETING: MAJORITY SAW STRONGER GROWTH LIFTING LIKELIHOOD OF FURTHER HIKES;Almost all Fed officials see inflation rising to 2% goal

(US) Fed's Kashkari (dove, non-voter): US economy is doing very well, surprised at confidence and optimism due to tax cut, not sure how much of a long term difference tax cut will make

(US) Fed’s Harker (non-voter, moderate): US inflation to hit or exceed 2% goal by end of 2019;Reiterates he sees two 2018 rate hikes as appropriate

(US) Fed's Quarles (hawk, FOMC voter): Economy is performing well; current policy remains accommodative, gradual rate increases are appropriate

(US) TREASURY'S $35B 5-YEAR NOTE AUCTION DRAWS: 2.658%; BID-TO-COVER RATIO: 2.44 V 2.48 PRIOR AND 2.45 OVER THE LAST 12 AUCTIONS

(US) Weekly API Oil Inventories: Crude: -0.9M v +3.9M prior

Looking Ahead: Canada Dec Retail Sales and US Weekly DoE Crude Oil Inventories to be released; Fed’s Dudley expected to speak in NY morning; Other Fed speakers expected include Bostic

Europe

(DE) German FinanceMinistry Feb Report: Jan Tax Rev +2.8% y/y; No end in sight for German economicexpansion

(GR) Moody's raises Greece sovereign rating two notches to B3 from Caa2;outlook Positive

(UK) Reportedly the PM May's Cabinet did not agree to her negotiating strategy for the Brexit transition period - UK Telegraph

(UK) Govt spokesperson: UK continues to see 2 year Brexit transition period, while EU is saying 21 months

(DE) ZEW raises concern about higher EU contribution by Germany – European Press

Looking Ahead: Germany Feb Ifo Survey due for release, along with second reading of UK Q4 GDP

ECB to also publish monetary policy meeting minutes

Levels as of 01:00ET

Nikkei225 -1.1%, Hang Seng -0.8%; Shanghai Composite +2.2%; ASX200 +0.1%, Kospi -0.6%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.5%,Dax -0.1%; FTSE100 -0.1%

EUR 1.2344-1.2300; JPY107.77-107.15; AUD 0.7809-0.7790;NZD 0.7321-0.7308

Apr Gold -0.5% at $1,326/oz; Apr Crude Oil -0.9% at $61.12/brl; Mar Copper -1.0% at $3.17/lb

Aussie Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.83% against the USD and closed at 0.7801.

LME Copper prices declined 0.3% or $24.0/MT to $7003.0/MT. Aluminium prices declined 2.2% or $49.0/MT to $2190.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7798, with the AUD trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7766, and a fall through could take it to the next support level of 0.7735. The pair is expected to find its first resistance at 0.7854, and a rise through could take it to the next resistance level of 0.7911.

With no macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Manufacturing Sector Activity At A 4-Month Low In February, While Germany’s Manufacturing Sector Growth Weakest Since August 2017...

For the 24 hours to 23:00 GMT, the EUR declined 0.45% against the USD and closed at 1.2280, following a slew of downbeat economic releases across the Euro-zone.

Data revealed that the Euro-zone's preliminary Markit manufacturing PMI dropped more-than-expected to a level of 58.5 in February, hitting its lowest level in 4 months. In the prior month, the PMI had registered a level of 59.6, while investors had envisaged for a fall to a level of 59.2.

Moreover, the region's flash Markit services PMI registered a 2-month low level of 56.7 in February, compared to market expectations for a fall to a level of 57.6. In the previous month, the PMI had registered a reading of 58.0.

Separately, growth in Germany's manufacturing sector cooled to a level of 60.3 in February, expanding at its weakest pace in 6 months. Market anticipation was for the PMI to ease to a level of 60.5, after registering a reading of 61.1 in the prior month. Additionally, the nation's services sector activity eased more-than-anticipated to a level of 55.3 in February, marking its slowest pace of growth in 3 months. The PMI had registered a level of 57.3 in the prior month, while markets were expecting for a drop to a level of 57.0.

The greenback advanced against its major peers, following upbeat minutes of the Federal Reserve's (Fed) January meeting.

As per the minutes, officials painted an upbeat picture of the US economy and were increasingly optimistic on reaching their 2.0% inflation target over the medium term. Further, many officials upgraded their economic growth forecasts and pointed to the recent tax cuts as well as the improved global economic outlook as factors contributing to the US economic growth this year. Additionally, committee members shared the view that a strengthening economy supported future gradual interest rates hikes, while cautioning that the impact of the tax cuts is not yet clear.

Gains in the US Dollar were boosted further, after macroeconomic data revealed that activity in the US manufacturing sector recorded an unexpected rise to a level of 55.9 in February, accelerating by the most in over 3 years, thus highlighting a solid upturn in business conditions. In the previous month, the PMI had recorded a level of 55.5, while market participants had expected for an unchanged reading. Moreover, the nation's services sector growth surged to a 6-month high level of 55.9 in February, beating market anticipations for a rise to a level of 53.7. the PMI had registered a level of 53.3 in the previous month.

Other economic data indicated that existing home sales in the US surprisingly eased 3.2% on a monthly basis to a level of 5.38 million in January, defying market expectations for a rise to a level of 5.60 million. Existing home sales had registered a revised reading of 5.56 million in the previous month. Also, the nation's MBA mortgage applications fell 6.6% in the week ended 16 February, following a drop of 4.1% in the previous week.

In the Asian session, at GMT0400, the pair is trading at 1.2276, with the EUR trading a tad lower against the USD from yesterday's close.

The pair is expected to find support at 1.2241, and a fall through could take it to the next support level of 1.2205. The pair is expected to find its first resistance at 1.2336, and a rise through could take it to the next resistance level of 1.2395.

Ahead in the day, traders would keep a close watch on the European Central Bank's (ECB) latest meeting minutes as well as Germany's Ifo business climate and expectations indices for February. Moreover, the US initial jobless claims followed by the leading index for January, slated to release later in the day, would attract a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.