Sample Category Title

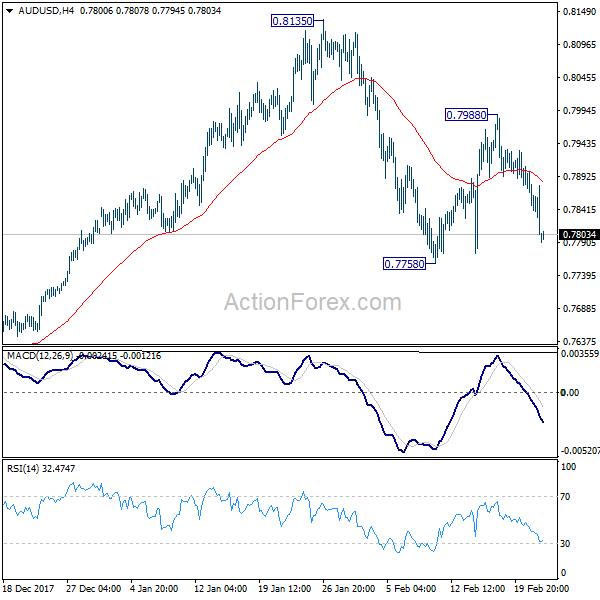

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7770; (P) 0.7834; (R1) 0.7867; More...

At this point, AUD/USD is staying in range of 0.7758/7988. Intraday bias remains neutral. On the upside, above 0.7988 will extend the rebound to retest 0.8135. On the downside, below 0.7758 will resume the fall from 0.8135 and target 0.7500 key near term support. At this point, there is no strong case for a range breakout yet and 0.7500/8135 could hold for a while.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

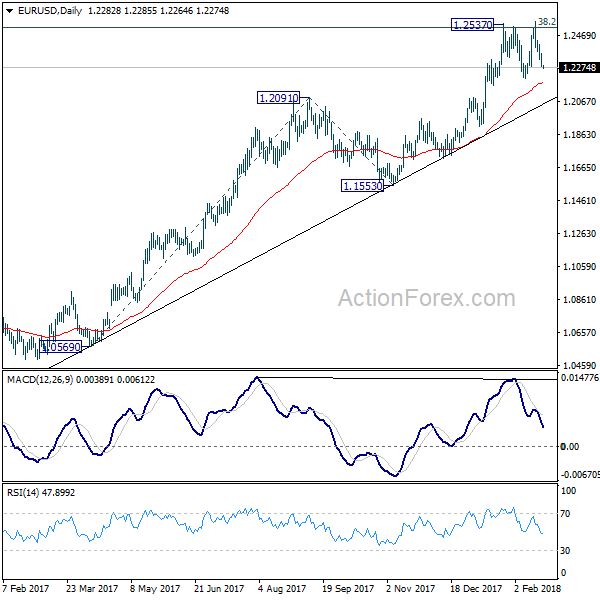

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2255; (P) 1.2307 (R1) 1.2335; More....

EUR/USD is still staying in range above 1.2205 support and intraday bias remains neutral. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

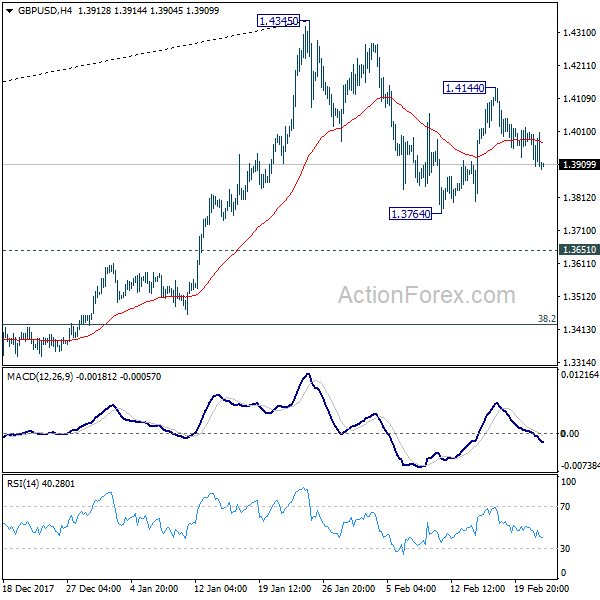

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3876; (P) 1.3942; (R1) 1.3981; More....

Intraday bias in GBP/USD remains neutral as it's bounded in range of 1.3764/4144. On the upside, break of 1.4144 will extend the rebound from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

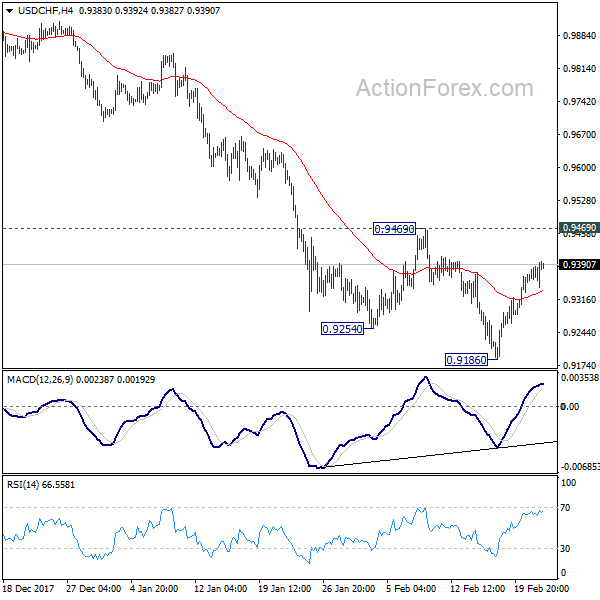

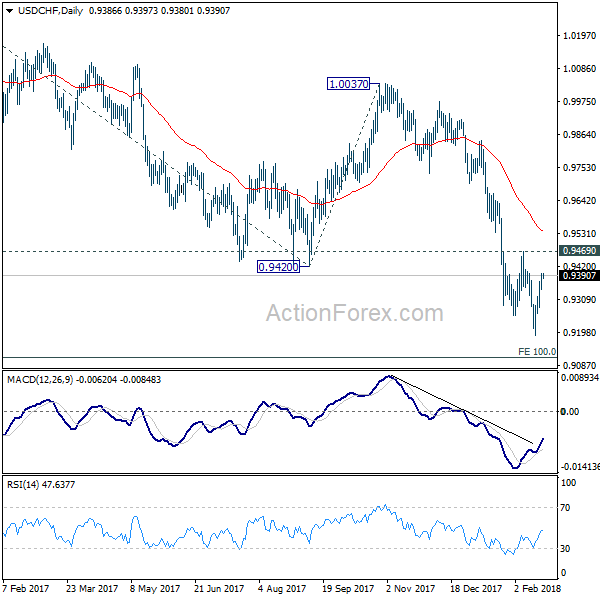

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9356; (P) 0.9376; (R1) 0.9410; More...

While there rebound from 0.91863 is strong, USD/CHF is limited below 0.9469 near term resistance. Such rebound is still viewed as a corrective move. Intraday bias remains neutral and outlook stays bearish for another decline. Break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9541) and above.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

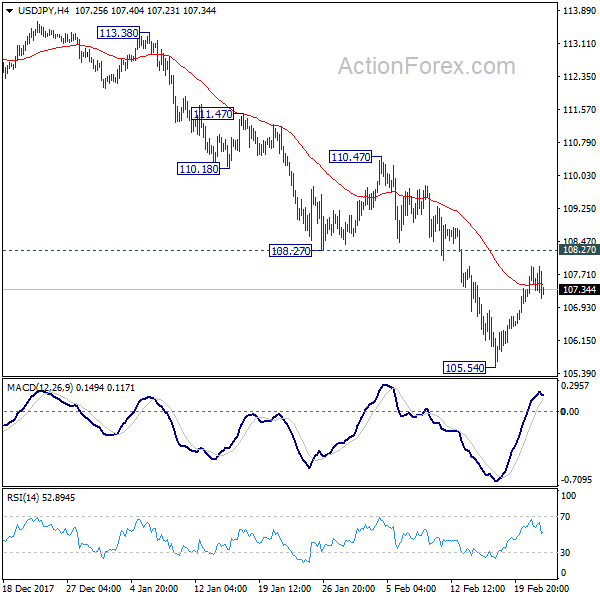

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.39; (P) 107.64; (R1) 108.03; More...

No change in USD/JPY's outlook. While the rebound from 105.54 is strong, it's limited below 108.27 support turned resistance. Such rebound is seen as a corrective move. Intraday bias stays neutral and near term outlook remains bearish. Below 105.54 will extend the larger fall from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 107.72 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Dollar Jump on FOMC Minutes, But Still Held Below Near Term Resistance Levels

Dollar jumps overnight after hawkish FOMC minutes and remains the strongest one for the week. Nonetheless, the greenback is paring some gains in Asian session. And it's still limited below key near term resistance against most major currencies, except versus Canadian Dollar. Markets sentiment have shifted much since the start of the year. Back then, most doubted whether Fed would really hike three times this year. After a string of solid data and yesterday's minutes, traders are now talking whether Fed could hike more than four times. US treasury jumped on such expectations while stocks reversed some of recent rebound. DOW ended the day down -0.67% at 2479.78. For now, it remains to be seen whether Dollar would finally re-couple with yields.

FOMC minutes affirmed more hikes ahead

Minutes of the January 30-31 FOMC meeting affirmed the Fed's hawkish stance. The key take away is that "a majority of participants noted that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate. Growth remained "above trend" while labor market "stayed strong". And there are "upside risks" to growth because of the tax cuts. Meanwhile, "almost all participants" expected inflation to move up to the 2% target over the "medium term".

It should be noted that the meeting was held before January non-farm payroll report and CPI release. NFP showed stronger than expected wage growth at 0.3% mom. CPI jump a strong 0.5% mom while core CPI rose 0.3% mom. The developments could prompt Fed to turn even more hawkish ahead.

Treasury yields extended recent rally after the FOMC minutes. 10 year yield reached as high as 2.943 and hit the highest level since 2014. Recent up trend in TNX is on track for 3.036 key resistance. We'd like to reiterate that the zone between 3.036 and 100% projection of 1.336 to 2.621 from 2.034 at 3.318 is the long term trend redefining area. A solid break above will declare we've finally exited the low interest rate era.

BoE Haldane: Wage growth could jump above 3%

BoE Chief Economist Andrew Haldane told Parliament Treasury Committee that wage growth will pick up amid record low unemployment. He said that "the long-awaited -- and we have been waiting for a long time -- pickup in wages is starting to take root." And, "We get intelligence from our agents that would suggest that wage settlements this year were going to pick up, perhaps to a number with a three in front of it, rather than a two in front of it." Also, risks for the UK economy were "to the upside". Nonetheless, neither Haldane, nor Governor Mark Carney, gave any hint on the timing of the next rate hike.

Looking ahead

ECB minutes will be the main focus of the day. The central bank has hinted at tweaking its forward guidance regarding the asset purchase program. But nonetheless was done so far. The markets would like to know what were being discussed during the meeting regarding this topic, for gauging the chance of ending the APP after September.

In addition, Germany will release Ifo business climate in European session. UK will release Q4 GDP revision, index of services and CBI reported sales.

Later in the day Canadian Dollar will take center stage with retail sales featured. US will release jobless claims and leading index.

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.39; (P) 107.64; (R1) 108.03; More...

No change in USD/JPY's outlook. While the rebound from 105.54 is strong, it's limited below 108.27 support turned resistance. Such rebound is seen as a corrective move. Intraday bias stays neutral and near term outlook remains bearish. Below 105.54 will extend the larger fall from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 107.72 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | German IFO Business Climate Feb | 117 | 117.6 | ||

| 09:00 | EUR | German IFO Expectations Feb | 107.9 | 108.4 | ||

| 09:00 | EUR | German IFO Current Assessment Feb | 127 | 127.7 | ||

| 09:30 | GBP | GDP Q/Q Q4 P | 0.50% | 0.50% | ||

| 09:30 | GBP | Index of Services 3M/3M Dec | 0.50% | 0.40% | ||

| 11:00 | GBP | CBI Reported Sales Feb | 14 | 12 | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (17 FEB) | 231K | 230K | ||

| 13:30 | CAD | Retail Sales M/M Dec | -0.10% | 0.20% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Dec | 0.00% | 1.60% | ||

| 15:00 | USD | Leading Index Jan | 0.70% | 0.60% | ||

| 15:30 | USD | Natural Gas Storage | -194B | |||

| 16:00 | USD | Crude Oil Inventories | 1.8M |

Can Crude Oil Price Break This Crucial Resistance Post FOMC?

Key Highlights

- Crude oil price found support around $58.00 after the last decline and recovered against the US dollar.

- There is a crucial resistance zone forming near $63.00 on the 4-hours chart of XTI/USD.

- The price needs to break the $63.00 resistance to gain upside momentum towards $65.00-66.00.

- The US Manufacturing PMI in Feb 2018 (Preliminary) increased to 55.9 from 55.5.

Crude Oil Price Technical Analysis

During the start of February 2018, there was a major decline in crude oil price against the US dollar. Later, the price found support near $58.00 and started a fresh upside move.

Looking at the 4-hours chart of XTI/USD, the price recovered above the $59.20 and $60.00 resistance levels. It even traded above the 50% Fibonacci retracement level of the last decline from the $66.30 high to $58.08 low.

However, the price is now facing an uphill task near the $63.00 level. The stated $63.00 is near the 200 simple moving average (green, 4-hours). An immediate resistance is around a bearish trend line at $62.40 on the same chart.

The trend line resistance at $62.40 is positioned with the 100 simple moving average (red, 4-hours). Therefore, it won’t be easy for buyers to break the $62.40-63.00 resistance region.

On the downside, an initial support is around the 50% Fib retracement level of the last wave from the $58.08 low to $62.75 high at $60.41. Below $60.40, the price could retest the $60.00 level.

US Manufacturing PMI and FOMC Meeting Minutes

Recently in the US, the FOMC meeting minutes were released. The minutes highlighted a strong growth in the US throughout 2018 and further rate hikes. The overall sentiment favored the greenback after the release, and pushed the US Dollar higher.

Moreover, the Manufacturing Purchasing Managers Index (PMI) for Feb 2018 (Preliminary) was released by the Markit Economics. The market was looking for a minor decline in the PMI from 55.5 to 55.4.

However, the actual reading was positive as there was an increase in the PMI from 55.5 to 55.9. Commenting on the report, the Chief Business Economist at IHS Markit, Chris Williamson, stated:

Business activity growth accelerated markedly in February, suggesting the economy is growing at its fastest pace for over two years. The upbeat February PMI surveys are indicative of GDP rising at an annualised rate of 3.0%.

In short, the market sentiment is positive and the US dollar could gain further momentum versus other major currencies such as the Euro, British Pound and the Japanese Yen.

USD/JPY recently recovered above the 107.00 level and is currently showing positive signs. On the other hand, EUR/USD broke a major support at 1.2380 and is currently trading in a bearish zone.

Market Morning Briefing: Gold Is Testing Immediate Support At Current Levels

STOCKS

Almost all stock indices except Shanghai are weak globally. A corrective dip is likely in place and may continue for a couple of sessions before recovering.

Dow (24797.78, -0.67%) seems to be holding well below the 21-day MA on the daily line charts as mentioned yesterday. While the downside momentum continues, a test of 24500-24000 looks possible in the coming sessions.

Dax (12470.49, -0.14%) was almost stable yesterday. We look at resistance near 12600 to hold in the medium term. We repeat, trade within 12600-12300 is likely for the coming sessions.

Nikkei (21712.20, -1.18%) could come off a bit in the near term to re-test support near 21200-21000. Overall 21000-22500 region is likely to hold in the medium term before the index tries to move up. Looking at the long term channel support, the index has scope on the upside for the longer run.

Shanghai (3251.35, +1.63%) opened with a gap up today after a week long holiday. Note immediate resistance near 3260-3270 region. A break above 3060-3070 could take it higher towards 3300-3350 in the near term. View is bullish for the coming sessions.

Both Nifty (10397.45, +0.36%) and Sensex (33844.86, +042%) were slightly up yesterday almost trading along the support region. It would be important to see if the indices sustains to remain above the support or breaks sharply on the downside. The next 2-sessions may be spent quietly but going into next week some weakness is likely to come in.

COMMODITIES

WTI (60.99) has come off a bit while Brent (64.85) remains stable at levels seen yesterday. There is some scope on the downside for WTI to test 60-59 again in the coming sessions while resistance near 63 holds. Brent is likely to remain stable but also has some scope of falling towards 64.

Gold (1326) is testing immediate support at current levels. If the price falls below 1325, it could be vulnerable to eventually test 1315-1310 on the downside. Sustenance above 1325 is necessary to keep the possible upside intact for the medium term. Else we may have to start looking at more downside levels for the medium term.

Copper (3.1675) is trading lower but could face some support near 3.12-3.15 region. If that holds, the price could again start moving up from there; else a test of 3.10-3.07 would be the next target on the downside.

FOREX

As expected, the Dollar Index (90.063) is testing resistance on daily candles near 90.1-90.2. Resistance on weekly candles is slightly higher near 90.3-90.4, which might also be tested in the next couple of sessions in the aftermath of heightened inflation expectations and rising yields, triggered by the US Fed minutes release yesterday (see Interest rates below). However, a rise beyond 90.3-90.4 might be difficult and we could see a dip from those levels.

As per expectations, Euro (1.2278) is testing lower support near 1.2275-1.2265 on the daily candles (which is also seen as crucial support on weekly candles). We might see a false break of support on weekly candles towards 1.221-1.223 as was seen in the previous 2 weeks, but a further downmove might be unlikely.

The Dollar-Yen (107.34) saw a high of 107.90 yesterday, just below resistance near 108 on the daily candles and is now seeing a slight dip. On previous 2 instances when support on weekly candles was tested, the Dollar Yen saw 4 consecutive weeks of upmoves. We are almost through the 1st week of upmove after the most recent test of support – it would be interesting to see if the previous pattern is again followed next week.

The Euro-Yen (131.80) against our expectations has broken below 132 but might now find support near 131.5 on the daily candles – since chances of Euro breaking below 1.221-1.223 are low and the Dollar Yen might just see a bullish week again, the Euro yen could stay above 131.50.

Pound (1.3909) as per earlier expectation is now testing immediate support near 1.39 on the daily candles. A further dip to lower support near 1.38 on daily and 3 day candles might now happen next week.

Dollar-Rupee (64.76): Likely to test support near 64.60/50 before again bouncing back towards 65 or higher in the medium term.

INTEREST RATES

Yesterday’s US Fed minutes have reinforced the market’s belief of 3 to 4 rate hikes this year, which in turn has further pushed US yields up. The ongoing treasury auctions are also adding to the supply of US debt and putting upward pressure on yields.

US 10 Year Yield (2.9335), US 30 year Yield (3.2028), US 5 year yield (2.6566), US 2 year yield (2.258) : After the auction of US 2 Year notes (fetching yield rates near 2.255%) pushed up the 2 year yield yesterday, the 10 year and 30 year yields have risen by 4 to 5 bps after the release of the Fed minutes. The 30 year yield is hovering around our earlier mentioned long term resistance level of 3.20% while the 10 year yield saw a record high (2.95%) above the resistance level (2.9%) and is currently trading around 2.93-2.94%.It had risen to 2.93% last week as well, post which it dipped below 2.9% again.

However, given that there is further auctioning slated in this week for the 5 year notes, we could expect some more volatility for the 10 year above 2.9%. However, as mentioned previously as well, there is a strong possibility of high yield levels attracting investors towards US debt and thereby pushing down yields from current levels. After this week’s volatility, we might well see another few sessions of consolidation next week..

(Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

FOMC Meeting Minutes Suggest More Rate Hikes Ahead

Participants of the late-January meeting round believed that the economy continued to grow at an above-trend pace from mid-December through late-January, generally revising up their economic projections since then.

The Committee viewed the impacts of tax cut as though it "might be somewhat larger in the near term than previously thought".

FOMC members viewed the labor market in a positive light, with solid job gains and a jobless rate measure that is near a two-decade low. Moreover, they suggested that broader measures of slack were returning to pre-recession levels.

Wage pressures were quoted by several participants but broad based moves remained absent. Moreover, some participants believed that the TCJA-related payments to employees could materialize in bonuses or other one-time payments and not become permanent.

Discussions on inflation generally pointed to expectations for gradual increases, with some already suggesting that some were already able to raise prices due to rising costs. However, participants also said that the TCJA may lead firms to cut prices to remain competitive, posing some downside risk.

Participants concluded that "upside risks" had increased due to tax cuts, increased consumer spending, and improving global growth, with only a 'couple' worried about economy.

A majority of participants believed that the improved outlook for growth "raised the likelihood that further gradual policy firming would be appropriate."

Key Implications

In her last meeting as Chair, Janet Yellen passed the economic baton to Jerome Powell. And what a baton it is, with unemployment near two-decade lows, solid growth momentum, additional fiscal stimulus on the way, healthy global growth, and nascent signs of wage and inflation pressures.

In fact, it would appear that the economy is almost too healthy for its own good, particularly in light of the fiscal stimulus coming online this year. From this viewpoint, Chair Powell and team will have their hands full, as they try to analyze every bit of information for signs of economic overheating.

All in all, the Fed minutes suggest that the improved outlook raised the likelihood of further gradual policy firming, corroborating the sentiment in the Fed statement itself which added the word "further" to the text. While March is not a done deal, it would take some pretty dreadful data to derail a 25 basis point hike – making Powell one-for-one should it materialize.

Confusion Reigns

Confusion reigns

In a market starved for significant news, the FOMC minutes provided just enough talking points to keep the dollar bid as US bond yields nudged towards crucial resistance levels.However, the Feds assortment of views on wage growth suggests the FOMC remains pliable during the transition phase from Yellen to Powell. In other words, the Feds stay in wait and see mode regarding inflation.

Of course, the market latched on to the dovish stuff as traders were partial to sell the dollar, but as is so often the case when interpreting the Feds exercise in verbal gymnastics, the market got it wrong. The FOMC minutes were eventually deemed slightly more hawkish after suggesting economic growth will surpass their estimates which caused STIRT traders to nudge rate hike expectations higher through 2018 and providing a bump to dollar sentiment. But given the lack of follow-through, the jury remains out.

The exciting part of the equation today will be the return of China investors which should provide a spark to regional sentiment. But the jury is out on the currency markets and in particular USDJPY which remains the primary vehicle to express currency sentiment.

So there lies the debate, interest rate hawks preach the FOMC had not seen last week’s sharp inflation report while the doves suggest a need for a string of convincing inflation prints before moving to the four rate hike camp.

Bond Markets

The bond market is confused, but as my first boss on the BondDesk was always quick to remind me, when in doubt Sell.

Oil prices

Tumbling oil prices got a reprieve at the end of the day after American Petroleum Institute data showed a drop of 0.907 million barrels in US crude inventories. Given all the noise about a shale production ramp, Traders were expecting an increase in the warehouse when in reality improved pipeline infrastructure to the Gulf coast and the decreased supply via TransCanada’s Keystone pipeline, sent Cushing inventories tumbling.But the firming dollar continues to thwart investor sentiment despite the bullish inventory data. By no means is the dollar returning to form so this upbeat inventory data could have some legs.

Gold Prices

It was a meltdown in Gold markets overnight, and I’m not talking about scrap prices. But in reality, this should provide Gold investors with another opportunity to re-engage as the Fed fell well short of confirming a 4th rate hike in 2018. The minutes were more balanced in my view as the recent uptick in volatility will have as much bearing on Fed policy decision as the subtle rise in inflation.

G-10

The Euro

Disappointing price action from the long perspective continues to weigh on sentiment; bullish views continue to be challenged ahead of the Italian elections, as near-term convictions turn neutral to slightly bearish

The Japanese Yen

There remain substantial offers between 107.50-108 levels that are providing a cap on USDJPY, but Traders remains exceptionally cautious in either direction despite increasing signals for a structural demise in USD sentiment.While fiscal stimulus looks good on paper, we’re entering uncharted territory as the Fed pares back bond purchases while the Treasury issues absurd amounts of debt.

Malaysian Ringgit

We should anticipate more liquidity coming back to the market as mainland investor return. While we’re nowhere near a make or break scenario for the Ringgit, short-term sentiment remains tarnished by an unexpectedly faster rise in US bond yields. While this is mildly negative for local opinion, the main issue is investors are growing increasingly concerned about a quicker pace of interest rate normalisation from the Fed which could trigger regional capital outflow.

The FOMC minutes served up little more than a plate of confusion last night, so I expect G-10 along with Asia FX to remain in a state of limbo until Fed Chair Powell takes the podium later this month.