Sample Category Title

Sterling Drops on Unexpected Rise in Unemployment Rate, Dollar Firm ahead of FOMC Minutes

Dollar stays firm and is trading broadly higher going into US session. FOMC minutes will be closely watched later in the session. But it's unsure how much boost the hawkish Fed could give Dollar. For the moment, the greenback is staying below near term trend definite resistance against all other major currencies despite this week's rebound. That is, Dollar remains in down trend and the rebound is viewed as a correction only. Elsewhere in the currency markets, Sterling is trading broadly lower as job data showed first rise in unemployment rate since 2016. Wage growth met expectation but stayed below inflation.

UK unemployment climbed for first time since 2016

UK jobless claims dropped -7.2k in January, better than expectation of 2.3k. However, unemployment rate rose to 4.4% in the three months to December, above expectation of 4.3%. That's the first rise in unemployment rate since August 2016. Unemployment jumped 46k in the final quarter of 2017, sharpest increase in almost five years. Average weekly earnings grew 2.5% 3moy, in line with consensus. However, wage growth continued to be lower than inflation. Also from UK, public sector net borrowing dropped to GBP -11.6b in January.

ECB Vasiliauskas: Nobody expects sudden end to asset purchase

ECB Governing Council member Vitas Vasiliauskas said that recent rise in Euro is "quite a normal reaction". And, "it's the outcome of the strong euro zone economy." Also, "the economy is improving and markets expect higher inflation in the medium term". Regarding the asset purchase program, Vasiliauskas said "nobody expects a scenario with a sudden end to the programme. Especially having in mind the experience of other central banks. You don't want to take steps forward then back, so we should be careful in making (a) decision."

Eurozone PMI showed mild cooling in expansion

Eurozone PMI manufacturing dropped to 58.5 in February, down from 59.6 and missed expectation of 59.2. Eurozone PMI services dropped to 56.7, down from 58, missed expectation of 57.6. Germany PMI manufacturing dropped to 60.3, down from 61.1, missed expectation of 60.5. Germany PMI services dropped to 55.3, down from 57.3, missed expectation of 57.0. France PMI manufacturing dropped to 56.1, down from 58.4, below expectation of 58.0. France PMI services dropped to 57.9, down from 59.2, missed expectation of 59.0.

Markit noted that "Eurozone business activity continued to rise at a steep pace in February, albeit with the rate of expansion cooling from the near 12-year high recorded in January." Regarding Germany, Markit noted that "while February's flash PMI figure was down on January's recent high, it still continued to point to a robust pace of private sector expansion in the Eurozone's largest economy." Regarding France, Markit also noted that "private sector growth in France shifted down a gear in February, with the rate of expansion in output and new orders each hitting four-month lows."

Japan PMI: Yen appreciation dragged export growth

Japan PMI manufacturing dropped to 54.0 in February, down from 54.8 and missed expectation of 55.2. In particular, new export orders index dropped notably from 57.4 to 54.0, hitting the lowest level in three months. Markit noted in the release that "recent yen appreciation has coincided with slower new export order growth." Also, "a number of panelists indicated that the stronger currency had prompted them to lower prices to overseas customers." And, "further yen strengthening will create unwanted drag on inflationary pressures". Also from Japan, all industry activity index rose 0.5% mom in December.

FOMC minutes to turn more hawkish

It's generally believed that minutes of the January 30-31 FOMC minutes would show a hawkish twist in the languages The questions is just on the extent. Recent solid data, including job and inflation, are solidifying the case for three rate hikes this year. And markets would now wand to see if more board members are starting to considering four hikes. That would also be tied to policymakers' view on the impact of the tax reform. In addition, markets will look at whether Fed officials are getting more comfortable with the inflation outlook.

Dollar has so far received no support from surging treasury yields, Fed hike expectation, nor the tax reform this year. There is doubt on whether the FOMC minutes could give the greenback sustainable strength. We'll keep an eye on it.

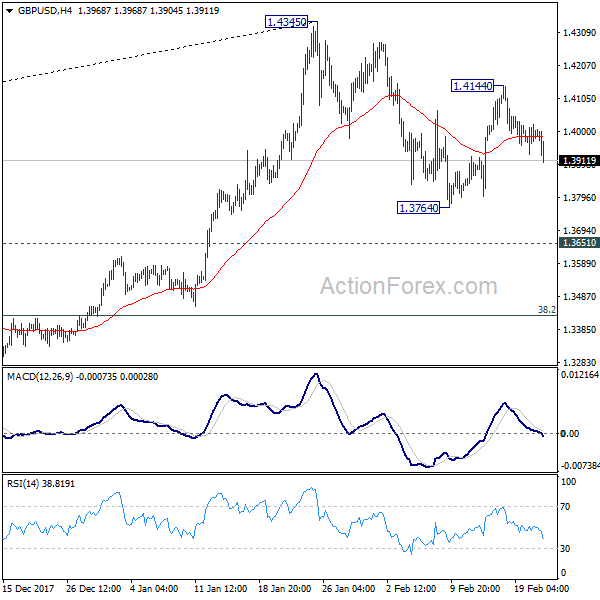

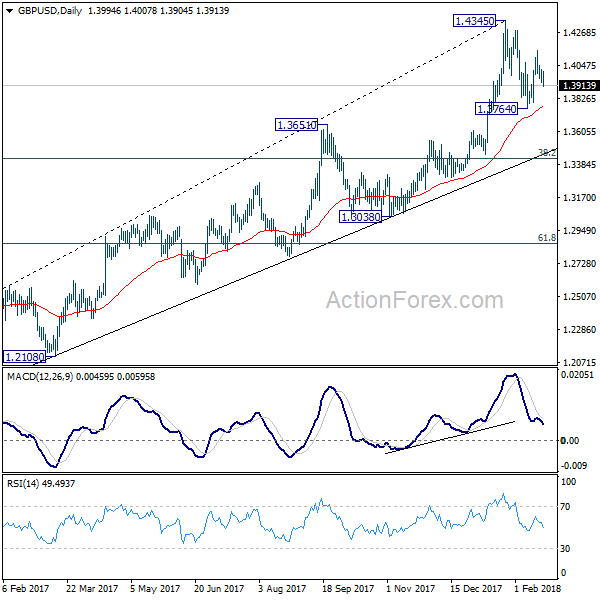

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3942; (P) 1.3983; (R1) 1.4036; More....

GBP/USD's fall from 1.4144 extends lower today but it's so far staying in range of 1.3764/4144. Intraday bias remains neutral first. On the upside, break of 1.4144 will extend the rebound from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Wage Price Index Q/Q Q4 | 0.60% | 0.50% | 0.50% | |

| 0:30 | AUD | Construction Work Done Q4 | -19.40% | -10.00% | 15.70% | 16.60% |

| 0:30 | JPY | PMI Manufacturing Feb P | 54 | 55.2 | 54.8 | |

| 4:30 | JPY | All Industry Activity Index M/M Dec | 0.50% | 0.40% | 1.00% | |

| 8:00 | EUR | France Manufacturing PMI Feb P | 56.1 | 58 | 58.4 | |

| 8:00 | EUR | France Services PMI Feb P | 57.9 | 59 | 59.2 | |

| 8:30 | EUR | Germany Manufacturing PMI Feb P | 60.3 | 60.5 | 61.1 | |

| 8:30 | EUR | Germany Services PMI Feb P | 55.3 | 57 | 57.3 | |

| 9:00 | EUR | Eurozone Manufacturing PMI Feb P | 58.5 | 59.2 | 59.6 | |

| 9:00 | EUR | Eurozone Services PMI Feb P | 56.7 | 57.6 | 58 | |

| 9:30 | GBP | Jobless Claims Change Jan | -7.2K | 2.3K | 8.6K | |

| 9:30 | GBP | Claimant Count Rate Jan | 2.30% | 2.40% | ||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Dec | 2.50% | 2.50% | 2.50% | |

| 9:30 | GBP | ILO Unemployment Rate 3Mths Dec | 4.40% | 4.30% | 4.30% | |

| 9:30 | GBP | Public Sector Net Borrowing Jan | -11.6B | -11.0B | 1.0B | |

| 14:45 | USD | US Manufacturing PMI Feb P | 55.5 | 55.5 | ||

| 14:45 | USD | US Services PMI Feb P | 54 | 53.3 | ||

| 15:00 | USD | Existing Home Sales Jan | 5.63M | 5.57M | ||

| 19:00 | USD | FOMC Meeting Minutes |

Canadian Dollar Subdued Ahead of Fed Minutes

The Canadian dollar has recorded slight losses in the Tuesday session. Currently, USD/CAD is trading at 1.2669, up 0.16% on the day. On the release front, there are no Canadian releases on the schedule. In the US, the key event is the Federal Reserve minutes from the January meeting. We'll also get a look at Existing Home Sales, which are expected to climb to 5.61 million. On Thursday, Canada releases retail sales reports and the US will publish unemployment claims.

The week started on a sour note for Canadian indicators, as Wholesales Sales declined 0.5%, short of the estimate of 0.4%. It marked the first decline in three months. The markets are expecting another soft release from Core Retail Sales, a key barometer of consumer spending. The indicator posted a strong gain of 1.6% in December, but is forecast to slow to just 0.1% in January. If consumer spending posts a weak reading, the Canadian dollar could lose more ground. The pair is under pressure, and has shed 1.0% so far this month.

It has been an eventful few weeks for Jerome Powell, who has just commenced his stint as chair of the Federal Reserve. Strong US data in recent weeks has raised speculation that the Fed may need to accelerate the pace of interest rate hikes in 2018. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four, or even five times in 2018. Meanwhile, concern over higher inflation and more rate hikes sent the stock markets into a frenzy earlier in February. Powell sought to reassure the markets that the Fed was monitoring the situation, but it's doubtful that the Fed can do much to prevent volatility in the markets.

Pound Faces Headwinds As UK Unemployment Rate Rises, Fed Meeting Minutes Pending

Here are the latest developments in global markets:

FOREX: Although British average earnings (excluding bonuses) in January appeared stronger than expected, reaching the highest growth in a year, pound/dollar eased to a one-week low of 1.3913 (-0.51%) as the unemployment rate rose surprisingly for the first time since June 2015 in the three months to December. In Brexit news, more than 60 Conservative members wrote a letter to the UK Prime Minister, Theresa May, demanding a clean exit from the EU a day after the Brexit Minister, David Davis, said that the UK wants to avoid any obstacles to smooth trade with the EU, echoing the division over Brexit issues in May’s government and party. The Eurozone’s flash Markit PMI readings for the month of February disappointed, weighing on euro/dollar which already faced pressure from the rising dollar. Euro/dollar changed hands lower at 1.2319 (-0.13%) and euro/pound was up at 0.8845 (+0.33%). Dollar/yen reversed part of earlier gains made on the back of higher US Treasury yields, last trading at 107.44 (+0.12%), while the dollar index inched up to 89.87 (+0.12%). Aussie/dollar and kiwi/dollar stood at 0.7855 (-0.33%) and 0.7343 (-0.03%) respectively.

STOCKS: Rising bond yields gave a knock to the European stocks on Wednesday, with the pan-European STOXX 600 losing 0.46% and the blue-chip Euro STOXX 50 moving lower by 0.42% at 1000 GMT despite encouraging earnings releases by telecommunication companies, and the Lloyds Bank. The German DAX 30 retreated by 0.46% with all sectors being in the red, the French CAC 40 weakened by 0.26%, the Italian FTSE MIB fell by 0.87% and the Spanish IBEX 35 dropped by 0.96%. US stock futures were pointing to a negative open.

COMMODITIES: A strengthening dollar continued to weigh on oil prices during early European trading hours, while worries that US oil production could hamper OPEC’s efforts to curb supply also hanged in the background. WTI crude and Brent were down by 1.0% at $61.12/barrel and $64.59/barrel respectively at 1020 GMT. In other commodities, the dollar-denominated gold was trading at one-week lows, last seen at $1328.88/ounce.

Day ahead: Bank of England to discuss inflation before British Parliament; US FOMC minutes eyed

After the wage growth figures, the next challenge for the pound today would be the Bank of England’s inflation hearing before the British parliament where the BOE Governor, Mark Carney, and a number of Monetary Policy Committee members will discuss the latest inflation readings, giving further guidance on the central bank’s monetary policy path. Note that growth in consumer prices stood flat at 3.0% y/y in January, unlike analysts’ expectations of a soft decline towards 2.9%.

In politics, a meeting taking place today that could touch on Brexit issues is the one between UK PM Theresa May and Dutch PM Mark Ruttee.

In the US, investors will be waiting for the release of the FOMC minutes regarding the Fed’s last meeting held at the end of January where Fed policymakers decided to hold interest rates unchanged. Particularly market watchers will be interested to identify any details on the Fed’s future monetary policy strategy as markets are currently betting that the central bank will likely deliver another rate hike at its next meeting on March 20-21.

In terms of data, the economic calendar will feature US figures in the remaining of the day. At 1445 GMT February’s Markit flash PMI estimates will be available, while a few minutes later at 1500 GMT the National Association of Realtors will publish stats on existing home sales. Moreover, before the day ends, the American Petroleum Institute will report on the US crude oil stocks for the week ending February 16 at 2130 GMT, bringing some volatility to oil prices.

Turning to public appearances in the US, the Philadelphia Fed President Patrick Harker – a non-voting FOMC member in 2018 – is scheduled to speak on the US economic outlook at 1400 GMT.

Traders will be also paying attention to this week’s US government debt auctions.

Earnings releases will continue to attract attention in the stock markets.

Technical Outlook: EURGBP Bounces After Rise In UK Unemployment Deflated Pound

The cross bounced on Wednesday after bears were repeatedly rejected just above psychological 0.88 support, also 50% retracement of 0.8686/0.8919 upleg and unexpected rise in UK unemployment deflated pound. Reversal of daily slow stochastic from oversold zone supports the action and fresh bullish acceleration improved the setup of daily MA's. Positive momentum studies are supportive but recovery faced strong headwind from converged 10/100SMA's at 0.8855, where recovery rally was so far capped. However, improved near-term outlook sidelined immediate bearish threats, but recovery needs to clear initial barrier at 0.8855 and more significant 0.8875 resistance (200SMA/Fibo 61.8% of 0.8919/0.8804 bear-leg) to generate stronger bullish signal and confirm higher base at 0.8804. Cluster of converging daily MA's (20/30/55) at 0.8830 zone now marks solid support, guarding lower breakpoint at 0.8804.

Res: 0.8857, 0.8875, 0.8892, 0.8919

Sup: 0.8830, 0.8800, 0.8775, 0.8732

Euro Ticks Lower As German Manufacturing PMI Softens

The euro has posted small losses in the Wednesday session. Currently, the pair is trading at 1.2317, down 0.16% on the day. On the release front, German and Eurozone Manufacturing PMIs slowed in January. The German PMI dipped to 60.3, shy of the estimate of 60.6 points. It was a similar story with the Eurozone PMI, which dropped to 58.5, shy of the estimate of 59.2 points. In the US, the key event is the Federal Reserve minutes from the January meeting. The US will release Existing Home Sales, which are expected to climb to 5.61 million.

Federal Reserve chair Jerome Powell has just started his new job, and there is plenty on his plate. Strong US data in recent weeks has raised speculation that the Fed may need to accelerate the pace of interest rate hikes in 2018. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four or even five times in 2018. Meanwhile, concern over higher inflation and more rate hikes sent the stock markets into a frenzy. Powell sought to reassure the markets that the Fed was monitoring the situation, but it’s doubtful that the Fed can do much to prevent volatility in the markets.

Should cryptocurrencies be regulated? The recent turbulence in the global stock markets has triggered strong volatility in the currency markets, and ECB President Mario Draghi recently stated that the ECB was concerned about the euro’s sharp fluctuations. Last week, Draghi weighed in on Bitcoin, a cryptocurrency which has seen wild fluctuations in recent months. There are growing calls for regulation of these currencies, and central banks could play a key role in such oversight. However, Draghi poured cold water on any ECB involvement, saying that it was not the ECB’s responsibility to ban or regulate Bitcoin. Draghi added that the ECB was exploring the use of blockchain, a digital technology to monitor bitcoin transactions. France and Germany want to cryptocurrencies on the agenda at the next G-20 meeting, and there is bipartisan support in Congress to adopt new rules to regulate virtual currencies.

New Zealand Retail Sales Eyed, Will It Affect The Kiwi’s Bearish Retracement In Short-Term?

New Zealand retail sales data for the fourth quarter of 2017 are due for release at 2145 GMT on Thursday, with forecasts pointing to a strong rise in quarterly terms. The indicator is expected to edge up by 1.4% in the three months to December, following a rise of 0.2% before.

The latest release was the slowest gain since June 2015, mainly explained by weaknesses in housing construction and in food and beverage services. Also, the attention will turn on the kiwi as there is plenty of room for a surprise if the release beats expectations.

Turning to monetary policy, the Reserve Bank of New Zealand (RBNZ) announced its official cash rate on February 7 and kept it at a record low of 1.75%, as widely expected. The central bank last changed the key rate in November 2016. Also, policymakers mentioned that the global economy has continued to improve and recognized that inflation remains subdued. The policy statement highlighted some signs of emerging pressures, namely, an increase in commodity prices, strong equity markets, and less stimulatory monetary policy.

In addition, the RBNZ stated that monetary policy will remain accommodative for a considerable period, as numerous uncertainties remain, and policy may need to adjust accordingly. It is worth mentioning that the nation's consumer prices increased by 1.6% year-on-year in the fourth quarter from 1.9% in the prior period. It was the lowest quarterly inflation in a year.

However, other recent data has been more encouraging, such as a tightening labour market, rising exports, and higher credit card spending. This points to a pick-up in growth towards the end of 2017 following the uncertainty created by the inconclusive outcome of the September general election. Moreover, GDP growth was stronger than projected in the third quarter, which advanced by 0.6%. The next release of GDP growth for the fourth quarter is scheduled for March 14.

From the technical point of view, kiwi/dollar slipped over the last three days after the strong rebound on the 5-month high of 0.7435, which it reached again on January 23. The pair has fallen almost 1% since February 16 as the US dollar is recovering some of its losses.

In addition, in the short-term timeframe, the price challenged a five-day low of 0.7325 during today's European session. If retail sales surpass the consensus then the expectation is a run until the 0.7435 resistance level. A break above the aforementioned obstacle could open the door towards the next barrier of 0.7560 taken from the significant top on July 27. Such a major big move could happen on a medium-term basis.

A worse-than-expected figure could continue the downward pressure for the pair and would retest the 0.7175 support level, but the price would first need to go through the 20 and 40-day simple moving average near 0.7320 and 0.7265 respectively at the time of writing.

Forex Analysis: UK Brent Oil And USDCAD

Crude Oil prices fell on Wednesday, with losses in both U.S WTI and U.K. Brent, as the market awaits inventory data. Energy Information Administration (EIA) data last week showed U.S. inventories rising by 1.8 million barrels, which was smaller than expected. The American Petroleum Institute (API) will release its forecast on U.S. crude inventory on Wednesday, followed by official supply data from the (EIA) on Thursday.

UK Brent Oil

In the daily timeframe, Brent had a sharp decline from the highs but bounced from the October trend line at 61.60. The commodity has now found resistance at the June rising trend line at 64.40 and is resuming the decline. There is now a possibility that a head and shoulders pattern is developing, which would be fully formed if the neckline at 61.60 is broken. Near-term support is at 64.60, which if broken, would lead to further declines to support at 62.90 and then 61.60. However, a break of 64.40 would change the outlook, with upside resistance at 66.70 and then 68.0.

USDCAD

The Canadian Dollar has come under pressure in recent days due to worries over NAFTA and a decline in crude oil prices. Moreover, recent strength is the U.S Dollar has helped the USDCAD pair to climb. In the daily timeframe, USDCAD is now close to strong technical resistance due to a confluence of trendlines and horizontal resistance at 1.2685, which if broken, would find further resistance at the 38.2% Fibonacci retracement level of 1.2720, followed by 1.2780. On the flip-side, a bearish reversal will find initial support at 1.2640, followed by 1.2590 and then 1.2550.

BoE Hearing And Fed Minutes In Focus

- US Futures Continue to Pare Last Week's Gains;

- GBP Slips as Unemployment Ticks Higher;

- BoE Inflation Report Hearing Eyed as Markets Price in Rate Hikes.

US Futures Continue to Pare Last Week's Gains

US equity markets are expected to open in the red again on Wednesday, tracking losses in Europe as stocks continue to pare last week's strong rebound.

It's been a relatively quiet start to the morning and the week, with the bank holiday in the US and Canada contributing to this. The European session has been dominated by economic data releases so far and that's likely to continue, with flash manufacturing and services data due from the US shortly after the open. It's the FOMC minutes that will be released later in the day though that will likely be the standout event from a US perspective, particularly as the statement caused quite a stir at the end of January.

The sell-off in the markets may have come a couple of days later but part of the initial trigger was a more hawkish sounding Fed, with the jobs report then being the straw that broke the camel's back two days later. While the minutes may not generate quite the same response, traders will likely monitor what they say very closely for signs that policy makers are now leaning more towards three to four rate hikes this year, rather than two or three.

GBP Slips as Unemployment Ticks Higher

Sterling is coming under a bit of pressure this morning after UK jobs data for the three months to December showed wages still growing at a moderate pace and unemployment ticking up to 4.4%. While a higher reading on wage growth may have triggered a more bullish response from the pound, the data turned out to be quite insignificant as it's unlikely to change the views at the Bank of England.

Wages have been slowly ticking higher recently and they could continue to do so as workers demand more due to the higher cost of living and a tight labour market. The move higher in the unemployment rate won't be a concern at this moment with it potentially being a one-off move and still very low. As long as inflation remains at upper range of what is deemed acceptable, the central bank seems intent on raising rates at least once more this year, despite the temporary factors driving it and economic uncertainty that lies ahead.

BoE Inflation Report Hearing Eyed as Markets Price in Rate Hikes

Members of the Monetary Policy Committee including Governor Mark Carney will appear before the Treasury Select Committee later on today, during which they will be questioned on their latest inflation report forecasts and expectations for interest rates going forward. While it's always interesting to get the views of policy makers and the pound will likely be volatile throughout, I wonder how much of what they have to say will now already be priced in, with at least one rate hike now expected this year.

With that in mind and with Brexit transition negotiations likely to dominate the next month, we could see the pound lose some of the momentum that's been gathering over the last six months or so. It's recent failed to make new highs on two occasions against the dollar and it's also slipping against the yen in a possible sign that traders are beginning to lock in profits ahead of what could be a difficult month.

Technical Outlook: Spot Gold Holds In Narrow Consolidation After Heavy Losses, Awaits FOMC Minutes

Spot Gold is trading within narrow consolidation above one week low at $1325 as traders await release of FOMC minutes later today. The yellow metal fell sharply on Tuesday, driven by stronger dollar, making the strongest one-day fall since 06 Feb. Today's extension lower cracked important support at $1328 (Fibo 61.8% of $1307/$1361 upleg), but was so far unable to clearly break lower. Daily 10/20/30 MA's in bearish setup and 14-d momentum heading south in the negative territory are supportive for further weakness, as yesterday's long red candle weighs. Close below $1328 is needed to generate fresh bearish signal for extension towards $1320 (Fibo 76.4%) violation of which would unmask key near-term support at $1307 (08 Feb trough). FOMC minutes are expected to give fresh signals about the pace of Fed's rate hikes in 2018, with hawkish tone expected to further inflate the greenback and increase pressure on gold. Alternative scenario requires firm break above the cluster of daily MA's between $1334 and $1336 to ease immediate downside pressure and signal stronger retracement of $1361/$1325 bear-leg.

Res: 1331, 1334, 1336, 1339

Sup: 1325, 1320, 1317, 1314

Market Update – European Session: Major European PMI Data Continues To Move Off From Recent Cycle Highs, UK Wage...

Notes/Observations

Major European PMI data continued to move off record highs reached back in Dec (Misses: France, Germany and Euro Zone)

UK jobless rate rises unexpectedly, wage growth steady

Asia:

Japan Feb Preliminary Manufacturing PMI: 54.0 v 54.8 prior; new export orders slow on rising JPY currency (Yen)

Japan Currency Head Asakawa reiterated yen moves are one sided. Did not see need for major change from G20 agreement to refrain from currency devaluation. Noted that surging US Treasury yields as beginning of a sea change and that going forward the US economy will probably be robust and interest rates will rise

Japan PM Abe seeking more stimulus to support economy beyond Olympics, he raised thetopic at a meeting of the Council on Economic and Fiscal Policy

Europe:

Over 60 Members of Parliament send Brexit suggestions to PM May believing that UK should be free to negotiate and sign trade deals with other countries as soon as it left and wanted "full regulatory autonomy" for the UK after March 2019

Sweden Central Bank Dep Gov Floden stated that inflation and inflation expectations have trended upward. Reiterated Riksbank will likely raise rates in H2 2018

Americas:

EU and Mexican negotiators said to have agreed on five new chapters and made important progress on others during its 9th round of trade talks

Economic Data:

(NL) Netherlands Feb Consumer Confidence: 23 v 24 prior

(NL) Netherlands Dec Consumer Spending Y/Y: 1.2% v 2.5% prior

(NL) Netherlands Jan House Price Index M/M: 1.5% v 0.4% prior; Y/Y: 8.8% v 8.2% prior

(NO) Norway Dec AKU Unemployment Rate: 4.1% v 4.1%e

(FR) France Feb Preliminary Manufacturing PMI: 56.1 v 58.0e (17th month of expansion), Services PMI: 57.9 v 59.0e, Composite PMI: 57.8 v 59.2e

(ZA) South Africa Jan CPI M/M: 0.3% v 0.3%e; Y/Y: 4.4% v 4.4%e

(ZA) South Africa Jan CPI Core M/M: 0.2% v 0.3%e; Y/Y: 4.1% v 4.2%e

(CH) Swiss Jan Money Supply Y/Y: 4.1% v 3.6% prior

(DE) Germany Feb Preliminary Manufacturing PMI: 60.3 v 60.5e, Services PMI: 55.3 v 57.0e, Composite PMI: 57.4 v 58.5e

(EU) Euro Zone Feb Preliminary Manufacturing PMI: 58.5 v 59.2e, Services PMI: 56.7 v 57.6e, Composite PMI: 57.5 v 58.4e

(UK) Dec Average Weekly Earnings 3M/Y: 2.5% v 2.5%e; Weekly Earnings (ex Bonus) 3M/Y: 2.5% v 2.4%e

(UK) Jan Jobless Claims Change: -7.2K v +8.6K prior; Claimant Count Rate: 2.3% v 2.4% prior

(UK) Dec ILO Unemployment Rate: 4.4% v 4.3%e; Employment Change 3M/3M: +88K v +165Ke

(UK) Jan Public Finances (PSNCR): -£26.4B v +£25.3B prior; Public Sector Net Borrowing: -£11.6B v -£11.4Be; Central Govt NCR: -£27.3B v +£18.8B prior; PSNB (ex-banking groups): -£10.0B v -£9.5Be

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month,6-month and 12-month bills

(DK) Denmark sold total DKK2.12B in 2020 and 2027 DGB Bonds

(SE) Sweden sold SEK500M vs. SEK500M indicated in 2.25% 2032 bonds; Avg Yield: 1.184% v 1.1017% prior; Bid-to-cover: 3.69x v 2.26x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.6 at 378.4, FTSE -0.2% at 7236, DAX -0.6% at 12416, CAC-40 -0.4% at 5269 , IBEX-35 -1.0% at 9798, FTSE MIB -0.9% at 22477 , SMI -0.6% at 8927, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European Indices trade lower across the board following on from the weakness on Wallstreet overnight as Walmart dropped 10% following earnings. US futures have been mixed this morning ahead of another raft of earnings. In the banking sector Lloyds posted strong Q4 results, with Wolter Kluwer, Orange and Glencore also trading higher after earnings. Atos trades lower after disappointing margin outlook, while First Group trades sharply lower after its trading update. Elsewhere Temenos agreed terms to acquire Fidessa and AA trades sharply lower following its new business strategy. Looking ahead notable earners include Dish Network, Advanced Auto Parts, Southern Company and Delphi Automotive.

Movers

Consumer Discretionary [First Group [FGP.UK] -10.5% (Trading update), Wolter Kluwer [WKL.NL] +3.20% (Earnings)]

Materials [ Glencore [GLEN.UK] +4.1% (Earnings)] -Technology [Atos [ATO.R] -3.7% (Earnings)]

Telecom [ Orange [ORA.FR] +1.1% (Earnings), O2 Deutschland [O2D.DE] +0.5% (Earnings)]

Financial [ Lloyds [LLOY.UK] +1.4% (Earnings), Fidessa [FDSA.UK] +3.1% (To be acquired), Deutche Boerse [DB1.DE] +1.6% (Earnings), AA Plc [AA.UK] -20% (Strategy update)]

Speakers

Spain PM Rajoy: Still seeking support for 2018 budget and sought to get the budget bill passed in July

UK Brexit Transition draft: In broad agreement with EU on transition period; sought end-date of transition

Italy Econ Min Padoan: Should not take for granted that next ECB president will be Germany's Weidmann

Eurogroup chief Centeno: Region growth should be sustained in coming years

Sweden Debt Office updated itsborrowing forecasts which cut the nominal bond issuance for both 2018 and 2019. It noted that a larger budget surplus led to lower bond issuance but added that a further reduction was not appropriate since it would risk worsening market liquidity so much that investors might leave the mark

Russia Deputy Foreign Min Ryabkov: Could respond to possible new sanctions by the US

Japan Cabinet Office (Gov’t) Monthly Economic Report for February: Maintained its overall assessment that the domestic economy was recovering at a moderate pace

Brazil Fin Min Meirelles said to question a Senate proposal that would introduce a duel mandate for the central bank

Currencies

USD maintained its recent strength aided by rising bond yields. Dealers noted that the US 2-year results saw the highest yield in almost a decade with good demand.

EUR/USD was softer for the 4th straight session at 1.2320

GBP/USD moved lower as UK jobless rate rose unexpectedly while wage growth was steady. Pair was off by 0.4% at 1.3935 just ahead of the NY morning.

USD/JPY was higher by 0.2% but off the late Asian session highs of 107.70. Japanese officials touting the higher US yields as beginning of a sea change for the currency (aka weaker yen)

Fixed Income

Bund Futures trades up 41 ticks at 158.79 as Bunds remain in recovery mode. Upside targets159.25, while a return lower targets the157.75 level.

Gilt futures trade at 121.82 up 50 ticks after the UK labor report shows no sign of improvement and wages pick up. Support continues to stand at 120.75 then 120.15, with upside resistance at 121.75 then 122.25.

Tuesday's liquidity report showed Monday's excess liquidity fell to €1.835T from €1.854T prior. Use of the marginal lending facility rose to €76M from €47M prior.

Corporate issuance saw 3 issuers raise $2.4B in the primary market

Looking Ahead

(CO) Colombia Jan Industrial Confidence: No est v -4.8 prior; Retail Confidence: No est v 21.4 prior

05:30 (SE) Sweden Central Bank ( Riksbank) Jansson speech

05:30 (PT) Portugal Debt Agency (IGCP) to sell Bills

06:00 (RU) Russia to sell combined RUB45.9B in 2021 and 2028 OFZ Bonds

06:00 (CZ) Czech Republic to sell 2026 and 2029 Bonds

06:30 (ZA) South Africa Fin Min Gagaba budget speech

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Feb 16th: No est v -4.1% prior

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:15 (UK) Baltic Dry Bulk Index

08:55 (US) Weekly Redbook Sales

09:00 (US) Fed’s Hawker (non-voter, moderate) on Economic Outlook

09:00 (NG) Nigeria to sell combined NGN100B in 2021 and 2028 Bonds

09:15 (UK) BOE Gov Carney with members Broadbent, Haldane and Tenreyro

09:45 (US) Feb Preliminary Markit Manufacturing PMI: 55.5e v 55.0 prior, Services PMI: 54.0e v 53.3 prior, Composite PMI: No est v 53.8 prior

10:00 (US) Jan Existing Home Sales: 5.60Me v 5.57M prior

11:30 (US) Treasury to sell 2-Year Floating Rate Notes Reopening

12:00 (SE) Sweden Central bank ( Riksbank) Dep Gov Ohlsson (hawk) speech in Frankfurt

12:00 (CA) Canada to sell 10-Year Bonds

13:00 (US) Treasury to sell 5-Year Notes

14:00 (AR) Argentina Jan Trade Balance: -$0.6Be v -$0.9B prior

14:00 (US) FOMC Minutes from the Jan 31st meeting

16:30 (US) Weekly API Oil Inventories