Sample Category Title

GBP/USD Sideways Price Action

GBP/USD is maintained at the 1.40 range, trading between hourly resistance and support at 1.4151 (05/02/2018 high) and 1.3742 (16/01/2018 low). The technical structure suggests further sideway moves.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Decreasing

EUR/USD is decreasing further, heading for support at 1.2276 ( 14/02/2018 low). Hourly resistance at 1.2510 (15/02/2018 high) is distanced. The technical structure suggests further downside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

EUR/GBP 4H Chart: Confirms Medium-Term Pattern

The common European currency has been bound in several long and medium-term patterns which have guided the currency pair lower since August 2017.

When taking a look at the price movement, the pair's has been trading in a large-scale triangle which was formed in August. The Euro bounced off the lower boundary of a medium-term pattern on January 24 and has since surged against the Pound Sterling.

Meanwhile, EUR/GBP is facing a support at the weekly pivot point near 0.8818. Also, it is important to point that technical indicators favour bearish movement.

GBP/JPY 4H Chart: Set To Surge

The Pound Sterling has been constrained by a descending channel against the Japanese Yen after the pair touched the upper boundary on February 2.

Following a breakout from the upper trend-line, the currency exchange rate also breached the 55—hour simple moving average and tested the weekly R1 at 150.70.

Given that a breakout occurred through the upper boundary, this suggests that the bullish sentiment could continue dominating the currency pair. However, it is important to note that the rate is likely to encounter a stronger resistance cluster set by the weekly pivot point and the combination of the 100-, and 200-hour SMAs near the 152.19. mark.

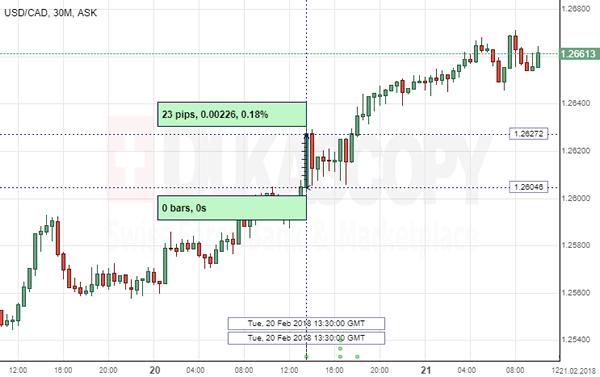

USD/CAD: Canada Wholesale Sales

The Greenback strengthened against the Loonie following the release of the report on Canadian wholesale sales. The USD/CAD currency pair jumped 23 base points, reaching 1.2627.

The volume of Canada's wholesale sales decreased after the downwardly-revised 0.3% gain registered in the prior month, closing the year 2017 in red. Statistics Canada stated that the country's wholesale trade declined 0.5% in the reported month, representing the first drop in the last three months. The move was driven by weaker demand in personal and household goods and miscellaneous subsectors. In terms of volume, the actual wholesale sales tumbled 0.9%.

EUR/USD: German ZEW Economic Sentiment

The Euro weakened against the Greenback despite the data showing an unexpected uptick in the German ZEW economic sentiment. The EUR/USD exchange rate dropped four base points to 1.2339.

In February, Germany's investors continued to show strong confidence in the current economic situation even despite the ZEW indicator recording a decrease of 2.6 points from the prior month. Commenting on the matter, ZEW President Professor Achim Wambach said that the German economy continued to perform on an optimistic note in early 2018, adding positive results come from solid global economic growth and private consumption and that Europe's largest economy is expected to continue its growth trajectory in the next six months.

Technical Outlook: WTI OIL – Strong Negative Signals On Bearish Harami And Penetration Of Rising Daily Cloud

WTI oil extends lower on Wednesday and penetrated rising daily cloud which underpinned the action in past couple of sessions.

Tuesday's close in red was initial signal that strong four-day recovery rally from higher base at $58.10 zone is running out of steam, with completion of bearish Harami pattern generating stronger negative signal.

Break into daily cloud (cloud top so far caps today's action and marks strong resistance at $61.73) extended lower to crack next pivotal support at $60.93 (Fibo 38.2% of $58.19/$62.63 upleg), with close below here to generate reversal signal.

Slow stochastic reversed from oversold territory on daily chart, RSI turned south after ranging in neutrality zone, while 14-d momentum continues to trend lower, deeply in negative territory, reinforcing bearish signal.

Firm break below $60.93 would spark further weakness and expose targets at $60.34 (daily Tenkan-sen) and key $59.89/84 supports (Fibo 61.8% of $58.19/$62.63 / daily cloud base).

Alternatively, bounce and close above daily cloud would neutralize bearish threats and shift focus higher.

Release of US API crude inventories due later today is eyed, ahead of EIA crude stocks report, which will be released tomorrow (releases were postponed for one day due to US holiday on Monday).

Traders are cautious ahead of inventories reports, with concerns about further build of US crude stocks which could put oil prices under additional pressure.

Res: 61.73, 62.00, 62.35, 62.63

Sup: 60.90, 60.64, 60.34, 59.89

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2324

The downtrend is still underway, with an initial resistance at 1.2370. A violation of the latter will signal a completion of the whole slide from 1.2550 and will challenge 1.2460.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2370 | 1.2650 | 1.2290 | 1.2290 |

| 1.2460 | 1.2870 | 1.2290 | 1.2210 |

USD/JPY

Current level - 107.51

The recent rise has peaked below 108.00 resistance and my outlook is already bearish, for a downswing towards 106.80.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 108.00 | 108.30 | 107.35 | 105.40 |

| 108.30 | 110.40 | 106.80 | 102.40 |

GBP/USD

Current level - 1.3961

Yesterday's reaction above 1.3920 was a short-lived one and the pair is ready for another test of the mentioned support. While the latter is intact, my outlook will remain counter-trend, for another upswing towards 1.4280.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4060 | 1.4280 | 1.3920 | 1.3760 |

| 1.4185 | 1.4340 | 1.3800 | 1.3620 |

US Dollar Continues To Recover Ahead Of FOMC Minutes

From now on, it will cost to short the buck

Despite the lack of news on both the political and economic sides, the US dollar erased almost completely last week losses, which sent the Dollar Index down to 88.25 – another multi-year low. The buck started the week on a solid footing even though US investors were off for President’s Day. Since then, the greenback kept grinding higher supported by rising US rates, especially on the short-end of the yield curve. Indeed, the US 2-year Treasury yield inched higher to 2.25% amid rising inflation expectations; the 2-year breakeven inflation hit 2.03%.

Looking at interest rate differentials, one observes that US rates are rising faster than its G10 peers. For the FX market, this has immediate consequences, as forward points on AUD/USD are now positive (beyond 2 months maturity). This is the first time since March 2001 that 1-year forward points moved above the neutral threshold. It will now cost around 20bps per year to go long AUD against USD. The situation is almost similar with the New Zealand dollar. 1-year forwards points are not in positive territory yet, but are about to cross the line.

The implication of this new situation are significant for investors. From now, it will cost investors to go short USD against those currencies and it could really act as a disincentive for investors to speculate on a weaker dollar. In other word, this new set-up up should benefit the greenback.

The agenda is quite light today. However, traders will be watching closely the minutes of the January FOMC meeting, looking for clue regarding the Fed rate path. The statement released on January 31st was considered as slightly hawkish. It will therefore be the opportunity to validate this point of view. We believe those minutes won’t have a big a big impact on market, as trades have already priced in a March rate hike. The market will have to wait until then to get updated forecast. This could be a game changer, especially if Fed members revised to the upside the number of rate hike for 2018.

German market expectations are better than expected

German investor opinion remains optimistic despite political turmoil according to yesterday’s published economic data from economic institute ZEW and German Federal Statistic Office. The February ZEW Survey Expectations index came out at 17.80 (consensus: 16) against 20.4 for January, in line with December numbers amounting to 17.40. January Producer Price Index Y/Y was announced at 2.10% (consensus: 1.80%) against 2.30% the previous month, maintained at a high rate.

Political uncertainty remains around the German “GroKo” coalition that is supposed to be extended by Social-Democratic party (SPD) adherents on March 4th according to recent surveys anticipating a 60% support according to a survey from German Funke media group. In the case of a “no”, new elections would take place and new elections would probably occur, strengthening right extreme party “Alternative for Germany” (AfD) at the cost of SPD. The likelihood remains however slim, confirming our view that Germany remains in a positive growth setting, boosted by strong economic exports (December trade balance at EUR 18.20 billion) and sharp private consumption (January Consumer Price Index Y/Y at 1.60%, above 2 years’ average written at 1.10%), backing further improvement for the coming six months.

Yesterday the German DAX closed at 12’488 (+0.83%), supported by Materials (+1.44%), Utilities (+1.24%), Industrials (+1.12%) and Information Technology (+1.10%) while German 10-year Bund remained stable at 0.735%.

UK Data & FOMC Under Focus

There is a lot of noise for the Fed

The language of the FOMC minutes would be the key today

The resilience of Sterling against the dollar is something of interest

European markets and US futures are trading lower. Investors are paying attention to the headlines coming from Italy where another election could be a possibility. The spread between 10-year Italian and German bonds is the focal point for investors. We have seen this spread widened up to 132 basis points and it has the potential to continue to move higher.

In the Forex market, the strength of the dollar index is prominent and sellers are respecting it. The limelight is on the FOMC minutes today. The big question is if the Fed is going to stick to its gun -increase on the interest rate only three times a year?

No doubt, there is a lot of noise that the Fed could deviate from it's monetary policy stance due to the strength in inflation. This could result in Fed increasing the interest rates more than three times in 2018. The language of the FOMC minutes would be the key today, this would provide us with the clues about the Fed's intention and traders would adjust their positions on the back of that.

The FOMC minutes is not the only aspect which traders are going to watch closely. We also have some important economic numbers due today; the existing home sales data & Markit Economic PMI report. If we see these numbers coming out strong, traders would bet more on the dollar index to move higher.

The resilience of Sterling against the dollar is something of interest, and this is mainly because traders think that the Brexit deal could take place at the end of this year. Although, we have our doubts about this because the road is long and the progress is not substantial.

For now, it is more about the economic data which would be able to shift the momentum. The UK's labour market data is the chief factor which we think will help the Bank of England to make it's mind on another interest rate hike. Currently, the odds are sitting at 76% that another rate hike could become a reality as soon as May.

However, the upcoming labour data could certainly hammer those odds if the numbers do not stack up. What investors want to see is if the wage growth could outpace inflation given that the inflation is a major headache. The Bank of England surely understands that without job growth, changing the stance on it's monetary policy would be a destructive move.

Apart from the economic data, the testimony of the governor of the Bank of England, Mark Carney, along with monetary policy committee members, Broadbent, Haldane and Tenreyo, will be in the spotlight. They will be defending the level of inflation in front of the parliament. The probabilities are there could be some interesting headlines from some of the members and these headlines could bring huge moves for the currency.