Sample Category Title

Technical Outlook: USDJPY Extends Recovery But Overall Picture Remains Bearish

Recovery rally extends into fourth straight day and probed above pivotal barriers at 107.43/48 (Fibo 38.2% of 110.48/105.54 bear-leg / falling 10SMA) to hit one-week high at 107.90 (14 Feb high).

Bulls faced strong headwinds here and show initial signs of stall as falling 4-hr cloud (spanned between 107.51 and 108.25 weighs on near-term action.

Overall bearish structure keeps negative bias for fresh weakness after correction. Daily MA's in firm bearish setup and 14-d momentum deeply in negative zone maintain negative outlook.

Strong barriers at 107.90 (recovery high) and 108.00 (50% of 110.48/105.54 downleg) should limit upside attempts before broader bears resume.

Conversely, lift above 108.00 will be initial bullish signal which needs confirmation on break and close above falling 4-hr cloud top (108.25) and descending 20SMA (108.36).

FOMC minutes are eyed for more clues about dollar's near-term action.

Res: 107.90, 108.00, 108.36, 108.60

Sup: 107.43, 107.00, 106.72, 106.44

EUR/USD Analysis: Faces Senior Channel

Despite flashing bullish signals on Tuesday, the bearish momentum took over the market during the first part of the day, as the Euro managed to gather enough momentum to breach the 200-hour SMA and the 23.6% Fibo retracement. A further decline, however, did not follow, as the bottom boundary of a four-month channel circa 1.2320 restricted the pair from moving below this level.

It is likely that the pair tries to re-gain some of the lost positions during the following hours, but with limited success due to the combined resistance of the 200– and 55-hour SMAs being located near the 1.2370 mark.

Meanwhile, some volatility is likely to be introduced in the market later in the evening when the FOMC publishes its meeting minutes at 1900GMT.

GBP/USD Analysis: Unchanged From Tuesday

Despite some minor fluctuations, the Pound has maintained the same price level for the second day. No advances either direction were made due to strong barriers on each side.

Today, the Sterling could continue trading between the 55– and 200-hour SMAs slightly below the 1.40 mark. The northern side is also restricted by the weekly and monthly PPs, while the southern area—by the 38.20% Fibo retracement. Thus, it is likely that the pair continues trading sideways for several hours, thus approaching the bottom line of a two-week ascending channel circa 1.3950 prior to forming a breakout.

Technical indicators are in favour of a bullish surge towards the senior channel. The pair's movement later in the evening should be guided by trader response to FOMC meeting minutes released at 1900GMT.

USD/JPY Analysis: Breaches 200-Hour SMA

The US Dollar continues to gain momentum against the Yen for the third consecutive session. The previously-drawn narrow channel up held strong on Tuesday even when the pair breached several notable resistance levels, such as the weekly PP, the monthly S1 and the 200-hour SMA. As a result, the US Dollar was located near the senior channel by Wednesday morning.

Converging technical indicators suggest that the bearish sentiment might take over the market soon just to push the rate away from the overbought territory. This decline should be limited by the long-term moving average and the monthly S1 near 107.20.

Conversely, notable advances should be stopped by the upper boundary of the senior channel and the weekly S1 circa 108.30.

Gold Analysis: Respects Junior Channel

Tuesday's morning session was spent calmly, as the pair was fluctuating between the 23.60% Fibo and the weekly PP. This still movement changed later in the day when a strong hourly plunge allowed for a breakout of the 200-hour SMA circa 1,335.00. Gold has since edged slightly lower; however, it did remain within the bounds of a narrow short-term channel down.

Given that technical indicators are still located in the oversold region, a bullish recovery is still expected to occur in the nearest time. The pair should gain some pips during the following hours; however, the 1,335.00/1,340.00 area is likely to restrict further advance.

In terms of support, the yellow metal should not exceed the weekly S1 at 1,320.00. The market might also be steady prior to FOMC meeting minutes published at 1900GMT.

SP500 Adam And Adam Double Bottom Pattern In Progress

The SP500 has formed Adam and Adam double bottom pattern. Adam pattern is very similar to a W shaped reversal pattern except for the two related bullish spikes that distinguish the pattern from the W bullish. Point 1 and Point 3 form the basis while point 2 is a continuation point. The POC is formed within 2688-2700 zone and the price could spike from the zone towards 2727 (point 2). A 4h close above 2727 should target 2772 followed by 2808 on a further bullish momentum. Only below W L4 - 2662 the price might turn neutral again.

W H3 -Weekly Camarilla Pivot (Weekly Interim Resistance)

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

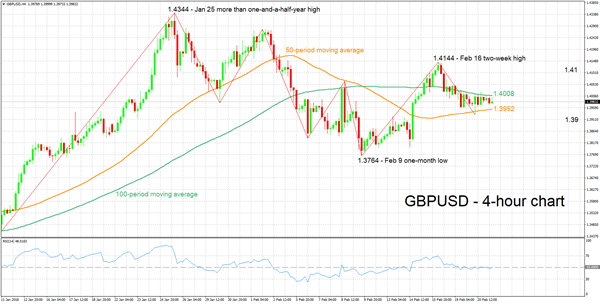

Technical Outlook: GBPUSD Remains At The Back Foot Ahead Of Data

Cable extends weakness on Wednesday's after mixed previous day's action ended in long-tailed Doji and signaled indecision.

Pound was lifted by media comments on Brexit, upside attempts above 1.40 handle were short-lived.

Fresh weakness tests again 10SMA (1.3952) which contained yesterday's dip (Tuesday's spike low lies at 1.3931) and sustained break lower is needed to signal further easing towards 1.3909 (Fibo 61.8% of 1.3764/1.4144 upleg).

Bearishly aligned daily techs are supportive but need further negative signals for confirmation.

UK jobs data are key event for pound today (avg. earnings are expected to remain unchanged at 2.5% in Dec along with unemployment rate (4.3%), while jobless claims are forecasted to fall in Jan (2.3K vs 8.6K in Dec).

A number of speakers from BoE today and FOMC minutes are expected to create firmer signals for sterling.

Res: 1.3977, 1.4018, 1.4049, 1.4104

Sup: 1.3952, 1.3931, 1.3909, 1.3854

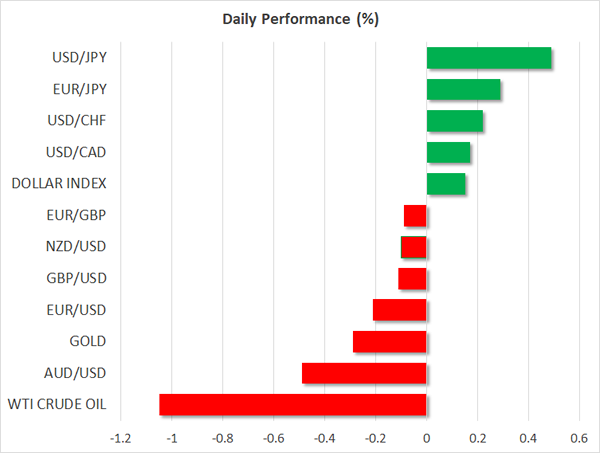

Dollar Continues To Recover Ahead Of Fed Minutes, Eurozone PMIs & UK Employment Data In Focus

Here are the latest developments in global markets:

FOREX: The dollar index was nearly 0.2% higher on Wednesday ahead of the release of the FOMC minutes, extending the notable gains it posted yesterday.

STOCKS: US equity markets closed lower on Tuesday. The Dow Jones fell the most, closing 1.0% lower, while the S&P 500 declined by 0.6%. The Nasdaq Composite retreated as well, but by less than 0.1%. The volatility index (VIX) also moved up, suggesting that the recent turmoil in equity markets is not done yet. In Asia, Japanese markets were mixed as the Nikkei 225 rose 0.2%, but the Topix closed marginally in the red. In Hong Kong, the Hang Seng surged by 1.8%, while markets in mainland China remain closed as Lunar New Year celebrations continue taking place. In Europe, futures tracking the Euro STOXX 50 and most of the major equity indices were in negative territory, suggesting they could open lower today.

COMMODITIES: Oil prices fell on Wednesday, with WTI and Brent crude declining by 1.1% and 0.7% respectively. With no major news in the oil market, the pullback is probably owed to the recovery in the US dollar. Since oil is traded in dollars, it becomes less attractive for investors using other currencies when the greenback strengthens. As for potentially market moving events, the API inventory data are due later on Wednesday. In precious metals, gold was 0.3% lower, last trading near $1327 per ounce. Gold is denominated in dollars too, and thus also becomes less appealing when the US currency gains.

Major movers: Dollar rebound continues ahead of FOMC minutes; sterling catches a bid on Brexit reports

The dollar continued to recover yesterday as the yields on two-year US Treasuries surged to reach 2.26%, a high last seen in 2008. Besides movements in the bond market, the dollar’s gains may be partly owed to investors covering some of their short-dollar positions ahead of the release of the FOMC minutes later today. The minutes will be closely watched as markets try to gauge whether the broader USD weakness has run its course for now, or whether this is just a reprieve before the next leg lower.

The statement accompanying the policy decision back then was changed only slightly, but those changes were perceived as being hawkish, as they indicated more confidence in the inflation outlook. Should the minutes reflect an equally optimistic bias, and perhaps show that the Committee discussed the prospect of faster rate hikes in light of the recently-passed tax overhaul, then the greenback’s rebound could well continue.

The British pound caught a bid yesterday, after a media report suggested that the European Parliament is preparing legislation aimed at allowing Britain to retain “privileged” access to the single market after Brexit. The report likely caught markets by surprise, as EU negotiators have repeatedly said the UK could only have limited access to the single market if it does not adhere by EU regulations after the divorce. If this is indeed confirmed by official EU sources in the coming days, it would mark a clear shift in the Brexit negotiating landscape. From a market perspective, it would likely heighten speculation that Britain may indeed manage to secure a favorable trade deal, and perhaps unleash the next wave of Brexit-related sterling appreciation.

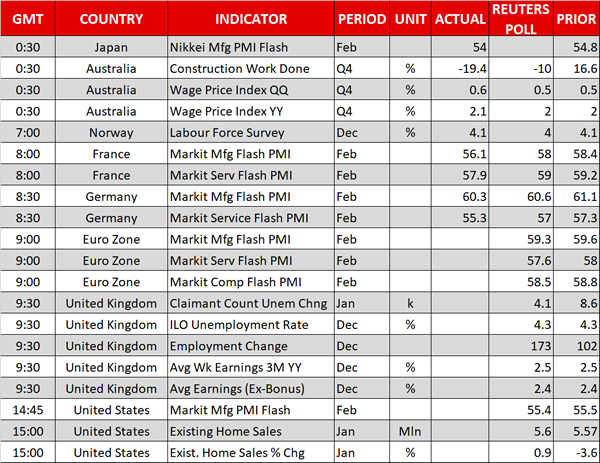

Overnight, Australia’s wage price index for the fourth quarter surprisingly accelerated, reaching 2.1% in yearly terms. This is a positive development for the RBA as it shows that wages are slowly but surely picking up speed. While aussie/dollar spiked higher on the news, it quickly gave back its gains to trade 0.5% lower in the following hours. The pair’s inability to sustain its gains was likely owed to the other piece of data released alongside wages; construction work. It fell by much more than expected in the fourth quarter, likely generating speculation that the economy may have lost some momentum.

Elsewhere, the yen lost some ground against its major counterparts after Japan’s top currency diplomat, Masatsugu Asakawa, said that he views the yen’s recent surge as excessive, and that the recent movements were one-sided.

Day ahead: Eurozone PMIs, UK unemployment & wage growth, US existing home sales & Fed minutes on the agenda

Flash eurozone PMI figures for the month of February for the manufacturing and services industries, as well as the composite measure that blends the two sectors, are due at 0900 GMT. The numbers for all three are expected to slightly ease relative to January, though still remain comfortably in expansion territory above 50 and continue to support the view that growth in the euro area is picking up steam. The data have the capacity to move the euro.

Sterling pairs would be eyed next as UK data on employment and wage growth for December will be made public at 0930 GMT. The unemployment rate is projected to remain at a four-decade low of 4.3%, with the economy expected to have added 173k workers in the three months to December. Particular attention would be falling on average weekly earnings as they’re seen – in case they come in strong – as having the ability to push the Bank of England to hike rates again sooner rather than later. The three-month average of earnings (both including and excluding bonuses) is anticipated to have risen at the same pace as the previously recorded data; 2.5% y/y including bonuses and 2.4% excluding them.

Out of the US, existing home sales data for the month of January due at 1500 GMT will be attracting interest. Sales are anticipated to expand by 0.9% m/m after December’s decline by 3.6%. It should be stated though that last month’s decline was attributed to record low supply of houses driving prices higher and thus discouraging some potential first-time buyers to purchase a house, rather than to intrinsically weak demand. A little earlier (1445 GMT), Markit’s flash manufacturing PMI for the month of February might also attract some attention out of the US.

But perhaps having the highest likelihood of spurring positioning on the dollar will be the official record of Janet Yellen’s last meeting at the Federal Reserve. Fed minutes pertaining to the late January meeting will be released at 1900 GMT, with a hawkish tilt in FOMC members’ views having the ability to maintain the short-term positive momentum for the greenback.

Market participants are also watching the outcome of this week’s US government debt auctions amid concerns of ballooning budget deficits and debt levels.

In policymakers’ appearances: the Swedish central bank Deputy Governor Per Jansson will be talking about the economy and monetary policy at 1030 GMT. Philadelphia Fed President Patrick Harker – a non-voting FOMC member in 2018 – is scheduled to speak on the US economic outlook at 1400 GMT. Bank of England Governor Mark Carney, Deputy Governor Ben Broadbent, chief economist Andy Haldane and Monetary Policy Committee external member Silvana Tenreyro will be answering lawmakers’ questions relating to the central bank’s February Inflation Report at 1415 GMT.

Oil traders will be paying attention to API data on US crude stocks scheduled for release at 2130 GMT.

In politics, a meeting taking place today that could touch on Brexit issues is the one between UK PM Theresa May and Dutch PM Mark Ruttee.

In equities, companies releasing quarterly results will be in focus.

Technical Analysis: GBPUSD looking neutral in short-term

GBPUSD has been moving sideways, painting a neutral picture in the short-term. This view is supported by the RSI indicator which has been hovering around the 50 neutral perceived level.

Should UK employment and wage growth data out during morning European trading beat expectations, the pair is anticipated to head higher. Resistance could be taking place at the moment around the 100-period moving average at 1.4008, with an upside break shifting the focus to the area around 1.41, this being a potential psychological level.

On the downside and in case of a data miss, the pair is likely to head lower. A downside violation of the range around the 50-period MA at 1.3952 which could be providing support at the moment, would turn attention to the 1.39 handle – the area around this point was congested recently.

Lastly, it is worthy of mention that US releases – for example the Fed meeting minutes due later in the day – also have the capacity to spur movements in the pair.

Forex Analysis: AUDUSD And EURGBP

The AUDUSD pair had tried to build a base of support around the 0.78900 level after price moved above this area on the 14th of February. However, the level was breached from above yesterday and, after a protracted battle that saw the 4-hour moving averages used as resistance, the price dropped under the 0.78690 support level and is currently trading around 0.78566. Support can now be seen at 0.78430 and 0.78241. The falling channel bottom comes in at 0.78170, with the 0.78025 level below. Deeper support comes from 0.77771 and the lows of February at 0.77606.

Resistance is now found at the crucial 0.78900 level and a retest here will be of interest to traders going forward. The moving averages are clustered above this level, with the 100-period the highest at 0.79070. Should price break above this area, resistance is located at 0.79550, ahead of 0.80000. Further resistance comes in at 0.80347 and the January high of 0.81352.

EURGBP

The EURGBP pair has once again failed at resistance and remains inside its channel, as seen on the chart. There is quite a reluctance for the price to spend anything more than a few hours above the 0.89000 level, with only one daily close above this level since last November. This then remains the marker for traders to signal a sustained breakout. If the market can string together a break above the resistance and hold the 0.89000 level, then resistance at the descending trend line channel top can be tested with vigour.

Resistance at the blue trend line is located at 0.89015, with 0.89274 above. The 0.89550 is being strengthened by the channel top, with a break out here targeting 0.89816 and the 0.90000 level. A move to 0.90316 may see a constructive retest of support, which if successful would challenge resistance overhead at 0.90891, 0.91433 and 0.92018. The high for 2017 comes in at 0.93071. Support is found at the rising red trendline at 0.87754, followed by 0.87574 and 0.87162. Below these levels, there is support at 0.86901 and the red descending channel bottom at 0.86376.

Technical Outlook: AUDUSD Accelerated Lower On Downbeat Data And Pressure Daily Cloud Top, FOMC Minutes Eyed For Fresh Signals

The Australian dollar remains firmly in red and extended weakness in Asia on Wednesday, hitting one-week low at 0.7840.

Stronger US dollar continues to drive the Aussie lower, with additional pressure coming from downbeat Australian construction data which fell by 19.4% in Q4, strongly undershooting forecast for 10.1% drop and against upward-revised increase by 16.6% in Q3.

Fresh extension lower cracked support at 0.7846 (Fibo 61.8% of 0.7758/0.7988 upleg) and pressures next strong support at 0.7816 (top of rising daily cloud).

Daily techs are turning into firm bearish mode (south-heading RSI and slow stochastic, growing bearish momentum and 10/20SMA’s in bearish setup) and support further weakness.

Close below 0.7846 Fibo support will be bearish signal which needs confirmation on close below cloud top, to expose key near-term support at 0.7758 (09 Feb correction low/daily cloud base).

Broken 10SMA offers immediate resistance at 0.7848, followed by broken Fibo 38.2% barrier at 0.7900, with near-term action weighed by thick hourly cloud (spanned between 0.7911 and 0.7939). Near-term focus is turning to the minutes of the Fed’s late January policy meeting which could provide more clues about the pace of central bank’s actions in 2018.

Hawkish tone from the minutes would increase hopes for faster interest rate hikes this year and could lift the greenback further.

Res: 0.7848, 0.7900, 0.7939, 0.7947

Sup: 0.7840, 0.7816, 0.7773, 0.7758