Sample Category Title

Technical Outlook: EURUSD Extends Lower, EU PMI And FOMC Minutes Could Further Pressure The Pair

The Euro continues to trend lower from 1.2555 spike high/strong upside rejection and pressures psychological support at 1.2300, in extension on previous day's strong fall which generated bearish signal on close below 1.2339 (Fibo 61.8% of 1.2205/1.2555 upleg). Tuesday's long bearish candle and descending thick hourly cloud continue to weigh on near-term action, with 10/20SMA's in bearish setup and 14-d momentum in steep descend, deeply in negative territory, adding to negative outlook. Break below 1.2300 handle and 1.2288 (Fibo 76.4%) would open way towards pivotal supports at 1.2205 (09 Feb correction low) and 1.2172 (Fibo 38.2% of larger 1.1553/1.2555 ascend), loss of which would generate strong bearish signal. German PMI data fell below expectations in Feb with EU Manufacturing PMI forecasted at 59.2 in Feb vs 59.6 in Jan and Manufacturing PMI forecasted at 57.7 in Feb vs 58.0 in Jan, expected to add to existing pressure on downbeat releases. FOMC minutes are also in focus, with hawkish tone from the US central bank expected to further depress the single currency.

Res: 1.2344, 1.2360, 1.2380, 1.2412

Sup: 1.2300, 1.2288, 1.2235, 1.2205

Currencies: Dollar Tries To Fight Back

Sunrise Market Commentary

- Rates: More underperformance of US Treasuries?

Today’s eco calendar heats up with EMU PMI’s, more US supply and FOMC Minutes. The EMU composite PMI is forecast to correct lower from a multi-year high. Minutes should reflect the previous Fed’s statement hawkish tone. US Treasuries’ underperformance against German Bunds can continue. - Currencies: Dollar tries to fight back

Yesterday, the dollar extended the gradual rebound that started at the end of last week. Today, the focus is on the Minutes of the January Fed meeting and on the US Treasury auctions. We expect the Fed to confirm a modestly hawkish stance. The downside of the dollar looks a bit better protected.

The Sunrise Headlines

- US markets ended mixed yesterday. The Nasdaq closed merely flat while the S&P (-0.5%) and Dow (-1%) lost ground. Most Asian equity indices trade positive with mainland China still closed for Lunar NY.

- Dutch FM Hoekstra told the FT that the Netherlands is demanding that private investors face mandatory dent write-downs in future EMU bailouts.

- US Special Counsel Mueller stepped up pressure on two former Trump campaign aides to cooperate in his probe into possible collusion with Russia, unsealing a criminal charge against a lawyer for lying to Mueller's investigators.

- The FT reports that a group of Tory Eurosceptic MPs has tried to flex its political muscle with a letter to PM May, urging her to hold firm on plans for Brexit to mean leaving the single union and customs union.

- Japanese manufacturing activity expanded at a slower pace in February (PMI down to 54 from 54.8) as growth of new export orders slowed due to the yen's appreciation.

- Australian wages rose a tad faster than forecast in Q4. Wages increased by 0.6% Q/Q and 2.1% Y/Y. However, a RBA rate hike is still some distance away.

- Today’s eco calendar contains EMU PMI’s, the UK labour market report, US existing home sales and FOMC Minutes. The US taps the market. Fed Harker speak on the eco outlook while several BoE members testify to Parliament

Currencies: Dollar Tries To Fight Back

More underperformance of US Treasuries?

Global core bonds started on a weak footing yesterday morning. US Treasuries had some catching up to do following Monday’s President’s Day Holiday, but the Bund lost ground as well (higher-than-expected German PPI). The intraday downside was rapidly exhausted with core bond markets returning to opening levels (US Note future) and beyond (German Bund). US Treasuries underperformed German Bunds. The start of this week’s heavy US supply operation went plain vanilla. US yields ended 1 bp (7-yr) to 2.9 bps (2-yr) higher. Changes on the German curve varied between -0.5 bps (5-yr) and +0.8 bps (30-yr). 10-yr yield spread changes vs Germany widened up to 3 bps with Greece underperforming (+11 bps).

The US Note future trades near yesterday’s official close. Asian stock markets don’t copy WS losses, but risk sentiment seems fragile. Oil prices lose some ground. We expect a neutral opening for the Bund.

Today’s eco calendar heats up with EMU PMI’s and FOMC Minutes. The composite PMI hit a multiyear high in January. A small setback is expected today, but PMI’s will still point at good growth levels going forward. They probably won’t move markets. The US’s heavy supply operation continues with amongst others a 5-yr Note auction against a background of an uptrend in yields and a projected increase in the US’s twin deficit. FOMC Minutes will probably be hawkish in line with the Fed’s previous statement in which it twice added the word “further” in relationship with more tightening. US events could push additional downward pressure on US Treasuries, with more underperformance vs Bunds. US yields are near cycle highs and might be attracted by key resistance levels (eg US 10-yr yield 3.05%; 2014 high). Philly Fed Harker speaks on the economic outlook. He’s a non-voter this year who favoured 2 rate hikes in his previous public address early February.

Strong growth momentum, rising inflation (expectations) and the global turn towards monetary policy normalization are structurally negative factors for core bonds medium term. US and German yields cleared resistance levels earlier this year and are moving towards next targets. The trading band for the US 10-yr yield is 2.64%-3.05%. The German 10-yr yield’s trading band is 0.62%-1.06%. Correction towards the lower bounds could be used to put up short positions in the Bund and the US Note future.

German Bund consolidates around sell-off lows

USD tries to fight back

The dollar extended its the gradual rebound yesterday. German ZEW sentiment was better than expected, but didn’t help the euro. Interest rate differentials widened in favour of the dollar. The US 2-yr auction was a bit sluggish, but with little impact on global markets. EUR/USD declined in the 1.23 big figure, drifting further away from the key 1.2555/98 resistance area. The pair closed the session at 1.2337. USD/JPY finished the day at 107.33.

Most Asian equities show modest gains this morning, supported by a gradual further rise of the USD (despite the negative WS close). USD/JPY is drifting to the high 107 area. EUR/USD trades near 1.2325. Australian wages grew slightly faster than expected in Q4 (0.6% Q/Q; 2.1% Y/Y). AUD/USD ticked briefly higher, but turned back south in line with overall USD strength. An RBA rate hike isn’t around the corner yet.

February EMU PMI’s will be published today. A modest decline from historically high levels is expected. The impact on the euro should be limited. In the US, the PMI’s, existing home sales and the Minutes of the January Fed meeting will be published. The Treasury will sell 2y floating rate Notes and 5y bonds. We expect the Minutes to be modestly hawkish. The auction might keep US yields under upward pressure. Over the previous days, the dollar staged a cautious rebound. This rebound might still go a bit further today. US equities show tentative signs of underperformance. Of late this context was often mildly USD positive. From a technical point of view, EUR/USD 1.2555/98 (correction top, 62% retracement) is a key resistance. A break would indicate more trouble for the USD. Economic fundamentals don’t call for a break, but USD sentiment stays fragile. We expect EUR/USD to hold the 1.2598/1.2206 band.A downside break would call of the ST USD alert.

Sterling regained some further traction yesterday as markets hoped for a more constructive approach from the EU in the Brexit negotiations. At the same time, the pressure from hardline Brexiteers on PM May persists. Today, the UK labour data will be published. Employment growth is expected solid, but wage growth might remain modest (2.5% Y/Y). Over the previous days, sterling was better bid as the test of EUR/GBP 0.8930 was rejected. However, we don’t expect this move to go very far as long as there is no real progress on Brexit

EUR/USD: drifting back south in the 1.2206/1.2555 ST range

Elliott Wave Analysis: AUDUSD Update

AUDUSD is nicely falling away from 0.7988 level, where corrective blue wave b found a top. We can see that Fibonacci ratio of 61.8 also proved to be good region of resistance and helped push price lower. That said, we now think blue wave c can take price lower towards the 0.7760/0.7650 in upcoming sessions.

On the second scenario, we see price trading in a bearish reversal, with recent temporary recovery representing corrective wave 2, with more weakness to follow.

AUDUSD, 4H

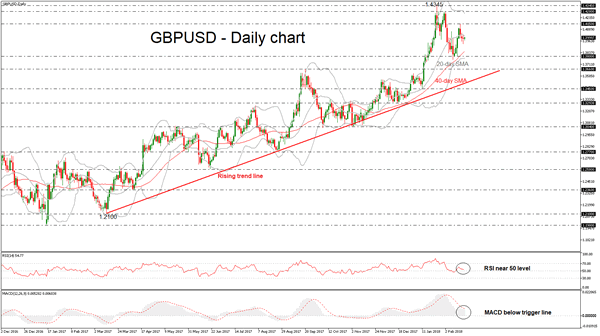

GBPUSD Bearish Retracement In Progress In Short-Term, Next Immediate Support 1.38

GBPUSD remains under pressure and risk is still to the downside as prices continue to drift lower from the 1.4150 resistance level. The short-term technical indicators are bearish and point to more weakness in the market, while the price capped by the 20-day simple moving average of the Bollinger band.

Looking at the daily timeframe, the Relative Strength Index (RSI) is moving in the positive territory and is approaching the 50 level. Also, the MACD oscillator is holding below its trigger line, however, is still holding above the zero line.

Remaining in the same timeframe, if price continues the downside retracement and extends its losses, it could open the door for the 1.3800 strong psychological level. If there is a fall below the latter level, there would be scope to test the next immediate support of 1.3770, which is near with the lower Bollinger band.

To the upside, cable could move towards the 1.4150 resistance level, taken from the peak on February 16. A break above the aforementioned obstacle could take the price towards the 1.4280 resistance level, which is standing near the upper Bollinger band.

Forex Analysis: Jobs Report For UK, PMIs For Europe And US, Along With FOMC Minutes

There is a busy day of Economic Data ahead, starting with PMIs for European countries and the Eurozone as a whole. PMI Data across the Euro block has been improving but the consensus is for a slight drop in figures today. The UK Jobs data then follows, with most data points expected to be in line with expectations. However, Claimant Count Change is expected to be lower, and while this data is volatile at the best of times, the January number is particularly so as seasonal workers are released from contracts from the Christmas period. BOE Members will testify in parliament in the afternoon, followed by US PMI data and FOMC minutes this evening. Chinese traders will return from Spring Festival celebrations tomorrow.

The US Treasury auction sold $179B to drive yields to the highest in ten years. US Stock markets slipped lower following the sale, to finish just off the lows.

Eurogroup meetings will take place today and this may impact on moves in EUR crosses.

German Producer Prices Index (MoM) (Jan) was 0.5% v an expected 0.3%, from 0.2% previously. Producer Prices Index (YoY) (Jan) was 2.1%v an expected 1.9%, from 2.3% previously. EURUSD reached a high of 1.23915 before selling off to 1.23449 after the release of this data.

German ZEW Survey – Current Situation (Feb) was 92.3 v an expected 93.9, from a prior 95.2. ZEW Survey – Economic Sentiment (Feb) was 17.8 v an expected 16.0, from 20.4 previously.

Eurozone ZEW Survey – Economic Sentiment (Feb) was released, coming in at 29.3 against an expected 28.4, from 31.8 previously.

Eurozone Consumer Confidence (Feb) was 0.1 v an expected 1.0, from a previous reading of 1.3. EURGBP sold off from a high of 0.88318 to a low of 0.88109 following this data release.

Japanese All Industry Activity Index (MoM) (Dec) was released, as expected, at 0.5%, from 1.0% prior.

EURUSD is unchanged overnight, trading around 1.23328.

USDJPY is up 0.37% in early session trading at around 107.724.

GBPUSD is down -0.04% to trade around 1.39880.

AUDUSD is down -0.29% overnight, trading around 0.78582.

Gold is down -0.14% in early morning trading at around $1,327.40.

WTI is down -0.58% this morning, trading around $61.22.

Major data releases for today:

At 08:00 GMT, the ECB’s Non-Monetary Policy meeting will take place and this may impact on moves in EUR crosses.

At 08:15 GMT, Swiss Industrial Production (YoY) (Q4) will be released, with a previous value of 5.5%. Industrial Production (QoQ) (Q4) will also be released, with a previous value of 8.6%. CHF crosses may increase in volatility after this release.

At 08:30 GMT, German Markit Manufacturing PMI (Feb) is expected to come in at 60.6 from 61.1 previously. Markit Services PMI (Feb) is expected at 57.0 v 57.3 previously. Markit PMI Composite (Feb) is expected to be 58.5 from 59.0 prior. EUR traders will be closely following this data release.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Feb) is expected to come in at 59.3 from 59.6 previously. Markit Services PMI (Feb) is expected at 57.6 v 58.0 previously. Markit PMI Composite (Feb) is expected to be 58.5 from 58.8 prior. EUR crosses could see a spike in volatility should the data released differ from the consensus.

At 09:30 GMT, UK Average Earnings Excluding Bonus (3Mo/Yr) (Dec) is expected unchanged at 2.4%. Claimant Count Change (Jan) is expected at 4.1K from a previous reading of 8.6K. ILO Unemployment Rate (3M) (Dec) is expected to be unchanged at 4.3%. Average Earnings Including Bonus (3Mo/Yr) (Dec) is expected to be unchanged at 2.5%. Claimant Count Rate (Jan) was 2.4% previously. Public Sector Net Borrowing (Jan) is expected to be £-11.100B from £0.979B prior. GBP crosses could be influenced by this data release.

At 14:00 GMT, FOMC Member Harker will speak, with his comments potentially influencing prices in USD and US assets.

At 14:15 GMT, BOE Governor Carney and MPC Members Broadbent, Haldane and Tenreyo will take part in the Parliament’s Treasury Committee Hearings and Inflation Report Hearings. Comments made here may potentially influence prices in GBP crosses.

At 14:45 GMT, US Markit Manufacturing PMI (Feb) is expected to come in at 55.4 from 55.5 previously. Markit Services PMI (Feb) is expected at 54.4 v 53.8 previously. Markit PMI Composite (Feb) is expected to be 54.0 from 53.3 prior. USD crosses may be heavily traded as a result of this data.

At 19:00 GMT, the Federal Open Market Committee Minutes will be published from the last meeting three weeks ago. Traders will look for changes in the text of the previous meeting’s minutes that may point to policy adjustments impacting future interest rates.

At 23:50 GMT, Foreign Investment in Japanese Stocks (Feb 16) is expected to be in the region of the previous number of ¥-429.5B. Foreign Bond Investment (Feb 16) was ¥-973.2B previously. The report is released by the Ministry of Finance, detailing the flows from the public sector, excluding the Bank of Japan. The net data shows the difference of capital inflow and outflow. A positive difference indicates net sales of foreign securities by residents (capital inflow), and a negative difference indicates net purchases of foreign securities by residents (capital outflow).

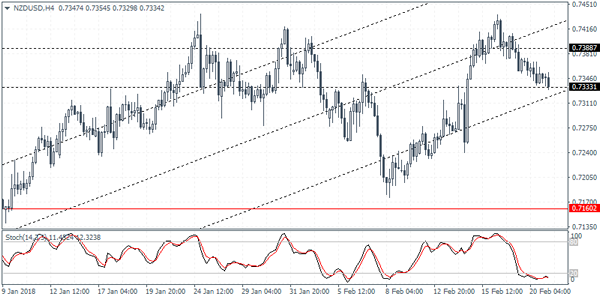

NZDUSD Intraday Analysis

NZDUSD (0.7334): The New Zealand dollar has been gradually posting a decline with price action now trading close to the 0.7333 level of support. As long as the support holds NZDUSD could remain biased to the upside. However we expect NZDUSD to consolidate within the range of 0.7388 and 0.7333 region. This sideways consolidation could see NZDUSD likely to break down to the downside targeting the lower support at 0.7160. To the upside, if NZDUSD clears the upper range of 0.7388, then we can anticipate further gains in the near term.

GBPUSD Intraday Analysis

GBPUSD (1.3985): The GBPUSD closed with a doji yesterday but price action remains biased to the downside, targeting 1.3902. For the moment, the consolidation taking place at the current levels could indicate further declines on a break down below 1.3902. In the event that GBPUSD breaks below this support level, we expect to see the declines being extended down to 1.3611 - 1.3589 level of support where price action is yet to retest the support at this zone. To the upside, the gains are capped near the previous resistance level of 1.4127.

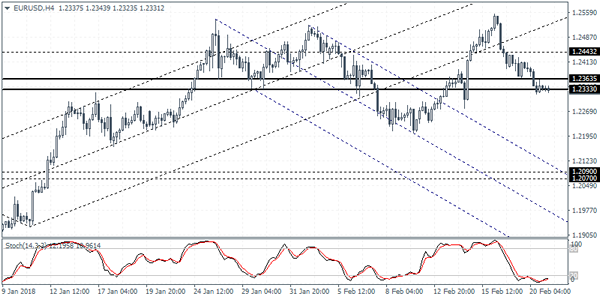

EURUSD Intraday Analysis

EURUSD (1.2331): The EURUSD continued to post declines for the third consecutive day yesterday. However, price action is limited within the range established in the past month. Currently, EURUSD is seen consolidating near the support level of 1.2363 - 1.2333 region. There is a potential for EURUSD to post a rebound of this level. This could send EURUSD back to test the minor resistance level at 1.2443. Alternately, if EURUSD breaks past the support level, the declines could see EURUSD falling to the 9 February lows of 1.2205 where support could be established. Further downside momentum could see EURUSD testing the major support level at 1.2090 - 1.2070.

Investors Brace For Hawkish Fed Minutes

The U.S. dollar continued to rise higher on Tuesday as the U.S. markets opened after a long weekend. Economic data was sparse for the most part. The USD managed to remain strong as investors focused on the upcoming FOMC meeting minutes.

In the Eurozone, the ZEW economic sentiment survey showed that German economic sentiment rose to 17.8, beating estimates of 16.0 while the Eurozone economic sentiment was also higher at 29.3. However, both the indexes were weaker compared to the previous month.

Looking ahead, the FOMC meeting minutes today will stand out amid a somewhat busy day ahead. Data from the Eurozone will cover the flash manufacturing and services PMI figures for February.

In the UK, the monthly jobs data will be coming out. No major changes are expected as economists forecast that the UK's unemployment rate will remain unchanged at 4.3%. Wage growth is also expected to remain broadly stable.

Treasury Will 5Y Notes As Well As 2Y Floaters

Market movers today

The main event today is the FOMC minutes from the January meeting. The statement has not changed significantly but the minutes may give an overview of the different opinions within the Fed. In particular, we are interested if the minutes will indicate whether the tax reform will cause more rate hikes than the three the Fed signalled in December. We still expect an increase in the interest rate at the next Fed meeting in March.

Furthermore, the US Markit PMI service and manufacturing indices for February are due for release. We estimate Markit PMI manufacturing rose further to 56.5 and the service index to rise in February, up to 54.

In the euro area, February's PMI figures are due for release. Manufacturing PMI saw a large fall to 59.6 in January and the leading order-inventory indicator has been declining since October 2017, pointing towards lower manufacturing output in the near future, while the extremely high optimism for the manufacturing sector is likely to be exhausted and head to lower levels. We expect manufacturing PMI to be 59. 3 in February and believe that service PMI is also set for a similar decline to 57.6.

In the UK, focus is on the labour market report for December. We estimate that the unemployment rate (3M average) i s unchanged at 4.3%. The report is important, as the market is trying to assess whether the Bank of England will hike as early as May .

In Norway, we will get LFS jobless data for December, and we expect a modest decline on the back of the modest decline in the NAV's numbe rs.

Selected market news

There is significant focus on this week's US Treasury auctions given the possible impact on both the dollar and global bond markets – whether investors require a higher premium to buy dollar assets given that the hedging costs for non-US investors continue t o rise. At yesterday's auction the yield on the 2Y notes was the highest in a decade, but demand at the auction was decent. Today, the Treasury will 5Y notes as well as 2Y floaters.

The US equity market closed in the ‘red' with a decline in the major indices. The VIX index also moved higher although a modest pace. Hence, the uncertainty is still there. The negative sentiment from the US has sent the Asian equity markets lower as well this morning. The dollar has been range bound relative to the yen and the euro. The Swedish kroner is test ing the 10 level versus the euro after the lower-than-expected Swedish inflation data released yesterday.

The Swedish bond market also rallied yesterday and outperformed EU peers. Hence, there will be significant focus on the Swedish borrowing requirement . We expect to see solid demand at the Swedish government bond auction today.