Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.79; (P) 107.08; (R1) 107.61; More...

USD/JPY's rebound from 105.54 continues today but after all it's staying below 108.72 support turned resistance. Intraday bias stays neutral and near term outlook remains break. Below 105.54 will extend the larger fall from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 107.72 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

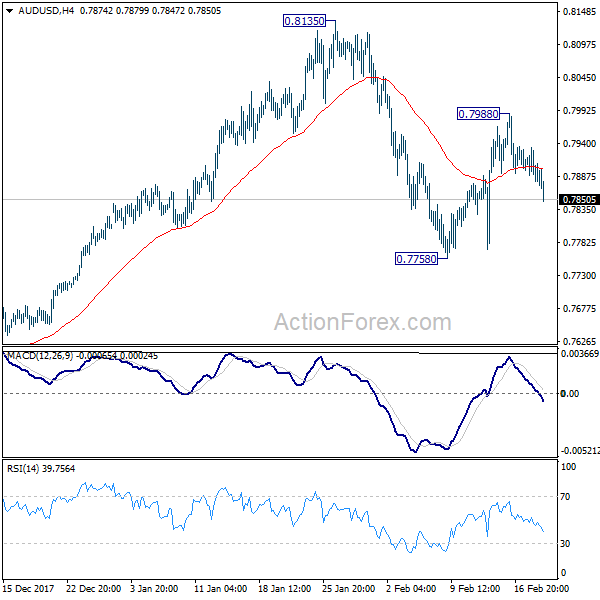

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7860; (P) 0.7897; (R1) 0.7919; More...

AUD/USD is staying in range of 0.7758/7988 and intraday bias remains neutral first. On the upside, above 0.7988 will extend the rebound to retest 0.8135. On the downside, below 0.7758 will resume the fall from 0.8135 and target 0.7500 key near term support. At this point, there is no strong case for a range breakout yet and 0.7500/8135 could hold for a while.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

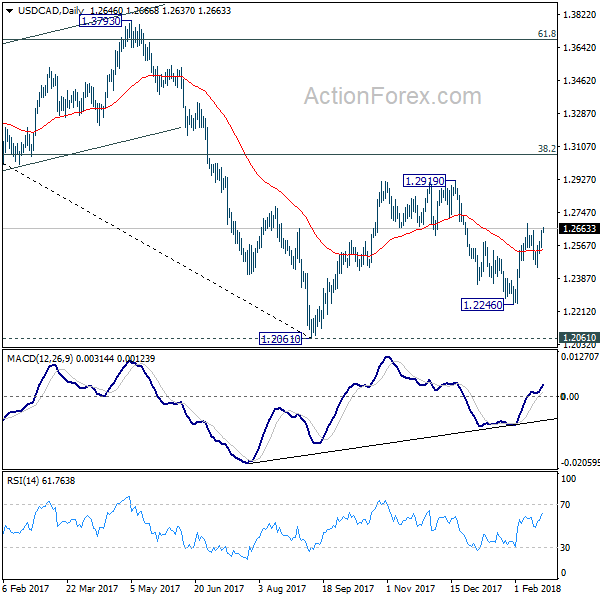

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2559; (R1) 1.2592; More....

USD/CAD rises further today but is still staying below 1.2687 resistance. Intraday bias stays neutral at this point. On the upside, break of 1.287 will resume the rebound from 1.2246 and should target a test on 1.2919 key near term resistance. On the downside, below 1.2450 will target 1.2246 first. Break there will extend the fall from 1.2919 and target 1.2061 keys support level.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA, hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Dollar Rebound Continues as Markets Await Hawkish FOMC Minutes

Dollar's rebound extends further in Asian session today. Momentum is starting to looking promising. But technically, there is still no confirmation of reversal yet. At the time of writing, EUR/USD is held well above 1.2205 key near term support. USD/JPY stays below 108.27 near term resistance. The greenback will look further to FOMC minutes to be released later today. Elsewhere in the currency markets, Euro and Sterling are following Dollar as the strongest ones for today. Aussie and Yen are broadly lower.

FOMC minutes to turn more hawkish

It's generally believed that minutes of the January 30-31 FOMC minutes would show a hawkish twist in the languages The questions is just on the extent. Recent solid data, including job and inflation, are solidifying the case for three rate hikes this year. And markets would now wand to see if more board members are starting to considering four hikes. That would also be tied to policymakers' view on the impact of the tax reform. In addition, markets will look at whether Fed officials are getting more comfortable with the inflation outlook.

Dollar has so far received no support from surging treasury yields, Fed hike expectation, nor the tax reform this year. There is doubt on whether the FOMC minutes could give the greenback sustainable strength. We'll keep an eye on it.

IMF endorses Australia's tax reform

The International Monetary Fund endorsed Australia's move to lower corporate taxes. Thomas Helbling, Division Chief in the IMF's Asia and Pacific Department, said that "for a country like Australia looking at the international standing of corporate tax rates is important and we would endorse that." And according to IMF's annual assessment, broader tax reform could boost GDP growth by as much as 1.3%, through lowering corporate and personal income tax, while increasing GST and introduce a land tax. According to the Treasury, its target to lower corporate tax to 25% could boost growth by 1% when fully implemented in a decade.

Release from Australia, wage price index rose 0.6% qoq in Q4. Construction work down dropped -19.4%.

Japan PMI: Yen appreciation dragged export growth

Japan PMI manufacturing dropped to 54.0 in February, down from 54.8 and missed expectation of 55.2. In particular, new export orders index dropped notably from 57.4 to 54.0, hitting the lowest level in three months. Markit noted in the release that "recent yen appreciation has coincided with slower new export order growth." Also, "a number of panelists indicated that the stronger currency had prompted them to lower prices to overseas customers." And, "further yen strengthening will create unwanted drag on inflationary pressures".

Also from Japan, all industry activity index rose 0.5% mom in December.

Looking ahead

Eurozone PMIs and UK employment data are the main focuses in European session. US will release PMIs, existing home sales and FOMC minutes later in the day.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2559; (R1) 1.2592; More....

USD/CAD rises further today but is still staying below 1.2687 resistance. Intraday bias stays neutral at this point. On the upside, break of 1.287 will resume the rebound from 1.2246 and should target a test on 1.2919 key near term resistance. On the downside, below 1.2450 will target 1.2246 first. Break there will extend the fall from 1.2919 and target 1.2061 keys support level.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA, hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Wage Price Index Q/Q Q4 | 0.60% | 0.50% | 0.50% | |

| 0:30 | AUD | Construction Work Done Q4 | -19.40% | -10.00% | 15.70% | 16.60% |

| 0:30 | JPY | PMI Manufacturing Feb P | 54 | 55.2 | 54.8 | |

| 4:30 | JPY | All Industry Activity Index M/M Dec | 0.50% | 0.40% | 1.00% | |

| 8:00 | EUR | France Manufacturing PMI Feb P | 58 | 58.4 | ||

| 8:00 | EUR | France Services PMI Feb P | 59 | 59.2 | ||

| 8:30 | EUR | Germany Manufacturing PMI Feb P | 60.5 | 61.1 | ||

| 8:30 | EUR | Germany Services PMI Feb P | 57 | 57.3 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Feb P | 59.2 | 59.6 | ||

| 9:00 | EUR | Eurozone Services PMI Feb P | 57.6 | 58 | ||

| 9:30 | GBP | Jobless Claims Change Jan | 2.3K | 8.6K | ||

| 9:30 | GBP | Claimant Count Rate Jan | 2.40% | |||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Dec | 2.50% | 2.50% | ||

| 9:30 | GBP | ILO Unemployment Rate 3Mths Dec | 4.30% | 4.30% | ||

| 9:30 | GBP | Public Sector Net Borrowing Jan | -11.0B | 1.0B | ||

| 14:45 | USD | US Manufacturing PMI Feb P | 55.5 | 55.5 | ||

| 14:45 | USD | US Services PMI Feb P | 54 | 53.3 | ||

| 15:00 | USD | Existing Home Sales Jan | 5.63M | 5.57M | ||

| 19:00 | USD | FOMC Meeting Minutes |

Can GBP/USD Regain Bullish Momentum?

Key Highlights

- The British Pound failed to move above 1.4150 this past week against the US Dollar and declined.

- There is a crucial bearish trend line forming with current resistance at 1.4080 on the 4-hours chart of GBP/USD.

- The UK CBI Industrial Trends Survey Orders Index declined from 14 to 10 in Feb 2018.

- Today, the UK Claimant Count Change figure for Jan 2018 will be released, which is forecasted to come in at 4.1K, less than the last 8.6K.

GBPUSD Technical Analysis

The British Pound made a nice upside move this past week and traded above 1.4100 against the US Dollar. However, the GBP/USD pair failed near 1.4150 and started a downside correction.

The pair declined and traded below the 23.6% Fib retracement level of the last wave from the 1.3799 low to 1.4144 high. It even traded below the 1.4000 support and closed below the 100 simple moving average (red, 4-hour).

However, the downside move found support near the 61.8% Fib retracement level of the last wave from the 1.3799 low to 1.4144 high.

On the upside, there is a crucial bearish trend line forming with current resistance at 1.4080. If the pair moves higher from the current levels, then it could face a strong selling interest near 1.4050 and 1.4080.

A successful close above 1.4080, followed by a break of 1.4100 may open the doors for more gains in the near term. On the downside, the 1.3920-1.3930 support area is important. If the pair declines below 1.3920, there could be further losses.

Today, there are many significant economic releases lined up in the UK, including the Claimant Count Change figure for Jan 2018. The market is looking for a change of 4.1K in the Claimant Count, down from the last 8.6K.

On the other hand, the UK Unemployment Rate is forecasted to remain at 4.3%. Therefore, it would be interesting to see how the British Pound trades after the actual data is out. If the Claimant Count Change figure beats the forecast, there could be an upward move towards 1.4080 in GBP/USD.

On the contrary, if the actual is below the forecast, then the pair could struggle to hold the 1.3920 support level.

Market Morning Briefing: Gold Has Fallen Sharply From Levels Near 1360

STOCKS

Dow (24964.75,-1.01%) fell slightly yesterday. The 21-day MA on the daily line charts seems to be acting as a near term resistance and while that holds, Dow could possibly test lower levels of 24500 24000 in the coming sessions.

Dax (12487.90, +0.83%) continues to trade below 12600. While below 12600,near term looks bearish. As mentioned yesterday, trade within 12600-12300 levels looks possible.

Nikkei (22064.55, +0.64%) is almost stable and seems to have paused near current levels. A break above 22200-22400, if seen could be crucial as that could indicate some near to medium term upmove towards 22800. But there could be some chances that the index remains stable near current levels before coming off towards 21400 or lower. That if seen could lead to some weakness in Dollar Yen as well.

Nifty (10360.40, -017%) has immediate support at current levels and if that manages to hold, we could see a bounce back towards 10500 or higher in the coming sessions. Else a break below current support could turn bearish for the index for the coming weeks.

Sensex (33703.59, -0.21%) on the other hand closed below the immediate support on the daily candles and can test levels of 33250-33000 on Sensex and 10200-10080 on Nifty.

COMMODITIES

63 on the WTI (61.31) seem to be an important resistance that is likely to hold in the near term. While below 63, the price may trade lower and again head towards 60.

Brent (64.86) also could come off to re-test 63 while below 66. Near term look bearish.

Gold (1326.70) has fallen sharply from levels near 1360. While the immediate resistance near 1360-1370 holds, it would be difficult to move up towards 1380-1400 levels in the near term. A re-test of 1300 looks possible with another attempt back towards 1360/70 in the sessions to come.

Copper (3.1855) is down sharply and could come off towards 3.15-3.07 in the coming sessions.

FOREX

As mentioned yesterday as well, the Dollar Index (89.78) is bouncing from support on daily candles near 88.5 towards important resistance just above 90 on the daily and weekly candles. As US bond yields touch new record highs (see Interest Rates below), we could see the Dollar Index touch 90.00-90.25 by Friday.

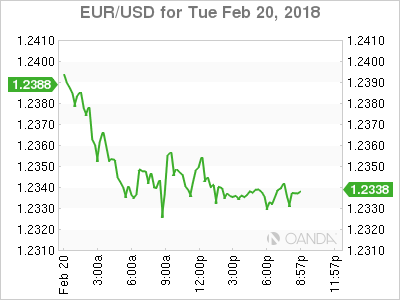

As per expectations, Euro (1.2338) tested 1.235 and is now trading at levels near 1.234. There is support on daily and weekly candles in the 1.2275-1.2315 range, which should be tested this week.

After seeing a low of 105.55 (support on daily candles) last Friday, Dollar-Yen (107.76) has bounced rapidly and is now targeting resistance near 108 on the daily candles this week itself. There could be crucial higher resistance near 109.00-109.25 on the weekly line chart, which could keep the upside restricted in the next week.

The Euro-Yen (132.96) is once again seeing a bounce from crucial support near 132 on the 3 day candles. Yesterday, we had spoken about the possibility of Euro Yen breaking below 132 this week if the Dollar Yen stays below 107.5 and the Euro touches 1.23. However, with a rise towards 108 and a dip towards 1.23 looking likely, we could expect Euro Yen to hover around levels near 132.8-133.0 this week.

Pound (1.3991) is pausing in its forecasted dip towards immediate support near 1.39 on the daily candles. Yesterday's prediction of a test of lower support near 1.38 on daily and 3 day candles would have to be postponed for next week.

Dollar-Rupee (64.7950): With yesterday's rise past 64.70 the long-term trend could be turning to the upside. Within that, there are chances of a near-term correction down to 64.55-50. If that does not happen, we may see 65.20 immediately.

INTEREST RATES

US 10 Year Yield (2.8969), US 30 year Yield (3.1588), US 5 year yield (2.6566), US 2 year yield (2.262) : Yesterday's auction of US 2 Year notes fetched yield rates near 2.255%, which was a reflection of overall bearish sentiments on bond prices (largely driven by high inflation expectations). There is further auctioning slated in this week for the 5 year notes, which might just lead to a rise in the 5 year yield from the current 2.65%. We could expect a sustained elevation of both 2 year and 5 year yields to also pull up the longer term yields above their long term resistance levels. However, there is also a strong possibility of high yield levels attracting investors towards US debt and thereby pushing down yields from current levels. It will be interesting to see how yields behave in the next week.

For the moment, we retain our preference for a dip in the 2 year yield over the next week below 2.2%. (Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

Yield-O-Mania

Yield-o-Mania

Global yields ratcheted higher after a stronger than expected jump on Germany’s PPI which bolsters the hotter than expected comprehensive inflation narrative. But it was the jump in US 2-year note yields that provided the extra boost to the US dollar as shorter-dated tenors provides investors with better goalposts for determining how the market is viewing Fed sentiment

However, the lukewarm demand for two-year notes at auction and with supply concerns expected to weigh heavy on investor bond appetite this week, we could see the dollar back under pressure. Of course, traders are erring on the side of caution ahead of the release of the FOMC Jan 30-31 minutes and given the short dollar bus had reached standing room only portions, the short-term pause in this year’s grand dollar sell-off was not too unexpected.

US stock markets

US equity markets fell overnight on the back of higher US Treasury yields which are providing investors with more income than dividends on the S&P 500 Index. While the prospect of higher interest rates will keep investors on edge, it’s not like we’re returning to double-digit levels or the Fed is moving its terminal rate.So even the uptick in ten-year yields to 3 % or even 3.25 % is unlikely to kill the equity market rally as the benefits from fiscal stimulus should continue to feed through the markets. Investors are banking on much higher returns from equities than bonds again in 2018.

Oil markets

Amid OPEC supply compliance, WTI markets are focusing on dwindling inflow of Crude from Canada to Cushing due to limited accommodation on the Keystone pipeline.The disruption is providing a fillip to WTI prices while the stronger dollar has Brent prices falling and narrowing the WTI-Brent spread. Also, WTI is getting a boost from rising exports attributed to better infrastructure connecting the Permian Basin to the Gulf Coast. But of course, we are tapering expectation on WTI rally as the USD continues to find firmer footing.

Gold markets

A tough week for the Gold market so far as the dollar has rebounded and US Bond yields have jumped higher ahead of the FOMC minutes. Traders are hedging for a possible shift in guidance given the uptick in inflation, so this presents a significant market tail risk which could cause traders to reprice rate hike expectations in 2019 aggressively higher. A quicker and steeper slope of interest rate normalisation offers the most prominent near-term threat to gold prices as this outcome will send the USD surging.

G-10

The Euro

The lack of demand for EUR Monday certainly opened the door, and predictably on the first sign of abject news, we dipped to the low 1.23’s after the German ZEW survey plunged. The market is forever a discounting mechanism and given the extremely disappointing price action from the long perspective; it triggered one-way position squaring ahead of the FOMC minutes. And while the bullish EUR narrative continues to resonate, both bearish and bullish views will be inevitably challenged with Italian elections, January NFP and an ECB meeting due over the next few weeks so near-term convictions could turn neutral and tarnish the EUR appeal

The Japanese Yen

The USDJPY should be the best game in town this week especially if traders interpret the FOMC minute’s colour as bold. However, the risks are balanced entering the FOMC minutes as the recent uptick in volatility could have as much bearing on Fed policy decision as the subtle rise in inflation

But until the market takes out the significant 108.15 level I continue to view the current move as little more than a pre FOMC meeting squeeze driven by yields and positioning and believe there will be substantial resistance between 107.50-108 levels.

The Australian Dollar

Pre-data comments. Given the RBA has been very vocal on wage growth as the missing piece of the economic puzzle, today’s Wage Price Index will attract an unusual amount of focus. Unfortunately, everyone is looking at this trade so the news reading algorithms will likely get there well ahead of everyone on a surprise uptick.

The Malaysian Ringgit

Riskier currencies are trading on poor footing given the firmer dollar and negative global equity sentiment. And of course, we can not overlook higher US yields which are driving opinions this week. This package of coincidences does not make a very conducive environment for regional risk.

Dollar Rebounds Awaiting Fed Minutes

Rising inflation could urge central bank to tighten faster

The USD rebounded against on Tuesday with North American markets coming out of a long weekend. The correlation between rising US bond yields and currency strength had broken down this year, but it now back on track with the 10 year Treasury note hitting a 10 year high driven by higher inflation expectations. The Fed has been divided internally on how to proceed in a slow inflation environment, but if prices suddenly accelerate there will not be need for debate with a higher pace of interest rate moves expected from the central bank. The January Federal Open Market Committee (FOMC) meeting was seen as hawkish and marked the end of Janet Yellen’s tenure. The notes from that meeting will be published on Tuesday, February 21 at 2:00 pm EST with the market scanning the documents looking for clues on the central bank’s views on inflation.

- CME FedWatch puts US interest rates 25 bps higher in March

- French, German and European flash PMIs expected to show slowdown

- FOMC minutes to provide clues on Fed’s inflation outlook

Market looking for clues on March rate decision

The EUR/USD lost 0.57 percent on Tuesday. The single currency is trading at 1.2336 with the USD regaining some traction after the Presidents’ Day holiday. The US dollar hit a three year low last week and it triggered some profit taking from dollar bears ahead of the release of the Fed’s minutes from the January FOMC meeting. The meeting went as expected on January 31 with the rate untouched at its 1.25 to 1.50 percent range. The statement provided few clues but the market zeroed in on the Fed anticipating inflation to reach the 2 percent target in the medium term.

The members of the FOMC have been divided between those that would rather hike now and let inflation catch up, to those more dovish who want higher inflation before raising interest rates. The final meeting chaired by Janet Yellen was hawkish by removing all the transitory factors and with a higher inflation outlook. The market is pricing in a 83.1 percent probability of a rate hike on March 21 as seen in the CME FedWatch tool.

The US central bank has forecasted 3 to 4 interest rate lifts this year. Several members of the FOMC have backed this view in their personal statements and with multiple signs of higher inflation the market, but the question remains. Why is the USD so low? The Fed hiked three times in 2017 and the market has once again priced in a Fed enacting a tighter monetary policy. Growth in the US is also expected to keep gaining at the same rate, but issues with political stability and rising twin deficits have made investors flock to other safe havens instead of the American currency.

European manufacturing data will kick off the Wednesday economic calendar. Flash PMIs for the EU, France and Germany will be published starting at 3:00 am EST with forecasted slowdowns across the board. If manufacturing in Europe is facing a slowdown it could add further momentum to a rising dollar if the minutes from the Fed meeting follow through on the hawkish Fed statement from January 31.

Market events to watch this week:

Wednesday, February 21

4:30am GBP Average Earnings Index 3m/y

2:00pm USD FOMC Meeting Minutes

Thursday, February 22

4:30am GBP Second Estimate GDP q/q

8:30am CAD Core Retail Sales m/m

11:00am USD Crude Oil Inventories

4:45pm NZD Retail Sales q/q

Friday, February 23

8:30am CAD CPI m/m

Gold Slides On Concerns Of Fed Tightening As Fed Minutes Loom

Gold has posted sharp losses in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1330.89, down 1.16% on the day. On the release front, there are no US events on the schedule. On Wednesday, the Federal Reserve will publish the minutes of its January meeting. As well, the US will release Existing Home Sales.

Gold continues to fluctutate, and the base metal has surrendered much of last week’s gains. Investor fears of more rate hikes from the Fed sparked the turbulence in global stock markets, and gold has shown volatility, as gold prices are sensitive to moves (or expected moves) in interest rates. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four, or even five times in 2018. This sentiment is weighing on gold, and traders should expect more volatility on Wednesday, as the Fed may show some of its cards regarding future rate policy.

It’s been a busy start for Jerome Powell, who has just commenced his stint as chair of the Federal Reserve. Strong US data in recent weeks has raised speculation that the Fed may need to accelerate the pace of interest rate hikes in 2018. Meanwhile, concern over higher inflation and more rate hikes sent the stock markets into a frenzy earlier in February. Powell sought to reassure the markets that the Fed was monitoring the situation, but it’s doubtful that the Fed can do much to prevent volatility in the markets.

Pound Hovers At 1.40, British Job Reports Next

The British pound is trading quietly for a second straight day. In Tuesday’s North American trade, GBP/USD is trading at 1.3990, down 0.07% on the day. On the release front, there are no US events on the schedule. In the UK, CBI Industrial Order Expectations continues to lose ground, and slowed to 10 points in February. This was shy of the estimate of 12 points and marked a 4-month low. Wednesday has a host of market-movers, so traders should be prepared for some movement from the pair. The UK releases wage growth and unemployment rolls, and the Federal Reserve will publish the minutes of its January meeting. As well, the US will release Existing Home Sales.

The focus will be on UK employment numbers on Wednesday. Wage growth is expected to remain at 2.5% for a third straight month. Claimant Count Change is expected to slow to 2.3 thousand, and the unemployment rate is expected to remain at 4.3%, where it has been pegged since July. The markets will also be keeping a close eye on BoE Governor Mark Carney, who will testify on inflation before a parliamentary committee. Consumer inflation continues to run at a brisk pace of 3%, well above the BoE target of 2%. This has eroded the purchasing power of the British consumer and also dampened consumer confidence.

It’s been a busy start for Jerome Powell, who has just commenced his stint as chair of the Federal Reserve. Strong US data in recent weeks has raised speculation that the Fed may need to accelerate the pace of interest rate hikes in 2018. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four, or even five times in 2018. Meanwhile, concern over higher inflation and more rate hikes sent the stock markets into a frenzy earlier in February. Powell sought to reassure the markets that the Fed was monitoring the situation, but it’s doubtful that the Fed can do much to prevent volatility in the markets.