Sample Category Title

WTI OIL Eases after Week-Long Rally; Rising Cloud Continues to Underpin

WTI rose eased on Tuesday after hitting new nearly three-week high at $62.63, as overbought slow stochastic on daily chart suggests that four-day recovery from higher base at $58.10 zone may take a breather.

Rising daily cloud which underpinned recovery in past few sessions now marks immediate support (cloud top lies at $61.46) which should ideally contain as oil market remains boosted by efforts from major oil producers to cut global oil production and stabilize oil markets.

OPEC reported 133% compliance with output cut program in January, adding to positive impact on oil prices.

Bulls need break through $62.86 (falling 20SMA) to generate fresh bullish signal for extension of recovery leg from $58.10 base.

Extended dips below cloud top should find footstep at $60.93/72 (Fibo 38.2% of $58.19/$62.63 upleg / 10SMA) to keep bullish structure intact, otherwise, risk of stronger pullback on firm break below 10SMA would sideline near-term bulls and expose psychological $60.00 support.

Bearish extension below $59.42 (daily cloud base) is needed to neutralize bulls and turn near-term focus lower.

Res: 62.35; 62.63; 62.86; 63.36

Sup: 61.67; 61.46; 60.93; 60.72

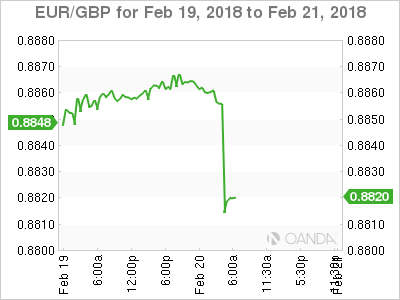

HSBC’s Profit Fails To Impress Lofty Forecast

Share buyback on hold

HSBC to raise more debt

Technical analysis shows upward channel broken

Europe's largest bank produced a set of disappointing numbers today. The company reported a sharp decline in trading income at its investment bank. The bank was badly hit due to the collapse of two high profile borrowers; UK's Carillion PLC and Steinhoff from South Africa. Both pushed the banks bad loan charges to $1.77billion for the year. The South African firm said back in December that it found accounting problems while Carillion actually went bust. The pretax profit in 2017 was less than the Street's estimate (Actual $17.17 billion Est $19.55 billion).

The bank is no longer going to look at the share buyback program which usually boosts the value of the stock and it helps the firm in the longer term perspective. HSBC bought nearly $3 billion worth of shares last year and the incoming CEO does have a plan to continue the process but only after the debt sale is completed.

The below chart shows that we have broken the upward channel and there is a massive gap to the downside after the earning's announcement

Higher Yields Pushing Dollar Up

Overnight, global stock indexes have declined along with U.S futures, while the 'big' dollar has rallied a tad as U.S Treasury yields back up towards their four-year highs.

No central bank meetings are scheduled for this week although minutes from the latest FOMC (Wed) and the ECB meetings (Thurs.) will be published.

Note: Given the forthcoming March FOMC meeting (March 20 -21) when markets expect another +25 bps increase, dealers will be looking for signs that the majority of the committee is aligned for the increase. They also will be looking to see how the FOMC's views on inflation have evolved.

In the U.K, there will be two major releases – the labor market report (Wed) and the second estimate of Q4 GDP (Thurs.) Elsewhere, Canada will post December retail sales (Thurs.) and consumer prices for January (Fri).

With little to no economic U.S data on tap, the markets focus now turns to the U.S Treasury department, which opens its auction floodgates beginning with today's record supply of +$151B of three- and six- month bills (Total new debt supply is +$258B this week).

The U.S debt sales should provide a better market understanding of how steep yields can back up in the short-term.

Note: Fed policy makers speaking this week include NY Fed President Dudley and Atlanta Fed President Bostic and Cleveland Fed President Mester is among speakers at the U.S Monetary Policy Forum in NY.

1. Global stocks see 'red'

Asian equities took their cue from Monday's European bourse direction as U.S stocks and Treasuries took a break for the Presidents' Day holiday.

In Japan, the Nikkei fell -1%, surrendering some of its early-week rise thanks to weakness in its electronics and banking sectors. Selling came despite a slip in the yen outright (¥107.10). The Topix fell -0.7%.

Down-under, the Aussie's S&P/ASX 200 ended flat. In S. Korea, the Kospi fell -1.1%, dragged lower by index heavyweight Samsung Electronics, which dropped another -2% after falling -1.3% on Monday.

In Hong Kong, the Hang Seng Index pared an early slide, down -0.2%, on its first full day of trading in nearly a week. The main benchmark in Singapore fell -0.2%; while Indian's Sensex was last up +0.4%.

Note: With Chinese and Taiwanese markets still closed for the Lunar New Year holiday, investors should be cautioned against reading too much into recent price action due to thin volumes.

In Europe, indices trade mostly higher across the board following the weakness seen yesterday, with the FTSE under performing being weighed on by HSBC and BHP Billiton following results.

U.S stocks are set to open in the 'red' (-0.8%).

Indices: Stoxx600 flat at 378.3, FTSE -0.5% at 7213, DAX -0.1% at 12373, CAC-40 flat at 5257, IBEX-35 +0.2% at 9829, FTSE MIB +0.1% at 22582 , SMI flat at 8907, S&P 500 Futures -0.8%

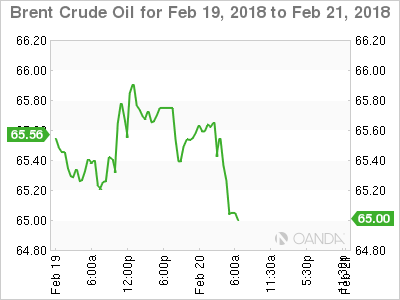

2. Oil markets mixed, Brent and WTI move in opposite directions

U.S crude prices are still carrying momentum from Friday's gains due to yesterday's President Day's holiday while international Brent prices have eased.

U.S West Texas Intermediate (WTI) crude futures are at +$62.31 a barrel, up +63c, or +1% from Friday's close. Ongoing supply reductions from Canada to the U.S due to pipeline reductions are supporting WTI prices.

Brent crude has eased on the back of a dip in Asian stocks and a stronger dollar. Brent crude futures are at +$65.54 per barrel, down -13c, or -0.2% from yesterday's close.

Note: Oil markets remain well supported due to supply restraint by the OPEC. Yesterday, OPEC Secretary-General Barkindo said the organization registered a +133% compliance with agreed output reduction targets in January.

However, soaring U.S production is threatening to erode OPEC's efforts. Last week, the amount of U.S oilrigs drilling for new production rose for a fourth consecutive week to +798.

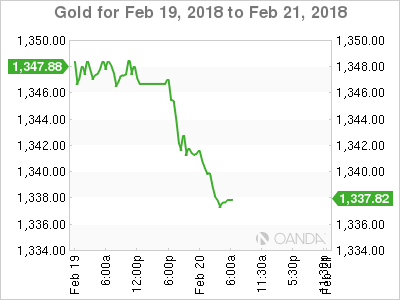

Ahead of the U.S open, gold prices have slid for a third consecutive session as the 'mighty' buck rebounds from its three-year lows, while the market waits Wednesday's Fed minutes for clues on the outlook for U.S interest rates. Spot gold is down -0.2% at +$1,343.22 an ounce.

3. Sovereign yields trade atop record highs

This is a huge week for bond investors, as the U.S Treasury prepares to sell +$258B worth of new debt, starting with today's record sale of +$151B of three- and six- month bills. These debt sales should provide a better understanding of how steep U.S yields could back up in the short-term.

After building up a record “short” position in U.S 2-year futures and historically large short positions across other maturities, higher volatility this month has seen a sharp reduction in these record shorts over the past week.

The biggest reversal was in two-year product – net short positions were slashed by +76,772 contracts to -133,986.

The U.S 10-year is now at +2.92% ahead of the first trading day this week after yesterday's holiday.

In Japan, BoJ Governor Kuroda did not discuss monetary policy during an appearance in parliament. Speculation has been swirling about the possibility the BoJ might scale back its stimulus since they reduced their purchases of JGB's last month.

Down-under, the Reserve Bank of Australia (RBA) reiterated in its minutes of this month's policy meeting that inflation is expected to “only gradually” accelerate as the economy strengthens and wage pressures increase.

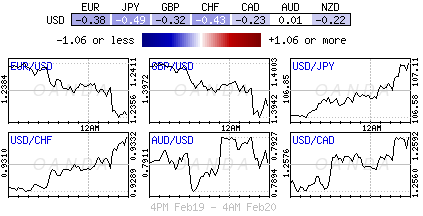

4. Dollar gains against most G7 pairs

Ahead of the U.S open, the U.S dollar has seen some steady gains outright versus G7 currency pairs, aside from sterling. The gains are reflective of U.S yields pushing a tad higher.

Sterling has jumped from its overnight low of £1.3934, to again trade north of the psychological £1.4000 handle on news that the European Parliament is putting a document together outlining its desire for an “association agreement” with post-Brexit Britain. This is a break from the position of the chief E.U negotiator Barnier and could allow Britain to retain “privileged” access to the single market.

5. German ZEW Survey moves off from record highs

Germany's ZEW Indicator of Economic Sentiment recorded a decrease of 2.6 points this month and currently stands at 17.8 points.

The indicator remains slightly below the long-term average of 23.7 points. The assessment of the current economic situation in Germany decreased by 2.9 points, with the corresponding indicator currently standing at 92.3 points.

Comments from ZEW President Wambach: “The latest survey results continue to show a positive outlook for the German economy. The assessment of the current economic situation is still on a very high level and the economy is expected to improve in the coming six months. Economic growth in Germany is substantially driven by the very good development of both the global economy and private consumption. Inflation expectations for Germany and the Eurozone have also started to increase.”

DAX Under Pressure Despite Strong German Releases

The DAX index has posted slight losses in the Tuesday session. Currently, the index is trading at 12,362.98, down 0.19% since the Monday close. On the release front, German and eurozone confidence reports for February beat the estimates, but slowed compared to the January releases. German ZEW Economic Sentiment came in at 17.8, beating the estimate of 16.0 points. Eurozone ZEW Economic Sentiment dropped to 29.3, above the estimate of 28.4. German PPI improved to 0.5%, above the estimate of 0.3%. This marked the strongest reading since January 2017. There are no US releases on the schedule. On Wednesday, Germany and the eurozone release manufacturing PMIs. In the US, the Federal Reserve will release the minutes of its January meeting.

The recent turbulence in global stock markets have sent the DAX lower, and the index has shed 5.9% in February. However, the index rebounded last week, posting a winning week for the first time since mid-January. The catalyst for the gains were positive corporate earnings in Europe. The US recently passed massive corporate and individual tax reform, worth $1.5 trillion. This could significantly boost earnings in Q1 of 2018 for European companies which have major operations in the US, such as banking giants Deutsche Bank and Commerzbank, which are listed on the DAX.

The recent turbulence in the global stock markets has triggered strong volatility in the currency markets, and ECB President Mario Draghi recently stated that the ECB was concerned about the euro’s sharp fluctuations. Last week, Draghi weighed in on Bitcoin, a cryptocurrency which has seen wild fluctuations in recent months. There are growing calls for regulation of these currencies, and central banks could play a key role in such regulation. However, Draghi poured cold water on any ECB involvement, saying that it was not the ECB’s responsibility to ban or regulate Bitcoin. Draghi added that the ECB was exploring the use of blockchain, a digital technology to monitor bitcoin transactions. France and Germany want to cryptocurrencies on the agenda at the next G-20 meeting, and there is bipartisan support in Congress to adopt new rules to regulate virtual currencies.

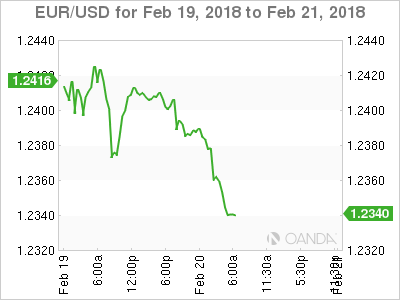

EUR/USD – Euro Slips As German Economic Sentiment Softens

The euro has posted considerable losses on Tuesday, after a slow start to the week. Currently, the pair is trading at 1.2341, down 0.53% on the day. On the release front, German and eurozone confidence reports for February beat the estimates, but slowed compared to the January releases. German ZEW Economic Sentiment came in at 17.8, beating the estimate of 16.0 points. Eurozone ZEW Economic Sentiment dropped to 29.3, above the estimate of 28.4. German PPI improved to 0.5%, above the estimate of 0.3%. This marked the strongest reading since January 2017. There are no US releases on the schedule. On Wednesday, Germany and the eurozone release manufacturing PMIs. The Federal Reserve will release the minutes of its January meeting. As well, the US will release Existing Home Sales.

Federal Reserve chair Jerome Powell has just started his new job, and there is plenty on his plate. Strong US data in recent weeks has raised speculation that the Fed may need to accelerate the pace of interest rate hikes in 2018. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four or even five times in 2018. Meanwhile, concern over higher inflation and more rate hikes sent the stock markets into a frenzy. Powell sought to reassure the markets that the Fed was monitoring the situation, but it’s doubtful that the Fed can do much to prevent volatility in the markets.

Should cryptocurrencies be regulated? The recent turbulence in the global stock markets has triggered strong volatility in the currency markets, and ECB President Mario Draghi recently stated that the ECB was concerned about the euro’s sharp fluctuations. Last week, Draghi weighed in on Bitcoin, a cryptocurrency which has seen wild fluctuations in recent months. There are growing calls for regulation of these currencies, and central banks could play a key role in such oversight. However, Draghi poured cold water on any ECB involvement, saying that it was not the ECB’s responsibility to ban or regulate Bitcoin. Draghi added that the ECB was exploring the use of blockchain, a digital technology to monitor bitcoin transactions. France and Germany want to cryptocurrencies on the agenda at the next G-20 meeting, and there is bipartisan support in Congress to adopt new rules to regulate virtual currencies.

CRUDE OIL Recovery Continues

Crude oil increases back, trading above the 62 range and heading higher. Crude oil is contained between resistance at 64.77 (11/01/2017) and support at 55.82 (07/12/2017 low). The technical structure suggests short-term upside moves.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being, the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Decrease Maintained

Silver is heading lower following recent sideways trading. Silver lies between hourly resistance and support at 17.07 (09/11/2018 high) and 16.03 (05/12/2017 low), heading further down. The technical structure suggests further short-term weakness.

In the long-term, the trend remains negative/ sideways. Further downside is very likely. The pair is trading below its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Failing To Break Resistance At 1366

Gold is trading lower due to strong selling pressure below hourly resistance at 1366 (25/01/2018 high). Hourly supports are given at 1306 (04/01/2018 low) and 1290 (16/10/2017). The technical structure suggests further downside moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Strong Recovery

Bitcoin is trading above 11000, confirming its upward trend and approaching resistance at 12130 (18/01/2018 high). Strong support remains at 5605 (13/11/2017 low). The short-term technical structure suggests further upside moves.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 7'000 - 12'000 in 2018. Bitcoin is trading above its 200 DMA (6'500 range)

EUR/CHF Consolidation At 1.15 Continues

EUR/CHF is trading sideways at the 1.15 range following recent decline at 1.1448 (08/02/2018 low). Hourly resistance is at 1.1685 (26/01/2018 high) while strong resistance remains at 1.1833 (15/01/2018 high). Hourly support is given at 1.1388 (02/10 2017 low). The technical structure suggests further short-term sideways moves.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support can be found at 1.0234 (20/04/2015 low).