Sample Category Title

Dollar Recovery Gains Momentum After Fed Minutes, UK GDP And ECB Minutes Due

Here are the latest developments in global markets:

FOREX: The dollar index was 0.2% higher on Thursday, adding to the notable gains it posted yesterday on the back of the Fed minutes from the January meeting, which were quite upbeat. The greenback moved in tandem with US Treasury yields that surged across the board in the aftermath of the minutes, to reach fresh multi-year highs.

STOCKS: US markets took a hit from the Fed minutes, as speculation for faster rate hikes and higher Treasury yields weighed on risk appetite. The Dow Jones fell 0.7%, while the S&P 500 followed in its tracks, declining 0.6%. The Nasdaq Composite pulled back only by 0.2%. Moreover, futures tracking the Dow, S&P, and Nasdaq 100 are all flashing red at the time of writing, suggesting that volatility will probably remain the dominant theme in equity markets for a while more. The negative sentiment spilled over to Asia as well, with Japan's Nikkei 225 and Topix falling by 1.1% and 0.9% respectively, while Hong Kong's Hang Seng index declined 1.3%. The exception to this pattern were Chinese markets, which posted significant gains on their first day back from holidays. In Europe, futures tracking the major equity indices were a sea of red.

COMMODITIES: Oil prices plunged as the dollar strengthened. WTI is down by almost 1.1% while Brent crude is trading lower by 0.9%, even despite the private API inventory data overnight surprisingly reporting a drawdown in US stockpiles. Today, the oil market will turn its sights to the official EIA inventory data, for a fresh indication of whether US production continues to soar higher. In precious metals, gold is 0.2% lower as well, last trading near $1321/ounce as the firmer greenback made the dollar-denominated metal less appealing.

Major movers: Dollar gains as dust settles after Fed minutes; BoE expects wages to surge

Yesterday, the Fed released the minutes from the latest FOMC meeting. The tone of the minutes was rather upbeat on practically every front. On economic growth, 'most' policymakers judged that recent data suggested a stronger near-term outlook than they had anticipated previously. On inflation, 'most' members noted it would likely move up in 2018 and stabilize around its 2% target over the medium-term, with only 'a couple' of officials expressing concerns on that prospect.

Overall, the minutes painted a picture of a Fed that is becoming increasingly more confident on the economy, even though this meeting took place prior to the surprising acceleration in wages and the stronger-than-anticipated inflation prints for January. Without saying so clearly, the minutes kept the door open for the prospect of four quarter-point rate hikes this year, something that could be signaled as early as at the March meeting provided the economy remains on a strong path. While the knee-jerk reaction in the dollar was lower at the release, the currency quickly recouped all of its losses to trade much higher in the following hours.

Despite this rebound in the greenback though, one must sound a note of caution and reiterate that the broader narrative remains one of USD weakness, amid concerns regarding widening US deficits and longer-term debt sustainability. For this narrative to change and the dollar's downtrend to reverse, it may take something bigger than simply a more upbeat tone in the Fed minutes. In this respect, markets will pay very close attention to Jerome Powell's testimony before Congress next week. The remarks of the new Fed Chair could be the biggest determinant of expectations over what the Fed is likely to deliver this year and thus, the dollar's overall direction.

Sterling/dollar experienced a very busy session yesterday, amid data releases and some remarks from BoE policymakers. The pound fell initially after the UK unemployment rate surprisingly rose, though wages did pick up some speed. Meanwhile, BoE Governor Mark Carney and three other policymakers testified before Parliament. While most comments were a reiteration of what was said at the latest BoE meeting, the officials did deliver a few fresh points, such as the fact that they expect wages to firm and reach 3% soon.

Day ahead: UK GDP, ECB minutes, US jobless claims and Canadian retail sales among Thursday's releases

Thursday's calendar features numerous releases that could spur positioning in the markets.

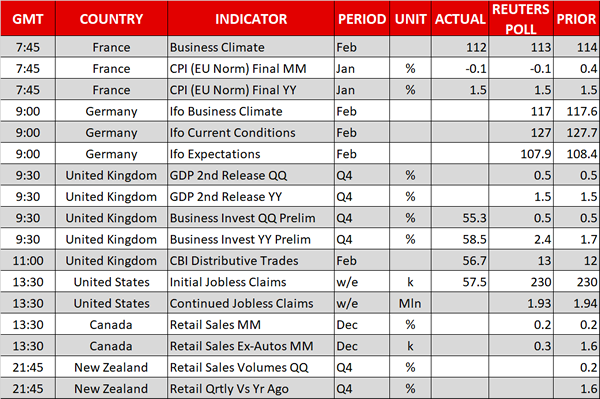

At 0900 GMT, the Ifo Institute for Economic Research will release numerous surveys gauging business sentiment in Germany, Europe's largest economy. All relevant indices - Business Climate, Current Conditions and Expectations - are projected to decline in February relative to January's respective readings, though not by much.

The UK will see the second release of Q4 2017 GDP growth at 0930 GMT. The pace of growth is forecast to remain unchanged at 0.5% and 1.5% on a quarterly and annual basis respectively. Beyond GDP numbers, data on investments by businesses in Q4 2017 will also be made public at the same time, while the Confederation of British Industry's Distributive Trades figure for the month of February is due at 1100 GMT. The latter attempts to measure the change in the volume of orders placed on suppliers during a given month - in this case February - versus the same month a year ago.

The European Central Bank will release its account of the monetary policy meeting that took place in January at 1230 GMT. The minutes from the December meeting took markets by surprise by being more on the hawkish side of the spectrum than markets expected, leading to a rally in the euro. It would be interesting to see if today's release builds on the 'hawkish momentum', propelling the single currency higher.

US initial and continued jobless claims data for the week ending February 17 are scheduled for release at 1330 GMT. Individuals applying for unemployment benefits for the first time are yet again expected to remain below the 300k threshold that's associated to a healthy labor market. Specifically, projections are for the number to stand at 230k, the same as in the week that preceded.

Of importance out of Canada will be retail sales figures for the month of December due at 1330 GMT. New Zealand will also see the release of retail sales numbers for Q4 2017 at 2145 GMT; kiwi pairs would be eyed.

Policymakers making appearances include ECB board member Yves Mersch who is scheduled to give a speech at 0930 at the European Banking Federation's executive committee meeting in Frankfurt. New York Fed President William Dudley - a permanent FOMC voting member - will be participating in an economic briefing on the impact of hurricanes Irma and Maria in Puerto Rico and the Virgin Islands at 1500 GMT. Atlanta Fed President Raphael Bostic - a voting FOMC member in 2018 - will be speaking on Banking at 1710 GMT, with Dallas Fed President Robert Kaplan - a non-voting FOMC member in 2018 - participating in a Q&A session on NAFTA at 2030 GMT.

The Energy Information Administration's (EIA) report including information on US crude and gasoline stocks for the week ending February 16 is scheduled for release at 1600 GMT. Crude inventories are anticipated to increase by around 1.8 million barrels in the period of coverage - around the same as in the previously tracked week - recording their fourth straight weekly rise.

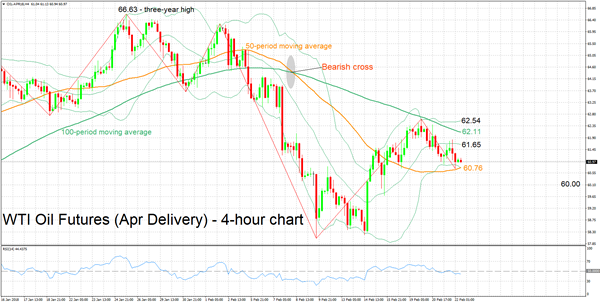

Technical Analysis: WTI oil futures hit one-week low; RSI halts decline

WTI oil futures for April delivery are currently trading not far above 60.72, this being a one-week low recorded earlier in the day. Despite this, the RSI seems to have halted its decline, moving sideways for the most part and projecting a mostly neutral short-term picture.

If the Energy Information Administration's weekly report shows a smaller-than-anticipated increase in US crude oil inventories, prices could advance. In this scenario, resistance could come around the middle Bollinger line - a 20-period moving average line - at 61.65. Further above, and given stronger bullish movement, the attention would shift to the area around the current level of the 100-period MA at 62.11.

On the other hand, should crude inventories rise by more than projected, then prices could post losses. In this case, the area around the current level of the 50-period MA at 60.76 might provide support. Notice that the lower Bollinger band coincides with the 50-period MA. A downside violation would turn the attention to the 60 handle, this being a level of potential psychological significance.

USDJPY Faces Weaker Movement After Four Green Days, Remains Below Symmetrical Triangle

USDJPY recorded four bullish trading days in a row following the rebound on the 15-month low near the 105.50 support level. The aggressive bearish rally in the previous week started after the fall below the 50.0% Fibonacci retracement level near 108.80 of the up-leg with the low of 98.96 and the high of 118.60 and drove the price below the medium-term symmetrical triangle, which has been holding since May 2015.

Currently, the price is developing near the lower band of the triangle with weaker momentum than the previous days but there is a possible scenario of a jump above the 108.00 handle. The upside bias is also confirmed by the technical indicators in the daily timeframe.

From the technical point of view, the MACD oscillator is moving slightly higher in the negative territory and posted a bullish cross with its trigger line, suggesting further gains. Moreover, the stochastic oscillator is extending its upside movement and has entered the overbought zone.

If prices continue the buying interest, immediate resistance could come at 108.20, which is near the 20-day simple moving average. The next significant resistance to have in mind is the 50.0% Fibonacci mark at 108.80. In addition, a jump above the latter level could open the way towards the 40-day SMA around 109.85 at the time of writing.

However, the price has found a strong obstacle on the lower band of the symmetrical triangle and in case of a deeper move down, the focus could shift again to the downside until the 61.8% Fibonacci level near 106.50. Falling below this area could see prices re-testing the 105.50 barrier.

EURO Strongly Bearish Below 1.2292 Level

The euro has continued to move lower against the greenback, with price-action hitting 1.2268 overnight, as traders bought U.S dollar following the release of the FOMC Meeting Minutes. Price-action currently trades around the 1.2270 region, with intraday sellers firmly in control of the EURUSD whilst the pair trades below the 1.2292 technical level. Moving into today’s European session, traders look to the release of the ECB Meeting Minutes from the Governing Councils January 24th to January 25th policy meeting.

The EURUSD pair is strongly intraday bearish whilst trading below the 1.2292 level, further losses towards the 1.2232 and 1.2210 levels remain possible.

Should EURUSD price-action move back above the 1.2292 level, we may see a relief rally towards the 1.2330 and 1.2363 resistance level.

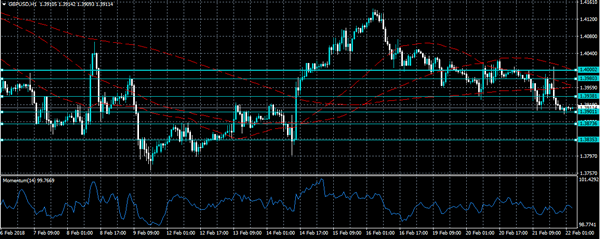

GBPUSD Further Bearish Below 1.3901 Level

The British pound continues to hold around the price-lows of the week against the U.S dollar, as traders remain cautious ahead of the release of key economic data from the United Kingdom. The GBPUSD pair currently trades just above the 1.3900 handle, ahead of the release of the second estimate of fourth fiscal quarter UK Gross Domestic Product. Moving into Thursday’s European trading session, a clear break of the 1.3901 to 1.3938 price-range is likely to define the pairs intraday directional bias.

The GBPUSD pair is likely to experience further losses below the 1.3901 level, key downside support is then found at the 1.3873 and 1.3835 levels.

Should GBPUSD price-action move above the 1.3938 resistance level, buyers may attack the 1.3980 and 1.4000 resistance areas.

The Path Of Least Resistance For Bitcoin

Yesterday, bitcoin fell more than 1000 points. It found its support at the $10,155 level. This drop was purely technical since there was no major negative market-moving data. Potentially, this drop came as traders took profits following a more than 50% gain.

Today, bitcoin has recovered from some of the losses after reports emerged that Bitfinex and Coinbase were introducing a new software to reduce transaction costs by more than 20%. As you possibly know, one of the reasons why cryptocurrencies exist is to make transactions cheaper but this has not been the case. With reduced costs, there is a likelihood that more people and companies will adopt bitcoin.

The adoption of Segwit by these exchanges will ultimately increase the transaction speed, reduce costs, and help create a more vibrant community.

Therefore, with positive news coming internally from exchanges and externally from regulators, in the short term, bitcoin is likely to continue moving up.

Dollar Firms As FOMC Minutes Sound Hawkish

The dollar firmed against the major currencies in early trading today. This followed the release of Fed minutes which showed that officials sounded more upbeat about the US economy. These sentiments bolstered analysts’ estimates that more rate hikes were coming. After the release, the dollar index which tracks the dollar against major currencies rose to the highest level since February 13. Traders now expect the Fed to raise rates in their March meeting.

This week, the euro index which tracks the euro against major currencies fell by 0.52%. Part of the reason for this fall was the stronger dollar. Today, traders will watch for key economic data from key European countries. In France, we will receive inflation data while in Italy, we will get industrial and inflation data. In Germany, business sentiment about the economy is also due out. The Euro index is now trading at a weekly low of 108.19.

The Canadian dollar has been in free fall this week, dropping by more than 1.66% against the dollar. Like in most currency pairs this week, the fall of the pair is associated with a stronger dollar. Today, with insignificant data coming from the United States, traders will focus on retail sales from Canada. They expect core retail sales to grow by 0.1% compared to December’s 1.6%. They also expect retail sales growth to drop from 0.6% to 0.05.

EUR/USD

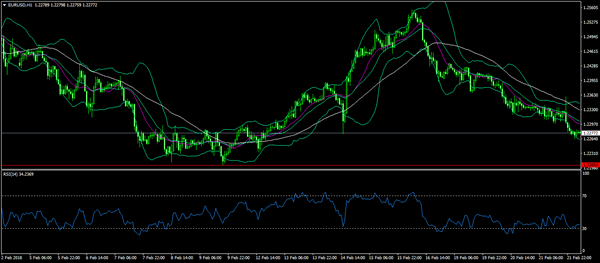

The EUR/USD is trading at the 1.2276 level, which is near a two-week low. Still, the downward trend seems not to be over. As shown below, the RSI of the pair is currently near the oversold level while the Bollinger bands show that more downside could happen. The next price target for the pair is possibly at 1.2205.

USD/CAD

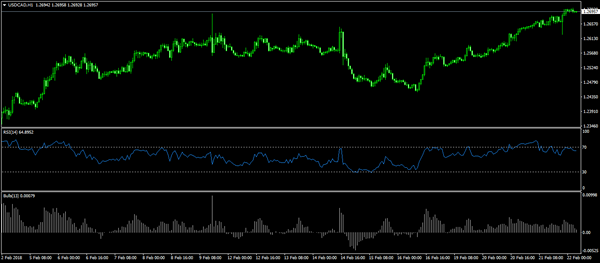

The USD/CAD is trading at 1.2695, which is the highest level since January 27. The pair’s upward trend is more about a stronger dollar and the doubts about the future of NAFTA. As shown below, possibly, the end of this rally could be close since the RSI is near the overbought territory while the Bulls power is diminishing.

EUR/GBP

The EUR/GBP pair has traded sideways in the last few days. As a result, the pair is currently trading at its 25-day and 14-day moving average level of 0.8825. This shows that the pair could break out in either direction. Today’s data from the EU, and the GDP data from the UK coupled with Brexit talks could determine how the pair moves.

Forex Analysis: US Yields Higher Post FOMC Minutes, Stocks Drop, USD Strengthens

German Markit Manufacturing PMI (Feb) was 60.3 v an expected 60.6, from 61.1 previously. Markit Services PMI (Feb) was 55.3 v an expected 57.0, from 57.3 previously. Markit PMI Composite (Feb) was 57.4 v an expected 58.5, from 59.0 prior. EURUSD moved lower from 1.23318 to 1.23168 following this data release.

Eurozone Markit Manufacturing PMI (Feb) was 58.5 v an expected 59.3, from 59.6 previously. Markit Services PMI (Feb) was 56.7 v an expected 57.6, from 58.0 previously. Markit PMI Composite (Feb) was 57.5 v an expected 58.5, from 58.8 prior. EURUSD moved higher from 1.23168 to 1.23393 in reaction to this data.

UK Average Earnings excluding Bonus (3Mo/Yr) (Dec) was 2.5% v an expected 2.4%, from 2.4% previously, which was revised down to 2.3%. Claimant Count Change (Jan) was -7.2K v an expected 4.1K, from a previous reading of 8.6K, which was revised down to 6.2K. ILO Unemployment Rate (3M) (Dec) was 4.4% v an expected 4.3%, from 4.3% previously. Average Earnings including Bonus (3Mo/Yr) (Dec) was, as expected, at 2.5%, from 2.5% previously. Claimant Count Rate (Jan) was 2.3% against a reading of 2.4% previously. Public Sector Net Borrowing (Jan) was £-11.620B against an expected £-11.100B, from £0.979B prior, which was revised down to £0.280B. GBPUSD sold off from 1.39736 to a low of 1.39280 before recovering briefly and then setting a daily low of 1.39043 after this data release.

In his speech, FOMC Member Harker said that US inflation would reach or exceed the 2% goal by the end of 2019. The Unemployment rate is to fall to 3.6% by the beginning of H2 2019 and then retrace higher. US GDP is expected to grow as much as 2.5% this year and 2% in 2019. He also said that a trade war would not be good for the US economy. Changes to the FED’s long-term policy strategy would probably not need legislative change and he was in no rush to make changes to the Fed’s strategy framework. He said that he would have to think long and hard about raising the inflation target. USD moved to a low of 1.07333 from 107.477.

BOE Governor Carney and MPC Members Broadbent, Haldane and Tenreyo took part in the Parliament’s Treasury Committee Hearings and Inflation Report Hearings. Comments made were as follows:

BOE Governor Carney said he does not ever commit to a specific path of interest rates except in exceptional circumstances. He said he generally uses a “conditioning path” and the path at the November report was two rate hikes but is now almost three. He also said that the UK is not in exceptional circumstances currently. The horizon to bring inflation back to the target has moved to less than three years but is not two years in the collective opinion of the MPC. Further stimulus withdrawal will be needed in the coming years. The FX pass-through has a prolonged effect on the UK. The biggest uncertainty is Brexit. The monetary policy is nimble and can react to changing circumstances. The case for a withdrawal of stimulus will arise if GDP exceeds 1.5%. The financial markets are starting to price in rate hikes due to the underlying data.

Carney also said that Brexit uncertainty is weighing on business investment. The traditional boost from the weaker pound on trade has held but there hasn’t been an added boost to investment. He is seeing a variety of indicators that are consistent with firming wage pressures, and most recent figures still show firming in private sector wages ex-bonuses and high-quality job creation. We are probably at the peak point of impact of a weaker sterling on inflation but some impact will last for years. Currency depreciation is not a good economic strategy and makes a country poorer. It was becoming unhealthy how little volatility there was in the markets but it is healthy that the correlation between bonds and equities has changed. A pick up in volatility is not a concern in terms of the path of UK interest rates.

Haldane said that there are reasons for a more hawkish view including a stronger UK and global economy. Momentum was stronger than expected last year. The trade-offs facing rate-setters have been less acute and look set to disappear completely. The slack in the economy is close to being fully absorbed. The level of heightened Brexit uncertainty is a downside risk. The risks in the latest BOE projections are to the upside, with a potential for greater than forecast global momentum. The BOE would hike rates gradually and in a limited manner. There is some distance to travel in order to get back to even 1% productivity in the UK. He also said that it was more likely to see a pickup in wage growth, and that average weekly wage growth would reach 3%.

Broadbent said that the spare capacity in the UK has shrunk and inflationary pressures are firming. Brexit uncertainty is weighing on business investment and if that uncertainty was lifted, then there would be a marked rise in investment. The UK interest rate futures and bond yields are more sensitive to economic news, this is welcome.

US Markit Manufacturing PMI (Feb) was 55.9 v an expected 55.4, from 55.5 previously. Markit Services PMI (Feb) was 55.9 v an expected 54.4, from 53.8 previously. Markit PMI Composite (Feb) was 55.9 v an expected 54.0, from 53.3 prior.

The Federal Open Market Committee Minutes were published from the last meeting three weeks ago. The majority of Fed members say stronger growth increases the likelihood of more hikes, and some officials saw appreciable risk of inflation lag to target. Voters agreed that the recent strengthening of the economy increased the likelihood of further gradual rate increases, and most voters said recent data suggested a modestly stronger near-term economic outlook than was seen in December. A number of policymakers raised near-term economic growth forecasts because of stronger data and info suggesting a larger impact from tax overhauls, and a few said that it was important to monitor the slope of the yield curve. It generally judged risks as roughly balanced but several saw increased upside risks in the near-term and warned imbalances in financial markets may emerge as the economy operates above potential. The EURUSD pair moved up to 1.23596 but then dropped to session lows around 1.22800. USDJPY sold off to a session low of 107.287, before settling higher around 107.665. US stocks rallied initially, with the US 500 Index reaching 2749.9 before selling off to close around 2700.0. Gold tested the 1335.5 resistance before moving lower to a 1321.8 low. US 10-year yields rose to fresh highs of 2.94% not seen since 2014.

Foreign Investment in Japanese Stocks (Feb 16) was ¥127.1B, from an expected value close to the previous number of ¥-429.5B, which was revised down to ¥-430.0B. Foreign Bond Investment (Feb 16) was ¥-553.1B from ¥-973.2B previously, which was revised up to ¥-967.3B.

US Fed’s Quarles delivered a speech titled “10 years after the Global Financial Crisis: How has the world economy changed and where will it go?” at the International Financial Symposium in Tokyo. His comments were: the US economy is performing very well and monetary policy remains accommodative. He anticipates further gradual rate increases and soft inflation is likely transitory. A gradual rise in interest rates is appropriate. Small divergences on the inflation target are not of great concern. He said that the investment drought that has afflicted the US economy may be breaking, and recent US tax and fiscal policy could help sustain the economy’s momentum. The recent volatility in equities shows that asset prices can move rapidly and unexpectedly.

Earlier, US Fed’s Kaskari spoke at a Bloomberg event and made the following comments: the US economy is doing very well, he is surprised at the confidence and optimism due to the tax cut and the best hope is that it leads to greater investment and productivity. He doesn’t really know if US is at full employment and it’s not clear how much of a long-term difference the tax cut will make. We are not sure about neutral rate, or output gap either, and the Fed should be patient and let inflation build. Reaching a 2% inflation target would give the Fed more flexibility in fighting future downturns. We are seeing some signs of inflation building but it takes more than one month’s data and the Fed will respond if inflation starts to show itself. He wants to see definitive signs of inflation rising to 2% before supporting more rate hikes. The Fed could invert the yield curve and tip the economy into recession if it raises rates too aggressively. There could be another million Americans on the side-lines of the labour market, he doesn’t want to cut that off. He is very focused on wage growth, labour market slack, and inflation.

EURUSD is down -0.14% overnight, trading around 1.22648.

USDJPY is down -0.19% in early session trading at around 107.567.

GBPUSD is down -0.26% to trade around 1.38811.

Gold is down -0.25% in early morning trading at around $1,320.99.

WTI is down -0.48% this morning, trading around $61.04.

Major data releases for today:

At 07:45 GMT, French Consumer Price Index (EU norm) (YoY) (Feb) is expected to be unchanged at 1.5%.

At 09:00 GMT, German IFO – Current Assessment (Feb) is expected to come in at 127.0 from 127.7 previously. IFO – Business Climate (Feb) is expected at 117.0 v 117.6 previously. IFO – Expectations (Feb) is expected to be 107.9 from 108.4 prior. EUR crosses could see a spike in volatility should the data released differ from the expected consensus.

At 09:30 GMT, UK Gross Domestic Product (YoY) (Q4) is expected to be unchanged at 1.5%. Gross Domestic Product (QoQ) (Q4) is also expected to be unchanged at 0.5%. GBP crosses could be influenced by this data release.

At 12:30 GMT, ECB Monetary Policy Meeting Accounts may impact on moves in EUR crosses.

At 13:30 GMT, US Continuing Jobless Claims (Feb 9) is expected at 1.930M from a previous number of 1.942M. Initial Jobless Claims (Feb 16) is expected to come in at 230K from a prior reading of 230K. USD crosses may see increased volatility around this data release.

At 13:30 GMT, Canadian Retail Sales Ex-Autos (MoM) (Dec) is expected to be 0.3% from 1.6% previously. Retail Sales (MoM) (Dec) is expected to be unchanged at 0.2%. CAD crosses could be affected by this release.

At 15:00 GMT, US Fed’s Dudley is due to speak about the economic situation in Puerto Rico and the United States Virgin Islands following Hurricanes Irma and Maria at a press briefing hosted by the Federal Reserve Bank of New York. Audience questions are expected afterwards, with comments having the potential to move USD pairs.

At 17:10 GMT, US FOMC Member Bostic is due to speak at the Banking Outlook Conference hosted by the Federal Reserve Bank of Atlanta. Audience questions are expected to follow and this event may impact USD crosses and assets.

At 20:30 GMT, US FOMC Member Kaplan is scheduled to speak and his comments will be followed by traders for any hints on future US FOMC policy.

At 23:30 GMT, Japanese National Consumer Price Index (YoY) (Jan) is expected to be 1.3% against a prior 1.0% in December. National Consumer Price Index Ex-Fresh Food (YoY) (Jan) is expected to be 0.8% against a prior 0.9% in December.

Currencies: USD Nearing First Significant Resistance Area

Sunrise Market Commentary

- Rates: US 10y real interest rate reaches 5-yr high

US yields reached new cycle highs in the wake of FOMC Minutes which shifted market bets more towards a hawkish Fed this year. The US 30-yr yield tests first resistance around 3.21%. Interestingly, the latest increase in US yields is spurred by a rising real interest rate rather than by higher inflation expectations. - Currencies: USD nearing first significant resistance area

The dollar extended gains yesterday as the FOMC minutes were perceived as being on the hawkish side. The dollar is nearing first intermediate resistance. The calendar is rather thin today. In this context, the USD rally might slow. Brexit noise could block the recent (albeit modest) comeback of sterling.

The Sunrise Headlines

- US markets at first shrugged off FOMC Minutes, but faced selling pressure into the close (-0.5%) as the sell-off in core bonds continued. Asian indices lose ground as well with China outperforming (catch-up after Lunar NY holidays).

- Federal Reserve officials signalled growing confidence in the US economy when they met in January, bolstering their plans to continue raising short-term interest rates as soon as next month.

- One of the Federal Reserve's newest policymakers, Quarles, added his voice to the majority at the US central bank calling for interest rate hikes amid rising business optimism and faster growth in the world's biggest economy.

- The BoJ should consider buying foreign bonds as part of efforts to reflate the economy during Governor Kuroda's second term at the central bank helm, an economic adviser to PM Abe said.

- The UK’s cabinet didn’t agree to Theresa May’s negotiating strategy for the Brexit transition period before it was sent to EU nations, the Telegraph reported, citing senior ministers.

- The BoE could end up needing to raise interest rates faster than investors expect, chief economist Haldane told lawmakers, striking a slightly more hawkish tone than his central bank colleagues.

- Today’s eco calendar contains German IFO business sentiment, US weekly jobless claims and details of Q4 UK GDP. Minutes of the previous ECB meeting will be published and Fed Dudley, Bostic and Kaplan speak.

Currencies: USD Nearing First Significant Resistance Area

USD nearing first resistance

The dollar gained further ground yesterday, but initially it occurred only at a snail’s pace. EMU PMI’s disappointed, but had hardly any negative impact on the euro. The EUR/USD decline even stalled early in US dealings. Markets hesitated which way to go after the release of the Fed Minutes. Finally the coin fell to the hawkish side. US bond yields rose further and so did the dollar. EUR/USD dropped below the 1.23 mark and closed the session at 1.2284. USD/JPY closed at 107.78, within reach of the intraday top even as US equities came under pressure at the end of the session. The trade-weighted dollar closed the day exactly at 90.00 (compared to last week’s low of 88.25).

The calendar is moderately interesting today. The German IFO Business climate is expected to ease from 117.6 to 117. Yesterday, the PMI’s declined more than expected and this might also be the case for the IFO. The PMI release triggered a modest intraday decline in EMU yields, but hardly affected the euro. There are plenty of Fed speakers, the ECB publishes the account of the January meeting and the US Treasury sells 7-yr bonds. We don’t see any of these factor containing a trigger for a big USD move. LT US yields are nearing (10y)/testing (30y) key resistance levels. It probably needs high profile news to go for a test/break. In this context, the recent USD rebound might also slow. 90.57 is first resistance for the trade-weighted dollar. First support in EUR/USD (1.2206/1.2165) is coming on the radar. In a day-today perspective, we think it might be a bit too early for a test/break.

The gradual rebound of sterling ran into resistance yesterday. The UK currency returned part of Tuesday’s gain after mediocre UK labour data. Brexit noise remained a negative, too. BoE governors, including Carney, indicated that further rate hikes are on the cards in a hearing before parliament. However they deliberately remained vague on the timing. EUR/GBP returned south to the low 0.8815 area, but a test of the 0.88 big figure didn’t occur. Details of the UK Q4 GDP and the CBI retail data will be published today. PM May and 11 top Ministers meet to clarify the Brexit strategy. Consensus still looks far away. We see little upside for sterling (against the euro) as long as Brexit uncertainty remains as high as it is.

EUR/USD: drifting back south in the 1.2206/1.2555 ST range

Elliott Wave Analysis: Bullish Structure On USDCAD

USDCAD is trading nicely bullish, after a base was found for corrective wave 2 at the 1.2446 level. Current strong rally can be part of wave 3, the strongest and steepest wave, that is also usually the longest. Wave 3 can so approach levels near the 1.297 region, before a new temporary retracement as wave 4 shows up. At the 1.297 area, the upper base channel line and the Fibonacci ratio of 161.8 can offer resistance.

USDCAD, 4H

Fed Minutes Turned Bulls To Bears In 30 Minutes

Volatility soared in equity and fixed income markets in the final hours of yesterday’s U.S. trading session. After dropping to 17, the Cboe Volatility Index gained 19%, ending the day above 20. The S&P 500 reversed a gain of 1% to end the day 0.55% lower. Similarly, the Dow Jones gave up 470 points from peak-to-trough, while U.S. Treasury yields spiked across the curve,and 10-year yields breached2.95% for the first time in four years.

What drove the U-turn?

Initial investor reaction to the minutes of the Federal Open Market Committee meeting was very welcoming. U.S. monetary policymakers marked up their growth forecasts in January, due to firm global growth, supportive financial markets and the potential for tax cuts to boost the economy more than was expected. The updated outlook on the U.S. economic growth sent stocks higher 30 minutes afterthe release of the FOMC minutes. However, this didn’t last long after diving further into the details. What triggered the selloff, in my opinion, was a sentence in page 16 of the FOMC minutes, that stated “a majority of participants noted that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate.”

This led to a repricing of interest rate expectations for 2018. Investors have raised their expectations for three rate hikes this year, to 67.3% from 57% a month ago, while the chance ofa fourthrate hike grew to 30% from 20%.

With more Treasury supply coming in the weeks ahead, breaking above 3% on the 10-year yields looks more likely. Given that Wall Street overreacts on every piece of news, we’re likely to see another sharp leg down when the 3% level is breached.

In currency markets, the dollar soared against its major peers, with the Dollar Index trading back above 90. I’m still not confident that the greenback started responding to higher interest rate differentials. Otherwise, the Yen should have declined, but instead is the top performing currency today. So far, I think it’s the selloff in equities and investor uncertainty that is driving the dollar and the yen higher.

The Euro has fallen 2.2% from the 1.2555 peak reached on 16February, but is still up more than 2.3% for the year. The latest Eurozone PMI releases have shown activity slowed in February and likewise, the German ZEW indicated that confidence eased. However, these economic indicators are just retreating from record highs and do not indicate any serious threat to the Eurozone recovery. Today’s German IFO is likely to show a similar pullback, but traders should take the cue from stock markets and not the economic data.