Sample Category Title

GBPUSD Now Bullish Above 1.3880 Level

The British pound has moved higher against the U.S dollar during the European trading session, reaching an intraday trading high of 1.3915. Buying interest in the GBPUSD quickly accelerated after the pair broke through the 1.3880 level, encouraging further upside towards the 2018 price-high. Financial markets will now turn their attention to a potential resolution of the United States government shutdown, during the upcoming U.S trading session.

The GBPUSD pair has turned bullish above the 1.3880 level, key upside targets remain 1.3944 and the 1.4000 level.

Should price-action on the GBPUSD pair start to trade below the 1.3880 level for an extended period, sellers may test towards the 1.3850 and 1.3810 support zones.

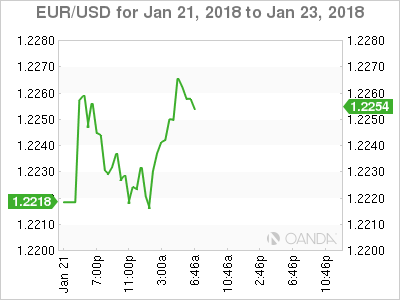

EURUSD Direction Defined by 1.2258 Level

The euro has moved marginally higher against the greenback in early Monday trading as the U.S dollar index starts to retreat, amidst the ongoing U.S Government shutdown. The EURUSD pair has also received a boost, after coalition talks in Germany held over the weekend ended with a largely positive outcome. With a lack of macro-economic news today, technical trading will likely dominate, with the 1.2258 level the key pivot point intraday traders are watching.

The EURUSD pair remains intraday bearish while trading below the 1.2258 level, further losses towards 1.2200 and 1.2150 appear possible.

Should buyers push the EURUSD pair above the 1.2258 level, price-action may press towards the 1.2294 and 1.2320 levels.

DAX Quiet on Lack of Data

The DAX has started the week with little movement. In the Monday session, the index is trading at 13,442.50, up 0.06% on the day. The only two releases on the calendar are the Eurogroup meetings and the German Buba monthly report. On Tuesday, Germany and the eurozone will release the ZEW Economic Sentiment reports. As well, the eurozone will release Consumer Confidence.

Germany's economy continues to outperform its eurozone peers, but the country's current account and budget surpluses have turned into 'too much of a good thing.' A strong demand for German products, record low unemployment and the ECB's expansionary monetary policy have all contributed to the surpluses. What should be done with all these funds? This was a source of disagreement a recent conference in Frankfurt, hosted by the IMF and German Bundesbank. IMF Managing Director Christine Lagarde suggested that Germany should increase public spending. However, Bundesbank President Jens Weidmann acknowledged that the surpluses may be getting too large, but that increasing public expenditures was not the solution.

The US government shutdown has entered its third day, but global stock markets have not reacted negatively, and European stock markets are steady on Monday. Without funding, many non-essential government services have been forced to shut down. Democrats and Republicans are now playing the 'blame game' and pointing fingers at who is responsible for the crisis. The Democrats refused to vote for the spending measure until a deal is hammered out over Daca, an program for children who are illegal immigrants that Trump has threatened to deport. On Sunday, Senate majority leader, Mitch McConnell suggested that he would allow a vote on immigration reform in February if Democrats agree to fund the government. With congressional elections looming, both parties will not want to anger voters, so we could see the crisis resolved this week.

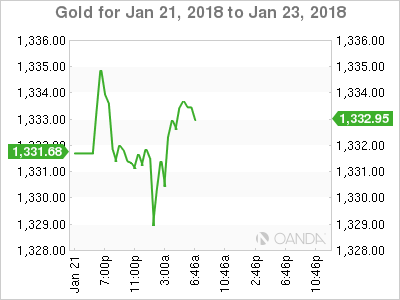

Gold Makes Corrective Move Lower After Challenging New 4-Month High

Gold moved lower over the previous week following the pullback from the 4-month high of 1344. The price snapped the five weekly winning sessions and posted a negative week as it lost momentum. The short-term technical indicators seem to be turning negative and point to more weakness in the market.

In the 4-hour chart, the RSI indicator is pointing slightly to the upside near the 50 level, whilst the MACD oscillator lost its momentum and is flattening near the zero line. Moreover, the 40-simple moving average created a bearish crossover with the 20-SMA, indicating further losses.

If price action remains below 1344 (immediate resistance), there is scope to test the immediate support at 1324. Clearing this key level would see additional losses towards the 1300 – 1305 support zone. Also, falling below it could see prices creating a strong sell-off until the 1263 support level.

Conversely, upside moves are likely to find resistance at 1344. A climb above 1344 could see gains towards the 1357 barrier, which is near the upper boundary of the weekly symmetrical triangle.

It is worth mentioning, in the long-term timeframe, that the price has been trading within a symmetrical triangle over the past two years as it failed to post a higher top from 1375 on June 2016. The price failed to extend its gains above the aforementioned level and has been creating a continuation pattern, indicating a breakdown as the previous tendency was a descending move.

Euro Higher, Investors Look For Cues

The euro has posted losses in the Monday session. Currently, EUR/USD is trading at 1.2256, up 0.31% on the day. In economic news, it's a very quiet start to the week. There are no data releases out of the eurozone, and no indicators in the US. On Tuesday, Germany releases ZEW Economic Sentiment, which is expected to rise to 17.8 points.

It's Day Three of the US government shutdown, which began Friday at midnight when the Senate failed to approve a short-gap spending bill. Without funding, many non-essential government services have been forced to shut down. Democrats and Republicans are now playing the ‘blame game' and pointing fingers at who is responsible for the crisis. The Democrats refused to vote for the spending measure until a deal is hammered out over Daca, an program for children who are illegal immigrants that Trump has threatened to deport. Lawmakers are scrambling to reach common ground, and on Sunday, Senate majority leader, Mitch McConnell suggested that he would allow a vote on immigration reform in February if Democrats agree to fund the government. With congressional elections looming, both parties will not want to anger voters, so we could see the crisis resolved this week.

The German economy is humming, but the country's current account and budget surpluses have turned into ‘too much of a good thing.' A strong demand for German products, record low unemployment and the ECB's expansionary monetary policy have all contributed to the surpluses. What should be done with all these funds? This was a source of disagreement a recent conference in Frankfurt, hosted by the IMF and German Bundesbank. IMF Managing Director Christine Lagarde suggested that Germany should increase public spending. However, Bundesbank President Jens Weidmann acknowledged that the surpluses may be getting too large, but that increasing public expenditures was not the solution. With the German economy far outpacing its eurozone peers, most of them would likely envy Germany's quandary over what to do with its large surpluses.

Central Banks Key To Dollars Short Term Direction

Despite the distraction of a U.S government shutdown, the focus of capital markets this week will return to the more upbeat message of the global growth upswing and a couple of G7 central banks monetary communications.

The Bank of Japan (Tuesday) and the European Central Bank (Thursday) both hold policy meetings and both are expected to leave their respective policies unchanged. Nevertheless, the market will be listening to governor Kuroda and president Draghi for hints of possible policy changes going forward as growth picks up.

In North America, Canada release retail sales Thursday and inflation numbers Friday, while stateside, the U.S will release its initial Q1 estimates of GDP Friday.

Overnight, global equities traded mixed, while sovereign bonds halted a recent selloff as investors assessed the impact of the U.S federal government’s partial shutdown.

Note: The Senate is to vote on later today to try to reopen government and fund it through Feb 8.

The U.S dollar is steady as we enter the third day after Senate leaders failed to end the impasse on the weekend. The EUR has gained on optimism that Germany’s Merkel has made a breakthrough towards her fourth term after the Social Democrats backed formal coalition talks with the Chancellor after their divisive party convention Sunday.

Note: The SPD voted to support the opening of formal coalition talks with Chancellor Merkel’s conservative bloc with vote by 362 to 279.

1. Stocks mixed results

In Japan, stocks produced small gains on Monday, with strength in securities and insurers offsetting falls in resources-related sectors. The Nikkei index was flat, while the broader Topix added +0.1%.

Down-under, afternoon selling took Aussie shares to a fifth consecutive loss and the benchmark to a seven-week low. Settling at the session low, the S&P/ASX 200 dropped -0.2% as the major banks in particular weighed. In S. Korea, the Kospi was down -1.05%, pressured by worries over the U.S government shutdown.

In Hong Kong, equities traded close to flat in the overnight session. Chinese H-shares listed in Hong Kong eased -0.02%, while the Hang Seng Index was down -0.04%.

In China, stocks rose overnight to new two-year highs, helped by gains in the defensive consumer and healthcare firms. The Shanghai Composite index was up +0.22%, while China’s blue-chip CSI300 index was up +0.75%.

In Europe, regional indices trade mixed this morning, with outperformance in the Spanish Ibex ahead of a busy earnings week.

Futures on the S&P 500 Index have dipped -0.1%.

Indices: Stoxx600 flat at 400.7, FTSE +0.1% at 7735, DAX -0.1% at 13423, CAC-40 -0.1% at 5520, IBEX-35 +0.4% at 10519, FTSE MIB +0.1% at 237773, SMI -0.2% at 9494, S&P 500 Futures -0.1%.

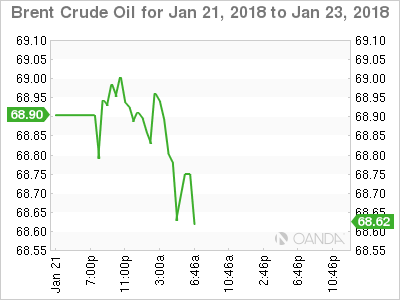

2. Oil rises as Saudi Arabia says producers will cooperate beyond 2018

Oil prices start the week better bid, pushed higher by comments from Saudi Arabia that cooperation between oil producers who are withholding supplies would continue beyond this year.

Strong global economic growth, coupled with a drop in U.S drilling activity is also supporting crude prices.

Brent crude futures are at +$68.84 a barrel, up +23c or +0.34% from Friday’s close. Brent on Jan. 15 rose to +$70.37, its highest print in three-years. U.S West Texas Intermediate (WTI) crude futures are at +$63.53 a barrel, up +16c, or +0.25% from their last settlement. WTI climbed to +$64.89 on Jan. 16, also its highest since December 2014.

Data stateside from Baker Hughes Friday showed that U.S drillers cut five oilrigs in the week to Jan. 19, bringing the count down to 747.

Note: Despite this, the rig count in 2017 and early this year remains much higher than in 2016, resulting in a +16% rise in U.S production since mid-2016, to +9.75m bpd.

Ahead of the U.S open, gold prices have inched as the dollar regained some of its strength after slipping earlier on a U.S government shutdown, with investors on wait-and-see mode. Spot gold has fallen -0.1% to +$1,329.75 an ounce.

Note: Spot gold fell -0.5% last week, it’s first weekly decline in six-weeks.

3. Yields changes on central banks message

Fixed income traders need a push from central bankers to plot the next directional phase for global yields. Currently, global sovereign yields have backed up their to their three year highs. The Bank of Japan and the European Central Bank both have policy decisions this week, before an announcement from the Federal Reserve on Jan. 31.

While no action is expected from any of the three this month, investors will be on alert for the latest signals on withdrawal of policy accommodation after years of unprecedented stimulus. Any ‘dovish’ hints from officials could pull the benchmark U.S 10-year Treasury note yield back – it touched +2.66% on Friday, the highest print since July 2014.

Note: Current technical indicators signal weak support for the U.S 10’s if the yield breaks even higher. However, if policy makers signal they’re hesitant to remove QE – if global rates are going to stay low, at least for this year – sovereign yield should pare back some of their recent gains.

Overnight, the yield on 10-year Treasuries decreased -1 bps to +2.65%, the biggest dip in more than a week. While in Germany, the 10-year Bund yield has advanced less than +1 bps to +0.57%.

4. Dollar’s undoing

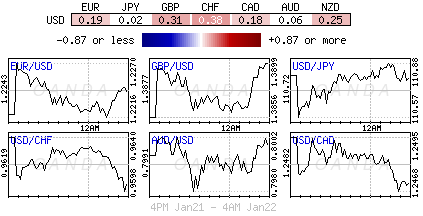

The ‘mighty’ USD is only modestly softer despite the shutdown of the U.S government.

The EUR/USD (€1.2248) remains within striking distance from its three month high of €1.2323 despite the bullish news that Germany’s SDP are willing to enter coalition talks with Chancellor Markel. Market focus now shifts to the ECB rate announcement and in particular the following press conference with President Draghi.

Has USD/JPY (¥110.70) broken its historical correlation with U.S bond yields? Forex dealers have noted that U.S bond yields are not supporting the USD/JPY pair. The Bank of Japan (BoJ) meets later this evening with no change expected in policy, but the market will focus on its forward communication especially on the inflation front.

Note: Japan will release its Dec CPI data on Friday – will an overshoot in the core raise the possibility of the BoJ moving to a normalize policy?

Elsewhere, TRY has weakened outright after Turkey launched a ground operation against Syrian Kurdish militia. From a market perspective, although the operation seemed to be well advertised, the news flow is unnerving for some investors. USD/TRY trades up +0.1% at $3.8100.

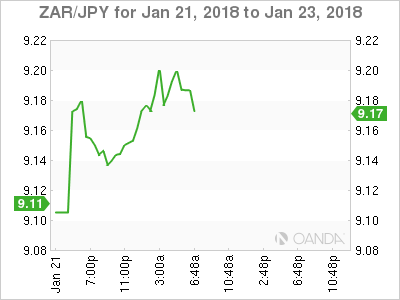

South Africa’s rand ($12.0438) has rallied to its strongest level in nearly three-years on speculation over how much longer President Zuma will remain in power.

5. Davos and World Economic Forum

Barring any last minute changes in Washington, President Donald Trump will join world leaders and senior executives in Davos, Switzerland, for the annual World Economic Forum, which will take place from this Tuesday to Friday.

Note: Trump is due to deliver a keynote address on the final day.

There is a possibility that the U.S President could use this platform to up the “protectionist ante.” Also, expect U.K PM Theresa May to try and “clear the air” with the President, who remains still furious with the way he has been treated by the British government and warned his deteriorating relationship with May is likely to kill any prospect of a swift post-Brexit bilateral trade deal.

US Shutdown, Earnings And Central Banks In Focus This Week

- US Investors Shrug Off Shutdown Concerns;

- Earnings Season Enters Key Period as 82 S&P 500 Companies Prepare to Report;

- ECB and BoJ Monetary Policy Decisions Eyed This Week;

- Bitcoin Off to a Rocky Start Again.

US Investors Shrug Off Shutdown Concerns

As we enter the third day of the US government shutdown, index futures are pointing to only a slightly lower open on Wall Street as investors shrug off the failure to pass a last minute spending bill.

There were some concerns that the shutdown may weigh on investor sentiment and halt what has been another impressive run in US stock markets but as of yet, there’s little evidence to support this. Yes futures are a little lower ahead of the open but these declines don’t even wipe out Friday’s marginal gains which suggests that what we’re seeing is not out of the ordinary.

As long as a solution is found in reasonable time to fund government and reopen the areas that are now closed, I don’t expect investors to concerns themselves much with it. The last shutdown in 2013 lasted 16 days and had minimal, if any, lasting economic impact and it’s this that is likely giving investors the confidence to shrug it off this time around.

Earnings Season Enters Key Period as 82 S&P 500 Companies Prepare to Report

Investors will likely be more concerned with earnings season this week with 82 S&P 500 companies, including nine from the Dow 30, reporting on the fourth quarter. This is therefore one of the busiest weeks in the earnings season and should give us a much better idea of how companies performed in the last quarter, with expectations still be very high.

ECB and BoJ Monetary Policy Decisions Eyed This Week

It’s going to be a very busy week for financial markets, with the political backdrop in the US providing a constant distraction while two major central banks will make monetary policy announcements and a number of key pieces of data will be released. The ECB decision on Thursday will likely be the highlight after the minutes from the previous meeting hinted at policy makers providing insight into policy changes later this year in the coming months.

The Bank of Japan will also be closely monitored after the central bank earlier this month bought slightly fewer bonds than it has in the past, fuelling speculation that it could be preparing to reduce its stimulus measures despite having claimed previously that it would not be doing so. The central bank may utilise this meeting to clarify its position and reassure investors.

Bitcoin Off to a Rocky Start Again

It’s likely to be another volatile week for bitcoin and other cryptocurrencies. Bitcoin staged a slight comeback after a rough start to last week but once again it appears to be struggling to gather any upward momentum. It is currently trading at around $11,500, having fallen close to $9,000 at one point last week and while this looks like a convincing bounce, it’s minor compared to the losses incurred over the last couple of weeks.

Technical Outlook: USDTRY – Strong Bullish Signal On Close Above Fibo 38.2% Barrier And 55SMA

The USDTRY pair spiked to 3.8458 high on Monday (the highest since mid-Dec) after opening with gap higher on fresh tensions over conflict on Turkey – Syria border as Turkish forces entered Syria.

Today's extension of recovery leg 3.7303 (correction low, posted on 05 Jan) dented pivotal 55SMA barrier at 3.8407, but without clear break so far.

Bulls require initial signal of continuation on close above cracked barrier at 3.8262 (Fibo 38.2% of 3.9814/3.7303 pullback), with close above 55SMA to confirm and open way for extension towards 14 Dec lower top at 3.8960.

Lira remains vulnerable after CBRT left rates unchanged on last week's policy meeting, avoiding to react and fight rising inflation, with fresh geopolitical tensions adding on existing pressure.

Underlying uptrend remains intact, with recent correction seen as buying opportunity for final attack at psychological 4.00 target.

Res: 3.8262, 3.8408, 3.8558, 3.8855

Sup: 3.8062, 3.7928, 3.7863, 3.7573

Technical Outlook: AUDUSD – Near-Term Focus Turns Higher After Shallow Dip, 0.8038 High Is Key

The Aussie dollar holds firm footing and returned above 0.80 handle after dipping to 0.7978 in Asia.

Reversal signal that was generated on strong upside rejection at 0.8035 on Friday which left Gravestone Doji candle, is fading on fresh bullish acceleration today.

Break and close above 0.8035 high is needed to neutralize existing bearish threats and open way for fresh extension of steep uptrend from 0.7500 trough towards key barrier at 0.8124 (08 Sep peak).

Session low at 0.7978 marks initial support ahead of pivotal point at 0.7940 (higher base, reinforced by rising 10SMA), loss of which would generate stronger bearish signal.

Res: 0.8038, 0.8065, 0.8102, 0.8124

Sup: 0.7978, 0.7940, 0.7923, 0.7900

Market Update – European Session: US Senate To Vote On Funding Govt Through Feb 8th

Notes/Observations

Senate to vote on later today to try to reopen govt and fund it through Feb 8th

BOJ and ECB rate decisions this week with focus on potential forward-looking discussions about the prospects for policy normalization

Asia:

Australia PM Turnbull affirms next election won’t be held until 2019

PBOC Adviser Sheng Songcheng:reiterated of no need for PBoC to raise benchmark interest rates as it would raise the cost of financing in the real economy and would not be conducive to financial deleveraging

China State Planner: Confident Chinese economy will maintain steady, good momentum in2018 ; will further guide Chinese firms in their overseas investment

Japan Cabinet Office confirmed speculation that it would push back its forecast for achieving primary budget surplus by two years to FY27

Europe:

Germany Social Democrats (SPD) voted to support the opening of formal coalition talks with Chancellor Merkel’s conservative bloc with vote by 362 to 279

Renewed speculation that EU officials could pick a new ECB vice president with the Eurogroup ministers to kick off the process today

PM May: Reiterates Britain wants to have a comprehensive trade deal with the EU as well as a defense pact in place once its leaves the bloc

France President Macron: UK could get a special trade deal with the EU after Brexit, UK will not have full access to the single market without accepting its rules

Former UKIP leader Nigel Farage said to be considering forming a new pro Brexit party after becoming dismayed with internal politics and scandal within UKIP since his resignation as leader 18 months ago

President Trumps anger with UK PM May puts US-UK trade deal after Brexit is at risk; relationship said to have "soured”. Trump is still furious with the way he has been treated by the British government and warned his deteriorating relationship with May is likely to kill any prospect of a swift post-Brexit trade deal. May will attempt to clear the air with Trump when she meets him at Davos (if he attends)

Fitch raised Spain sovereign rating one notch to A- from BBB+; revised outlook to Stable from Positive

S&P raised Greece sovereign rating one notch to B from B-; maintained outlook Positive

Americas:

US Senator Majority Leader Mcconnell (R-KY): Set next Senate procedural vote on 3-week stopgap spending bill for noon EST Monday

Senate minority leader Schumer (D-NY): Yet to reach agreement on path forward

Senator Flake (R-AZ):; Bipartisan meeting to be held on Monday at 10 am EST to discuss continuing resolution (CR)

President Trump if Govt shutdown stalemate continued, Republicans should use procedural “nuclear option” to change Senate rules and pass long-term spending bill

Energy:

Russia and OPEC reaffirmed that they will continue with oil-production cuts until year-end to clear a global glut, indicate willingness to cooperate beyond

Economic Data:

(NL) Netherlands Jan Consumer Confidence: 24 v 25 prior

(NL) Netherlands Nov Consumer Spending Y/Y: 2.6% v 1.7% prior

(JP) Japan Dec Convenience Store Sales Y/Y: -0.3% v -0.3% prior

(NL) Netherlands Dec House Price Index M/M: 0.4% v 0.5% prior; Y/Y: 8,2% v 8.2% prior

(NO) Norway Q4 Industrial Confidence: 6.4 v 5.0e

(TW) Taiwan Dec Export Orders Y/Y: 17.5% v 12.2%e

(TW) Taiwan Dec Unemployment Rate: 3.7% v 3.7%e

(CH) Swiss Dec M3 Money Supply Y/Y: 3.2 v 4.3% prior

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 flat at 400.7 , FTSE +0.1% at 7735, DAX -0.1% at 13423, CAC-40 -0.1% at 5520 , IBEX-35 +0.4% at 10519, FTSE MIB +0.1% at 237773 , SMI -0.2% at 9494, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes:

European Indices trade mixed this morning, with outperformance in the Spanish Ibex, as Indices trade off the sesssion highs in rangebound trade ahead of a busy earnings week.

Swiss financial giant UBS trades under pressure after reporting inline results, with electrical retailer Dixons Carphone trading higher with LFL growth of 6%. In the M&A space Sanofi confirmed the acquisition of Biovertativ in an $11.6B deal, while Richemont announced a voluntary tender for Yoox Net-A-Porter. Elsewhere in the UK Ocado trades over 10% higher after a partnership with Sobeys; Bookmaker Ladbrokes and William Hill trade sharply lower after reports of a new £2M maximum in gaming machines.

Looking ahead notable earners include Haliburton and Wynn Resorts.

Movers

Consumer Discretionary [Dixons Carphone [DC.UK] +2% (Chirstmas update), Ocado [OCDO.UK] +13% (Partnership with Sobeys), William Hill [WMH.UK] -12.5%, Ladbrokes [LCL.UK] -10% (UK said to be set to announce a new £2 maximum stake on lucrative high stakes gaming machines)]

Financials [UBS [UBSG.CH] -1.6% (Earnings)]

Technology [Aveva [AVV.UK] +5.0% (Trading update), Lending Tech [LTG.UK] +6.8% (Trading update)]

Healthcare [Sanofi [SAN.FR] -3.8% (To acquire Bioverativ for $11.6B) Swedish Orphan Biovitrum [SOBI.SE] +11% (up in sympathy)]

Speakers

ECB bond purchases are deviating from capital-key requirements with purchases of Italian, French, Austrian, Belgian Govt bonds last year was about 10% above the level justified by the capital key

EU draft document: Greece needs additional debt-mitigating measures (**note comments aheda of today's Eurogroup meeting)

Czech Central Bank Gov Rusnok: Saw a very good probability of a rate hike in Feb while no enormous inflation pressure on domestic economy

Spain prosecutor said to have asked Supreme Court judge Llarena to activate an European arrest warrant for former Catalan President Puigdemont (**Note: Request comes after Puigdemont left Brussels for Copenhagen)

Iraq Oil Min Luaibi: Oil prices are heading in the right direction

Currencies

The USD was only modestly softer despite the continued shutdown of the US govt

The EUR/USD remained about a big figure away from its recent 3-month highs of 1.2323 as the pair seemed to have failed to benefit from bullish news. Focus turning to ECB rate decision on Thursday.

USD/JPY seemed to break its historical correlation with US bond yields. Dealers noted that US bond yields are not supporting USD/JPY pair. BOJ meets on Tuesday with no change expected in policy but to focus on its forward communication especially on the inflation front. Japan will release its Dec COPI data on Friday with analysts noting that an overshoot in the core CPI would raise the possibility of the BOJ moving to normalize policy

Monday's Eurogroup meeting of eurozone finance ministers should sign off the latest bailout tranche and allow the closing of the third review. The fourth review is expected to be completed in June. The current Greek bailout runs until August

Fixed Income

Bund Futures trades down 11 ticks at 160.47 after initially rallying as strong support lies sub 160 level. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 123.50 down 12 ticks, hanging near Friday’s low. Support continues to stand at 123.55 then 122.83, with upside resistance at 124.25 then 124.96.

Monday’s liquidity report showed Friday’s excess liquidity rose to €1.863T from €1.860T prior. Use of the marginal lending facility fell to €237M from €434M prior.

Corporate issuance saw banks dominate with $47B issuance in high-grade raised last week

Looking Ahead

05:25 (BR) Brazil Central Bank Weekly Economists Survey

06:00 (DE) German Bundesbank monthly report

06:00 (IE) Ireland Dec PPI M/M: No est v -0.4% prior; Y/Y: No est v -3.6% prior

06:00 (TR) Turkey to sell 2024 Floating Rate bonds

06:00 (IL) Israel to sell Bonds

06:45 (US) Daily Libor Fixing

07:00 (RO) Romania to sell 3.25% 2024 Bonds

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week (to sell 3-month and 9-month Bills on Tues)

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Dec Chicago Fed National Activity Index: 0.22e v 0.15 prior

08:30 (CA) Canada Nov Wholesale Trade Sales M/M: 1.2%e v 1.5% prior

08:55 (FR) France Debt Agency (AFT) to sell combined €4.8-6.0B in 3-month, 6-month and 12-month BTF Bills

09:00 (MX) Mexico Dec Unemployment Rate (Seasonally Adj): 3.5%e v 3.5% prior; Unemployment Rate (Unadj):3.3%e v 3.4% prior

09:00 IMF updates its World Economic Outlook (WEO)

09:00 (EU) Eurogroup Finance Ministers meet

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (CO) Colombia Nov Trade Balance: -$0.8Be v -$0.6B prior; Total Imports: $4.0Be v $3.9B prior

11:00 (US) Senate Republicans will have a conference meeting

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

12:00 (US) Senate expected to vote to fund the government through Feb. 8th (expected not to pass)

14:00 (CO) Colombia Nov Economic Activity Index (Monthly GDP) Y/Y: 1.6%e V 1.4% prior

15:00 (MX) Mexico Citibanamex Survey of Economists

21:00 (PH) Philippines Q4 GDP Q/Q: 1.6%e v 1.3% prior; Y/Y: 6.7%e v 6.9% prior, GDP Annual Y/Y: 6.5%e v 6.8% prior

(JP) Bank of Japan (BOJ) Interest Rate Decision: Expected to leave Interest Rate unchanged at -0.10%