Sample Category Title

BoJ to Remain on Hold; All Eyes on Kuroda

The Bank of Japan (BoJ) will announce its policy decision during the Asian morning on Tuesday. No change in policy is expected and as such, focus will probably turn to Governor Kuroda's press conference for any signals on whether the Bank is considering to alter its ultra-loose framework, as has been speculated recently. With inflation still far away from its target though, the BoJ chief may push back against such expectations.

Speculation that the BoJ may be getting ready to scale back its massive stimulus program came back to the forefront lately, helping the yen to reach 4-month highs against the greenback. The move followed news that the Bank had purchased fewer longer-dated bonds than usual in its regular operations, leading investors to question whether this is a sign of what is to come.

Despite the market reaction, however, one should distinguish whether this was a signal or noise in the bigger picture. Under its current framework of QQE with yield-curve control, the BoJ has committed to buying as many Japanese Government bonds (JGBs) as needed to keep the yields on longer-dated bonds fixed near 0%. Therefore, the fact that it purchased fewer bonds in one of its operations merely shows the Bank needed to intervene less in the market in order to achieve its goal, and should not be confused with a policy signal.

Let's not forget that similar speculation occurred back in November as well, after Governor Kuroda mentioned the risk of low rates harming the profitability of banks and hence weakening the effects of ultra-easy monetary policy. The BoJ chief quickly came to the rescue though, reassuring investors in the press conference following the December meeting that the Bank sees no need to change its yield-targeting strategy, and that it "won't raise interest rates just because the economy is improving".

We could see such comments being repeated at this gathering. Core inflation ticked up to 0.9% y/y in November, but this is still a long way off from the BoJ's 2% target, implying the Bank is not ready to declare victory on inflation just yet. Moreover, any hints from Governor Kuroda about a reduction in stimulus would likely trigger a sharp appreciation in the JPY, which the Bank surely wants to avoid as that could make it more difficult for inflation to reach 2%.

Thus, should Kuroda reassure markets once again that the Bank is committed to its ultra-loose framework, then the yen may come under selling pressure. Dollar/yen could drift higher and target the 111.50 territory, where a potential upside break could see scope for extensions towards 112.00.

On the other hand, the slightest hint from the BoJ that a stimulus reduction may be on the cards would likely push the JPY higher. In such a case, dollar/yen could tumble and break below the crossroads of the 110.20 zone and the uptrend line taken from the lows of August 2016. Such a break could open the way for the 108.00 support area.

US 100 Index Trades Near Record High; RSI Overbought

The US 100 index is currently trading close to its all-time high of 6,844.45 hit during Friday's trading.

Rising prices in recent weeks are setting a bullish picture for the index in the short-term. The RSI, which has been heading higher throughout this period, is supporting the view for a positive market bias. The indicator though has crossed above the 70 overbought level; this being interpreted as increased risk for a pullback in the short-term.

The area around last week's record high of 6,844.45 could be providing some resistance at the moment, with a break above shifting the attention to the range around the upper Bollinger band at 6,931.68 as another potential barrier to the upside. In case of stronger bullish movement, the focus would turn to the 7,000 mark.

On the downside, the area around the middle Bollinger line - a 20-day moving average line - at 6,637.70 might act as support in case of declines. Before reaching this level, several round marks - for example the 6,700 and 6,800 handles - have the capacity to act as potential psychological support.

The medium-term outlook is bullish: the index is in an uptrend with price action taking place above the 50- and 100-day MAs and both MAs maintaining a positive slope.

Overall, the short-term momentum is positive with perhaps a warning sign given by an overbought RSI, while the medium-term picture is clearly bullish.

Sunset Market Commentary

Changes on global core bond markets were minimal today. The German Bund slightly outperformed the US Note future. Moves could have been larger given the weekend's events: the SPD formally entering German coalition talks, rating upgrades for Greece/Spain and the US government in shutdown mode. US investors apparently have strong faith in the outcome of tonight's new US Senate vote. The US 5-yr (2.42%) and 10-yr yields (2.63%/2.64%) marginally surpass key resistance levels; but we consider the test as ongoing. Changes on the German yield curve range between -0.1 bp (2-yr) and +1 bp (10-yr). The US yield curve flattens with yields up to 2 bps lower (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are close to unchanged with Spain (-3 bps) outperforming following this weekend's rating upgrade into "A" category (A-, stable outlook).

Trading on global FX markets remained very orderly even as the US Senate failed to strike an agreement on a funding bill, triggering a government shut-down. The dollar opened with a slight negative gap in Asia, but soon returned to Friday's opening levels. Later in the session, USD/JPY (currently 110.75) held a very tight range. The dollar ceded temporary ground against the euro in European trading, but EUR/USD (currently 1.2245) stayed well off the intraday top (1.2275 area). The LT US/German interest rate differential narrowed marginally, but European yields had till some catching up to do on Friday's US moves. Whatever, the USD price moves were modest and without clear trend. Investors simply stay sidelined and try to assess how long this stalemate will last. Other event risk includes tomorrow's BOJ policy decision and Thursday's ECB decision. For now, the dollar can cope with the political uncertainty. Of course, this won't last eternally.

Sterling remained well bid, as was the case at the end of last week. We didn't see any high profile news on data or on Brexit. The market is becoming positioned quite long sterling, but for now there is no clear trigger to change course. Dollar softness supports cable. The technical picture of EUR/GBP suggests some additional room to the downside if the 0.8810/00 intermediate support area would be broken. EUR/GBP currently tests the 0.8800 area. Tomorrow, the UK CBI retail data will be published.

European stock markets eke out small gains with the Spanish IBEX 35 outperforming (+1%), supported by Fitch's upbeat assessment and rating upgrade. US stock markets opened little changed with Dow slightly underperforming.

News Headlines:

Germany's SPD demanded concessions on immigration and healthcare from Chancellor Merkel's conservatives in looming coalition talks that the centre-left party voted for at the weekend. Full talks between Merkel, SPD leader Martin Schulz and the leader of Merkel's CSU Bavarian allies, Horst Seehofer may start as early as Tuesday.

The British government believes the question of whether it alone can stop Brexit is irrelevant, since it does not intend to change its mind about leaving the EU, according to its response to a legal challenge by Scottish lawmakers opposed to Brexit.

The IMF upgraded the outlook for the world economy, noting surprisingly strong growth in Europe and Asia and predicting that US tax cuts will give the American economy a short-term boost. Global growth is assumed to have expanded 3.7% for 2017 and to accelerate to 3.9% for this year and 2019.

The Czech National Bank is quite likely to raise interest rates at its next policy meeting on Feb. 1 and is not nervous about the crown, Governor Rusnok was quoted as saying.

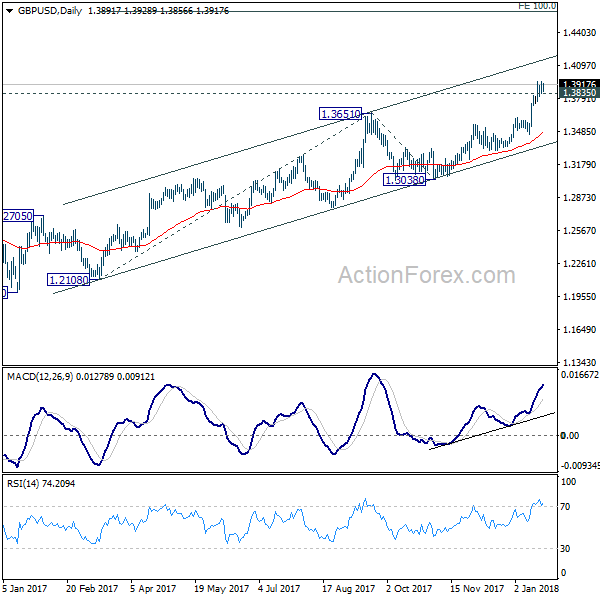

GBP Doing Good Despite the Fundamentals

Last week was good for the British pound, and the cable is still near the few-month highs as we are heading into week 4 of January. It looks like the market has finally abandoned all concerns with the Brexit negotiations, allowing the politicians to put an end to the issue without any trouble.

Meanwhile, Theresa May said there will be no additional Brexit referendum. Indeed, the talks about second referendum are groundless, although this topic is being very much discussed. Still, the referendum that was held in June 2016 is well enough for making a strategic decision.

The third reading regarding Brexit took place in the House of Commons on Jan 17 and was successful. Thus, the law is passed, and so the UK will leave the EU on March 29, 2019, which means there's a little more than a year for conducting the whole process, arriving to agreements, and designing the documents. This is very little time considering how hard such negotiations between the British and EU politicians usually are.

The pound's reaction towards fundamentals is mostly neutral in January. More reactions come from London fixing, the USD falling or recovery, and the general interest of the market towards buying.

An exception when the pound did react to the fundamentals were the retail sales data released on Friday. Core retail sales fell by 1.5% MoM in December, while it rose by 1% in November. YoY growth is at 1.4%, with it being 1.5% last month and the expectations at 2.6%.

Technically, FGBP/USD is heading towards the important level of 1.4000. Both mid term and long term trends are stable, and currently the mid term trend aims to reach the long term channel resistance at 1.4110. This could potentially lead to the price reaching 1.4235, which, with the mid-term channel resistance broken out, is quite probable. However, the price is now testing the resistance that became support, and, most likely, the pound is going to rise to 1.4110 and then retrace to 1.3910. If it happens so, the next important level for the downtrend will be 1.3610.

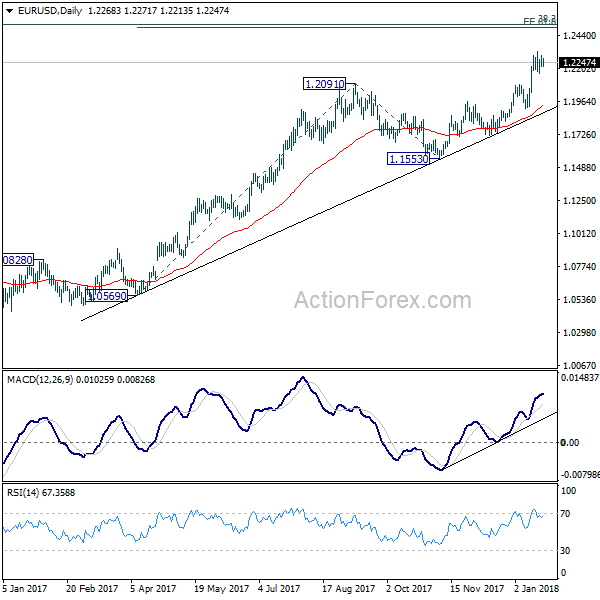

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2188; (P) 1.2241 (R1) 1.2269; More....

Intraday bias in EUR/USD remains neutral for consolidation below 1.2322. As long as 1.2088 resistance turned support holds, near term outlook remains bullish and another rise is expected. Above 1.2322 will extend the medium term rise to next key fibonacci level at 1.2494/2516. We'd expect strong resistance from there to bring reversal. Meanwhile, break of 1.2088 will argue that EUR/USD has topped earlier than expected. In that case, intraday bias will be turned to the downside for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of further rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

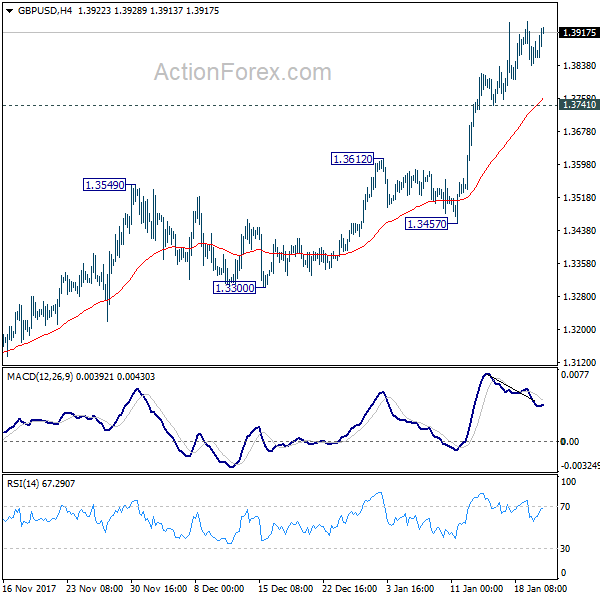

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3810; (P) 1.3878; (R1) 1.3917; More.....

No change in GBP/USD's outlook. As long as 1.3741 minor support holds, further rally is expected. Sustained trading above 1.3835 key resistance could trigger upside acceleration to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, considering bearish divergence condition in 4 hour MACD, break of 1.3741 will indicate short term topping. More importantly, that would suggest rejection from 1.3835 and turn bias to the downside for 1.3457.

In the bigger picture, sustained break of 1.3835 key resistance level will indicate that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. In that case, further rise should be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Nonetheless, rejection from 1.3835 will maintain medium term bearishness and thus, the risk retesting 1.1946 ahead.

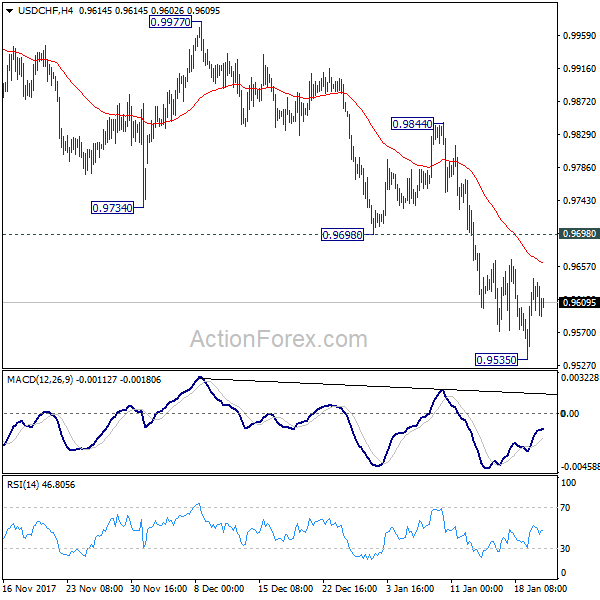

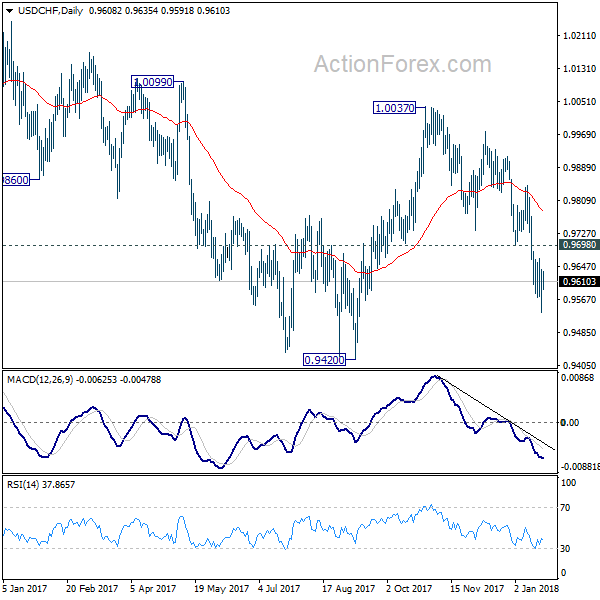

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9566; (P) 0.9602; (R1) 0.9668; More....

USD/CHF is staying in range above 0.9535 and intraday bias remains neutral first. Near term outlook will stay bearish as long as 0.9698 resistance holds. Below 0.9535 will extend the fall from 1.0037 and target a test on 0.9420 low. Nonetheless, firm break of 0.9698 will be the first sign of near term reversal. And, intraday bias will be turned back to the upside for 0.9844 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.48; (P) 110.80; (R1) 111.12; More...

USD/JPY is staying in range of 110.18/111.47 and intraday bias remains neutral first. On the upside, break of 111.47 will affirm the case that correction from 114.73 is finished with three waves down to 110.18. Intraday bias should then be turned back to the upside for 113.38 resistance for confirmation. However, below 110.18 will extend the correction lower. But we'd again look for bottoming signal in next fall.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Canadian Dollar Edges Higher, Wholesale Sales Disappoints

USD/CAD has edged lower in the Monday session. Currently, the pair is trading at 1.2474, down 0.24% on the day. On the release front, Canadian Wholesale Sales, slowed to 0.7%. This was shy of the estimate of 1.0%. The sole event in the US is the Richmond Manufacturing Index, with an estimate of 19 points.

It's Day Three of the US government shutdown, which began Friday at midnight when the Senate failed to approve a short-gap spending bill. Without funding, many non-essential government services have been forced to shut down. Democrats and Republicans are now playing the 'blame game' and pointing fingers at who is responsible for the crisis. The Democrats refused to vote for the spending measure until a deal is hammered out over Daca, an program for children who are illegal immigrants that Trump has threatened to deport. Lawmakers are scrambling to reach common ground, and on Sunday, Senate majority leader, Mitch McConnell suggested that he would allow a vote on immigration reform in February if Democrats agree to fund the government. With congressional elections looming, both parties will not want to anger voters, so we could see the crisis resolved this week.

As expected, the Bank of Canada pressed the rate trigger on Wednesday, raising interest rates by 25 basis points, from 1.00% to 1.25%. However, traders hoping for a stronger loonie were disappointed, as dovish comments from BoC Governor Stephen Poloz kept the currency from making headway against the US dollar. Poloz noted his concerns over NAFTA, the three-way free trade agreement which is crucial to the Canadian economy. US President Trump has threatened to cancel the pact unless Mexico and Canada make major concessions to the US. If the agreement is terminated, the Canadian dollar would likely take a tumble. Another round of negotiations is slated to be held in Montreal next week, and a lack of progress could weigh on the Canadian dollar.

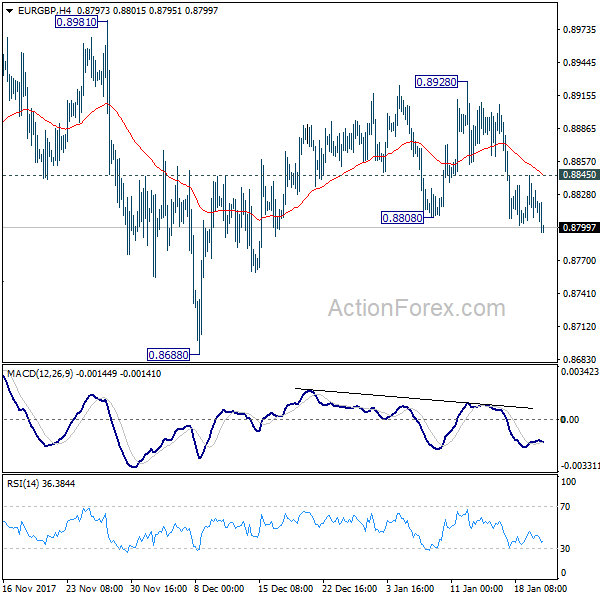

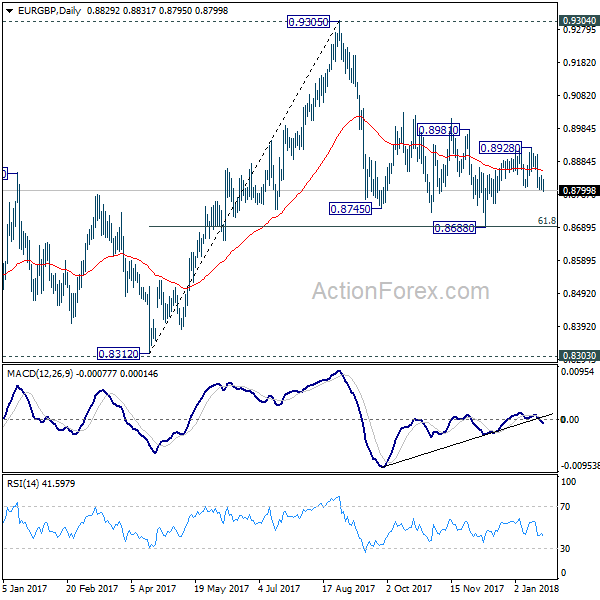

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8796; (P) 0.8820; (R1) 0.8839; More...

EUR/GBP's decline continues today and dips to 0.8795 so far. Intraday bias stays on the downside. as noted before, rebound from 0.8688 could have completed 0.8928 already. Deeper decline would be seen back to retest 0.8688 first. Firm break there would resume whole fall from 0.9305 to retest 0.8303/12 key support zone. On the upside, above 0.8845 minor resistance will turn intraday bias neutral first. But outlook will remain bearish as long as 0.8928 resistance holds, even in case of recovery.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.