Sample Category Title

Forex Analysis: BOJ Decision Day, US Fires Opening Salvo In Trade War

The Bank of Japan Interest Rate Decision was as expected and left unchanged at -0.1%. The Japanese 10-Year JGB yield target is around zero percent. JGB purchase remains at current pace to ensure holdings increase to around ¥80 Trillion a year. The BOJ raised its expectations on inflation in the quarterly report and extended the deadline for loan programmes aimed at boosting growth potential by 1 year. The Economy is expected to expand moderately. The BOJ will maintain QQE with yield curve control for as long as needed to stably hit 2% inflation. Risks remained roughly balanced and price risks tilted to the downside. Inflation is likely to continue to increase towards 2%, reaching it by around 2019/20. Also released was the All Industry Activity Index (MoM) (Nov), which came in at 1.0% v 0.9% expected, from 0.3% previously. BOJ Governor Kuroda made the comment that there was 'No need to adjust yield curve control (YCC) simply due to rise in inflation expectations'.

In China news, it was reported that the country is considering more Tax cuts to sustain economic recovery. This was in response to earlier reports that the Chinese commerce ministry was expressing strong dissatisfaction regarding US tariffs of 30% on solar imports and washing machines. It said the US decision further deteriorates the global trade environment and hopes the US will refrain from using trade remedy measures, but China will resolutely safeguard its own interests. The head of the Trade Remedy and Investigation Bureau from the Chinese commerce ministry says that 'China will work with other WTO members to resolutely defend its legitimate interests in response to the erroneous US decision'.

South Korea has responded to the US trade tariffs by saying they will look to reinstate tariffs on US goods and services. South Korea's Trade Minister said that the 'latest safeguard measures are in violation to WTO rules' and that 'the government will actively respond to the spread of protectionist measures to defend national interests'. Samsung and LG sell between 2.5 to 3 million washing machines per year in the US.

The US Chicago FED National Activity Index (Dec) was released, with the number coming in at 0.27. The consensus was for 0.44 from 0.15 previously, which was revised down to 0.11. USDJPY rallied briefly in the midst of a move lower when the data was released.

EURUSD is down -0.11% overnight, trading around 1.22485.

USDJPY is up 0.18% in early session trading at around 111.125.

GBPUSD is down -0.08% to trade around 1.39753.

USDCAD is up 0.13%, trading around 1.24577.

Gold is up 0.22% in early morning trading at around $1,336.81.

WTI is up 0.08% this morning, trading around $64.00.

Major data releases for today:

At 09:30 GMT, Public Sector Net Borrowing (Dec) is expected to come in at £4.200B from £8.118B previously. GBP traders will be closely following this data release.

At 10:00 GMT, Eurozone ZEW Survey – Current Situation (Jan) is expected to be 29.7, with a previous reading of 29.0. German ZEW Survey – Economic Sentiment (Jan) is expected to be 17.9, with a previous reading of 17.4. German ZEW Survey – Current Situation (Jan) is expected to be 89.7 from 89.3 prior.

At 15:00 GMT, Eurozone Consumer Confidence (Jan) is expected at 0.6 from 0.5 previously. EUR pairs and Eurozone assets could be influenced by this data release.

At 23:50 GMT, Japanese Adjusted Merchandise Trade Balance (Dec) will be released and is expected to be ¥261.7B v ¥364.1B previously. Merchandise Trade Balance Total (Dec) is expected to be ¥520.0B with a prior of ¥113.4B. Exports (YoY) (Dec) are expected at 10.1% from 16.2% previously. Imports (YoY) (Dec) is expected to be 12.3%, with a prior reading of 17.2%. JPY crosses may be heavily traded as a result of this data.

Currencies: Dollar Doesn’t Profit From New Spending Bill

Sunrise Market Commentary

- Rates: End of government shutdown hardly impacts trading

US Congress approved a stopgap funding bill until February 8, ending the government shutdown. The market impact on US Treasuries was modest, but the close of the 5- and 10-yr yields above key resistance could have important consequences if confirmed. European investors count down to Thursday's ECB meeting. - Currencies: Dollar doesn't profit from new spending bill

Yesterday, the dollar held tight ranges. The US currency hardly profited from the approval of a new spending bill. FX markets look forward to Thursday's ECB policy meeting. For now there is little investor appetite to be ‘short euro' ahead of this meeting. The Yen eases slightly this morning as BOJ Kuroda signals ongoing ample monetary stimulation.

The Sunrise Headlines

- US stock markets ended around 0.5% higher yesterday with Nasdaq outperforming (+1%). Asian risk sentiment is positive overnight with Japan and Korea outperforming.

- Congress approved a measure to fund the government for about 3 weeks and halt a 3-day shutdown, after Senate Democrats accepted Republicans' assurance that they would bring an immigration bill to the floor in the coming weeks.

- Donald Trump has approved broad tariffs on imports of solar cells and washing machines, the first in a series of anticipated moves aimed at cracking down on China and fulfilling his protectionist promises to US rust belt voters.

- The BoJ maintained its massive monetary stimulus program and kept its price and economic forecasts unchanged. In a small sign of progress, it said inflation expectations had stopped falling.

- EMU FM's welcomed Greek progress in delivering reforms but will only disburse the next aid tranche once all agreed actions are complete (February?). Ministers said they would start technical work on more debt relief for Greece that could be granted after the end of the bailout in August.

- The UK is one of the only major markets where house prices are unlikely to grow in 2018, according to new forecasts from Fitch. The only housing markets with a worse outlook for 2018 were Greece (-2%), and Norway (-5%).

- Today's eco calendar contains EMU consumer confidence, German ZEW and Richmond Fed manufacturing index. Germany and the US tap the market. The Q4 earning releases continue (J&J, P&G, Verizon,…).

Currencies: Dollar Doesn't Profit From New Spending Bill

USD still going nowhere, despite end of shutdown

Trading on global FX markets remained very orderly yesterday even as the US Senate didn't reach an agreement on a funding bill during the weekend. The dollar hovered sideways. News on the approval of a ST spending bill supported the dollar temporary. USD/JPY and EUR/USD held within established ranges. EUR/USD finished the day little changed at 1.2262. USD/JPY gained a few ticks to close the day at 110.92.

The BOJ as expected left its policy unchanged overnight. They were slightly more optimistic on inflation (expectations), but there is no indication of an imminent policy change. USD/JPY dropped temporary from the high 110 area to the 110.60 area, but rebounded during Kuroda's press conference. The (tradeweighted) dollar is holding within reach of the recent lows. The dollar doesn't profit from the end of the government shut-down. EUR/USD even has a slight upward bias, hovering in the 1.2250/75 area.

German ZEW investor confidence and EC consumer confidence are expected slightly higher. The Richmond Fed manufacturing index is expected marginally softer (19 from 20), but at a high level. Any reaction on the FX market will only be of intraday significance, at best. The rise in US yields indicated that markets anticipate more policy normalization. It still doesn't help the USD as markets are pondering when and at what pace the ECB will join the Fed. ECB's Draghi will maintain a soft tone at Thursday's press conference. Even so, there is little appetite to be positioned 'euro short' going in to the ECB meeting. Global Picture: the dollar was in the defensive of late as markets prepare for a change in policy from central banks outside the US. This propelled EUR/USD despite a huge interest rate differential in favour of the dollar. The USD decline slowed last week, but any ‘rebound' remained unconvincing. A return below previous resistance at 1.2092 is needed to call off the ST alert for the dollar. EUR/USD 1.2598 (62% retracement) is next important resistance on the charts.

Sterling was in good shape of late. EUR/GBP tested the 0.8810/00 intermediate support and finally dropped below this level. Cable nears the 1.40 mark. UK public finance data and the CBI order data will be published today. EUR/GBP is drifting lower in the 0.8928/0.8692 consolidation range. The day-to-day momentum is sterling positive but we keep the view that the EUR/GBP 0.87 area is a tough resistance. Gains of cable beyond 1.40 might also become less easy .

EUR/USD: stays away from recent top despite US political uncertainty

Appetite For Risk Returns As U.S. Government Shutdown Ends

The rally in Asian equities resumed on Tuesday taking the lead from Wall Street, after the U.S. government shutdown came to an end on Monday. Although reaching a deal to fund the government for another 17 days is positive news, it isn’t necessarily the key driver of investors’ decisions. After all, government shutdowns have little or no impact on corporate earnings, and during the previous three, stocks still moved to the upside. However, a longer-term solution is required as we get closer to the debt ceiling. Failing to raise the borrowing limit would lead to a technical default, send yields on Treasuries higher, and potentially lead to a downgrade of U.S. credit rating.

Meanwhile, investors are likely to ignore the overstretched valuations and continue moving with the flow. Many factors are likely to keep fueling the rally including, positive earnings, Merger and Acquisition deals, and the upsurge in global growth. The IMF joined the party yesterday, raising its outlook for economic growth in 2018 and 2019 to 3.9%. That represents an upgrade of 0.2% for each year.

BoJ: No Change in policy

The Bank of Japan decided not to surprise markets by keeping monetary policy unchanged. Traders who were speculating on early withdrawal of stimulus receivedno signs that one would materialise. The fact that price projections remained unchanged, indicates that the exit of unconventional monetary policy isn’t likely to occur anytime soon. This is despite the BoJ announcing earlier this month that it was marginally reducing the purchase of long-dated JGBs. The lack of surprise kept the USDJPY trading within a range of 50 pips during the Asian session.

Sterling pops above $1.4

The British Pound attracted most of the traders’ attention after breaking above $1.4 earlier today. The 1.4 is not only a psychological level, but it has also been considered a key support level during the past three decades prior to the Brexit vote. Although a lot of the currency’s strength is attributed to dollar’s weakness, the Pound is the best performing major currency this year, and it’s up 1.35% against the Euro YTD which is a better proxy for Brexit negotiations. With only tier-2 economic data due for release today, I don’t expect to see big moves, however I still believe there’s more upside potential if Brexit talks continue to move forward when they resume in March.

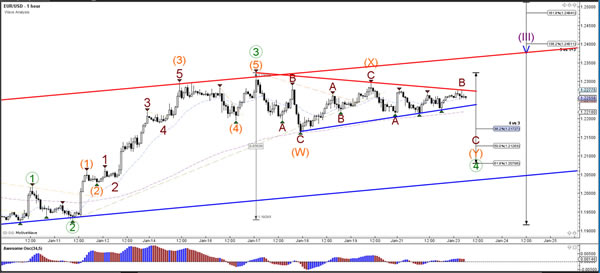

Daily Wave Analysis: GBP/USD Wave 3 Hits 1.40 Resistance Level

Currency pair GBP/USD

The GBP/USD made a bullish bounce at the support trend line of the bullish channel and price is now challenging the round level of 1.40, which is an important bounce or break spot. A breakout could see price move towards the next Fibonacci target

The GBP/USD bullish momentum is probably a wave 3 (blue). Price could build a bearish retracement here at the resistance trend line but the pullback could find support and bounce at the Fibonacci levels of wave 4 (blue).

Currency pair EUR/USD

The EUR/USD is in a triangle chart pattern marked by support (blue) and resistance (red) trend lines. A bullish breakout above that resistance trend line (red) could indicate a continuation of the uptrend towards the Fibonacci targets of wave 5 (blue).

If the EUR/USD breaks below the support trend line (blue) then price could also expand the bearish correction via a bearish ABC (brown) zigzag.

Currency pair USD/JPY

The USD/JPY seems to be stuck between support (blue) and resistance (red) trend lines. A breakout could indicate the new trend direction,

The USD/JPY could be completing wave 2 (purple) and starting a wave 3 (purple) bullish momentum if price manages to break above resistance.

Market Update – Asian Session: BOJ Holds Policy Steady

Headlines/Economic Data

General Trend: Asian equities track US gains

Traders looking ahead to BoJ Gov Kuroda's post rate decision press conference (expected around 6:30 GMT)

US dollar (USD) generally weaker versus Asian currencies: PBoC fixed yuan at multi-year high for 3rd straight session

GBP/USD: During Asian session, the pair briefly traded above 1.40 for the first time since June 2016 Brexit vote

Japan

Nikkei 225 opened +0.5%; closed +1.3%

(JP) Japan's Topix passes 1,900 for the first time since 1991

TOPIX Real Estate Index +2.0%, Securities +1%, Information/Communication +0.8%

Automakers trade generally higher: Honda +1.5%, Toyota +0.9%, Nissan +0.9%

(JP) BoJ Jan Loan Officer Opinion Survey: Company loan demand 8 v 6 prior

(JP) Japan and France will agree on a defense logistics framework ahead of state visits – press

(JP) BOJ Quarterly Outlook for Economic Activity and Prices, Affirms all GDP and CPI forecasts

(JP) BANK OF JAPAN (BOJ) LEAVES INTEREST RATE ON EXCESS RESERVES (IOER) UNCHANGED AT -0.10%; AS EXPECTED: vote again 8-1 as Kataoka again dissents

Looking Ahead: Japan: BoJ Gov Kuroda due to hold post rate decision press conference after the close

Tokyo Steel expected to report earnings after the close

Korea

Kospi opened +0.3%

Financials trade broadly higher: Industrial Bank of Korea +2.9%, Woori Bank +2.7%, Shinhan +1.7%

LG Display, 034220.KR Reports Q4 (KRW) Net 36.9B v 203Be; Op 44.0B v 250Be; Rev 7.1T v 6.9Te

LG Electronics [066570.KR]: -1.5% (Trump administration approves safeguard tariff action on imported washing machines)

(KR) Reportedly South Korea govt has asked state banks to refrain from overseas bond offerings, in order to minimize impact on FX - Korean press

(KR) Six South Korean banks will begin issuing new trading accounts for cryptocurrencies next week by introducing a system that bans the use of anonymous accounts in cryptocurrency transactions - Korean press

China/Hong Kong

Hang Seng opened +0.7%, Shanghai Composite +0.1%

Hang Seng Information Tech Index +1.3%, Services +1.2% (strength in gaming names, Wynn Macau +5%), Financials +1.3%

(CN) China Premier Li: Needs to be solid efforts to push reforms and innovation in 2018 (Chairing a plenary meeting of the State Council) – Xinhua

(HK) IMF concludes Hong Kong Article IV Consultation talks: Sees Hong Kong SAR* 2018 GDP growth of 2.8%

(CN) HSBC's Asian Economics Research co-head Neumann: The use of the yuan is expected to increase going forward – Xinhua

(CN) China to consider more tax cuts to sustain economic recovery - Xinhua

(CN) China PBOC OMO: Injects CNY170B v CNY100B injected in 7,14 and 63-day reverse repos prior: Net injection CNY0B v CNY20B injected prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.4009 v 6.4112 PRIOR (strongest level since Dec 7th, 2015)

Leshi Internet, 300104.CN Says faces operational difficulty without new investment; to fix cash shortage through borrowings and capital raisings (halted)

Australia/New Zealand

ASX 200 opened +0.1%; closed %

ASX 200 Energy Index +1.5%, Resources +0.8%, Financials +0.8%

QBE.AU Guides FY17 combined ratio ~104% (prior 100-102%); To book A$700M impairment charge against North America assets, starts strategic review of Latin America operations; opens -5%

Other Asia

(PH) PHILIPPINES Q4 GDP Q/Q: 1.5% V 1.6%E; Y/Y: 6.6% V 6.7%E, 2017 GDP Y/Y: 6.7% V 6.7%E

(SG) SINGAPORE DEC CPI M/M: -0.1% V +0.2%E; Y/Y: 0.4% V 0.5%E

North America

US equity markets ended higher: Dow +0.6%, S&P500 +0.8%, Nasdaq +1%, Russell 2000 +0.5%

S&P500 Energy Sector +2.2%, Consumer Discretionary +1.1%, Tech +1%

WHR Trump administration approves safeguard tariff action on imported washing machines - press

Netflix [NFLX]: Gains over 8% in afterhours: Reports Q4 $0.41 v $0.41e, Rev $3.29B v $3.28Be; Guides Q1 $0.63 v $0.57e, total Rev $3.69B v $3.52Be; Q4 Total streaming net adds 8.3M v 5.3M q/q v 6.3M forecast

Steel Dynamics [STLD] Reports Q4 $1.28* v $0.49e, Rev $2.3B v $2.17Be

(US) Senate gained sufficient votes to end govt shutdown

(US) House passes stop gap govt funding bill (as expected), President Trump will sign and then go into effect

Looking Ahead: Weekly US API Crude Oil Inventories to be released

Companies expected to report earnings on Tuesday include JNJ, Procter & Gamble, State Street, Texas Instruments, Travelers, United Continental, Verizon

Europe

GEA Group [G1A.DE]: Guides FY17 adj EBITDA €585M v €566M y/y; Rev €4.58B v €4.49B y/y; Guides FY18 Operating EBITDA €590-640M

Logitech [LOGI]: Reports Q3 $0.65 v $0.56 y/y, Rev $812M v $667M y/y: Raised FY18 guidance

Volkswagen [VOW3.DE]: Guides 2018 China growth similar to 2017, sees passenger car market up around 4% and sees its own growth as similar

Looking Ahead: Germany Jan ZEW Survey due for release

Levels as of 01:00ET

Nikkei225 +1.3%, Hang Seng +1.2%; Shanghai Composite +0.6%; ASX200 +0.8%, Kospi +1.1%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 +0.1%

EUR 1.2276-1.2251; JPY 111.03-110.55; AUD 0.8029-0.7982;NZD 0.7354-0.7314

Feb Gold +0.3% at $1,335/oz; Mar Crude Oil +0.6% at $63.98/brl; Mar Copper -0.2% at $3.19/lb

The Bank Of Japan Kept Its Monetary Policy Steady

Market movers today

It is another quiet day on the data front with only the ZEW indicator in Germany and consumer confidence in the eurozone for January as the noteworthy releases.

Market focus will in coming days be on the political announcements from the gathering of leading policy makers and experts at the World Economic Forum in Davos. The meeting this year will be particularly interesting after the Trump administration yesterday imposed tariffs on solar panels and washing machines, drawing strong criticism from China and South Korea.

Selected market news

Asian shares are generally rising this morning to fresh highs. One positive aspect is the reopening of the US government starting today as the Republicans and the Democrats yesterday agreed on a short -term funding bill expiring on 8 February in an at tempt to get more time to negotiate the immigration reform. The deal probably comes as the Democrats were concerned about losing support , as a shutdown is very unpopular among voters amid the looming mid-term election in November. As the shutdown only lasted a few days, there are no real economic costs and thus we still believe the Fed is on track to deliver a hike in March (for more details see our flash comment here).

The rise in the Asian stock markets comes despite the US administ ration imposing temporary tariffs on imported solar panels and washing machines. A tariff of 30% will be applied to imported solar panels while tariffs will begin at 20% on large residential washing machines. The decision comes after the independent US International Trade Commission (ITC) determined that imports of solar panels and washers had hurt American companies. Tariffs will be in place for three years and will taper down. Most of US imports of solar panels come from China. The US move drew strong criticism from China and South Korea, with the South Koreans warning to taking the case to the WTO. The move by the US administration is particularly interesting ahead of new negotiations on NAFTA later this week and US President Trump participating in the World Economic Forum in Davos with all world leaders.

This morning, the Bank of Japan (BoJ) kept its monetary policy steady (keeping its short -term interest and 10-year yield targets unchanged), while sounding slightly more upbeat on inflation expectations. It left JGB purchases unchanged at the current pace of about JPY80trn. The USD/JPY dropped 30 pips to 110.60 initially, before rebounding back to 110.80. The press conference is due to start at 7:30 CET.

Aussie Trading Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.25% against the USD and closed at 0.8015.

Yesterday, the IMF forecasted that China, Australia's largest trading partner, is expected to grow at 6.6% this year before slipping to 6.4% in 2019.

LME Copper prices declined 0.4% or $30.0/MT to $7049.0/MT. Aluminium prices declined 0.9% or $21.0/MT to $2235.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7988, with the AUD trading 0.34% lower against the USD from yesterday's close.

The pair is expected to find support at 0.7972, and a fall through could take it to the next support level of 0.7956. The pair is expected to find its first resistance at 0.8017, and a rise through could take it to the next resistance level of 0.8046.

Moving ahead, traders would focus on Australia's Westpac leading index for December, due to release overnight.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro Trading Marginally Higher, Ahead Of The ZEW Economic Sentiment Survey Across The Euro-Zone

.

For the 24 hours to 23:00 GMT, the EUR rose 0.18% against the USD and closed at 1.2258, following encouraging political developments in Germany, as the Social Democrats (SPD) voted in favour of pursuing coalition talks with Angela Merkel's conservatives.

The greenback declined against a basket of major currencies, as news of the US Senators voting to lift a three-day government shutdown failed to boost investor sentiment.

In the US, data indicated that the Chicago Fed national activity index rose to a level of 0.27 in December, compared to a revised reading of 0.11 in the previous month, while market participants had anticipated for an increase to a level of 0.22.

Separately, the International Monetary Fund (IMF), in an update of its World Economic Outlook, boosted its global economic growth forecast to 3.9% for both 2018 and 2019, up by 0.2% from its previous estimate. Additionally, the Fund revised up its economic outlook for the Euro-bloc to 2.2% in 2018, up 0.3% from its earlier projection in October.

However, the organisation also forecasted that economic growth in the US would likely slowdown after 2022, as the tax cuts would give the American economy a short-term boost. The Fund now expects the world's largest economy to expand by 2.7% in 2018, sharply higher than its previous prediction of 2.3%. Growth was projected to slow to 2.5% in 2019.

In the Asian session, at GMT0400, the pair is trading at 1.2259, with the EUR trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.2223, and a fall through could take it to the next support level of 1.2188. The pair is expected to find its first resistance at 1.2285, and a rise through could take it to the next resistance level of 1.2312.

Going ahead, market participants would look forward to the release of the ZEW economic sentiment index for January across the Eurozone, scheduled in a few hours. Also, the region's flash consumer confidence index for January, slated to release later in the day, would be eyed by traders. Additionally, the US Richmond Fed manufacturing index for January, would be on investors' radar.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Pound Trading A Tad Lower This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.79% against the USD and closed at 1.3984, as a more upbeat outlook among investors regarding Brexit negotiations boosted gains in the local currency.

Yesterday, the IMF maintained its projection for Britain's economic growth at 1.5% for this year.

In the Asian session, at GMT0400, the pair is trading at 1.3983, with the GBP trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.3893, and a fall through could take it to the next support level of 1.3803. The pair is expected to find its first resistance at 1.4038, and a rise through could take it to the next resistance level of 1.4093.

Looking ahead, traders would await UK's public-sector net borrowing data for December, set to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoJ Announced No Change To Monetary Policy, Retained Its Inflation Outlook

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the JPY and closed at 110.95.

In the Asian session, at GMT0400, the pair is trading at 110.77, with the USD trading 0.16% lower against the JPY from yesterday's close.

The Japanese Yen gained ground against the USD, after the Bank of Japan (BoJ), at its January monetary policy meeting, opted to leave the key interest rate steady at -0.1% and held the yield target for 10-year Japanese government bonds around 0%. In its quarterly economic outlook report, the central bank stuck to its view that inflation in Japan will likely achieve its 2.0% target in the 2019 fiscal year.

Earlier today, data showed that Japan's all industry activity index climbed more-than-expected by 1.0% MoM in November, compared to an advance of 0.3% in the prior month. Market anticipation was for the activity index to climb 0.8%.

The pair is expected to find support at 110.48, and a fall through could take it to the next support level of 110.19. The pair is expected to find its first resistance at 111.14, and a rise through could take it to the next resistance level of 111.51.

Looking forward, traders would keep a close watch on Japan's flash Nikkei manufacturing PMI for January and adjusted merchandise trade balance for December, due to release overnight.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.