Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2250

Nothing interesting here, as the pair remains caught in a tight range trading below 1.2300 and I favor a dip to 1.2160 before renewal of the general rise beyond 1.2320.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2300 | 1.2500 | 1.2217 | 1.2090 |

| 1.2320 | 1.2500 | 1.2160 | 1.1910 |

USD/JPY

Current level - 110.97

I favor another intraday rise to 111.50 resistance area, before renewal of the general slide towards 109.50. Key intraday support lies at 110.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.50 | 112.00 | 110.50 | 109.50 |

| 112.00 | 113.75 | 110.20 | 109.50 |

GBP/USD

Current level - 1.3963

The consolidation pattern below 1.3940 is complete and the uptrend is renewed, currently testing 1.4000 sentiment area. Next target projection lies at 1.4150. Initial intraday support is projected at 1.3940 and crucial on the downside is 1.3830.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4000 | 1.4000 | 1.3940 | 1.3830 |

| 1.4150 | 1.4340 | 1.3830 | 1.3611 |

Technical Outlook: AUDUSD Eases From 0.80 Zone, Pressured By Stronger Greenback And Lower Copper Price

The Aussie dollar eases on Tuesday after repeated failures to sustain break above 0.80 barrier with 0.8030 zone topping recent upside attempts.

Stronger greenback on deal of US policymakers to end government’s shutdown and weaker copper price added on fresh pressure on Aussie.

Fresh easing pressures strong support at 0.7950 (rising 10SMA/Fibo 38.2% of 0.7807/0.8038 upleg, reinforced by top of thickening 4-hr cloud), violation of which would signal deeper correction.

Daily RSI turned south and is emerging from overbought territory, generating bearish signal.

Extended dips could travel to 0.7895/82 (strong supports provided by Fibo 61.8% of 0.7807/0.8038/rising 20SMA), where correction should find ground to keep overall bulls in play for fresh probes through at 0.80 and eventual attack at key barrier at 0.8124 (2017 high, posted on 08 Sep).

Res: 0.8029, 0.8038, 0.8065, 0.8102

Sup: 0.7950, 0.7936, 0.7895, 0.7882

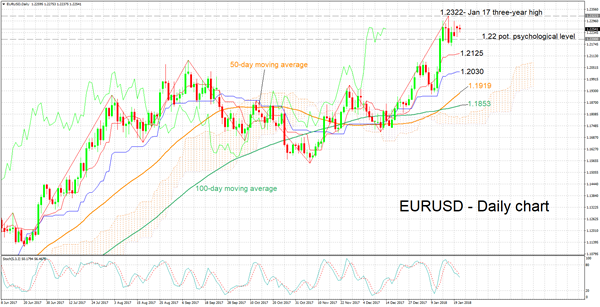

Is EUR/USD Ready For A Correction?

Correction in the EUR/USD is likely

A midterm-spread in US-Bunds and US-Europe yields suggests a correction in EUR/USD is likely. This, after the minutes of the last European Central Bank monetary policy meeting triggered an extension of EUR/USD rally to current 1.22 highs. They suggest that the ECB plans to address quantitative easing earlier than was expected. March is too early for the ECB to remove QE bias, as recent inflation data has been subdued. But heading into Italian elections on 4 March, the ECB must keep a reign on interest rates. This also suggests that ECB President Mario Draghi will sanitize any hawkish tone, even if Europe’s growth and inflation are above the ECB’s own forecast.

In Italy, deep austerity has created a solid populist base likely to make itself known in March. Still, the measures have failed to lower debt to GDP (now over 130%, 2nd highest in Europe) or generate strong economic growth. A hawkish ECB could trigger hikes in Italian rates, worsening current economic difficulties.

China booms ahead

We remain optimistic on China, with an above-consensus GDP forecast. This is based on global economics and China’s ability to harvest demand. Domestically, China is unbalanced but on a global basis it is diversified (its New Silk Road strategy is on mark). Moreover, in 2018, trade matters more than local consumption. On one hand, strong growth will help support weaker property prices that peaked in 2016, but should trigger action by policy makers to accelerate deleveraging and lower fiscal spending. Lower capital outflows and renewed positive investor confidence has lowered CNY deprecation risks.

South Africa on a marketing campaign

Following President Zumas’ reelection in 2014, his recent rejection by the ruling party African National Congress (ANC) and his 783 related charges upheld by the South African Supreme Court of Appeal, investors have become optimistic, thus reinforcing the South African Rand (ZAR) and equity market since the beginning of 2018 (USD/ZAR: -2.95%; EUR/ZAR: -0.25%; FTSE/JSE 40: +3.11%, MSCI South Africa: +1.98%). Initiated by its new party leader Cyril Ramaphosa who’s confirming his willingness to wipe out corruption matter within the country, the ANC has initiated talks to replace Zuma before the end of his mandate, formally ending in 2019. Rumors even arising mention that the resignation could occur as early as within two to four weeks according to local analysts.

The World Economic Forum (WEF) is therefore a great opportunity to show investors how attractive South Africa remains and to regain investor confidence. South Africa has proven strong economic achievements since the beginning of the year: December 2017 Business Confidence surged by 96.4, November Retail Sales of 8.20% (consensus at 3.10%) and inflation is contained at 4.6% (way below the 13.6% hike in 2008). For these reasons we maintain our stance that South Africa is on its way to further economic growth for the 2018 outlook. This week we will be looking at December 2018 Consumer Price Index (January 24th 2018) and December 2018 Trade Balance (January 31st 2018).

Technical Outlook: GBPUSD Cracked 1.40 Barrier But Consolidation Could Be Expected Before Bulls Continue

Cable cracked psychological 1.40 barrier today, posting new post-Brexit vote recovery high at 1.4002, but was unable to sustain break at first attempt and eased back to 1.3940 in early European trading.

Further consolidation before final break higher could be expected as daily studies are overbought and traders started to take profits on larger longs at 1.40 target.

However, overall strong bullish sentiment keeps pound well supported and clear break above 1.40 pivot would trigger stops parked above and spark fresh bullish acceleration towards 1.4100 (round-figure barrier) and 1.4123 (FE 161.8% of current wave C of five-wave sequence from 1.3038).

Buying on correction remains favored scenario, with 4-h Tenkan-sen marking initial support at 1.3929, followed by Kijun-sen at 1.3879 and hourly trough at 1.3838 (18 Jan low).

Key near-term support lies at 1.3787 (rising 10SMA) and extended dips should reverse above it to keep bullish structure intact and avoid risk of deeper pullback seen on break.

Res: 1.4002, 1.4050, 1.4100, 1.4123

Sup: 1.3929, 1.3879, 1.3838, 1.3804

USDJPY Direction Still Defined By 110.80 Level

The U.S dollar remains range-bound against the Japanese yen, with buyers and sellers both failing to establish a clear intraday trend in early week trading. The Bank of Japan earlier kept monetary policy unchanged, causing the USDJPY pair to briefly drop towards the 110.58 support level, however, the pair quickly recovered back towards the 110.80 pivot. Going forward, traders will look to a raft of U.S data coming out later this afternoon, and the key 90.00 to 90.50 range on the U.S dollar trade weighted index.

USDJPY intraday buyers retain control of the pair while price trades above the 110.80 level, further buying towards 111.22 and 111.48 still appears likely.

Should USDJPY sellers push the pair below the 110.80 level, a further sell-off towards 110.48 and 110.18 seems possible.

GBPUSD Strongly Bullish Above 1.3944 Level

The British pound has moved to a fresh nineteen-month trading high against the U.S dollar, hitting 1.4002 in early Tuesday trading, as the U.S dollar index slips lower. The GBPUSD pair has continued to advance, despite the U.S government shutdown coming to an end on Monday, after a short-term spending agreement was made for the next three-weeks. Going forward, sterling buyers are looking to extend the upside rally above the 1.4000 level, with the 1.4030 level the next technical barrier head.

The GBPUSD pair remains strongly bullish while trading above the 1.3944 level, key upside resistance levels for the pair remain 1.4000 and 1.4030.

Should price-action on the GBPUSD pair start to trade below the 1.3940 level, intraday support is found at 1.3927 and 1.3880.

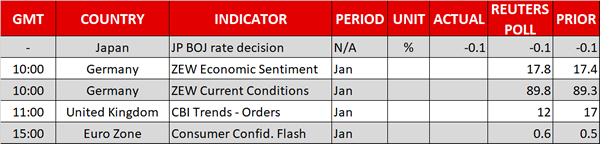

Eurozone Sentiment Indicators In The Spotlight On Tuesday

After a slow start to the week, Tuesday sees a broad pickup in reporting activity with a pair of Eurozone reports set to make headlines.

The ZEW Centre for European Economic Research will report a pair of sentiment indicators gauging institutional investor confidence. The German report will be released alongside the euro-wide data set at 10:00 GMT. Both indicators are expected to show a slight uptick in the economic sentiment index for January.

Later in the day, the European Commission's statistical agency will report on consumer confidence for the month of January. The preliminary reading is expected to show a slight increase to 0.6 from 0.5 in December.

In other European releases, the UK Office for National Statistics will report on public sector net borrowing for the month of December. Later in the session, the Confederation of British Industry (CBI) will release its industrial trends survey for January.

Shifting gears to the United States, the Richmond Federal Reserve Bank will release its monthly manufacturing index at 15:00 GMT. The manufacturing indicator is expected to dip slightly to 19 from 20 in December.

Energy traders will also be keeping a close eye on the weekly crude inventory report courtesy of the American Petroleum Institute (API). The US Energy Information Administration (EIA) will issue the official data set the following morning.

Oil prices have been riding multi-year highs in January, with investors rallying behind an improved supply-demand outlook in the global market. ICE Brent crude futures briefly traded above $70 a barrel, a positive sign for global producers.

In monetary policy news, the Bank of Japan (BOJ) voted to keep interest rates unchanged on Tuesday, as officials continued to look for signs of inflation. The Japanese central bank is maintaining ultra-low interest rates in support of a broader economic recovery that is finally showing signs of materializing.

EUR/USD

The euro maintained its composure on Monday even as the dollar showed signs of life following a decision by the Senate to reopen the US federal government. The EUR/USD exchange rate was last seen hovering around 1.2264, where it was little changed compared to the previous close.

USD/JPY

The dollar was back on the defensive against the yen, with the USD/JPY exchange rate falling 0.3% to 110.66. The yen is benefitting from a brief bout of risk aversion tied to geopolitical risks. In the short term, prices face a strong resistance around the 100-day SMA of 111.75.

CRUDE OIL

Crude oil has been one of the biggest stories of 2018 with prices rallying above the $70 mark on several occasions. UK crude prices were last seen hovering around $69.40 a barrel. The outlook remains firmly higher, with investors eyeing gains north of the psychological $70 barrier.

Technical Outlook: EURUSD Remains In Extended Consolidation And Eyes Fresh Direction Signals

The Euro remains within choppy consolidation after initial attempt above 1.2300 barrier failed.

Price action is holding in red on Tuesday, descending from Asian session high at 1.2275 and moving in the lower side of 1.2213/75 congestion on hourly chart.

Further easing could violate initial support at 1.2213 and expose 1.2192 (top of thickening 4-hr cloud which underpins near-term action), break of which would risk test of key near-term support at 1.2165 (consolidation range low).

Overall picture remains firmly bullish and sees scope for further advance, but looking for a catalyst to spark fresh action.

Today’s German/EU ZEW economic sentiment reports are the first events which could stronger influence Euro’s near-term action, followed by EU Consumer confidence and key event for the Euro this week, ECB’s policy meeting on Thursday.

Forecasts show ZEW numbers higher in Jan (17.8 f/c vs 17.4 previous – Germany and 29.7 f/c vs 29.0 previous – EU) but the figures are lower from the same period last year.

EU’s consumer confidence is forecasted at 0.6 in Jan vs 0.5% in Dec, which will be the second positive reading since Jan 2001.

Overall bullish techs remain supportive, however, further easing cannot be ruled out as daily RSI is turning south after holding in sideways mode in past few days and slow stochastic continues to trend lower.

Key supports lay at 1.2182 (rising 10SMA) and 1.2165 (consolidation floor) and sustained break here is needed to signal further easing.

Res: 1.2275, 1.2296, 1.2323, 1.2360

Sup: 1.2213, 1.2200, 1.2182, 1.2165

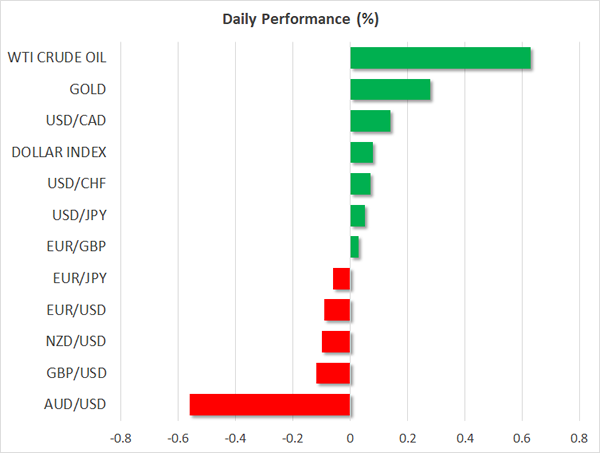

Yen Whipsaws After BoJ And Aussie Tumbles On Trade Risk As World Leaders Gather In Davos

Here are the latest developments in global markets:

FOREX: The US dollar index traded slightly higher on Tuesday, in the aftermath of Congress voting for a temporary funding bill, thereby ending the US government's partial shutdown.

STOCKS: Equities were in the green across the board. Japanese markets skyrocketed, with the Nikkei 225 and the Topix closing higher by 1.3% and 1.0% respectively; both indices reached fresh 27-year highs. In Hong Kong, the Hang Seng surged by 1.35%, breaking another all-time high, seemingly unfazed by increasing trade tensions between the US and China. In Europe, futures tracking the Euro Stoxx 50 are up 0.5%. Last but not least, the equity winning streak in the US continued unabated, with the Dow Jones, S&P 500 and Nasdaq Composite all closing at record highs once more. Futures tracking the Dow, S&P and Nasdaq 100 are all currently in positive territory as well.

COMMODITIES: Oil prices traded higher, with WTI and Brent crude being up 0.6% and 0.5% respectively. Although there is no clear fundamental catalyst behind the moves, the advances are being attributed to signs that healthy global economic growth could strengthen demand for the precious liquid. In precious metals, gold was higher by nearly 0.3%, last trading near $1336 per ounce.

Major movers: Yen whipsaws after BoJ; aussie tumbles on rising trade tensions

The Japanese yen whipsawed on Tuesday, in the aftermath of the Bank of Japan's (BoJ) policy decision. The BoJ kept its policy framework unchanged as was widely expected, while it upgraded its language around inflation expectations, which it now describes as “more or less unchanged” from “weakening” previously. This triggered a modest surge in the JPY, though the advance was short-lived, with the currency giving back all its gains to trade even lower against its major counterparts after Governor Kuroda stepped up to the rostrum.

The Governor sought to reassure investors that there is no need to adjust the Bank's policy framework simply due to a rise in inflation expectations, as actual inflation remains far away from its target. Moreover, he poured cold water on expectations that the Bank is moving towards the stimulus-exit door, noting that changes to day-to-day bond buying operations do not indicate the future course of monetary policy. Overall, the key message from the BoJ was that Japan's economy is gradually improving, but with inflation still so low, it is far too soon for markets to be speculating whether the Bank will scale back its massive stimulus program.

In the US, the government's partial shutdown ended yesterday after Congress voted in favor of a temporary funding bill that will keep public services running until the 8th of February.

The British pound surged on Monday, with sterling/dollar briefly touching the 1.4000 mark before pulling back, with no major piece of news behind the advance. Market chatter suggests that sterling's recent gains are being driven by a repricing of the Brexit risk premium, amid signs that the negotiations are slowly but surely moving forward, and that the two sides may soon agree on a transitional Brexit deal.

Elsewhere, aussie/dollar plunged overnight, weighed on by signs of increased protectionism in the US, after President Trump approved tariffs on imported solar cells and certain washing machines. This prompted China to reply in strong rhetoric, condemning the US action. The risk of further escalation in trade tensions between the world's two largest economies appears to be high, and should China decide to reply in similar fashion, then the AUD could extend its losses. Given Australia's heavy trade exposure to China, anything that could harm the Chinese economy is considered as a negative for the Australian dollar, which is seen as a liquid proxy for “China plays”.

Day ahead: Business surveys, politics and corporate earnings on the horizon

The ZEW research institute's surveys that gauge economic sentiment and current conditions in Germany, the eurozone's as well as Europe's largest economy, are scheduled for release at 1000 GMT. Both surveys are anticipated to reflect an improvement relative to December, with the reading on current conditions forecast to rise to its highest since 2011.

Remaining within Germany and turning to politics, there were some reports suggesting that talks to form a government between Chancellor Merkel's conservative bloc and the Social Democrats will commence today.

The Confederation of British Industry's survey on factory orders is expected to reflect a reduction in January after matching November's three-decade high in December. The relevant figure is due at 1100 GMT.

Eurozone flash consumer confidence for the month of January will be made public at 1500 GMT. The reading – released by the European Commission's Directorate General for Economic and Financial Affairs – is expected to come in in positive territory for the third straight month, as well as reflect an improvement for the sixth month in a row.

The US Senate Banking Committee will be holding a hearing on the nomination of Marvin Goodfriend as a member of the Federal Reserve Board of Governors at 1500 GMT.

The World Economic Forum in Davos, Switzerland is underway. Policymakers from around the world will be attending, with US President Donald Trump also likely to join although it is still not certain due to the government shutdown complications that took place in the US.

Weekly API data including information on crude inventories are due at 2135 GMT.

The earnings season continues with Johnson & Johnson, Procter & Gamble and Verizon being among the big names releasing quarterly results on Tuesday; all three will be reporting before the US market open.

Technical Analysis: EURUSD remains fairly close to 3-year high; bearish signal by stochastics in very short-term

EURUSD is currently trading not far below January 17's more than three-year high of 1.2322. The positively aligned Tenkan- and Kijun-sen lines continue to point to a bullish bias for the pair, though the two lines getting flatter suggests that positive momentum in the short-term is weakening. Turning to the stochastics, they are giving a bearish signal in the very short-term: the %K line has crossed below the slow %D line and both lines are moving lower.

In case of positive momentum in German government coalition talks, euro/dollar might receive a boost. In this case, the area around last week's three-year high of 1.2322 would come into view as a potential barrier to the upside.

In a stalemate scenario though, euro/dollar could face some weakness. In such an event, the range around 1.22 – this being a potential psychological mark – could offer support.

Technical Outlook: USDJPY – Limited Upside Despite US Deal, Speculations BoJ May Scale Back Monetary Stimulus

The dollar probed again above 111.00 handle on Tuesday, inflated by news that US policymakers reached a deal to temporarily end the shutdown of the government.

In addition, BoJ stayed unchanged as expected in today's policy meeting, with no signs of tightening in the short term, heard from governor Kuroda's speech after the meeting.

The central bank will maintain its easy stance as CPI remains weak and is ready to further ease and hold momentum for inflation rise towards projected 2% target.

However, greenback's recovery attempts on Monday/today were limited, keeping the downside vulnerable.

Upticks through falling 10SMA (currently at 110.96) were so far unable to make sustained break higher, keeping near-term risk shifted lower for renewed attacks at key 110.15/00 supports (Fibo 61.8% of 107.31/114.73 rally/psychological support).

Loss of initial supports at 110.49 (Monday/today's low) would open way towards 110.15/00 pivots, break of which would trigger fresh bearish acceleration..

Conversely, close above 10SMA will be initial bullish signal for further recovery and will unmask key barriers at 111.48 (18 Jan recovery high) and 111.72 (200SMA).

Res: 111.17, 111.22, 111.48, 111.72

Sup: 110.74, 110.49, 110.15, 110.00