Sample Category Title

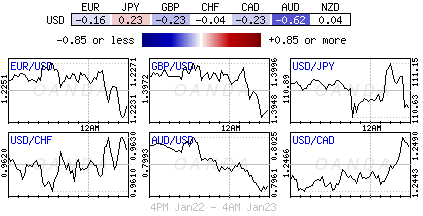

EUR/GBP Skewed To The Downside

EUR/GBP is trading mixed. The pair is distancing the resistance at 0.8929 (01/12/2017 high) and endures downward pressure. Support at 0.8761 (14/12/2017 low) is being monitored. Expected to show further decline.

In the long-term, the pair has largely recovered from lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading below the range of its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

USD/JPY Volatile But Upward Oriented

USD/JPY's demand increases at lower pace and is held at 111.10. Still a long way to go before reaching the 111.50 (17/01/2018) resistance point. Hourly support is now at 110.33 (15/01/2018 low). The technical structure suggests further short-term upside moves.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Increase

GBP/USD is upward oriented. The strong resistance at 1.3940 (17/01/2018) is now broken. The technicals is therefore positive. Hourly support remains at a distance of 1.3458 (11/01/2018 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is now moving upward. A long-term support given at 1.1841 (07/10/2017 low) and a strong resistance at 1.5018 (24/06/2016 high) are identified.

EUR/USD Ready For Another Leg Higher

EUR/USD is slowly increasing. The pair is maintained at a resistance given at 1.2325 (17/01/2018 high) and hourly support at 1.2165 (17/01/2017 low). The technical structure suggests further short-term upside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while stron

AUD/USD Bearish Momentum

AUD/USD's upside pressure is weakened. Supporting trend channel is almost reached. New resistance point is at 0.8040 (19/01/2018 high). Support at 0.7849 (12/01/2018 low) is distanced. The technical structure indicates further short-term downside move.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Rising Potential

USD/CAD remains weak but is slowly reaching the 1.2520 (17/01/2018 high) resistance. Hourly support is given at 1.2370 (17/02/2018 low). Further resistance is given at 1.2589 (01/01/2018). Expected to show short-term gains.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). New support point is identified at 1.2101 (17/04/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head lower. The pairs is trading below 200 DMA.

USD/CHF Increase Maintained

USD/CHF is trading slightly higher. The technical structure indicates that potential weakness achievable. Hourly support is given at 0.9533 (19/01/2018 low) and hourly resistance remains at 0.9668 (18/02/2018).

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

Market Update – European Session: German ZEW Current Situation Survey Hits An All-Time High

Notes/Observations

German ZEW Survey handily beats expectations to hit a record high as optimism prevails in Germany

BOJ tweaks language on inflation expectations; now saw it as flat compared to its prior view of being in a weakening phase

Asia:

BOJ kept its policy steady (as expected). Left Interest Rate on Excess Reserves (IOER) unchanged at -0.10% and maintained its policy framework of "QQE with Yield Control" around 0.00% and asset purchases at annual pace of ¥80T. Vote to keep policy steady was again 8 to 1 (Kataoka issued dovish dissent for 4th straight meeting and called for JGB purchases so that bond yields of maturities of 10-year+ fall broadly)

BOJ Quarterly Outlook for Economic Activity and Prices saw a tweak in language. Medium- to long-term inflation expectations had been more or less unchanged recently, after having remained in a weakening phase since summer 2015.

Europe:

Eurogroup called on the Greek authorities to complete the outstanding prior actions as a matter of urgency; following full implementation of prior actions by Greece euro zone bailout fund ESM will approve disbursement of new loans; new ESM loans to total €6.7B euros, to be disbursed to Greece in two tranches, starting in February with €5.7B euros for debt servicing needs

Greece Ministry memo: Greece govt could issue a new bond as early as Feb

UK Foreign Minister Boris Johnson said to demand an extra £5B annually for NHS beginning next year. Would frame the demand in terms of how best to take on Labour’s Corbyn rather than revisit his referendum claim that Britain will be better off by £350M a week in saved EU

Americas:

Senate and House passed a stop gap funding bill officially ending the 3 day govt shutdown; deal currently funds the govt until Feb 8th; bill signed by President Trump.

Senate agreed that if a global deal on immigration was not reached by Feb 8th, the Senate would immediately move to a fair process of debate and a vote on DACA; .

President Trump has approved recommendations to impose tariffs on imports of washing machines and solar cell manufacturers based on findings from the US International Trade Commission (ITC): imposed tariffs of 30% on solar power products in first year; and would fall 5% in each subsequent year for 3 year

Economic Data:

(DK) Denmark Dec Retail Sales M/M: -0.3% v 0.0%e; Y/Y: 1.1% v 2.4% prior

(DK) Denmark Dec Consumer Confidence: 8.2 v 7.0e

(ZA) South Africa Nov Leading Indicator: 105.4 v 105.4 prior

(TR) Turkey Jan Consumer Confidence: 72,3 v 65.1 prior

(TW) Taiwan Dec Industrial Production Y/Y: 1.2% v 1.2%e

(HK) Hong Kong Dec CPI Composite Y/Y: 1.7%e v 1.6% prior

(UK) Dec Public Finances (PSNCR): £25.1B v £13.2B prior; Public Sector Net Borrowing: £1.0B v £4.3Be

(DE) Germany Jan ZEW Current Situation Survey: 95.2 v 89.6e; Expectations Survey: 20.4 v 17.7e

(EU) Euro Zone Jan Expectations Survey: 31.8 v 29.0 prior

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) opened its book to sell new 10-year bond; guidance seen +46bps to mid-swaps

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B target in 2032, 2040, 2044 and 2048 bond

(ES) Spain Debt Agency (Tesoro) sold total €1.455B vs. €1.0-2.0B indicated range in 3-month and 9-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.3% at 403.4, FTSE +0.3% at 7730, DAX +0.8% at 13576, CAC-40 +0.1% at 5550 , IBEX-35 +0.4% at 10625, FTSE MIB +0.3% at 23952 , SMI +0.6% at 9583, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices continue to rally following another all time closing high in Wallstreet overnight, and strong markets in Asia as risk on sentiment continues. US futures point to another higher open with strong subscriber growth in Netflix helping the Nasdaq futures which trades higher by 0.3%. In France shares of Carrefour outperforms after announcing its 2022 ambition as well as partnerships in China. On the earnings front Easyjet trades over 5% higher following Q1 Rev beat; Logitech is higher after strong results. On the other hands Biomerieux, SGS and GEA Group trade lower following results and outlook. Looking ahead notable earners include Dow components Johnson and Johnson, Verizon, Travellers and P&G.

Movers

Consumer Discretionary [Easyjet [EZJ.UK] +6.1% (Earnings), Carrefour [CA.FR] +6.3% (Job cuts, partnership with Tencent), Sky [SKY.UK] +2.7% (CMA finds deal with FOXA not in public best interest), Pets At Home [PETS.UK] +7% (Earnings), Brown (N) Group [BWNG.UK] -12% (Trading update)]

Industrials [SGS [SGSN.CH] -2.5% (Earnings), GEA Group [G1A.DE] -1.6% (Cuts outlook)]

Financials [ Tryg [TRYG.DK] -2.6% (Earnings)]

Technology [ Logitech [LOGN.CH] +4% (Earnings)]

Energy [National Grid [NG.UK] -1.9% (Ofgem confirmed that the grid upgrade, currently estimated to cost around £800m to build, is needed)]

Speakers

ECB Q1 Lending Survey: Overall terms on corporate and household loans continued to ease. Q4 loan demand rose in all categories and saw rising loan demand in Q1

Portugal Econ Min Cabral: Country was reducing its debt to GDP ratio while the Banking sector was reducing bad loans

Sweden Central Bank Gov Ingves reiterates view at a hearing on financial stability that high indebtedness made the domestic economy vulnerable

Sweden Financial Supervisory Authority (FSA) Dir Thedeen: Still saw risks among households in banking sector but the sector resilience was satisfactory

Hungary Central Bank: No need to raise the counter-cyclical capital buffer - German ZEW Economists noted that the latest survey showed optimism for H1

BoJ Gov Kuroda post rate decision press conference reiterated view that would adjust policy as needed to maintain momentum towards 2% price target but saw no need to adjust yield curve control (YCC). Reiterated not in situation to consider exit from QQE, still some distance to meeting inflation target; need to maintain 'strong' monetary easing. Day to day JGB buying operations did not indicate future course of monetary policy. Target was yield curve and not the amount of JGB purchases. Did not see yen (JPY) rise in particular, as US dollar (USD) decline stem from Euro strength.

Thailand Central Bank Gov Veerathai: Trying to ensure that THB currency (Baht) is not too volatile; will not target specific levels in FX. Currency was at risk of increased volatility. To ensure Baht won’t impact business; not seeking trade advantage

Taiwan Central Bank official Yen reiterated view that TWD currency was determined by market forces

Japan Econ Min Motegi believed that thet start date for Trans-Pacific-Partnership would not change; March 8th is the target date for signing the agreement

Brazil Lower House Speaker Maia said to provide an alternative to pension reform

IEA chief Birol stated that he expected oil market volatility as price growth spurs US shale; Potential further upward revision of US shale output

Currencies

USD was slight firmer as political developments helped to support the greenback. US Senate helped to pass legislation to fund the government until Feb. 8th

EUR/USD hovered in the 1.2240 area as market participants showed little excitement to the recent German coalition developments in its effort to forge together a grand coalition. Focus turning to the ECB rate decision on Thursday for hints on forward guidance

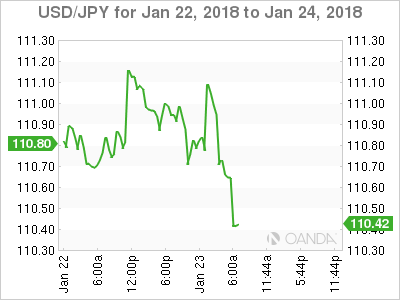

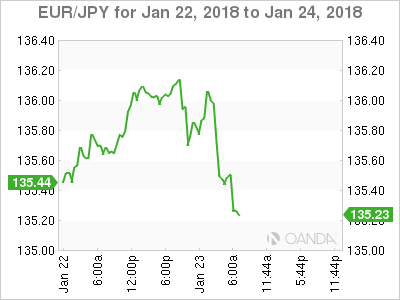

The main focus in FX was on the JPY currency. Bank of Japan helped push the yen higher after its quarterly forecasts tweaked the language on inflation and now noted that inflation expectations were flat compared to its prior view of it being in weakening phase. USD/JPY was softer by 0.2% just ahead of the NY morning at 110.70.

Fixed Income

Bund Futures trades up 36 ticks at 160.95 after German ZEW current situation had the highest reading since the beginning of the survey in Dec 1991. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 123.59 up 19 ticks and above the January 12th low of 123.48. Support continues to stand at 123.50 then 122.83, with upside resistance at 124.25 then 124.96.

Tuesday’s liquidity report showed Monday’s excess liquidity rose to €1.872T from €1.863T prior. Use of the marginal lending facility fell to €219M from €237M prior. - Corporate issuance saw 3 issuers raise $3.2B in the primary market

Looking Ahead

(RO) Romania Dec M3 Money Supply Y/Y: No est v 12.5% prior - (UR) Ukraine Dec Industrial Production M/M: No est v 0.3% prior; Y/Y: No est v 0.3% prior

(AR) Argentina Central Bank (BCRA) Interest Rate Decision: Expected to leave 7-Day Repo Rate unchanged at 28.00%

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (UK) DMO to sell 0.125% 2026 I/L Gilts (UKTi)

05:30 (DE) Germany to sell €5.0B in 0% 2019 Schatz

05.30 (UK) Weekly John Lewis LFL sales data

06:00 (UK) Jan CBI Industrial Trends Total Orders: 12e v 17 prior, Selling Prices: No est v 23 prior, Business Optimism: No est -11 prior

06:00 (BR) Brazil Mid-Jan IBGE Inflation IPCA-15 M/M: 0.4%e v 0.4% prior; Y/Y: 3.1%e v 2.9% prior

06:00 (TR) Turkey to sell 2027 and 2028 Bonds

06:30 (EU) ESM to sell €2.0B in 6-month bills

06:45 (US) Daily Libor Fixing

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (PL) Poland Dec M3 Money Supply M/M: 1.9%e v 0.6% prior; Y/Y: 4.4%e v 4.5% prior

08:05 (UK) Baltic Dry Bulk Index - 08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserve

09:00 (MX) Mexico Nov IGAE Economic Activity Index (Monthly GDP) Y/Y: 1.2%e v 1.5% prior

10:00 (EU) Euro Zone Jan Advance Consumer Confidence: 0.6e v 0.5 prior

10:00 (US) Jan Richmond Fed Manufacturing Index: 18e v 20 prior

10:30 (CA) Canada to sell 3-month, 6-month and 12-month Bills

11:30 (US) Treasury to sell 4-Week Bills

13:00 (US) Treasury to sell 2-Year Notes

14:00 (AR) Argentina Dec Trade Balance: -$0.9Be v -$1.5B prior

16:30 (US) Weekly API Oil Inventories

Euro Shrugs Off Sharp German, Euro Confidence Reports

The euro has ticked lower in the Tuesday session. Currently, EUR/USD is trading at 1.2248, down 0.11% on the day. In economic news, German ZEW Economic Sentiment improved to 20.4, beating the estimate of 17.8 points. Eurozone ZEW Economic Sentiment followed the same trend, climbing to 31.8, above the forecast of 29.7 points. In the US, the sole event is the Richmond Manufacturing Index, which is expected to edge lower to 19 points. On Wednesday, Germany and the eurozone release services and manufacturing PMIs.

The US government shutdown is over, after just three days. On Monday, the Senate voted 266-150 to extend funding until February 8. This stopgap measure will enable the government to provide services during that time, but the parties will have to hammer out a longer-term agreement. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

The ECB holds a policy meeting on Thursday, and traders should not expect any dramatics at the first policy meeting of 2018. The Bank is expected to retain its pledge to continues buying bonds under its asset-purchase program (QE). The ECB has trimmed QE from EUR 60 billion to 3o billion/mth, but is likely to hold interest rates for 3-6 months after that. Still, ECB policymakers have hinted that the Bank could wind up QE in September, and this pushed the euro higher in recent weeks. If ECB President Mario Draghi hints at an end to QE, the euro will likely gain ground. Draghi may prefer to keep a low profile until March, after policymakers have had a chance to review updated economic forecasts.

Central Banks Dictate FX Moves While Stocks Rock

Tuesday January 23: Five things the markets are talking about

Global equities have found fresh impetus for another attempt at new record highs, as investor optimism has again surged amid corporate earnings and the end of the U.S government shutdown.

And this despite U.S President Trump imposing, thus far, selected tariffs (on solar panels and washing machines) to achieve his own ‘level' playing field. Next step for investors is to see how markets will respond to Trumps selective protectionist policies.

The U.S dollar has found some traction against the EUR and GBP, along with U.S treasuries and gold. The outlier is JPY, which has rallied after the Bank of Japan (BoJ) dampened market speculation that Japanese policymakers are close to reducing monetary stimulation.

U.S government employees return to work after their three-day partial shutdown on Trumps signing of a temporary government-spending bill.

Note: Barring any last minute changes in Washington, President Trump is expected to join world leaders in Davos for the annual World Economic Forum.

1. Stocks ‘rock'

Equities probe fresh highs after U.S. government shutdown ends.

Fresh yen strength did nothing to deter Japanese stock investors, with the Nikkei closing above 24,000 for the first time since November 1991. At the close, the index was +1.3% higher.

Down-under, Aussie shares ended higher on Tuesday, snapping a five-session losing streak following Wall Street after U.S. senators struck a deal to end a three-day government shutdown. The S&P/ASX 200 index rallied +0.75%. In S. Korea, the Kospi added +1.4%.

In Hong Kong, stocks hit a fresh record, helped by Chinese money inflows. The Hang Seng index ended up +1.7%, while the China Enterprises index rallied +2.2%.

In China, banks and property firms powered China stocks to fresh two-year highs. At the close, the Shanghai Composite index was up +1.3% while the blue-chip CSI300 index was up +1.08%.

In Europe, Germany's DAX index has hit an all-time peak, and France's CAC is heading for its highest close in 12-years.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.3% at 403.4, FTSE +0.3% at 7730, DAX +0.8% at 13576, CAC-40 +0.1% at 5550, IBEX-35 +0.4% at 10625, FTSE MIB +0.3% at 23952, SMI +0.6% at 9583, S&P 500 Futures +0.2%

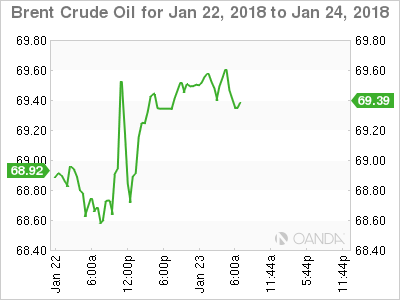

2. Oil supported by economic growth

Oil prices are on the march again, lifted by healthy economic growth as well as the ongoing supply curtailments by OPEC and Russia.

Brent crude futures are at +$69.38 a barrel, up +35c or +0.5% from Monday's close, not far off their three-year high of +$70.37 reached on Jan. 15. U.S West Texas Intermediate (WTI) crude futures CLc1 is at +$63.93 a barrel, up +36c, or +0.6% from their last settlement. WTI rose to its highest since December 2014 on Jan. 16 at +$64.89.

Traders said oil markets were generally well supported by healthy economic growth.

Note: The International Monetary Fund (IMF) on Monday revised upward its forecast for world economic growth in 2018 and 2019, to +3.9% for both 2018 and 2019, a +0.2% point increase from its last update in October.

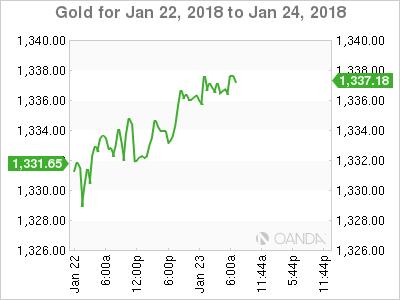

Gold prices have edged up overnight as the U.S dollar hovers atop of its three-year lows, with a surge in global equities capping further gains. Spot gold has rallied +0.2% to +$1,336.26 per ounce, up for a third straight session.

3. Sovereign yields fall after BoJ decision

Global bond yields have edged down overnight after the BoJ played down speculation that it was close to ending its stimulus, raising hopes that the European Central Bank (ECB) may follow suit Thursday.

The BoJ kept its policy steady, as expected and left Interest Rates on Excess Reserves (IOER) unchanged at -0.10%, while maintaining its policy framework of “QQE with Yield Control' around 0.00% and asset purchases at annual pace of ¥80T.

The vote to keep policy steady was again 8 to 1. There were no surprises that Kataoka issued his “dovish' dissent for a fourth consecutive meeting and called for further JGB purchases so that bond yields of maturities of 10-year+ fall broadly.

Note: The bond markets have been hit in recent weeks by growing talk that central banks in Japan and Europe could end monetary stimulus sooner rather than later.

The ECB meets on Thursday against a backdrop of heightened speculation over when it will end its QE program and signal a rise in interest rates from record lows.

The yield on 10-year Treasuries have fallen -3 bps to +2.62%, the biggest tumble in almost four-weeks, while in Germany, the 10-year Bund yield has declined -2 bps to +0.55%, the lowest in almost two weeks.

4. Dollar sits atop of three-year lows

The USD is a tad firmer against a number of currencies, aside from JPY, as political developments helped to support the greenback. The U.S Senate helped to pass legislation to fund the government until Feb. 8th.

The U.S dollar has dipped -0.33% to ¥110.55 after the BoJ maintained its short-term interest rate target at -0.1% and a pledge to guide 10-year government bond yields around zero percent. Governor Kuroda also said, “inflation expectations have moved sideways recently,' offering a slightly more upbeat view than three-months ago when he said they were on a “weak' note.

The EUR (€1,2255) continues to hover in yesterday's range as the market showed little enthusiasm to Sunday's German coalition developments in its effort to forge together a grand coalition. Market focus will now switch to the ECB's rate decision on Thursday for hints on forward guidance.

Bitcoin (BTC) was down -4.5% on the Bitstamp exchange at +$10,320.13 following news that S. Korea will ban the use of anonymous bank accounts in cryptocurrency trading from Jan. 30.

5. German ZEW survey handily beats expectations

Data this morning showed that German economic sentiment rose in January and that investors remained optimistic about Germany's near-term growth prospects despite the country's struggle to form a governing coalition.

The ZEW headline measure of economic expectations rose +3 points to 20.4, beating market forecasts of 17.5 points.

Digging deeper, financial analysts and investors polled were also more upbeat about Germany's current situation and the corresponding ZEW measure hit its highest level in 26-years.

The survey shows that Europe's largest economy continues to prosper despite its difficulties forming a governing coalition.