Sample Category Title

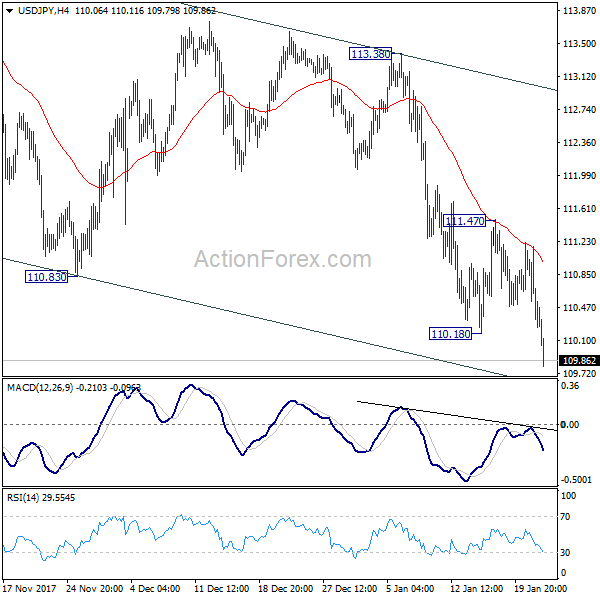

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.96; (P) 110.57; (R1) 110.88; More...

USD/JPY's fall resumed by taking out 110.18 and reaches as low as 107.09 so far. Intraday bias is back on the downside for lower channel support (now at 109.55). We'll look for bottoming signal around there. but Break of 111.47 resistance is needed to indicate short term bottoming. Otherwise, deeper decline is expected. Firm break of the channel support would pave the way to retest 107.31 low.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Yen Extending Rally Supported by Strong PMI and Exports, Dollar Back Under Pressure

Japanese Yen trades broadly higher today as supported by upbeat economic data. In particular, USD/JPY has now taken out 110.18 support (last week's low). Recent fallcould be extending towards next key support level at 107.31. Dollar is again back under pressure with weakness most notable against Sterling. In other markets, Nikkei is trading in red by -0.6% at the time of writing. That followed mixed US markets. S&P 500 and NASDAQ extended the record runs but DOW closed flat.

Japan PMI manufacturing hits near 4 year high

Japan PMI manufacturing rose to 54.4 in January, up from 54.0 and beat expectation of 54.3. The index has now stayed in expansionary region above 50 for the 17th consecutive month. January's reading was also the highest since February 2014. IHS Markit economist Joe Hayes noted in the statement that "the strongest reading in the PMI since February 2014 was supported by quickened rates of output and employment growth."

Also from Japan, adjusted trade balance showed surplus of JPY 86.8b, below expectation of JPY 270b. Nonetheless, the set of data is pretty strong. Exports rose 9.3% yoy to JPY 7.3T, largest since September 2008. Exports to China, the biggest trading partner, jumped 15.8% yoy and hit record JPY 1.5T. Imports jumped even larger by 13.9% yoy.

Powell confirmed as 16th Fed chair

Jerome Powell was confirmed by the Senate to be the 16th chairman of Fed. The final vote of the Senate was overwhelming by 84 to 13. Powell will officially take over the role from Janet Yellen early next month and is given a four-year term. Senate Banking Committee chairman Mike Crapo hailed that Powell will be "central to ensuring a safe and sound financial system while supporting a vibrant, growing economy." And he "will play a key role in rightsizing federal regulations and alleviating unnecessary burdens."

Nine Democrats and four Republicans opposed to the nomination. With progressive Democrat Elizabeth Warren expressing her concerns that Powell will " begin weakening the new rules Congress and the Fed put in place after the 2008 financial crisis."

Looking ahead

Eurozone PMIs and UK job data are the main focuses of today. The Euro has been trading mixed this week despite up beat confidence data. On the other, Sterling is lifted by hope of a good Brexit deal and is trading as the strongest one. Price actions in EUR/GBP suggest that it's heading down to 0.8688 near term support. And today's data might trigger some movements in the cross.

Later in the day, US will release PMIs, house price index and existing home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.96; (P) 110.57; (R1) 110.88; More...

USD/JPY's fall resumed by taking out 110.18 and reaches as low as 107.09 so far. Intraday bias is back on the downside for lower channel support (now at 109.55). We'll look for bottoming signal around there. but Break of 111.47 resistance is needed to indicate short term bottoming. Otherwise, deeper decline is expected. Firm break of the channel support would pave the way to retest 107.31 low.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Dec | 30% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Dec | 0.09T | 0.27T | 0.36T | 0.29T |

| 0:30 | JPY | PMI Manufacturing Jan P | 54.4 | 54.3 | 54 | |

| 8:00 | EUR | France Manufacturing PMI Jan P | 58.6 | 58.8 | ||

| 8:00 | EUR | France Services PMI Jan P | 58.9 | 59.1 | ||

| 8:30 | EUR | Germany Manufacturing PMI Jan P | 63 | 63.3 | ||

| 8:30 | EUR | Germany Services PMI Jan P | 55.5 | 55.8 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Jan P | 60.3 | 60.6 | ||

| 9:00 | EUR | Eurozone Services PMI Jan P | 56.4 | 56.6 | ||

| 9:30 | GBP | Jobless Claims Change Dec | 2.3K | 5.9K | ||

| 9:30 | GBP | Claimant Count Rate Dec | 2.30% | |||

| 9:30 | GBP | Average Weekly Earnings 3M/Y Nov | 2.50% | 2.50% | ||

| 9:30 | GBP | ILO Unemployment Rate 3Mths Nov | 4.30% | 4.30% | ||

| 14:00 | USD | House Price Index M/M Nov | 0.40% | 0.50% | ||

| 14:45 | USD | US Manufacturing PMI Jan P | 55 | 55.1 | ||

| 14:45 | USD | US Services PMI Jan P | 54.4 | 53.7 | ||

| 15:00 | USD | Existing Home Sales Dec | 5.72M | 5.81M | ||

| 15:30 | USD | Crude Oil Inventories | -6.9M |

GBP/USD Surges Above 1.4000, UK’s Employment Report Next

Key Highlights

- The British Pound traded higher this week and broke the 1.4000 mark against the US Dollar.

- There is an ascending channel forming with support at 1.3960 on the 4-hours chart of GBP/USD.

- The current market sentiment is positive and the pair is likely to move past 1.4050.

- Today, the UK Claimant Change Count for Dec 2017 will be released, which is forecasted to post 5.4K, down from the last 5.9K.

GBPUSD Technical Analysis

The British Pound is in a major uptrend above the 1.3900 support area against the US Dollar. The GBP/USD pair is holding bullish and eyes UK's employment report for Dec 2017 to make the next move.

Looking at the 4-hours chart of GBP/USD, there was a sharp rise from the 1.3450 swing low. The pair broke the 1.3600 and 1.3800 resistance levels to gain upside traction.

It touched 1.4003 before starting a downside correction. Sellers were able to push the pair below the 23.6% Fib retracement level of the last wave from the 1.3838 low to 1.4003 high. However, the pair found strong bids on the downside, recovered and moved above the 1.4020 level.

At the moment, it seems like there is an ascending channel forming with support at 1.3960 on the same chart. The channel support at 1.3960 is near the 38.2% Fib retracement level of the last wave from the 1.3838 low to 1.4036 high.

Therefore, the 1.3960 support holds a lot of importance in the near term. As long as the pair is above the 1.3960 and 1.3920 support levels, it remains in an uptrend. Should there be a decline below 1.3900, the pair could test the 1.3800 level.

On the upside, the 1.4000 handle was a monster resistance for buyers. A daily close above the mentioned 1.4000 level suggests more gains going forward. The next major hurdles for GBP/USD are 1.4080 and 1.4120.

Fundamentally, the UK Claimant Change Count for Dec 2017 will be released today. The market is not looking for any major change, which means if the outcome exceeds the forecast, British Pound could gain a lot of bullish traction.

Market Morning Briefing: Euro-Yen Has Dropped Further As The Yen Strengthened More Than The Euro

STOCKS

Dow (26210.81, -0.01%) is almost stable. We maintain our view of a rise towards 26400-26500 in the coming sessions .

Dax (13559.60, +0.71%) opened with a gap up and is trading higher just now. While above 13500, there is scope of further rise towards 13750 or even higher in the coming sessions.

Nikkei (23989.08, -0.56%) has paused near current levels and could be stuck in the 24150-23500 region for a couple of sessions before again trying to move up. Note that levels near 24200 is a decent near term resistance and if that holds, there could be a short dip or a sideways consolidation in the coming sessions.

Shanghai (3534.29, -0.34%) has come off from levels near 3557 maybe due to a fall in Copper prices as inventories surged and could come off towards 3525-3500 levels in the next few sessions. Note that 3500 is an immediate support and could hold for now. On a break above 3557 in the medium term, there is scope of testing 3600 in the longer run.

Nifty (11083.70, +1.07%) and Sensex (36139.98, +0.96%) has been rising since the last few days and it would be difficult to say what the immediate target would be. A test of 11200-11400 looks a possible scenario for the near term on the Nifty while for the Sensex 36500-36700 seems possible. A pause to the rising rally could be well seen by the end of the month.

COMMODITIES

Brent (69.77) and WTI (64.38), both have moved up and have again come close to the resistance levels of 70 and 65 respectively. Lack of a strong rejection from these resistances arise a question of whether the bulls still have some strength to show in the near term. While below 70 and 65, some sideways movement could be expected in the near term.

Gold (1340.75) has moved up as expected but could face some rejection from important resistance near 1345-1350 levels. Only in case Dollar Index moves down sharply and pushes up Gold to levels beyond 1350, we would shift our focus to higher levels.

Copper (3.1340) fell sharply to levels below 3.20 contrary to our expectation of a rise towards 3.25. This is mainly due to a rise in the inventories. News states that Copper sank below $7000 a tonne to a one month low yesterday. We may expect some recovery towards 3.15 or higher by next week.

FOREX

Dollar Index (89.973) against our expectations has dropped below the crucial level of 90 as the Euro and Yen both have made gains on back of strong economic data in Europe and Japan respectively. Weakness in the dollar has come about inspite of the fact that the US government shutdown has ended. Moreover higher US bond yields relative to the German bunds or Japanese bonds are also not bringing about any significant strengthening for the Dollar. We should still wait before a decisive break below 90 is confirmed, since the index is still near support on daily candles and weekly candles. There could still be a bounce in the near term towards 91-91.5.

Euro (1.2309) has risen on back of stronger consumer confidence data and can be expected to stay below 1.2320-1.2330 (which is seen as immediate resistance on the daily candles) for few more sessions. We still maintain the likelihood of a drop towards support near 1.21 on daily candles before it attempts higher levels.

Dollar-Yen (110.05) has reacted to strong Japanese economy data inspite of a dovish stance by the Bank of Japan yesterday. It even went below 110 to 109.93 but is trading above 110 currently. We could now see Dollar-Yen testing support near 109.5 on the daily and 3 day candles after which there should be a bounce.

Euro-Yen (135.41) has dropped further as the yen strengthened more than the Euro. We might have to wait for a couple of sessions to get more directional clarity on whether it will first drop to test support near 134 on daily candles or, resume its rise towards resistance at 137.

Pound (1.4025) also rose against the Dollar and will attempt to test resistance near 1.41 on the weekly candles this week.

Dollar Rupee (63.78) is likely to spend the next few sessions in the 64.00-63.70 region (possible extension to 64.10 and 63.60).

INTEREST RATES

US 10 Yr (2.6168%), 30 Yr (2.8953%), 5 Yr (2.4171%) & 2 Yr (2.0561%) have all come down further since yesterday, after the highs of day before, reflecting that there has been some bullishness on US bonds after yields shot up. The US 30 Yr as mentioned yesterday, came down from resistance near 2.92% and is now at earlier resistance of 2.89-2.9% which could act as support for the time being. Oscillation in a very narrow range of 2.9-2.92% could be expected.

The US 10 Yr is trading just below earlier resistance at 2.62%, and it will be interesting to see if this level acts as support now, or whether the yield stays below this level, making it act as resistance once again.

Japanese 10 Yr (0.073%) has come down as the Bank of Japan appeared to be dovish and kept rates constant. There is some support near 0.062% on the short term charts which could be tested if there is further bullishness on Japanese bonds

The Bank Of Japan Policy Is Under Pressure

The Bank of Japan policy is under pressure

An extremely active twenty-four hours in all asset markets in what was expected to be an extremely busy and no less noisy week for the markets.

Currency markets were extremely active with traders primarily looking for opportunities to sell that dollar. Not only is the big 2018 consensus trade, long EURO, sniffing recent highs, but now Yen traders are getting into the act, despite the fact that BoJ Kuroda attempted to ice a soaring JPY

To summarise the dollar fell as if it had an anvil around its neck, as did US yields Tuesday, while US stocks remained relatively bid on stronger earnings. Similar to last week, we’re back plumbing significant support on the DXY ( 90.10), and again suggesting a breaker lower would make a convincing argument for a steeper drop in the dollar. But unlike last weeks attempt the dollar bears are back en masse with the JPY bulls pulling the cart this time around.

Japanese Yen’s Reaction to BoJ Rate Decision

Going into the BoJ, as mentioned yesterday, traders adopted a mindset that with Japans economy firing on all cylinders and signs of deflationary pressures abating, they would buy Yen regardless. Thinking that it’s just a matter of time before the market does the tightening for the BoJ.(i.e. similar to what’s going on in the EURO )

Price action said it all; the dollar sold on the rate announcement and when USDJPY failed to gain any traction above 111.20 after Kuroda dovish press conference, it was game on for the dollar bears. However, for the Oldtimers dialling in on the real nuance within the statement, the proof was in the pudding. “Prolonged downward pressure on financial institutions’ profits under the continued low-interest-rate environment could create risks of a gradual pullback in financial intermediation and of destabilising the financial system. However, at this point, these risks are judged as not significant, mainly because financial institutions have sufficient capital bases.”

So the system is bust, and the BoJ will need to tweak the YCC by perhaps moving down the curve targeting shorter dated tenors as currency markets have typically enjoyed a stronger relationship with the short end of the yield curve.

But the big challenge for the BoJ is how to deal with investors expectations as any tweak in policy will be viewed as an opportunity to hammer the USDJPY mercilessly lower. However, the issue at hand if the US yields continue to fall we will most certainly test the 110 level , and with a convincing break, all hell will break loose.

Energy Markets

OIL

Brent nudged above 70 for the first time this week after the IMF report concluded that the markets are in the midst of broadest synchronised global growth spurt since 2010.

The IMF’s beaming economic forecast along with stout compliance from OPEC and comrades in arms through 2018 and possibly beyond is providing convincing support.Comments from Saudi oil minister Khalid al-Falih over the weekend continue to resonate that the cartel and its allies should extend their production pact quota beyond 2018. While this all sounds fine and dandy, but ultimately absolute price points and missed opportunity costs will be the essential arbiter in future discussion, not Saudi oil minister rhetoric.

Nat Gas

China’s voracious energy consumption is coming to the fore as their nascent environmental movement takes hold all but suggesting Coals days are finally numbered, but LNG’s outlook looks outrageously bright. Without question, China’s switch from coal to natural gas is sending demand through the roof pushing up LNG prices to three-year highs.Given that its early days in China Green Movement, LNG producers are probably smiling after shooting themselves in the foot last year by oversupplying the markets.

Gold Markets

Gold could move higher as we are still in the early stages of a broader USD sell-off, with all eyes focused on 110 USD JPY

Besides the political hot spots in the middle east providing support, investors are looking to hedge equity positions. Investors are spooked by a possible escalation of trade wars and are becoming jittery about overextended equity valuations. All of which is pushing investors back under golds safety umbrella.

G-10

The Australian Dollar

Aussie tumbled yesterday as Iron ore plummeted amid US trade sanctions and discussions. Iron ore got hit lower as the Trump tariffs caught markets in low a physical demand period ahead of Chinese New Year which toppled Iron ore prices and crushed the Aussie dollar. Naturally, given Australia significant role in the global supply chain, there was a risk wobble as the market came off pretty hard. But we have subsequently based around. While I think Trade War Escalation is a bit of a Red Herring, Trump is a wild car so better not to take anything for granted. However, the edge did come off the mini trade inspired currency tantrum when the TPP agreement was rejuvenated and then Trump suggested NAFTA negotiations were going on well. A definite scare for long Aussie positions, but its game on this morning.

But let’s face it. the political optics of trade sanctions directed at China and South Korea are poor given that both countries leaderships are key backroom negotiators to resolve North Korea problem

The Euro

Without repeating the bullish EUR views, Buy on Dip

Malaysian Ringgit

Despite a bit of a risk wobble overnight on the back or trade discussions, the sun shines on the Ringgit again this morning. The combination of firmer oil prices .broad-based USD dollar weakness and positive risk sentiment on the back an IMF report that suggested we are in broadest synchronised global growth spurt since 2010, has the Ringgit positioned favourably heading into tomorrow MPC

MYR vs Possible Trade Wars.

The the first salvo was launched today in what could develop into a long drawn out ” tit for tat” trade battle between the US vs China and Korea, and possibly the rest of Asia. The US administration imposed tariffs on imported solar panels and washing machines, in a move towards what could develop into the trade war between some global economies.

EM Asia will be following these developments closely as trade-related fears are probably the most prominent external risks since most regional economies are very trade oriented.

However, given the Ringgit is less sensitive to external shocks than regional peers due to surging oil prices but nonetheless the MYR could wobble on an escalation of regional trade wars with the US.

Yen Gains Ground As BoJ Cautiously Optimistic

The Japanese yen has posted gains in the Tuesday session. Currently, USD/JPY is trading at 110.33, down 0.46% on the day. On the release front, the Bank of Japan maintained interest rates at -0.10% at its policy meeting. Later in the day, Japan releases Trade Balance and Manufacturing PMI. In the US, the sole event of the day, Richmond Manufacturing Index, posted a 3-month low. The indicator slowed to 14, well off the estimate of 20 points. On Wednesday, the US releases Existing Home Sales.

As expected, the Bank of Japan held interest rates in negative territory, at -0.10%. The monetary policy statement noted that the economy should continue to show modest expansion, and that the BoE would maintain current qualitative and quantitative monetary easing until consumer inflation hits the 2 percent target. Recently, there has been talk of the BoJ tightening its policy, given the rebound in the economy. However, BoJ Governor Kuroda has taken pains to reiterate that the Bank will not be changing its ultra-accommodative monetary policy anytime soon. In a quarterly review, the BoJ made no changes to its economic and inflation projections, and reiterated its forecast that inflation will reach the 2 percent target in the 2019-2020 fiscal year.

The US government shutdown is over, after just three days. On Monday, the Senate voted 266-150 to extend funding until February 8. This stopgap measure will enable the government to provide services during that time, but the parties will still have to hammer out a longer-term agreement on funding the government. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

Gold Moves Higher, Congress Ends Shutdown

Gold has edged higher in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1337.52, up 0.26% on the day. On the release front, it’s another quiet day in the US. The sole event of the day, the Richmond Manufacturing Index, slowed to 14, well off the forecast of 19 points. On Wednesday, the US will publish Existing Home Sales.

The US government shutdown turned out to be little more than a nuisance, with only one working day lost. On Monday, the Senate voted 266-150 to extend government funding until February 8. This stopgap measure will enable the government to provide services during that time, but the lawmakers will need to hammer out a longer-term agreement, as these short extensions are just band aid solutions. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

What can we expect from the Federal Reserve over the next few months? The Fed was busy in 2017, raising interest rates three times. This month, the Fed began to trim its balance sheet, to the tune of $10 billion/mth. Next up is a policy meeting on January 31. A rate hike is a virtual certainty, with CME Fed Watch pegging the odds of a quarter-point hike at 98.5%. Although this means that a rate hike has been priced in by the markets, the dollar could nevertheless gain ground after a hike, as a rate increase would signify an important vote of confidence in the economy by the powerful Fed. If the US economy continues to expand at a clip of around 3 percent, there is a strong likelihood of a second rate hike in the first half of 2018.

Pound Ticks Lower, Markets Eye UK Employment Reports

The British pound is trading sideways in the Tuesday session. In North American trade, GBP/USD is trading at 1.3975, down 0.14% on the day. In economic news, the British public sector deficit dropped sharply to GBP 1.0 billion, beating the estimate GBP 4.2 billion. In the US, the Richmond Manufacturing Index, slowed to 14, well off the forecast of 19 points. On Wednesday, the UK release key employment numbers, led by Claimant Change. The US will publish Existing Home Sales.

Despite plenty of hand wringing over Brexit, the British economy has been performing fairly well. Key employment numbers will be released on Wednesday, and the markets are expecting solid readings for unemployment rolls and wage growth. If these predictions prove accurate, investors could give a thumbs-up and push the pound higher. The markets are keeping a close eye on Preliminary GDP for Q4, which will be released on Friday. Earlier on Tuesday, the pound hit the symbolic 1.40 level for the first time since June 2016. The currency has impressed in January, jumping 3.6% against the dollar.

The US government shutdown turned out to be little more than a nuisance, with only one working day lost. On Monday, the Senate voted 266-150 to extend government funding until February 8. This stopgap measure will enable the government to provide services during that time, but the lawmakers will need to hammer out a longer-term agreement, as these short extensions are just band aid solutions. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

New Zealand CPI Forecast Remains Within RBNZ Target; Will Kiwi Continue Bullish Run?

The focus on Thursday will be on New Zealand's headline consumer price index number at 2145 GMT. New Zealand will release its fourth-quarter of 2017 CPI that is forecasted to show an increase of 0.4% from 0.5% in the previous quarter. Also, the attention will turn on the kiwi as there is plenty of room for a surprise if the release beats expectations.

Consumer prices in New Zealand ticked higher to 1.9% year-on-year in the third quarter from 1.7% in the prior period and for the Q4 is predicted to remain unchanged at 1.9%. For now, inflation sits comfortably in line with the Reserve Bank of New Zealand's (RBNZ) 1-3% target band.

Shifting to monetary policy, the RBNZ kept its official cash rate unchanged at record low of 1.75% in November 2017, as widely expected. The key rate last moved in November 2016 from 2.00% to 1.75%. and during the last meeting, the central bank stated that economic growth has continued to improve, although inflation and wages remain subdued.

Also, the gross domestic product growth rate for the third quarter advanced to 0.6%, slowing down after an upwardly revised reading of 1.0% expansion before. The RBNZ also mentioned that monetary policy will remain accommodative for a considerable period, as numerous uncertainties hold, and policy may need to adjust accordingly. It is worth mentioning that the country's hourly wages increased to 30.51 NZD/hour in the third quarter of 2017 from 30.15 NZD/hour in the second quarter of 2017. The next policy meeting will take place on February 8 and the bank is widely expected to adopt a wait and see stance and keep the interest rate unchanged at 1.75% until June 2019 at the earliest.

Despite the relatively solid economic data however, businesses have become more pessimistic about the economy since the general election in September 2017. The elections showed a victory for the ruling National Party and the previous Prime Minister Bill English, with the Party winning 46% of the votes compared to 35.8% gained by the opposition Labour Party, but New Zealand's proportional representation system means neither won enough seats in parliament to govern alone. A month later Jacinda Ardern, Leader of the Labour Party, became the 40th Prime Minister after the securing the backing of the country's third largest party – the New Zealand first.

The country's ANZ business sentiment remained negative for the third month in a row, while in December the index remained close to an 8-year low at -37.8 from -39.3 in November, on lingering uncertainty about policy direction under the new Labour-led government.

From the technical point of view, kiwi/dollar skyrocketed over the previous six weeks after the strong rebound on the 0.6815 support level. The pair has risen more than 7% since December 10 as the US dollar has come under broad pressure.

In addition, the price climbed to a fresh 4-month high of 0.7353 today, and if the consumer price index surpasses the consensus, then the expectation is a run until the 0.7370 resistance level. A break above the aforementioned obstacle could open the door towards the next immediate resistance of 0.7430 taken from the significant top on September 20.

A worse-than-expected figure could create a downward pressure for the pair and would retest the 0.7210 support level, which holds near the 200-simple moving average in the daily timeframe.

Will UK Jobs Data Boost or Temper Sterling’s Rally?

UK employment data for November are due to be released on Wednesday at 09:30 GMT. Looking simply at economic forecasts, one may be tricked into thinking this data set represents little risk for sterling, as every indicator is projected to remain unchanged. The unemployment rate is forecast to have held steady at 4.3%, while average weekly earnings (both including and excluding bonuses) are anticipated to have grown at the same pace as previously.

What will markets focus on? Assuming the unemployment rate remains unchanged as anticipated, investors are likely to turn their attention to average weekly earnings, for any potential surprises. Wages are extremely important, especially in the context of the UK economy. Following the Brexit vote, inflation accelerated sharply, but wage growth remained largely flat, leading to a squeeze in the real incomes of UK consumers. This is one of the key factors that has deterred the Bank of England (BoE) from raising interest rates too much.

The Bank considers the surge in inflation to be a transitory effect that will fade over time, caused by the depreciation in GBP back in 2016. As such, it is reluctant to raise rates in order to fight high inflation, as that could weigh further on incomes and thereby, hurt consumption and the broader economy. Thus, an acceleration in wages would probably be a very pleasant development for policymakers, as it could open the way for the Bank to hike rates at a faster pace. Conversely, any slowdown in wages would probably keep the BoE sidelined for even longer.

So, what do gauges of the labor market suggest? The Markit UK report on jobs painted a relatively upbeat picture in November, indicating that staff appointments rose at the quickest pace for three months, and supporting the forecast for the unemployment rate to hold steady. In terms of earnings, it noted that despite easing slightly since October, wage growth remained sharp, amid strong demand for staff and a shortage of skilled workers.

A stronger-than-anticipated employment report, particularly on the wages front, could add to speculation that the BoE may raise interest rates faster than what is currently expected over the coming years. Something like that could add fuel to sterling's recent rally, with sterling/dollar likely to surge and target its recent highs at 1.4000. A potential upside break of that territory could open the way for the 1.4050 zone, marked by the lows of March 2016.

On the contrary, a disappointment in this data set could cause sterling/dollar to give back some of its recent gains. Immediate support may be found near 1.3890, but if the bears are strong enough to overcome that hurdle, the next area that could come into play is 1.3840.