Sample Category Title

Dollar Losing Streak Continues, UK Employment And Wage Growth Data Due

Here are the latest developments in global markets:

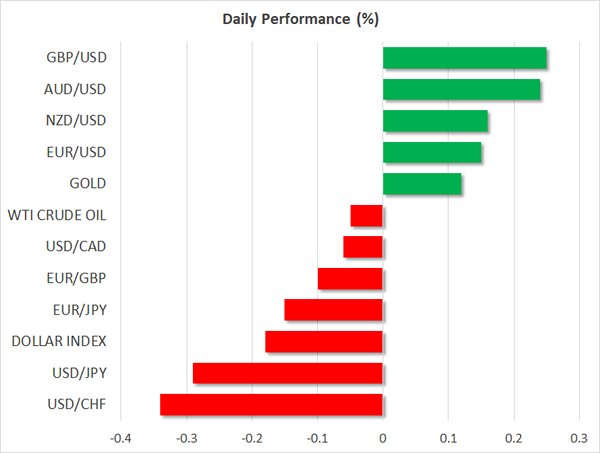

FOREX: The dollar index traded nearly 0.2% lower on Wednesday, extending the losses it posted yesterday amid concerns of a potential escalation in trade tensions with China.

STOCKS: Japanese equities corrected lower, with the Nikkei 225 and the Topix indices closing down by 0.8% and 0.5% respectively, as the latest surge in the yen took its toll on the nation’s markets. That said, both indices still stand near their corresponding 27-year highs. In Hong Kong, the Hang Seng was up by 0.2%, reaching a fresh all-time high. European investors appeared undecided, with futures tracking the Euro Stoxx 50 being flat, suggesting the index could open around yesterday’s close. The US saw yet another record high close for the S&P 500 and Nasdaq Composite yesterday, while the Dow Jones closed marginally in the red. Futures tracking the Dow, S&P and Nasdaq 100 are all currently in positive territory.

COMMODITIES: Oil prices traded slightly lower on Wednesday, giving back some of the gains they posted yesterday. The correction lower came after the private API inventory data – released overnight – showed that crude stockpiles rose during the last week, following nine consecutive weeks of drawdowns. Gold was 0.1% higher, last trading near $1343 per ounce. Technically, a potential upside break of the recent highs at $1344 could pave the way for advances towards the September highs at $1357, especially if the greenback remains on the back foot, helping to boost demand for the dollar-denominated precious metal.

Major movers: USD touches fresh 3-year lows on protectionism concerns

The greenback came under renewed selling pressure yesterday, with the dollar index falling to find support near the psychological level of 90.00. The selloff appears to be driven by worries around the protectionist set of measures introduced by the US recently, with markets potentially discounting the scenario of an analogous response from China that escalates the situation further, thereby harming both economies. The Australian dollar will likely be very sensitive to any updates in this story, as a US-China trade standoff could harm the Australian economy as well, due to its large trade exposure to China.

Euro/dollar broke above 1.23, boosted by the dollar’s underperformance. That said, the pair may be at risk of a modest correction today, as investors may opt to take some profits off the table ahead of the ECB policy decision tomorrow, where the central bank’s President, Mario Draghi, could talk down the euro.

Sterling/dollar breached 1.40 yesterday for the first time following the Brexit vote. Even though the latest leg up reflects more dollar weakness than sterling strength, evident by the subdued moves in euro/sterling and sterling/yen, the broader rally in the pound is undeniable, and is likely a result of markets repricing the Brexit risk premium amid growing optimism around the negotiations. However, there appears to be a risk of markets running ahead of themselves, as pricing-out Brexit concerns still appears somewhat premature at this stage. Excluding some constructive comments by French President Macron recently, there have been no material developments on the Brexit front that could justify such a sizeable rally. Expectations that the two sides are due to agree on a transitional deal by the end of March are elevated, suggesting that any disappointment in that process has the capacity to dent optimism around the negotiations, and perhaps the pound itself.

Day ahead: Eurozone PMIs, UK employment & wage growth and Davos on the agenda

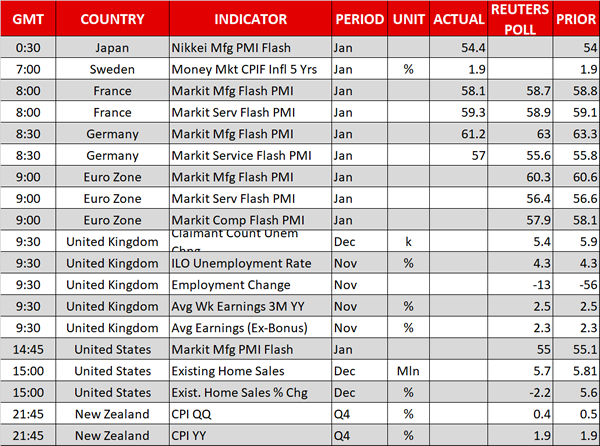

Eurozone flash PMI figures for the month of January – for the manufacturing and services sectors, as well as the composite measure that blends the two – will be made public at 0900 GMT. All three readings are anticipated to slow down relative to December’s releases, though not by much, remaining comfortably above the 50 threshold that separates expansion from contraction and continuing to project a relatively positive picture on eurozone growth. Deviations from expectations – and depending on the extent of the deviation of course – can lead to changes in positioning on the euro. Germany and France, the eurozone’s two biggest economies, saw the release of their respective figures earlier in the day; both countries’ services PMIs surprised to the upside, with their manufacturing PMIs missing forecasts.

The UK will see the release of important employment and wage growth data at 0930 GMT. The unemployment rate is expected to remain at the four-decade low of 4.3%, with the bulk of investors’ interest likely falling on average weekly earnings – year-on-year they’re anticipated to expand at the same pace as in the previous month. Growth on that front could spur expectations for further BoE tightening sooner rather than later; at the moment inflation outpaces wage growth, rendering it a risky endeavor to raise rates as it could further weigh on economic growth. Sterling is likely to be sensitive to today’s releases.

Out of the US, Markit’s January flash manufacturing PMI due at 1445 GMT and data on December existing home sales to be released at 1500 GMT will be attracting attention. The manufacturing PMI is expected at 55.0, only slightly below the respective figure from the previous month and existing home sales are forecast to decline by 2.2% after hitting an 11-year high in November.

New Zealand inflation figures for Q4 2017 are due at 2145 GMT. On an annual basis, the CPI reading is expected to grow by 1.9%, the same pace as in Q3, while it is forecast to reflect a slowdown on a quarterly basis; expectations are at 0.4%, down from Q3’s respective figure of 0.5%. The bank’s target range for annual inflation is 2% plus/minus 1%.

Trump administration officials, including the President himself, will be heading to the World Economic Forum in Davos, Switzerland on Tuesday and Wednesday. Trade could emerge as a hot topic at Davos after the Trump administration’s recent decision to impose tariffs on washing machines and solar panels.

Beyond Davos, other policymaker appearances include a discussion on the Riksbank’s current monetary policy by the Swedish central bank’s Deputy Governor Martin Floden. The discussion is set to commence at 1030 GMT and will be taking place at a Moody’s seminar on Credit Trends.

The EIA report including information on US crude and gasoline inventories for the week ending January 19 is due at 1330 GMT. Crude stocks are expected to decrease by 1.3 million barrels, posting their tenth straight weekly decline. This compares to a drawdown of around 6.9m barrels in the week that preceded.

On the corporate earnings front, Comcast and General Electric will be among companies releasing their results before Wednesday’s opening bell on Wall Street, with Ford following suit after the US market close.

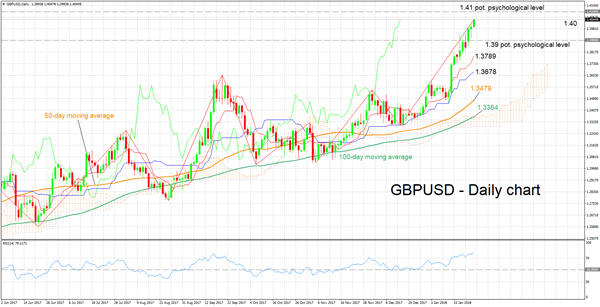

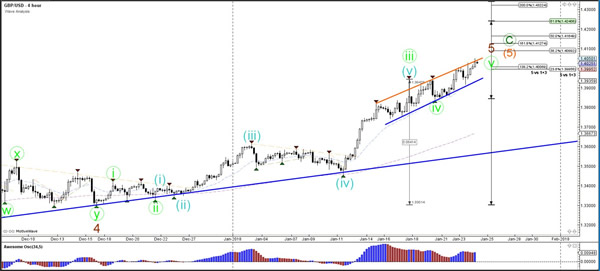

Technical Analysis: GBPUSD touches fresh 1½-year high; RSI overbought

GBPUSD has advanced considerably in recent weeks, reaching a fresh more than one-and-a-half year high of 1.4048 during today’s trading. The Tenkan- and Kijun-sen lines are positively aligned and the RSI is rising; all these point to a bullish short-term picture. However, notice that the RSI indicator is in overbought territory above 70.

Should today’s UK readings on employment and wage growth come in stronger than expected, then the pair is expected to gain, with the area around the 1.41 handle – a potential psychological level – coming into view as a potential barrier to the upside.

If the releases disappoint though, GBPUSD is likely to lose ground. In this case, support could come around the 1.39 level, this being another potential psychological mark. The 1.40 handle, which is relatively close to where price action is currently taking place, might function similarly as well.

Assuming an overextended market, it is worthy to point out that a data miss is likely to be met with a larger decline than an “equivalent” data beat (as it might spur profit-taking as well.)

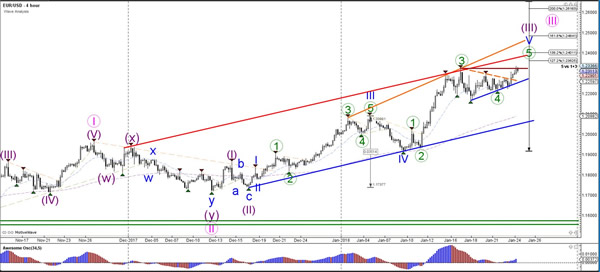

Technical Outlook: EURUSD Could Extend To 1.25 Zone On Break Above 1.2350 Trigger

The Euro moved higher on Wednesday and hit new high at 1.2335, the highest since mid-Dec 2014, completing shallow correction (1.2323/1.2165) and signaling further advance. Strong bullish sentiment was boosted by upbeat figures from EU / Germany on Tuesday (German / EU ZEW came well above expectations and EU Consumer confidence heavily beat forecast). Daily techs are in firm bullish setup and support the rally, along with weaker dollar, dragged by fresh strength of Japanese yen. Bulls eye next important target at 1.2350 (18 Dec 2014 high) firm break of which would open way towards 1.25 zone (17 Dec 2014 high lies at 1.2514). German/EU PMI data are key releases for the single currency today (all forecasts are slightly below previous month numbers), with focus on key event of this week – ECB interest rate decision, due tomorrow. Broken 1.2300 barrier acts as initial support, with rising 10 SMA (1.2226) expected to contain downside attempts. Key supports lay at 1.2105 (rising 20SMA) and 1.2036 (Fibo 38.2% of 1.1553/1.2335 ascend) and break here would generate stronger bearish signal.

Res: 1.2335, 1.2350, 1.2376, 1.2435

Sup: 1.2300, 1.2270, 1.2250, 1.2226

Currencies: USD Is Fighting An Uphill Battle

Sunrise Market Commentary

- Rates: More outperformance of US Note future vs Bund?

Short covering in an oversold US Treasury market started after US yields failed to pierce through key resistance levels after the end of the government shutdown. The correction can continue today, causing more outperformance of the US Note future vs the Bund. Another strong batch of EMU PMI's could weigh on the Bund from the EMU side. - Currencies: USD is fighting an uphill battle

The dollar couldn't profit from the end of the US government shutdown. Any USD up-tick was again used to offload USD longs with USD/JPY taking the lead. Investors also don't want to be positioned short euro/long dollar going into tomorrow's ECB meeting. Will Draghi be able to change fortunes for the euro?

The Sunrise Headlines

- US stock markets ended marginally higher with Nasdaq outperforming, receiving a strong boost from Netflix. Asian risk sentiment is more mixed overnight with Japan underperforming on yen strength.

- The Senate confirmed Jerome Powell to become the 16th chairman of the Federal Reserve, clearing the way for a new leader likely to continue raising interest rates to keep the nation's economic expansion on track.

- Japan's exports to China and Asia hit record levels as shipments rose for a 13th straight month in December and manufacturing growth hit a four-year high in January, pointing to an economy that powered through Q4 and into 2018.

- China's Ministry of Commerce condemned the US tariffs, calling them a misuse of trade measures, and said it hopes Washington will show restraint in imposing trade restrictions.

- Robert Mueller wants to question Trump about firing former FBI Director Comey and removing Flynn as national security adviser, a person familiar said, indicating the probe is intensifying its focus on possible obstruction of justice

- Eleven countries aiming to forge an Asia-Pacific trade pact after the United States pulled out of an earlier version will sign an agreement in Chile in March, Japan's economy minister said, in a big win for Tokyo.

- Today's eco calendar contains EMU PMI's, the UK labour market report and US existing home sales. The US Treasury continues its refinancing operation with 2-YR FRN and a 5-YR Note auctions

Currencies: USD Is Fighting An Uphill Battle

USD remains in the defensive

Dollar sentiment eroded again yesterday. The (temporary) solution of the government shutdown didn't help the USD. EMU eco data were strong, but no big factor for the EUR/USD rise. Broad-based USD softness prevailed. US yields failed to stay above key resistance levels and eased slightly. USD/JPY's price action was telling. Yen weakness after soft BOJ comments was soon undone and used to reduce USD exposure. USD/JPY dropped from 111+ levels to close the session at 110.31. EUR/USD revisited 1.23 and closed the session at 1.2299.

Overnight, Asian equities mostly trade with modest gains. Japanese trade data were ok with imports (14.9% Y/Y) rising faster than exports (9.3%), indicating a healthy economic context. Japanese equities underperform, suffering from a further rise of the yen. Yesterday's USD decline continues. USD/JPY dropped below the 110 barrier. EUR/USD set a minor new top in 1.2335 area. AUD/USD tries to sustain north of 0.80.

EMU PMI's are expected to ease slightly after last month's peak levels . The US Markit PMI's and existing home sales will only be of intraday significance. Global factors (comments on US tariffs in Davos), US interest rate markets and a positioning in the run-up to the ECB meeting will drive USD trading. The ST term trend is clearly USD negative. Investors are cautious on euro short positions going into the ECB meeting. Draghi will probably maintain a soft tone and warn on the impact of a strong euro to reach the inflation target. Whatever the outcome of tomorrow's ECB meeting, we look for signs of a pause on the recent euro rally. Global Picture: the dollar is in the defensive as markets prepare for a change in policy from central banks outside the US. This propelled EUR/USD despite a huge interest rate differential in favour of the dollar. The USD decline slowed last week, but the trend remains in place for now. A return below previous resistance at 1.2092 is needed to call off the ST alert for the dollar. EUR/USD 1.2598 (62% retracement) is next important resistance on the charts.

Sterling's rebound slowed yesterday despite constructive UK eco data. EUR/GBP settled in the upper half of the 0.87 big figure. Cable was well bid near 1.40 on USD weakness. Today, UK labour market data will be published. The report showed tentative signs of a loss of momentum in job creation last month. Weekly earnings are expect stable at 2.3% Y/Y. Another soft report might slow the recent performance of sterling. EUR/GBP is drifting lower in the 0.8928/0.8692 consolidation range. We keep the view that the EUR/GBP 0.87 area is a tough support.

EUR/USD: testing cycle top ahead of the ECB meeting

Daily Wave Analysis: US Dollar Shows Bearish Breakout Below Price Patterns

Currency pair EUR/USD

The EUR/USD broke above theresistance (dotted orange) of the triangle chart pattern, which could mark a continuation of the uptrend.A break above the previous top (dark red) could see price move towards the Fibonacci targets of wave 5 (blue) at 1.24 and 1.25.

The EUR/USD is challenging the previous top which could cause a potential retracement. If a pullback does occur, then the broken tops (blue) could become future support. A bullish breakout however could price move towards the 261.8% Fib target at 1.2362 and higher targets such as 1.24 and 1.25.

Currency pair GBP/USD

The GBP/USD bullish channel broke above the 1.40 resistance and is moving towards the Fibonacci targets. Price has reached the upper trend line (orange) of the bullish channel which could act as a potential resistance.

The GBP/USD indeed completed a wave 3-4 (blue) pattern as expected in yesterday’s analysis. Price could be in a wave 5 (blue) now. A bullish breakout could see price move towards the 161.8% Fibonacci target.

Currency pair USD/JPY

The USD/JPY broke the support trend line (dotted blue) and is continuing with the downtrend, which therefore indicates that the wave 2 or B (light purple) is still open. Price has respected the 38.2-50% Fib zone and could be moving towards the Fibonacci targets.

The USD/JPY bearish breakout is probably part of a wave 5 (blue) after completing a lengthy wave 4.

AUDUSD Trades Near 0.8000, Bullish Phase Remains Intact

AUDUSD has been outperforming over the last month, after the rebound on the strong psychological level of 0.7500, which coincides with the medium-term ascending trend line. The pair has been in bullish phase since January 2016, supported by higher bottoms and higher peaks.

During the prior week, the price reached a new 4-month high near the 0.8040 resistance level, while the short-term indicators are also pointing to a continuation of the bullish bias. The 20 and 40-day simple moving averages are following the significant upward movement of the price, signaling further gains.

In addition, the RSI indicator is still holding in the overbought area and is pointing to the upside. However, there is also the case of a bearish scenario as the upswing may be running out of steam and the risk of a near-term correction is high. The stochastic oscillator is creating a bullish crossover within the %K and the %D slightly below the overbought zone.

After this month's strong moves, the expectation for the pair is for further profit taking and could drive the price until the 0.8100 handle if the price surpasses 0.8040. A penetration above the aforementioned obstacle could open the door for the next immediate resistance of 0.8125.

On the flip side, if prices reverse lower, the next pause could be on the 0.7900 support level, which coincides with the 20-day SMA at the time of writing.

Forex Analysis: PMI Data Released Today In Europe And The US

Today we will have PMI data coming in from various economies around the world. Japan has already reported, with Europe next up, followed by the US in the afternoon. Japanese PMI data is close to a four-year high, showing good economic health in the manufacturing sector and the wider economy. Purchasing Managers Index measures the relative level of business conditions based on employment, production, new orders, prices, supplier deliveries and inventories in the manufacturing sector, giving an advance indicator of economic health.

Private Oil Stocks data was released yesterday afternoon, showing a surprise build in inventories. Crude inventories were up +4.754M. The price for WTI moved slightly lower on the data but has since recovered and is trading around $64.47

UK Public Sector Net Borrowing (Dec) was released on Tuesday and missed by a considerable amount, coming in at £0.979B despite being expected to come in at £4.400B, from £8.118B previously, which was revised down to £6.645B. EURGBP moved higher from 0.87686 to 0.87863 following this data release.

Eurozone ZEW Survey – Current Situation (Jan) was 31.8 v an expected 29.7, with a previous reading of 29.0. German ZEW Survey – Economic Sentiment (Jan) was 20.4 v an expected 17.8, with a previous reading of 17.4. German ZEW Survey – Current Situation (Jan) was 95.2 v an expected 89.8, from 89.3 prior. EURUSD fell from 1.22527 to 1.22227 in the time following the release of this data.

Eurozone Consumer Confidence (Jan) was 1.3 v an expected 0.6, from 0.5 previously. EUR pairs and Eurozone assets can be influenced by this data release.

Japanese Adjusted Merchandise Trade Balance (Dec) was released at ¥86.6B v an expected ¥261.7B, from ¥364.1B previously, which was revised down to ¥289.6B. Merchandise Trade Balance Total (Dec) was ¥359.0B v an expected ¥520.0B, with a prior of ¥113.4B. Exports (YoY) (Dec) were 9.3% against an expected 10.1%, from 16.2% previously. Imports (YoY) (Dec) were 14.9% against an expected 12.3%, with a prior reading of 17.2%. USDJPY fell from 110.293 as a result of this data.

Japanese Nikkei Manufacturing PMI (Jan) was released coming in at 54.4 v 54.3 expected, with a prior reading of 54.0. Leading Economic Index was 108.3 against an expected 107.7, from 108.6 previously. Coincident Index was 117.9 v a consensus of 117.1, from 118.1 prior. USDJPY continued to sell off to a low of 109.800 as these data points were made public.

EURUSD is up 0.09% overnight, trading around 1.23092.

USDJPY is down -0.25% in early session trading at around 110.030.

GBPUSD is up 0.24% to trade around 1.40285.

USDCAD is down -0.04%, trading around 1.24146.

Gold is up 0.13% in early morning trading at around $1,343.06.

WTI is unchanged this morning, trading around $64.47.

Major data releases for today:

At 08:30 GMT, German Markit Manufacturing PMI (Jan) is expected to come in at 63.0 from 63.3 previously. Markit Services PMI (Jan) is expected at 55.6 v 55.8 previously. Markit PMI Composite (Jan) is expected to be 58.6 from 58.9 prior. EUR traders will be closely following this data release.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Jan) is expected to come in at 60.3 from 60.6 previously. Markit Services PMI (Jan) is expected at 56.4 v 56.6 previously. Markit PMI Composite (Jan) is expected to be 57.9 from 58.1 prior. EUR crosses could see a spike in volatility should actual released data differ from the expected consensus.

At 09:30 GMT, UK Average Earnings excluding Bonus (3Mo/Yr) (Nov) is expected unchanged at 2.3%. Claimant Count Change (Dec) is expected at 5.4K from a previous reading of 5.9K. ILO Unemployment Rate (3M) (Nov) is expected to be unchanged at 4.3%. Average Earnings including Bonus (3Mo/Yr) (Nov) is also expected to be unchanged at 2.5%. Claimant Count Rate (Dec) is expected to be released, with a previous value of 2.3%. GBP crosses could be influenced by this data release.

At 14:00 GMT, US Housing Price Index (MoM) (Nov) is expected to be 0.3%, from 0.5% previously.

At 14:45 GMT, US Markit Manufacturing PMI (Jan) is expected to come in at 55.0, from 55.1 previously. Markit Services PMI (Jan) is expected at 54.0 v 53.7 previously. Markit PMI Composite (Jan) is expected to be 53.5, from 54.1 prior. USD crosses may be heavily traded as a result of this data.

At 15:30 GMT, US EIA Crude Oil Stocks Change (Jan 19) will be released. The previous reading was -1.600M. The expected reading this time is in the region of -6.861M. A build on stocks would be bullish for WTI prices.

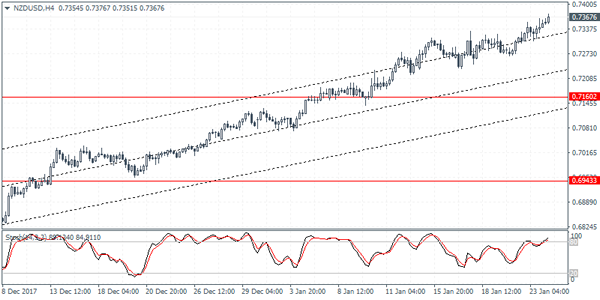

NZDUSD Intraday Analysis

NZDUSD (0.7367): The New Zealand dollar is looking to slowly edge higher with two consecutive days of gains. This comes amid Monday's bullish engulfing candlestick near the top end of the rally. Following a strong consolidation around 0.7300 level, NZDUSD is seen extending the gains closer to 0.7368 region. The continued upside momentum could keep prices supported near this level in the short term. Tonight's inflation report could however signal a short term correction in prices. Support is seen at 0.7160.

USDJPY Intraday Analysis

USDJPY (109.85): The USDJPY was seen extending the declines from yesterday. Price action broke past the 110.70 region of support with a strong bearish candlestick. On the 4-hour chart, the reversal coincides with the resistance level of 111.00 - 110.83. The declines could be extended to as far as 108.27 which marks the previously established support level around March 2017 and later in September last year. Any near term reversals could be seen to be short lived.

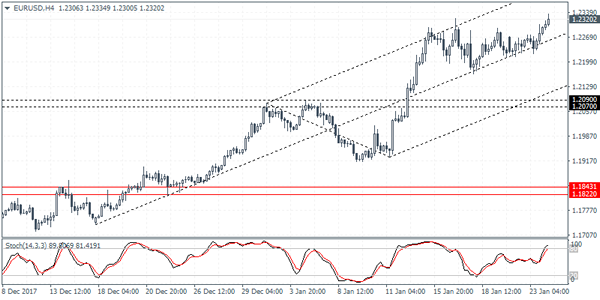

EURUSD Intraday Analysis

EURUSD (1.2320): The euro currency was seen turning bullish yesterday with price action seen extending the gains in the early Asian trading session today. The euro's gains came broadly from the USD's weakness. EURUSD managed to edge slightly higher trading near the 1.2300 handle. However, the current higher high posted is seen with the Stochastics oscillator forming a lower high. The divergence could potentially indicate a downside move in the euro. Price action is trading near the major resistance level of 1.2300 region. Unless there is a strong close above this level we expect to see the potential for a correction in the common currency.

UK Unemployment Rate Expected To Remain At Historic Lows

The U.S. dollar was on the defensive yesterday as the currency posted some sharp intraday volatility as the funding bill was approved for a few weeks. The USD continues to remain weak against its peers. Lack of economic data also made investors look at the broader themes.

BoJ's Kuroda held a press conference after the BoJ's statement was released. Reiterating the BoJ's commitment to its QE program, Kuroda quashed market expectations of a potential early exit to the central bank's monetary stimulus program.

The euro and the British pound managed to flirt near the highs. Data from Germany showed an improvement in the German ZEW economic sentiment. The index beat market consensus of 17.8 as it rose to 20.4, accelerating from 17.4 previously.

Looking ahead, investors will be focusing on the flash manufacturing and services PMI from Germany, France and the Eurozone. The UK's ONS will be releasing the monthly labor market statistics. The UK's unemployment rate is expected to stay put at 4.3% while average earnings are expected to rise at a steady pace of 2.5%.

Later in the evening, New Zealand will be reporting on its quarterly CPI figures. Economists have penciled a slower rate of inflation growth at 0.4% for the fourth quarter of 2017.