Sample Category Title

EUR/USD Renewed Buying Pressures

EUR/USD keeps on increasing. The pair has strongly bounced back and broke resistance at 1.2325 (17/02/2018). Hourly support is given at 1.2165 (17/01/2017 low). The technical structure suggests further short-term upside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Market Update – European Session: USD Weakness Gains Momentum After Treasury Sec Mnuchin Noted That He Was Not Concerned...

Notes/Observations

Potential shift in central bank policy communication cited as the driver of USD recent price weakness; focus turns to Thursday’s ECB decision

US Treasury Sec Mnuchin noted that he was not concerned about the level of the USD as it was good for trade

World Economic Forum annual meeting continues in Davos - Major European Manufacturing PMI move off multi-year highs

Asia:

Japan Dec Trade Balance registers a smaller surplus as exports slow to lowest growth since April (Trade Balance: ¥359.0B v ¥535Be with Exports Y/Y:9.3% v 10.0%e

Japan Jan Preliminary Manufacturing PMI nears a 4-year high ( 54.4 v 54.0 prior)

Europe:

Conservative MPs have told PM May that the UK must not be bound by EU rules during the Brexit transition period

Americas:

White House Econ Adviser Cohn: Trump's message at Davos will be to invest in America, not that he ws withdrawing the US from the global trade scene

President Trump: solar panel, washing machine tariffs show US will not be taken advantage of anymore; NAFTA negotiations going pretty well

Energy:

Weekly API Oil Inventories: Crude: +4.8M v -5.1M prior

Economic Data:

(FR) France Jan Preliminary Manufacturing PMI: 58.1 v 58.6e (16th month of expansion), Services PMI: 59.3 v 58.9e, Composite PMI: 59.7 v 59.2e

(ZA) South Africa Dec CPI M/M: 0.5% v 0.5%e; Y/Y: 4.7% v 4.7%e (9th straight month that CPI stays within the SARB target range of 3.0-6.0%)

(ZA) South Africa Dec CPI Core M/M: 0.3% v 0.2%e; Y/Y: 4.2% v 4.3%e

(CZ) Czech Jan Business Confidence: 16.4 v 17.1 prior; Consumer Confidence: 9.8 v 7.5 prior, Composite (Consumer & Business) Confidence: 15.1 v 15.1 prior

(DE) Germany Jan Preliminary Manufacturing PMI: # v 63.0e (37th month of expansion but moved off from record highs), Services PMI:57.0 v 55.5e, Composite PMI: 58.8 v 58.5e

(EU) Euro Zone Jan Preliminary Manufacturing PMI: 59.6 v 60.3e, Services PMI: 57.6 v 56.4e, Composite PMI: 58.6 v 57.9e

(PL) Poland Dec Unemployment Rate: 6.6% v 6.5%e

(UK) Nov Average Weekly Earnings 3M/Y: 2.5% v 2.5%e; Weekly Earnings (ex-bonus) 3M/Y: 2.4% v 2.3%e

(UK) Dec Jobless Claims Change: +8.6K v +12.2K prior; Claimant Count Rate: 2.4K v 2.3% prior

(UK) Nov ILO Unemployment Rate: 4.3% v 4.3%e, Employment Change 3M/3M: +102K v -12Ke

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

(EU) EFSF opens book to sell 0.125% Oct 2023 note; guidance seen -20bps to mid-swaps

(DK) Denmark sold total DKK2.28B in 2020 and 2027 Bonds

(SE) Sweden sold SEK2.0B vs. SEK2.0B indicated in 0.75% 2028 bond; Avg Yield: 0.8437% v 0.7161% prior; Bid-to-cover: 2.91x v 1.86x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 402.3, FTSE -0.5% at 7694, DAX -0.1% at 13544, CAC-40 -0.2% at 5524 , IBEX-35 -0.2% at 10588, FTSE MIB -0.2% at 23779 , SMI +0.5% at 9595, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade mostly lower, consolidating after recent gains with the exceptions of the Swiss SMI which trade modestly higher following strong results from Novartis which beat on the top and bottom line. The UK FTSE underperforms with continued strength in the Pound weighing. Notable earners this morning included Ahold Delhaize, which reported inline results, while an upbeat trading statement has pushed shares of JD Weatherspoons higher, with SMA Solar also higher following prelim results. Suez trades sharply lower after announcing another profit warning. Looking ahead notable earners include General Electric and United Technologies.

Movers

Consumer Discretionary [Barry Callebaut [BARN.CH] -1.8% (Prelim earnings), Ahold Delhaize [AD.NL] -2.9% (Prelim Q4), WH Smiths [SMWH.UK] -4.7% (trading update), SEB [SK.FR] -4.2% (Earnings), JD Weatherspoons [JDW.UK] +4% (Trading update), Staffline [STAF.UK] -2.6% (Earnings, CFO change)]

Financials [ Tryg [TRYG.DK] -2.6% (Earnings)]

Utilities [Suez [SEV.FR] -17% (Profit warning)]

Healthcare [ Novartis [NOVN.CH] +2.3% (Earnings)]

Energy [SMA Solar [S92.DE] +4.5% (Prelim earnings)]

Real Estate [Crest Nicholson [CRST.UK] -2.1% (Earnings)]

Speakers

ECB's Draghi QE bond buying has not led to a statistically significant exchange rate movement

Brexit Min Davis: Might publish Brexit paper on financial services. Expected to meet EU's chief negotiator Barnier during week of Jan 29th and aimed to maintain maximum access to European market. Expected a deal on transition before March

UK Trade Sec Fox commented from Davos that he was oen to some form of customs union with EU but UK must be able to sign its own trade deals beyond the EU

Eurogroup chief Centeno: Europe continued to look good fundamentally as economy has good momentum. Always worried about protectionist policies

Sweden Central Bank (Riksbank) Dep Gov Skingsley stated that made sense that tightening begins before the ECB as we achieved what we set out for in inflation (**in-line with recent rate statement). Forecasts now saw room for normalization but would be cautious on policy

Russia Econ Min Oreshkin: Russia GDP growth to reach 3.0-3.5% area in a few years

Turkey Dep PM Simsek commented from Davos that the TRY currency (Lira) depreciation could not go on forever. The country’s current account deficit (ex-gold) was reasonable

South Africa Central Bank (SARB) Gov Kganyago commented from Davos that the govt had taken decisive steps on reforms

Poland Central Bank Gov Glapinski stated that rates could increase in 2019 due to wage pressures

Indonesia Central Bank Gov Martowardojo reiterated view that sees small window for a rate adjustment

Treasury Sec Mnuchin commented from Davos that US Treasuries are not an issue in talks with China [**Reminder: On Jan 10th reports circulated that China Officials were said to view treasuries as less attractive and recommended slowing or halting Treasury buying (report was refuted by China FX Regulator SAFE)]

Brazil President Temer commented from Davos that Domestic economy is now growing after the recession . Both inflation and interest rates are falling

Currencies

USD continued to be on soft footing against the major pairs as central bank divergence themes continued to weigh upon the greenback. There continued to be mounting speculation that the ECB was near the end of its loose ultra-monetary policy. US Treasury Sec Mnuchin noted that he was not concerned about the level of the USD in the short-term as it was good for trade

EUR/USD was firmly above the 1.23 level for its highest level since December 2014 as the pair added to its recent surge since Nov (Euro stronger by 6% since then). Dealers noted that the rise in the euro had been in line with euro zone fundamentals. The recent break above the 1.21 level opened the door for a test towards 1,25. The key element for the Euro’s appreciation would be the level which would start to put pressure on inflation and thus creating an unwarranted tightening of monetary conditions

USD/JPY fell to its lowest level since September as the pair tested below 110

GBP/USD tested above the 1.41 level despite mixed wage and jobs data.

Fixed Income

Bund Futures trades down 25 ticks at 160.57 after major European countries missed on their preliminary manufacturing PMI’s. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 123.24 down 24 after strong UK employment data, the 10-year yield hit the highest level since October. Support continues to stand at 123.02 then 122.55, with upside resistance at 123.75 then 124.33.

Wednesday’s liquidity report showed Tuesday’s excess liquidity fell to €1.867T from €1.872T prior. Use of the marginal lending facility rose to €524M from €219M prior.

Corporate issuance saw 3 issuers raise $1.8B in the primary market

Looking Ahead

(BR) Brazil court rules whether former President Lula’s 9 ½ prison sentences for corruption will be upheld

(IL) Israel Central Bank (BOI) Jan Minutes

05:30 (SE) Sweden Central Bank (Riksbank) Dep Gov Floden

06:00 (RU) Russia to sell combined RUB40B in 2021 and 2028 OFZ bonds

To sell RUB25B in Dec 2021 OFZ bonds

To sell RUB15B in Jan 2028 OFZ bonds

06:30 (CL) Chile Central Bank Traders Survey

06:45 (US) Daily Libor Fixing

07:00 (CL) Chile Dec PPI M/M: No est v 1.1% prior

07:00 (US) MBA Mortgage Applications w/e Jan 19th: No est v 4.1% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (DE) German Chancellor Merkel at Davos

09:00 (US) Nov FHFA House Price Index M/M: 0.4%e v 0.5% prior

09:45 (US) Jan Preliminary Markit Manufacturing PMI: 55.0e v 55.1 prior, Services PMI: 54.3e v 53.7 prior, Composite PMI: No est v 54.1 prior

10:00 (US) Dec Existing Home Sales: 5.70Me v 5.81M prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:30 (US) Treasury to sell 2-Year Floating Rate Notes

12:00 (FR) France Dec Net Change Jobseekers: -19.3Ke v -29.5K prior; Total Jobseekers: 3.435Me v 3.454M prior

12:00 (CA) Canada to sell 3-Year Bonds

13:00 (US) Treasury to sell 5-Year Notes

14:00 (AR) Argentina Nov Economic Activity Index (Monthly GDP) M/M: No est v 0.2% prior; Y/Y: 4.0%e v 5.2% prior

16:00 (NZ) New Zealand Government 5-Month Financial Statements

16:45 (NZ) New Zealand Q4 CPI Q/Q: 0.4%e v 0.5% prior; Y/Y: 1.9%e v 1.9% prior

Euro Hits 3 Year High On Strong Services Reports

The euro continues to push higher this week. In the Wednesday session, EUR/USD is trading at 1.2334, up 0.34% on the day. The euro is currently at its highest level since December 2014. In Germany, Flash Manufacturing PMI slowed to 61.2, shy of the estimate of 63.2 points. There was better news from Flash Services PMI, which accelerated to 57.0. above the forecast of 55.6 points. The trend was similar in the eurozone, as Flash Manufacturing PMI dipped to 59.6, missing the estimate of 60.4 points. Flash Services PMI improved to 57.6, missing the forecast of 56.5 points. In the US, today's key event is Existing Home Sales, which is expected to dip to 5.72 million. On Thursday, Germany releases Ifo Business Climate, and the ECB will issue a monetary policy statement. The US will release unemployment claims.

What can we expect from the first ECB policy meeting on Thursday? We're unlikely to see any dramatics at the first policy meeting of 2018, as the ECB is likely to retain its pledge to continue buying bonds under its asset-purchase program (QE). The ECB has trimmed QE from EUR 60 billion to 3o billion/mth, but is likely to maintain interest rates for 3-6 months after that. Still, ECB policymakers have hinted that the Bank could wind up QE in September, and this has pushed the euro higher in recent weeks. ECB President Mario Draghi will speak after the statement, and if he hints that QE will not be extended, the euro could gain ground. However, Draghi may prefer to keep a low profile until March, when policymakers will have had a chance to review updated economic forecasts.

The US government shutdown turned out to be little more than a nuisance, as the shutdown affected only one working day. On Monday, the Senate voted 266-150 to extend government funding until February 8. This stopgap measure will enable the government to provide services during that time, but the lawmakers will need to hammer out a longer-term agreement, as these short extensions are just band aid solutions. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration.

XAUUSD Analysis: Reaches Four-Month High

Bulls dominated the market on Tuesday, thus allowing the yellow metal to appreciate by 0.57%. The pair showed low volatility during this time, except for some hourly jumps in both directions. From technical point of view, this surge resulted from the strong support of the 55-, 100– and 200-hour SMAs and the weekly PP circa 1,333.80, as bulls saw an opportunity to collect some gains. By early Wednesday, Gold had reached the weekly R1 and the four-month high at 1,344.00. In addition, the upper boundary of the prevailing short-term pattern is also located nearby. Even though technical indicators still show some upside potential, it is likely that the market introduces a slight correction southwards down to the aforementioned support. This area is expected to hold firmly.

USDJPY Analysis: Could Bounce Off From 109.80

The strong downside momentum that prevailed in the market on Tuesday breached any previous assumptions of a limited fall. The pair plunged 62 pips during the day and continued to move in the same direction early today, as well. The Greenback dashed through various support levels, but was stopped by the bottom boundary of a four-month descending channel near 109.80. This fall has sent technical indicators in the strongly bearish territory. This would suggest a possible period of appreciation up to the 110.50 area, especially if the US Dollar manages to surpass 110.30. However, such falls are occasionally followed by another plunge. In case this scenario occurs, the downside potential should not exceed the 109.50 mark where the weekly S2 is located.

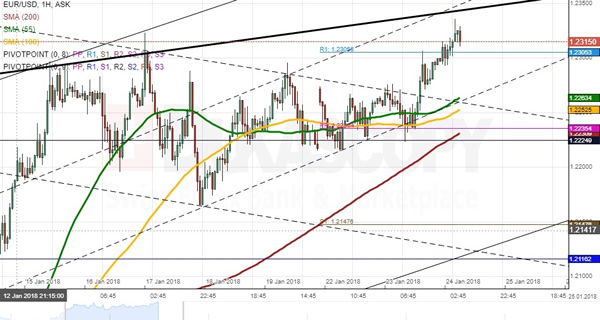

EURUSD Analysis: Tests Weekly R1

EUR/USD was trading in bullish market on Tuesday. Following a slight period of decline early in the session, the common European currency reversed from the combined support of the 55– and 100-hour SMAs and the weekly circa 1.2235 and surged 90 pips within the following hours. As a result, the pair had reached the 1.2315 mark at the time of this analysis. The aforementioned support area restricted the pair from initiating a new wave down; thus, the descending channel which was formed on January 14 was breached to the upside. It is still likely that the pair edges higher for several hours until the upper boundaries of both the senior and junior channels is reached circa 1.2360. The Euro should subsequently make a correction south towards 1.2250

GBPUSD Analysis: Breaches Psychological Level Of 1.40

The Pound remained relatively stable against the US Dollar yesterday. The pair edged lower during the first part of the day; however, the strong support of the bottom channel line and the 55-hour SMA circa 1.3930 stopped any attempts to edge lower. Subsequently, bulls took the upper hand and sent the Pound for a test of the most junior channel near 1.4035. Meanwhile, converging technical indicators suggest that the bullish sentiment might be exhausted, thus allowing for a correction south within the following trading hours. This scenario would return the rate back in the senior channel towards the weekly R1 and the 55– and 100-hour SMAs near 1.9350. In case the weekly R2 is breached, this high level is not expected to hold for long, as the Sterling should eventually be forced lower.

EUR/CHF 4H Chart: Kings Crown

The common European currency continues to surge against major currencies and the Swiss franc is no exception. The pair has continued the bullish movement since the last time Dukascopy research team reviewed the currency pair.

During the surge, the pair has reached a new high and has broken the previously mapped channel. Moreover, in the EUR/CHF chart, you can be observe a kings crown pattern.

Meanwhile, in regards to the future movement, the pair is likely to breach the dashed line, which is the support of the daily dominant channel. If and when this happens, it might find support at the weekly PP, combined with the 200 – hour SMA level 1.171.

USD/TRY 4H Chart: Fully Reviewed

USD/TRY appears to be walking its way towards the recent low level of 3.7290, as it extends the series of lower highs and lows since the pair was last reviewed.

The pair had a few weeks of consolidation to the north. However, it was stopped by the dominant downwards channel's trend line and the combination of the weekly and monthly PPs near 3.8465 mark.

Furthermore, in regards to the future movement, the pair might continue trading downwards and is likely to breach the low level 3.7290. If and when this happens, it might find support at the monthly pivot point of 3.656, combined with the 200 – hour simple moving average.

EUR/USD: German ZEW Economic Sentiment

The Euro strengthened against the US Dollar, reflecting the unexpectedly upbeat ZEW sentiment report. The EUR/USD exchange rate added 12 base points to get back into the 1.2250 area.

Germany's investors showed the strongest confidence in eight months, representing an optimistic tone for the economy entering 2018. The Mannheim-based ZEW Institute report revealed on Tuesday that the German Economic Sentiment Index rose to 20.4 points in January, following 17.4 in the last month of 2017. The country's economy grew at the strongest pace since 2011 last year, supported by solid global trade and domestic spending. The Bundesbank stated that the momentum is set to continue, driven mainly by private consumption.