Sample Category Title

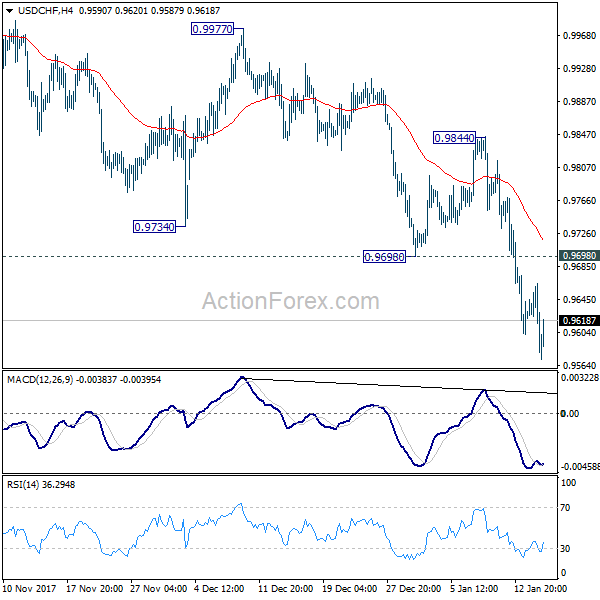

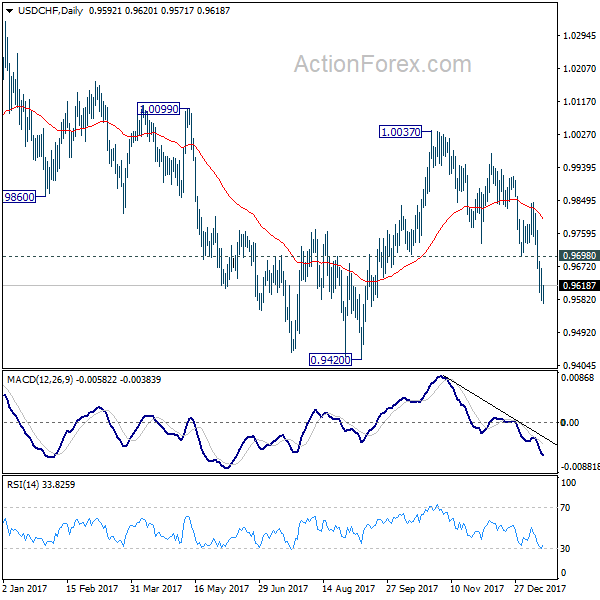

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9562; (P) 0.9613; (R1) 0.9647; More....

USD/CHF dipped to 0.9571 but quickly recovered. Intraday bias remains neutral at this point. As long as 0.9698 support turned resistance holds, deeper fall could be seen to 0.9420 low. Nonetheless, break of 0.9698 will indicate short term bottoming. Intraday bias would then be turned back to the upside for 0.9844 key near term resistance next.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

GBP/JPY: British Pound Bullish Above 151.50 Vs Japanese Yen

Key Highlights

- The British Pound traded higher from the 150.00-150.20 support area against the Japanese Yen.

- A bearish trend line with current resistance at 152.80 on the 4-hours chart of GBP/JPY is protecting gains.

- The pair must hold the 151.95 and 151.50 support levels to remain in the bullish zone.

- UK’s Consumer Price Index in Dec 2017 posted 3.0% (YoY), similar to the forecast.

GBPJPY Technical Analysis

The British Pound started a fresh upside wave from the 150.19 low against the Japanese Yen. The GBP/JPY pair is currently above a major support area at 151.50.

Considering the 4-hours chart of GBP/JPY, there is a positive price action forming above the 151.50 pivot level. The pair recently traded as high as 153.09 where it found a bearish trend line with current resistance at 152.80.

It moved down and broke the 23.6% Fib retracement level of the last wave from the 150.19 low to 153.09 high. However, there are many supports on the downside such as 151.95 and 151.50.

The 151.95 support is around the 100 simple moving average (red, 4-hour) and the 38.2% Fib retracement level of the last wave from the 150.19 low to 153.09 high.

The 151.50 support is a pivot zone and coincides with the 200 simple moving average (green, 4-hour). An intermediate support is the 50% Fib retracement level of the last wave from the 150.19 low to 153.09 high at 151.64.

Therefore, there is a cluster of supports between 151.50 and 151.95. As long as the pair is above 151.50, it remains supported for an upside push.

Recently, the UK saw the release of the Consumer Price Index for Dec 2017 by the National Statistics. The forecast was slated for a rise of 3.0% compared with the same month a year ago. The actual was similar to the forecast, but down from the last 3.1%.

In terms of the monthly change, the UK CPI was 0.4%, up from the last 0.3%. The result had a negative impact on the GBP/USD and GBP/JPY pairs, but both pairs are still in the bullish zone.

A break above the 152.80 and 153.00 resistance levels in GBP/JPY is required for buyers to gain upside momentum in the near term.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.14; (P) 110.56; (R1) 110.88; More...

USD/JPY dipped to 110.18 but quickly recovered ahead of 61.8% retracement of 107.31 to 114.73 at 110.14. Intraday bias stays neutral first. At this point, further decline cannot be ruled out. But we'd look for bottoming again below 110.14 fibonacci level. Meanwhile, on the upside, break of 111.26 support turned resistance will suggest that USD/JPY has bottomed slightly earlier than expected. In that case, intraday bias will be turned back to the upside for 113.38 resistance. Decisive break there will confirm completion of the corrective pull back from 114.73 and turn outlook bullish.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Dollar Maybe Ready for Rebound, Loonie Range-Bound ahead of BoC

While the forex markets remained generally steady, stock traders experienced a roller coaster ride overnight. DOW surged in initial trading to as high as 26086.12 (up 283 pts) but reversed gain and closed down -0.04% at 25792.86. That's the biggest single day reversal since February 2016. Similarly, S&P 500 surged to 2807.54 but closed down -0.35%. 10 year yield was relatively steady, closed down just -0.008 at 2.544. TNX is still struggling to have the momentum to get through 2.621 key resistance. A factor is the concerns over government shutdown in the US. The Congress will need to pass a spending bill by the end of this week to avoid the shutdown and it's seen as a risk by many traders

Dollar may be ready for a near term rebound

In the currency markets, Dollar remains in red against all major currencies for the week. Canadian Dollar follows as the second weakest one as traders are cautious ahead of BoC rate decision. Aussie and Swiss Franc are so far the strongest ones for the week. A key technical development to note is that the latest selling leg in Dollar looks rather weak. That is, EUR/USD jumped through 1.2296 temporary top, to just 1.2322 and is now back at 1.2265. USD/JPY dipped through 110.32, to 110.18 but is now back at 110.57. There are two key levels that Dollar pairs in in proximity to. The levels are 1.3835 resistance in GBP/USD and 110.14 fibonacci level in USD/JPY. The greenback could be ready for a near term rebound.

Canadian Dollar in range, traders cautious on BoC hawkish hold

Bank of Canada rate decision is the main focus today. After strings of strong economic data, BoC is generally expected to hike interest rate by 25bps to 1.25%. That will be the third hikes of the current tightening cycle. Canadian Dollar stays in range trading (started since January 5) as traders are awaiting the rate decision. The loonie struggled to follow others to extend gain against the greenback since last week, even though WTI crude oil extended up trend to just inch below 65 handle. An explanation is that some traders are cautious on the chance of a "hawkish hold" by BoC today. That is, while BoC also expects itself to raise interest rate in Q1, it wait until March to do so. In that case, we'd probably see more range trading in USD/CAD above 1.2354. Nonetheless, we're still a high chance of powering through 1.2354 support should BoC delivers the rate hike.

Elsewhere

Australia Westpac consumer confidence rose 1.8% in January, home loans rose 2.1% mom in November. Japan machine orders rose 5.7% mom in November. Eurozone CPI final is the main feature in European session. US will release industrial production, NAHB housing index and Fed's Beige Book economic report later today.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.14; (P) 110.56; (R1) 110.88; More...

USD/JPY dipped to 110.18 but quickly recovered ahead of 61.8% retracement of 107.31 to 114.73 at 110.14. Intraday bias stays neutral first. At this point, further decline cannot be ruled out. But we'd look for bottoming again below 110.14 fibonacci level. Meanwhile, on the upside, break of 111.26 support turned resistance will suggest that USD/JPY has bottomed slightly earlier than expected. In that case, intraday bias will be turned back to the upside for 113.38 resistance. Decisive break there will confirm completion of the corrective pull back from 114.73 and turn outlook bullish.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Jan | 1.80% | 3.60% | ||

| 23:50 | JPY | Machine Orders M/M Nov | 5.70% | -1.20% | 5.00% | |

| 0:30 | AUD | Home Loans M/M Nov | 2.10% | 0.00% | -0.60% | |

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | 1.40% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI M/M Dec | 0.40% | 0.10% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | 0.90% | 0.90% | ||

| 14:15 | USD | Industrial Production M/M Dec | 0.40% | 0.20% | ||

| 14:15 | USD | Capacity Utilization Dec | 77.30% | 77.10% | ||

| 15:00 | CAD | BoC Rate Decision | 1.25% | 1.00% | ||

| 15:00 | USD | NAHB Housing Market Index Jan | 72 | 74 | ||

| 19:00 | USD | Federal Reserve Beige Book | ||||

| 21:00 | USD | Net Long-term TIC Flows Nov | 23.2B |

Market Morning Briefing: The Aussie Has Seen A High Of 0.7999 Today

STOCKS

Dow (25792.86, +0.04%) dipped slightly from 26100 levels but while above 25500, the index looks bullish for the medium term. Note resistance visible near 26100 on the daily charts.

Dax (13246.33, +0.35%) has scope of testing 13400 on the upside and could come off from there in the near term. View is sideways for the coming sessions and bearish for the medium term.

Nikkei (23848.71, -0.43%) is trading below immediate weekly resistance and while that holds, a corrective dip is likely in the near term. A break above 24000, if seen could take it higher towards 24200/300 levels before coming off from there. /for the coming sessions we do not prefer a break above 24000.

Shanghai (3460.22, +0.69%) moved up breaking above immediate resistance near 3450. The index looks bullish for the coming sessions and may target 3500 soon.

Nifty (10700.45, -0.38%) and Sensex (34771.05, -0.21%) is likely to see a dip in the next few sessions of the week. Upside is likely to be limited to 10800 on Nifty and 35000 on Sensex.

COMMODITIES

Brent (69.17) and WTI (63.74) have come off as expected and could now continue to dip for a few sessions before trying to re-attempt higher levels. A test of 68 and 61 respectively is on the cards for the coming sessions.

Gold (1338.81) has paused near current levels and may come off to test 1330 in the near term before resuming its rise back to 1340-1350 levels.

Copper (3.2135) rose to almost test 3.30 on the upside before falling off sharply to close at lower levels. News states of a fading demand in China ahead of the Lunar Year. While the price trades below 3.35, the index looks bearish towards 3.15 in the longer run.

FOREX

Euro (1.2282) did see some consolidation yesterday, reaching a low of 1.2216, but is again trading just below its previous high of 1.2297. We could see a break past 1.23 soon for the next upside target of 1.24-1.25 to be tested in time for the ECB meeting next week (Thursday). Note that there is crucial resistance around 1.25 on the weekly line charts, which should ultimately hold in the near term.

Euro-Yen (135.77) is consolidating below 136 for the time being, but we might see a move past 136 as Euro moves past 1.23. There is resistance on daily candles near 137 which might be tested if Euro tests 1.24-1.25.

Dollar-Yen (110.66) tested support on the 3 day and weekly candles around 110.30 yesterday and may now gradually move up towards 112 by the end of this week. Upside may be restricted by crucial resistance near 112.5 on the weekly line charts.

Our expectation of a dip from Resistance near 1.3820-50 on the Daily candles for Pound (1.3794), seems to be holding on well for now. It might dip further towards 1.37, but the downside in the near term could be restricted to 1.36 (support on daily candles).

The Aussie (0.7969) has seen a high of 0.7999 today and is trading near 0.7970 currently, which might be reflective of some profit taking underway. This is an important resistance (as seen on weekly line chart) and could hold for the time being.

Dollar-Rupee (64.0375) saw a fast uprise yesterday and could now come off towards 63.90/85 on the downside in the coming sessions with an initial test of upside resistance near 64.20/25. It would be important to keep an eye on USD-CNY (6.4290) which is trading above the crucial 61.8% retracement level (6.3934, on the monthly chart) of the rise from Jan’14 to Dec’16 and this could be a crucial reversal level for the long term. A reversal on USD-CNY could signal long term bullishness for Dollar-Rupee.

INTEREST RATES

There is further yield curve flattening underway for US Yields as US 5 Yr (2.3602%) & 2 Yr (2.0224%) are seeing a continuing uprise while the 10Yr (2.5462%) & 30 Yr (2.8349%) continue to consolidate.

The US 10 Yr- 5 Yr spread (0.186%) now seems to be breaking support near 0.19-0.20% on the short term chart while the 30-10 Yr Spread (0.2887%) is moving towards previous lows near 0.25 on the long term chart.

Japanese 10 Yr Yield (0.085%) is continuing its ranging between 0.07% and 0.088% as expected. There is resistance near 0.17-0.18% for Japanese 10 Yr - 5 Yr spread (currently near 0.17%) and for Japanese 5 Yr (-0.085%) near current levels on the medium term chart. This suggests greater likelihood for the 10 Yr to trade near 0.07-0.075% for the next few sessions.

Crypto Shakeout, USD Wilt Continues, BOC Next

Tuesday was a brutal day for cryptocurrencies with falls from 20-40% before a late bounce but in FX the bounce for the dollar was fleeting as it sank late. The Swiss franc was the best performer Tuesday while the New Zealand dollar lagged. The BOC decision is coming later. There are 4 existing Premium trades in progress, all of which are in the green. Here is a tweet from Ashraf on Dec 12, 6 day before Bitcoin's peak.

Bitcoin fell 20% on Tuesday as the US returned from a holiday and talk of a regulator crackdown continued. Ripple fell 40% as well.

One story was the collapse of the cryptoscam from Bitconnect and that may have played into the larger jitters. Impressively, the dip buyers stepped in on a few fronts and Bitcoin rebounded from $10,200 to $11,500 while Ripple rebounded to $1.20 from $0.87.

In FX, the US dollar finally staged a rebound and EUR/USD briefly fell below 1.2200 but it couldn't even sustain itself for the day as EUR/USD rebounded to 1.2270 and USD/JPY made fresh lows, in part due to the first negative day of the year in stocks.

Taking a step back, it's clear that the animal spirits have been unleashed throughout markets. Some tipping point has been reached and the crisis-era wounds have finally been healed. That is changing the way markets behave and adapting with it will be a major theme this year.

In the global economy, the big question right now is how deeply central bankers believe that we've turned a corner. One big clue will come Wednesday in the Bank of Canada decision. Here is Ashraf's piece on the BoC. It's unlikely that Poloz badly wants to hike but he painted himself into a corner but committing to data dependence and saying that 'caution' doesn't mean they won't hike. He's also limited in his statement communication by the same misstep.

However, he may also increasingly believe that an acceleration in growth and inflation is right around the corner. In that case, a hike with a hawkish stance is appropriate and USD/CAD will be on its way to 1.20.

Never A Free Lunch In FX Markets These Days

Never a Free Lunch in FX market these days

Forex Overview

Trading currency markets can be cruel and unusual punishment and unforgiving at times. Which was typified by EURUSD moves overnight as two critical headlines sunk the EUR, causing some well thought out longs to get stopped out only to have the EUR consensus trade re-established later in the day?

The pair initially dipped on headlines that the Berlin regional branch of the SPD has supposedly rejected coalition talks with the Merkel bloc. However, given it represents 4% of the Bundestag the headline was quickly pushed aside, and the bulls were happy to buy dips. But in typical ECB fashion, the central bank rolled out the unmanned sources to the press dousing the party with ice water by suggesting the market is getting ahead of itself.

But later in the NY session reality set in that the coalescence of technicals and fundamentals continue to suggest a structural shift to sell USD is on the cards triggering market players to re-engage dollar shorts.

Expectations are increasing that other G-10, and Asian central banks are readying to enter a path of interest rate normalisation, with the ECB and BoJ joining the Fed spearheading the shifting Central Bank narrative for 2018. And the surging global growth narrative is providing the favourable scrim.

The Euro will remain the markets darling in this scenario as an undisguised explanation suggests that with the low level of EU bond yields relative to the US yields that when the ECB definitively embarks on policy normalisation the Euro could surge much higher. Considering a 50 basis point rise in EU yields could trigger a modest 2-3 % rally in EURUSD, but the thought of a 100 basis point jump and a 5-6 % bounce on the EURUSD, the top side risk appears oh so attractive.

Oil Market Overview

Occasionally the technical picture, suggesting we’re topping out on prices, can distort the fundamental premise that after years of oversupply the inventories are contracting much faster than the markets had anticipated as the surging global growth narrative ferments. And while US drillers may come back online more aggressively, but price response could dawdle, and WTI and Brent could move higher near-term regardless.

Of course, there’s some thought that Russia is willing to end the OPEC relationship, but until there is a simple quantifiable methodology to what constitutes global oil market balancing act, it far too early in the game to go down that road. The fact is OPEC nor its comrades in arms can incur another significant price slump suggesting a messy exit strategy is long ways off.

Overnight it was a mix of profit-taking, background discussions around Russia parting way with OPEC and Shale Producers ramping up production that has weighed on sentiment.

US Equities Market Overview

Equities were bid on the opening bell, but the 10 am NY option expiry coincided with the high water mark in US equities as the Dow Jones Industrial topped the 26,000 mark for the first time. But from there onwards, it was all downhill into the close. ( Just for the record, when it comes to option expiry referrals, I don’t believe in coincidences)

Energy sectors indeed weighed on stocks as the technical picture on oil prices suggests the long anticipated correction is in store. But with the Vix bid +12. % during the session, and while it still has a long way to go before it becomes significant, perhaps the uptick in vols convinced investors to book some profits and reduce some risk.

Not to mention the omnipresent political quagmire in Washington adding a level of angst after headlines suggesting Steve Bannon, Trump’s former right-hand man, will be subpoenaed to testify as part of the ongoing Russia gate investigation

Gold Market Overview

Gold Trader finally came up for air overnight after prices printed a four-month high this week. While the US dollar remains the most prominent driver of momentum, we can not overlook the meltdown in Bitcoin on the back of regulatory oversight adding to the Gold risk premium. Indeed, many retail traders suffered in the collapse, and at this stage, the actual economic impact is unquantifiable. And while it’s not as convincing an argument as a weaker dollar is for higher gold prices, at a minimum, it provides support from a cognitive perspective.

G10

The Euro

Indeed the market did not buy into the overnight headlines remained in buy the dip mode. Despite all the headline noise, the EURUSD held 1.22 as traders remained unwavering on their bullish Euro calls.

The Japanese Yen

The background conversation around the BoJ policy shift continues to resonate. With top side risk relatively limited in this cooler USD environment; traders become more attracted to risky trades than playing established ranges. Given that an appreciable break of 110 could drive a wave of impulse selling for well-established longs coupled with panic selling from exporters, the potential for 107 is not out of the question before the BoJ has time to react.

The Australian Dollar

Base metals have underperformed, and oil has pulled back from the highs, so not shocking that commodity currencies are settling while the USD sell-off abated. But Aussie traders remain focused on tomorrow’s Job report and China data dump.

Although Chinese Lunar New Year is over a month away, the market may start to reduce appetite for raw materials as virtually everything shuts down that week. So for the Aussie to take out the 80 level anytime soon, it will probably need a stellar jobs report coupled with an extension of the US dollar slump to get the market across the line.

The Chinese Yuan

The Yuan remains a major focal point, but the bottom line is the Pboc do not appear overly concerned with the strengthening Yuan as even in the face of substantial moves they’ve only marginally pegged the fix USD higher. Of course, the traditional thought that China needs a weaker Yuan to support exports does make sense, but as Mainland policy markets accelerate the internationalisation of the RMB complex, Beijing may merely be more focused on attracting inflow to support local capital markets while regulators continue the arduous process of deleveraging financial markets risk.

Asia FX

Lots of moving parts and idiosyncratic storylines in the region, but outside of the INR and PHP, short USD dollar positions remain favourable. INR trade poorly overnight after the RBI said that banks must manage their rate risks

The Malaysian Ringgit

With the markets focus shifting to Central Bank policy normalisation this should favour the MYR given the anticipated policy shift at the end of the month. But to get through the 6.95 level before the BNM rate hike, it will require either an extension of the Euro rally to break through 1.23 or USDJPY to fall convincingly below 111.00 as both currency pairs are steering FX markets right now.

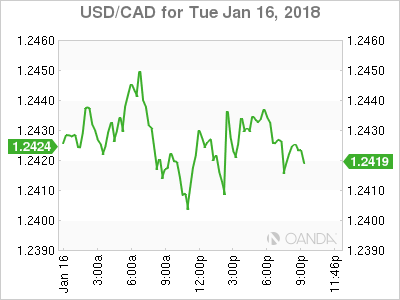

Canadian Dollar Awaits Central Bank Anticipated Rate Hike

The BoC will become the first G7 nation to raise rates in 2018

The USD/CAD has been almost flat this week awaiting the rate decision by the Bank of Canada (BoC). The central bank is expected to raise the benchmark rate to 1.25 percent in what could be the first of three rate hikes in 2018. The BoC governor will host a press conference at 11:15 am to give more details behind the monetary policy decision. Unlike the July rate hike in 2017 Canadian policy makers have not telegraphed the decision, but markets have priced in a 86 percent probability. While Poloz has surprised in the past, he has avoided outright wrong footing the market.

- Strong Canadian employment is driving the central bank to lift rates

- Majority of analysts expect a 25 basis points hike by the BoC

- Inflation is near the 2 percent target

The USD/CAD is flat at a 0.02 percent loss on Tuesday. The currency is trading at 1.2425 ahead of the Bank of Canada (BoC) rate statement on Wednesday, January 17 at 10 am EST. The loonie was stuck in a tight range and is trading near where it opened this morning.

The Bank of Canada (BoC) is worried that lifting rates too fast could hurt Canadian households with record levels of debt as well as taking out one of the main engines of growth of the economy, the housing sector. Also under consideration is the uncertain fate of NAFTA. The treaty has been under assault from President Trump ever since he was a candidate and he has followed through on his America First mandate which has hampered the renegotiation talks that have progressed with little to show. The next round will take place in Montreal on January 28.

The Canadian economy had a great year in 2017, defying expectations of growth and employment. There were signs of a slowdown toward the second half, but the December jobs report on the back of a solid November employment data started on a positive note for the loonie. The Canadian currency is up 1.2 percent against the USD year to date. The US dollar has not been able to gain momentum after the passing of tax reform and December rate hike were already priced in and left investors with few clues going into 2018.

A rate hike will benefit the CAD, but how much is hard to tell. Under normal circumstances the rate announcement would mean closing the gap between US rates and with better fundamentals the CAD should appreciated, but given the situation of the NAFTA negotiations it could have less of an impact. The talks in Montreal are been considered as a make or break meeting. There has been little to show on most fronts and with upcoming elections in Mexico and the United States it could be heavily politicized ending up in its demise. The loonie is not anticipated to rise as sharply if the BoC follows through with a rate hike given the NAFTA uncertainty with ongoing negotiations.

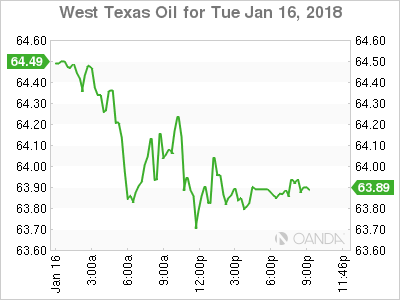

Energy prices dropped in the last 24 hours. The West Texas Intermediate is trading at $63.87 after traders booked profits after a sustained rally. The price of oil went at high as $64.80 near Monday’s close before falling to current levels. Stronger than expected demand has kept price close to $70. The battle between the Organization of the Petroleum Exporting Countries (OPEC) who agreed to cut production with other major producers and US shale producers drags on with the cut in supply receiving a boost by weather disruptions. US shale has not hiked production as fast as originally thought, specially considering rising prices. OPEC members and major producers have kept their production in check with the added bonus that any supply hiccups will help their cause.

Russian compliance was a concern going into the OPEC cut agreement extension but the comments from Energy Minister Alexander Novak was very supportive of the cuts and the need to keep them for longer until the oil market is balanced. The main difference between this rally and others in the past two years is that it not fuelled mainly by statements from producers, but instead has the backing of strong fundamentals. Energy imports have increased 1.8 percent in India and other developed countries have increased their appetite for the black stuff.

Threats remain with some analysts not convinced that the current conditions are sustainable. The OPEC are dealing with a potential breakdown if Saudi Arabia, Iran and Iraq continue their ideological disagreements. Disruptions are short lived and rising US, Brazil and Canada production could soon offset the wins of the oil supply cut agreement as they move in to benefit from higher prices.

Market events to watch this week:

Wednesday, January 17

10:00am CAD BOC Monetary Policy Report

10:00am CAD BOC Rate Statement

10:00am CAD Overnight Rate

11:15am CAD BOC Press Conference

7:30pm AUD Employment Change

Thursday, January 18

2:00am CNY GDP q/y

2:00am CNY Industrial Production y/y

8:30am USD Building Permits

8:30am USD Unemployment Claims

11:00am USD Crude Oil Inventories

Friday, January 19

4:30am GBP Retail Sales m/m

Gold Slips As Dollar Stems Broad Losses

Gold has reversed directions and posted losses in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1333.83, down 0.52% on the day. It’s a light day on the release front, with just one US indicator. The Empire State Manufacturing Index softened to 17.7, missing the forecast of 18.5 points. This marked the weakest reading since June.

Gold is trading in red territory on Tuesday, after posting four straight winning sessions. On Monday, the base metal climbed above $1344, for the first time since early September of 2016. The US dollar has lost ground against its major rivals, notably the euro. There are two main reasons for the euro’s recent rally. First, the ECB minutes from the December meeting were hawkish, leading to speculation that the ECB could wind up its asset purchase program in September. In the minutes, policymakers said that risks to the current outlook were to the upside, which could necessitate a gradual shift in guidance in the next few months. As for the eurozone, the minutes stated that the economy was displaying “continued robust and increasingly self-sustaining economic expansion”.

The second factor is major progress in coalition negotiations in Germany, raising hopes that the political stalemate may soon be over. There was a report on Friday that Angela Merkel’s conservative bloc and the Social Democrats have agreed on a coalition draft. This ends months of political uncertainty, which has eroded Merkel’s standing and also sidelined Germany on key issues such as Brexit and political reform in the eurozone. Still, the talks are only in the preliminary stage, and further negotiations will take at least several weeks before it is clear that the talks have been successful.

Gold often gains ground when investor risk appetite is weak, but that has not been the case early in 2018. Global stock markets are pointing higher and US economic numbers have been strong. This points to the broadly weaker dollar as the catalyst for stronger gold prices. If major currencies such as the euro and Japanese yen continue to make inroads against the dollar, traders can expect the gold rally to continue.

Pound Rally Pauses As UK Inflation Dips

The British pound has posted small losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3773, down 0.15% on the day. In economic news, British CPI edged down to 3.0%, matching the forecast. In the US, there were no key events on the schedule. The Empire State Manufacturing Index softened to 17.7, missing the forecast of 18.5 points. This marked the weakest reading since June 2017.

Inflation in the UK dipped to 3.0% in December, but that is still much higher than the Bank of England target of 2 percent. The BoE is reluctant to raise interest rates, especially with the uncertainties over Brexit, but high inflation continues to erode the purchasing power of the British consumer. A weak pound has further dampened consumer spending, although a cheaper pound has been a boon for the export sector. The BoE holds its next policy meeting in February, and as matters currently stand, the BoE is not expected to raise rates.

Brexit negotiations have been difficult and progress has been slow, as Europe is not keen on rewarding Britain for departing the European Union. There are serious divisions within the British government with regard to the talks, and Prime Minister May has to walk carefully, as she has a razor thin majority in parliament. May can ill afford any mistakes, and if her government runs into trouble, she may be forced to call elections, which could shake up the markets and send the pound downwards. The public is almost evenly split on whether Brexit is a good idea, and there are serious concerns that the British economy will take a hit, even if a deal is worked out before the March, 2019 deadline. The parties do not have a lot of time to hammer out a host of trade issues, and all indications are that the negotiations road will be bumpy and difficult. One card that Britain may hold is that the EU, which has been united so far in its position on Brexit, may see the unified front fall apart find that some countries try to cut favorable trade deals with Britain.