Sample Category Title

EUR/USD: German Final Consumer Price Index

The European single currency fell sharply against the US Dollar, following German inflation final report on Tuesday. The EUR/USD currency pair depreciated 40 base points or 0.33% to the 1.2228 mark.

German consumer price inflation growth accelerated to the strongest level in five years, final report showed on Tuesday. Destatis stated that the country’s CPI increased 1.8% on a yearly average in 2017, compared with the prior year’s 0.5%. Meanwhile, a yearly increase in the inflation rate was confirmed at 1.7% in December, supported by higher energy prices. Despite a monthly 0.3% drop in wholesale prices, the report showed their 1.8% rise year-over-year in December, while the average WPI index was 3.5% higher, compared with a 2016 average.

GBP/USD: UK Consumer Price Index

The Sterling weakened against the US Dollar on the row of mixed economic data releases for Britain on Tuesday. The GBP/USD currency pair lost 22 base points or 0.16% to fall slightly ahead of entering the resistance zone near the 1.3825 level.

The UK inflation eased slightly from its post-Brexit record high in December, official report revealed, indicating that the financial squeeze on households is likely to weaken. Britain’s consumer price inflation declined to a yearly rate of 3.0% in December from almost six-year high registered in the previous month. The BoE anticipated inflation to fall gradually over the next two to three years to the 2% target, while many economists revealed expectations for a faster decline in a year.

EUR/USD Nevertheless Managed To See A Brief Visit Above The 1.23 Mark

Market movers today

In the euro area, we are due to get the final December HICP inflation figures. We do not expect any revisions but instead will look for which items have weighed on service price inflation, as this HICP component will be key for core inflation to pick up. Overall, we expect core inflation to average only 1.1% in 2018, in line with the ECB's new forecasts.

In the US, industrial production for December is released. The current trend in industrial production is decent and based on ISM Manufacturing there is room for an uptick in growth of industrial production.

A few central bank speakers including the ECB's Ewald Nowotny, the Fed's Charles Evans (non-voter, dovish) and Loretta Mester (voter, hawkish) are due to speak today.

Speech from the Riksbank's Ohlsson this afternoon ; otherwise no Scandi events

Selected market news

Focus on the prospect of both the ECB and the Fed moving earlier on policy tightening than previously anticipated increasingly weighing on market sentiment. Equities ended the day in ‘red' in t he US and Asia like, and Brent crude oil dipped briefly below USD69/bbl. The US 2Y Treasury yield continued to creep higher and again settled above the 2% mark. Euro yields have moved little since the jump on ECB minutes last week, but EUR/USD nevertheless managed to see a brief visit above the 1.23 mark. Meanwhile, the US administration is mulling a short -term spending fix following the breakdown in talks with the democrats.

On Tuesday, an ECB sources Reuters story made a somewhat half -hearted attempt to talk down the market's hawkish take on last week's December meeting minutes, saying that the pledge to keep buying bonds would be kept at the January meeting, and that a possible change in guidance would rather be one for the March meeting. ECB communication has been somewhat muddy over the past few days, and the ECB's Jens Weidmann added further to the blurred picture of ECB intent ions by stating in a German newspaper interview yesterday that a first hike was more likely to happen in mid-2019 rather than around New Year 2018/19 as suggested by the latest market pricing. There are speeches from Ewald Nowotny today and Benoit Coeuré tomorrow, but we will probably have to wait for Mario Draghi at next week's ECB meeting to get a real clarification of stance.

Separately, yesterday we changed our call on the Fed and now expect Powell and co to deliver a next hike already at the March meeting (previously June). That said, we do not necessarily expect the Fed to change its communication at the upcoming meeting on 31 January, as this is one of the small meetings without updated project ions and a press conference; more important for communication during Q1 will be the individual speeches. Also, we now expect three hikes (previously two) with the second hike likely in June and the third one in December.

Market Update – Asian Session: Equities Track Lower On An Uninspiring US Session

Headlines/Economic Data

General Trend:

US dollar (USD) weakens broadly in early Asia, later pares losses

Aussie rises amid better than expected home loans data, Westpac Consumer Confidence hits 4-year high; later pares gain

Australia 10-year yield rises amid syndicate pricing

China continues to play down need for rate hike: PBoC Adviser said not necessary for China to raise benchmark interest rates in near term

China Q4 GDP and Australia monthly employment data due for release on Thursday

China sells 5-year bonds at lower than expected yield

(CN) PBOC reminds that RRR cut announced for some banks in Sept, to go into effect Jan 25th

Japan Nov Core Machine Orders has highest value since June 2008

BoJ again leaves bond purchases unchanged at daily operation

Bitcoin continues its weakness as Asia regulators continue to indicate they will crack down on cryptocurrency

Coinbase: Notes buys and sells are temporarily unavailable

Bithumb: Delayed cash withdrawals for some clients

Japan

Nikkei 225 opened -0.7%; closed -0.4%

TOPIX Iron & Steel Index -1.2%: Nippon Steel -1.5% (Fire reported at Nippon Steel's Naoetsu production facility - Japanese press)

General weakness in the Japanese mega banks: Sumitomo Mitsui -1%, Mizuho -1%, Mitsubishi UFJ -1% (tracks declines in S&P500 Financials sector)

Fast Retailing -1.3% (gained 2.8% prior session)

Softbank -1.2% (gained 2.0% prior session)

(JP) Japan Nov Core Machine Orders M/M: 5.7% v -1.4%e; Y/Y: +4.1% v -1.0%e

Toyota and Honda suspend exports to Vietnam since the beginning of the year following the implementation of a rule that requires stringent checks on imported vehicles - Nikkei

Looking Ahead: Japan Nov Industrial Production due for release on Thursday

Korea

Kospi opened -0.2%

Weakness in chip sector: Samsung Electronics -0.3%, Hynix -0.3%

Chemicals firms trade lower: LG Chemicals -2%, Lotte Chemical -2%

Celltrion [068270.KR]: -3.5% (cautious broker commentary)

Doosan Heavy [034020.KR] -4% (Doosan Group denied press report related to sale of Doosan Heavy)

Samsung SDS [0.18260.KR] +4.5% (positive broker commentary)

(KR) South Korea Deputy PM and Fin Min Kim: suggestion to close down cryptocurrency exchanges is still an option under consideration, despite anticipated side effects - Korean press

(KR) US Secretary of State Tillerson: North Korean intercontinental ballistic missile launch in November was witnessed by passengers on a San Francisco-to-Hong Kong commercial flight

(KR) Bank of Korea sells KRW2.43T in 2-year monetary stabilization bonds (MSB): yield 2.15%

(KR) South Korea Fin Min Kim: Will leave FX rates to market but take action if necessary

Looking Ahead: Bank of Korea interest rate decision due for Thursday (expected to leave rates unchanged at 1.50%)

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

China property names decline after report that China would continue with property curbs; Hang Seng Property/Construction Index -1.0%

Property company Country Garden [2007.HK] -4%: Planning to raise HK$23.4B by selling shares and convertible bonds

Hang Seng Materials Index -1.8% (+1.6% prior session), Energy -1.9% (+1.1% prior session)

HNA Group unit Bohai Capital halted ahead of ‘expected major issue’

General weakness among airlines: China State-owned Assets Supervision and Administration Commission (SASAC) said it will allow less than 50% state holding in top 3 state airlines

(CN) China researcher: No need for PBOC to hike interest rates – press

(CN) China PBoC OMO: Injects CNY200B in 7,14 and 63-day reverse repos v CNY320B prior: Net injects CNY100B v CNY270B drained prior

USD/CNY (CN) PBoC sets yuan reference rate at 6.4335 v 6.4372 prior (strongest fix since Dec 10, 2015)

(CN) China MoF sells 5-yr bonds: avg yield 3.81% v 3.84%e, bid to cover 3.39x

(HK) Hong Kong Chief Lam: Take ‘great exception’ to report compiled by British peer Paddy Ashdown that casts doubts on rule of law and China’s influence over city

Looking Ahead: China Q4 GDP and Dec data (Fixed Asset Investment, Industrial Production, Retail Sales) due for release on Thursday

Australia/New Zealand

ASX 200 opened -0.2%; closed -0.5%

ASX 200 Resources Index -1.4%,Telecom -1%, Financials -0.3%

(AU) Australia Jan Westpac Consumer Confidence Index: 105.1 v 103.3 prior; m/m: 1.8% v 3.6% prior (4-yr high)

(NZ) New Zealand Dec ANZ Commodity Price: -2.2% v -0.9% prior

(AU) Australia to sell A$9.6B in new 2029 bonds, priced at yield to maturity of 2.86%

(NZ) New Zealand mortgage brokers see uptick in interest after lending curbs lifted - NZ press

(AU) According to analysts the RBA cash rate is poised to fall below the Fed funds rate for the first time in over 15 years, will see a sharp fall in the the A$ as a result - AFR

(AU) AUSTRALIA NOV HOME LOANS M/M: 2.1% V 0.0%E; INVESTMENT LENDING: 1.5% V 1.8% PRIOR; Owner Occupied Loan Value m/m: 2.7% v -0.5% prior

Looking Ahead: Australia Dec Employment data due for release on Thursday

Other Asia

(IN) India Economic Affairs Sec Garg: Requirement of additional borrowing reduced to INR200B vs INR500B originally seen

(IN) India 10-year bond yield near 7.43%, down over 12bps

(SG) Singapore Dec Non-Oil Domestic Exports M/M: -5.0% v -4.4%e; Y/Y: +3.1% v 8.6%e; Electronic Exports Y/Y: -5.3% v 5.1% prior

(PH) Philippines Central Bank Gov Espenilla: Sees no Philippine Peso freefall given fundamentals

Nanya Technology [2408.TW] -4.7%: Sees Q1 DRAM prices rising 'mildly' - local press

North America

US equity markets reversed gains and ended mostly lower: Dow flat, S&P500 -0.4%, Nasdaq -0.5%, Russell 2000 -1.2%

S&P500 Energy Sector -1.3%, Materials -1.2%

(US) Pres Trump tweets: "The Democrats want to shut down the Government over Amnesty for all and Border Security."

(US) US House Republicans discuss stop-gap government funding bill through Feb 16th (in line with prior press speculation)

(US) Republican Representative Simpson: Stop-gap funding bill expected to include 6-year Childrens Health Insurance Program (CHIP) reauthorization; will not include 'Dreamer' immigration legislation

(US) Republicans said to discuss attaching 2-year delay of medical device and 'cadillac' health plan taxes related to Obamacare - financial press

(US) Former White House adviser Steve Bannon has reportedly been subpoenaed by Special Counsel Mueller in Russia investigation - NYT

Ford [F] -3% in afterhours: Reports prelim FY17 $1.78 v $1.81e, Guides initial FY18 adj EPS $1.45-1.70 v $1.53e; announces supplemental cash dividend ahead of DB conf

PayPal [PYPL] -2% in afterhours: Guides initial FY18 Rev $15.0-15.25B v $15.4Be; Affirms Op profit growth ~20%

Looking Ahead: US Dec Industrial Production and Nov TIC data due for release, along with Bank of Canada rate decision, Weekly API Crude Oil Inventories

Earnings expected from companies including ASML, Alcoa, Bank of America, Goldman Sachs

Europe

(EU) ECB Weidmann (Germany): would be appropriate to end ECB's asset purchases this year - press interview; Analyst expectation for a mid-2019 rate hike is about in line with ECB guidance

(FR) ECB's Villeroy (France): Must monitor Euro movements on prices; recent rise is a source of uncertainty - press interview

(EU) Eurogroup Chief Centeno: signals we're getting from Germany are very encouraging; it makes sense for a monetary union to have a budget capacity that plays a role of supporting investment

EUR/USD: During early Asia session, traded above highs seen in Dec 2014 amid broad US dollar weakness

Nestle: Confirms agreement to sell US confectionery business to Ferrero for $2.8B

Informa [INF.UK]: Boards of UBM and Informa confirm that they are in talks on potential combination of the two companies

Levels as of 01:00ET

Nikkei225 -0.4%, Hang Seng -0.3%; Shanghai Composite +0.5%; ASX200 -0.5%, Kospi -0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 +0.2%

EUR 1.2323-1.2238; JPY 110.91-110.19; AUD 0.7999-0.7948;NZD 0.7291-0.7237

Feb Gold -0.1% at $1,335/oz; Feb Crude Oil -0.1% at $63.64/brl; Mar Copper -0.6% at $3.20/lb

Elliott Wave View: SPX Remains Buy In Dips

SPX Short Term Elliott Wave view suggests that rally from 12/2/2017 low is unfolding as 5 waves impulsive Elliott Wave structure where Minute wave ((i)) ended at 2665.19, Minute wave ((ii)) ended at 2624.75, Minute wave ((iii)) ended at 2807.54, and Minute wave ((iv)) appears complete at 2768.64. Index still needs to break to a new high above Minute wave ((iii)) at 2807.54 to confirm this view. Until then, a double correction in Minute wave ((iv)) still can't be ruled out. Near term, while dips stay above 2768.64, and more importantly as far as pivot at 12/30/2017 low at 2674.73 stays intact, expect Index to find buyers in any dips in 3, 7, or 11 swing for further extension to the upside. We don't like selling the Index.

SPX 1 Hour Elliott Wave Chart

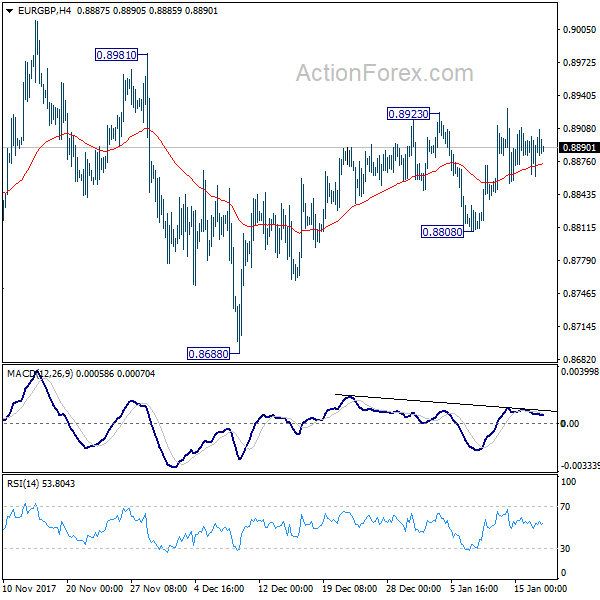

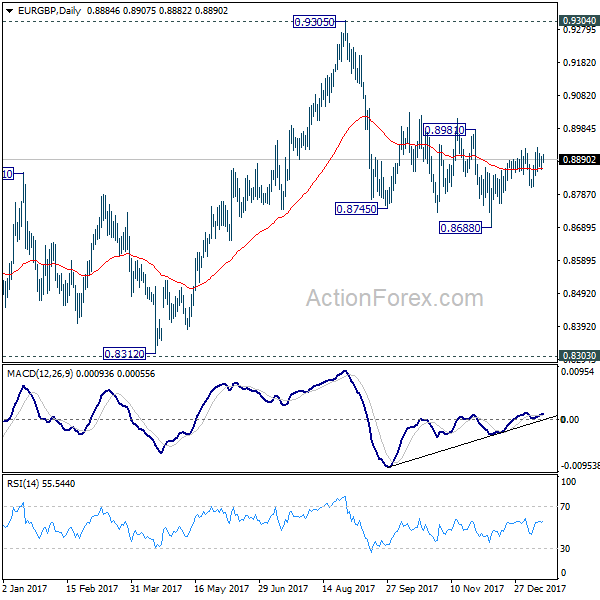

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8867; (P) 0.8884; (R1) 0.8906; More...

No change in EUR/GBP's outlook. Despite the rally attempt, upside momentum remains unconvincing. Break of 0.8981 resistance is needed to indicate completion of the decline from 0.9305. Otherwise, another fall would be mildly in favor. Below 0.8808 support will turn bias to the downside for 0.8688 support first.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

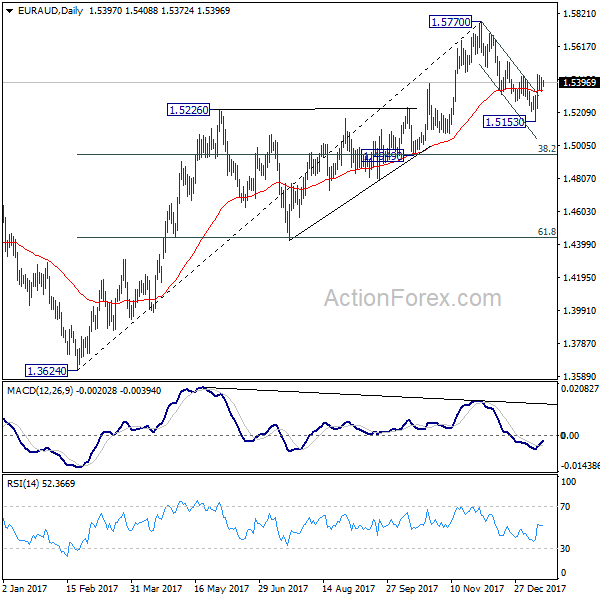

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5350; (P) 1.5387; (R1) 1.5434; More....

EUR/AUD lost some upside momentum as seen in 4 hour MACD. But we're still expecting further rally ahead. A short term bottom was formed at 1.5153 on bullish convergence condition in 4 hour MACD. Further rise would be seen back to retest 1.5770 high. On the downside, break of 1.5153 will resume the fall from 1.5770 to 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950).

In the bigger picture, decline from 1.5770 just breached 1.5226 key support briefly and recovered. The development is reviving the bullish case that rise from 1.3624 is still in progress. But considering bearish divergence condition in daily MACD, we'd prefer to see firm break of 1.5770 resistance to confirm. On the downside, sustained trading below 55 week EMA (now at 1.4950) will likely bring retest of 1.3624 support. Overall, there is still prospect of another medium term rally as long as 61.8% retracement of 1.1602 to 1.6587 at 1.3506 holds.

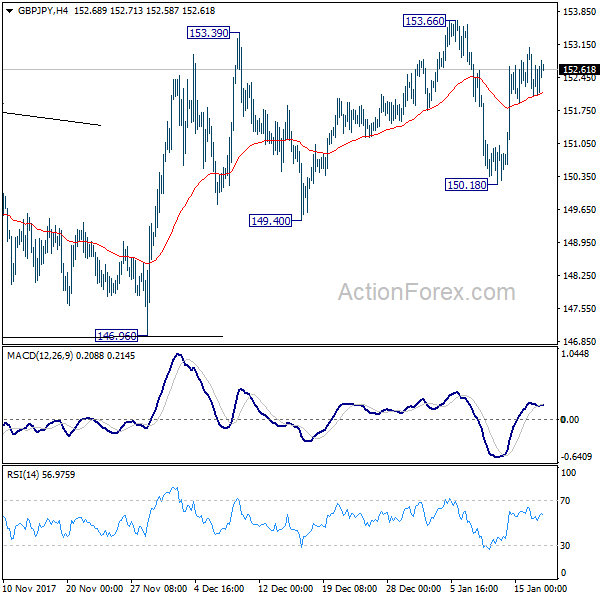

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.88; (P) 152.49; (R1) 152.93; More...

GBP/JPY continues to stay in range below 153.66 and intraday bias remains neutral. On the upside, break of 153.66 will resume medium term up trend. Meanwhile, break of 149.40 support will indicate trend reversal and turn focus to 149.96 for confirmation.

In the bigger picture, considering bearish divergence condition in daily MACD, the steep fall from 153.66 is now seen as first sign of trend reversal. Focus will turn to 146.96 support. Firm break there will at least confirm medium term topping and target 139.39 support next.

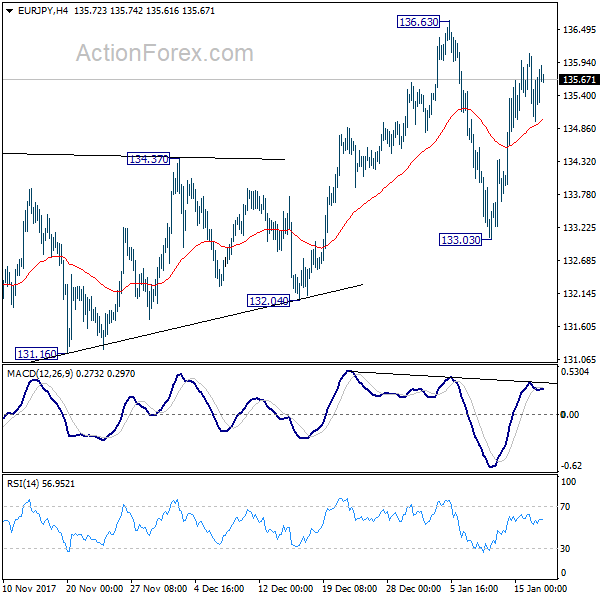

EUR/JPY Daily Outlook

Daily Pivots: (S1) 134.90; (P) 135.50; (R1) 136.02; More....

EUR/JPY is staying in range below 136.63 and intraday bias remains neutral. Outlook stays bullish with 133.03 support intact and further rally is in favor. Break of 136.63 will resume medium term up trend. However, below 133.03 will turn focus to 132.04. Firm break there will indicate medium term reversal.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

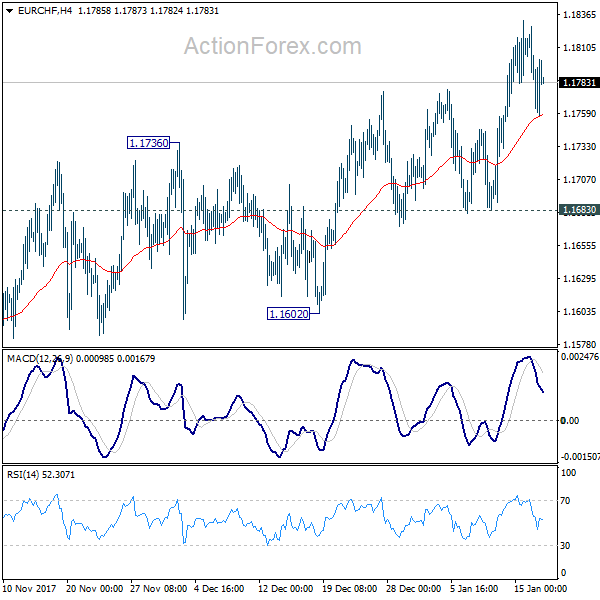

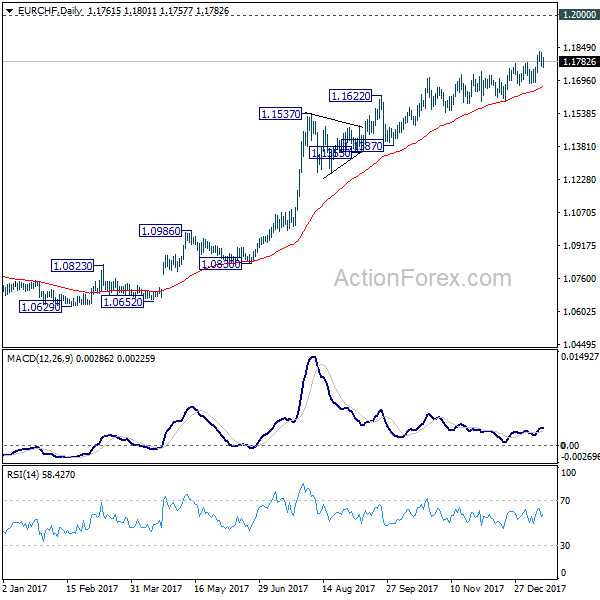

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1782; (P) 1.1807; (R1) 1.1832; More...

No change in EUR/CHF's outlook. Medium term rise is still in progress for 1.2 handle. At this point, considering relatively weak upside momentum as seen in daily MACD we'd still expect strong resistance below 1.2 handle to limit upside and bring medium term reversal. But break of 1.1683 support is needed to indicate short term topping first. Otherwise, outlook will remain mildly bullish in case of retreat.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.