Sample Category Title

Is The Market Too Aggressive On A BoC Slam-Dunk Rate Hike?

Wednesday January 17: Five things the markets are talking about

The Bank of Canada (BoC) is due to announce its interest rate decision at 10:00 am EDT and a full rate increase of +25 bps is almost priced in already.

But, has the market got too aggressive on a BoC 'slam dunk' rate hike? The stronger bets are on the BoC to hike by +25 bps and downplay the move by suggesting that future hikes are data dependent – 'dovish hike'.

There is no question that the Canadian economy in general has improved with retail sales, GDP growth, CPI and employment activity improving significantly over the last couple of months, nevertheless the BoC has more options than to raise interest rates immediately such as signaling plans to tighten in March – a 'hawkish' hold.

All week, FX traders who had all but priced in further tightening by governor Poloz have suddenly being paying up to hedge against the risk of a potential letdown. The cost to protect against significant loonie losses has been steadily climbing since reports that the U.S would/could withdraw from NAFTA if they did not get a better trade deal.

Note: NAFTA trade officials next meet in Montreal on January 23.

Monetary policy announcements are also this week due in South Korea, South Africa and Turkey.

1. Stocks pull back from record highs

In Japan, the Nikkei share average dropped overnight as mining, oil and shipping stocks lost ground, while bitcoin-related stocks tumbled after the cryptocurrency’s value extended its sharp decline on worries over tighter regulation. The Nikkei dropped -0.4%, while the broader Topix lost -0.2%.

Down-under, the Aussie ASX 200 was down -0.4% on broad based profit selling of mining stocks. In S. Korea, the Kospi rose +0.7%, its third consecutive day of gains.

In Hong Kong, the Hang Seng Index rose to a fresh closing high overnight, aided by continued strength in index heavyweight Hong Kong Exchanges and Clearing. At close of trade, the Hang Seng index was up +0.25%, while the Hang Seng China Enterprises index rose +0.64%.

In China, stocks end mixed as consumer, real estate firms take breather. The Shanghai Composite index was up +0.26%, while the blue-chip CSI300 index was down -0.23%.

In Europe, regional indices are trading mostly lower across the board following the yesterday’s pullback stateside.

Futures on the S&P 500 index have climbed +0.2%.

Indices: Stoxx600 -0.2% at 397.5, FTSE -0.3 at 7735, DAX -0.1% at 13230, CAC-40 -0.2% at 5501, IBEX-35 -0.5% at 10469, FTSE MIB -0.1% at 23485, SMI -0.2% at 9443, S&P 500 Futures +0.2%

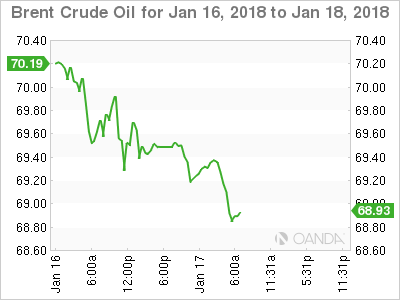

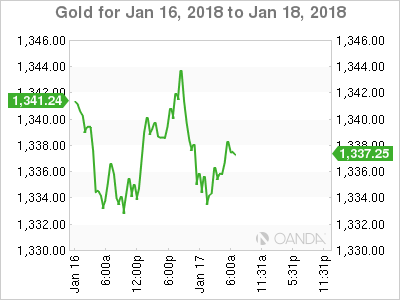

2. Oil loses early gains, but still well supported, gold lower

Oil prices weakened following early gains on Wednesday, but remained underpinned by tightening supply and strong global demand.

Tighter fundamentals have lifted both crude futures benchmarks about +13%since early December, helped by production curbs by OPEC and Russia, as well as by healthy demand growth.

Brent crude futures are at +$69.94 a barrel, down -21c from yesterday’s close, after hitting +$69.37. Brent on Monday rose to $70.37 a barrel, its’ highest since December 2014.

U.S. West Texas Intermediate (WTI) crude futures are at +$63.60 a barrel, down -13c. WTI hit +$64.89 yesterday, also the highest since December 2014.

Crude oil ‘bears’ are betting that the market may come under renewed pressure from rising U.S production. Yesterday, a report from the EIA indicated that it expected the country’s oil output to rise in February, with production from shale rising by +111k bpd to +6.55m bpd.

Note: U.S crude output is expected to soon break through the +10m bpd, challenging top producers Russia and Saudi Arabia.

Gold prices have reversed their early gains overnight to trade slightly lower ahead of the U.S open, as the dollar recovered from a three-year low against G10 currency pairs. Spot gold is down -0.3% at +$1,334.86 an ounce.

Note: It touched it’s strongest since Sept. 8 at +$1,344.44 on Monday.

3. Sovereign yields ease despite supply

U.S government bond prices edged higher in quiet trade yesterday following the holiday-extended weekend. With few economic reports scheduled for release stateside, market focus switched to the U.S Treasury Bill auctions (3-month, 6-month and 4-week bills) for directional clues.

Investors will now get a look at data on U.S housing starts and jobless claims, as well as comments from multiple Federal Reserve officials for directional yield clues.

Note: The yield on the two-year U.S note, which is considered to be especially sensitive to expectations for interest-rate increases from the Fed, settled last week above +2% for the first time in a decade.

The yield on the benchmark 10-year U.S Treasury note has fallen -2 bps to +2.532%. In Germany, the 10-year Bund yield fell -1 bps to +0.55%, while in the U.K the 10-year Gilt yield fell -1 bps +1.291%, the lowest in a week.

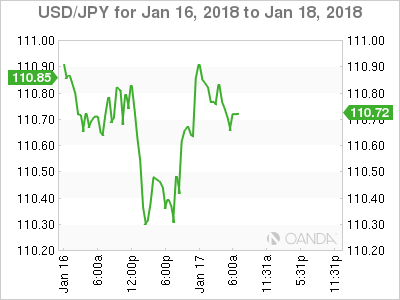

4. Dollar finds a toe-hole

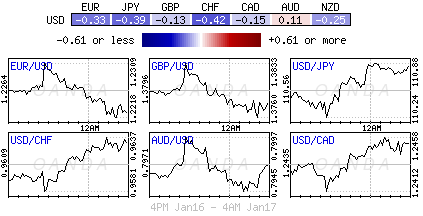

The USD has managed to move off its worst levels against G10 currency pairs.

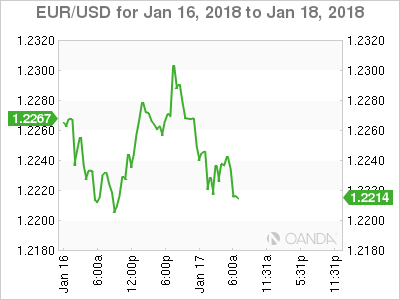

The EUR/USD (€1.2233) has managed to back away from its three-year overnight Asian high print on some aggressive profit taking. Various ECB members (Nowotny, Constancio and Villeroy) have made various comments on the recent price action of the ‘single’ currency. However, its the current German geo-political risks that has investors rethinking their ‘long’ EUR strategy ahead of this weekends German SPD vote on whether the social democrats are to go ahead with coalition talks with Chancellor Merkel (Sunday Jan 21).

GBP/USD (£1.3800) is a tad higher ahead of another vote in the House of Commons on the E.U withdrawal bill – The legislation is not expected to have any issues in its third reading, but could face some turbulence when it moves into the House of Lords.

USD/JPY (¥110.67) is slightly higher, but remains below the psychological ¥111.00 handle. The markets focus is switching to next week’s Bank of Japan (BoJ) meeting and is wondering if Kuroda and company might adjust their 'yield control guidance'.

USD/CAD (C$1.2433) is not straying too far from yesterday’s close ahead of this mornings Bank of Canada (BoC) rate decision. Markets are looking for the central bank to hike for the third time in its current tightening cycle, maybe a ‘dovish hike’.

Bitcoin (BTC) has fallen another -9% ($10,300) from yesterdays extended -26% sell-off.

5. Euro annual inflation down to +1.4%

Data this morning from the Euro area recorded annual inflation at +1.4% in December 2017, down from +1.5% in November. In December 2016, the rate was +1.1%, while in December 2017 it was +1.7%.

Digging deeper, the lowest annual rates were registered in Cyprus (-0.4%), Ireland and Finland (both +0.5%) and Denmark (+0.8%), while the highest annual rates were recorded in Lithuania and Estonia (both +3.8%) and the U.K (+3.0%).

Note: Compared with 2017, annual inflation fell in twenty-three Member States, remained stable in four and rose in one.

DAX Dips As Eurozone Final CPI Edges Lower

The DAX has posted losses in the Wednesday session. Currently, the index is trading at 13,217.50, down 0.22% from the Tuesday close. On the release front, Eurozone Final CPI edged lower to 1.4%, matching the forecast. Eurozone Final Core CPI came in at 0.9%, as expected. On Thursday, Bundesbank President Jens Weidmann will speak at an event hosted by the Bundesbank and the IMF.

European stock markets are in red territory on Wednesday, taking their cues from the Asian markets. As well, there is little support from the euro, which has posted declines on the day. After a tremendous start to the year for equity markets, traders have taken a pause, perhaps questioning the fast jump out of the gates in the first half of January. Still, the markets seem well positioned to continue the rally. The eurozone economy enjoyed a strong 2018, and growth should continue in early 2018. There has been positive developments on the political front in Germany, as Angela Merkel’s conservatives and the Social Democrats have signed a coalition blueprint, raising hopes that coalition talks will bear fruit.

The DAX has received a boost on speculation that the ECB could wind up its stimulus later in the year, and perhaps even raise interest rates. Is the market getting a bit ahead of itself? On Tuesday, Bundesbank President Jens Weidmann said in a newspaper interview that he did not expect interest rates to rise until mid-2019, even if QE ends in late 2018. If Weidmann reiterates this stance on Thursday, investors may take note and the euro could backtrack on some of its recent gains.

Euro Steady As Eurozone Final CPI Matches Forecast

The euro has posted losses in the Wednesday session. Currently, EUR/USD is trading at 1.2234, down 0.18% on the day. In economic news, Eurozone Final CPI ticked lower to 1.4%, matching expectations. In the US, there are no key events on the schedule. On Thursday, Bundesbank President Jens Weidmann will speak at an event hosted by the Bundesbank and the IMF. It’s a busy day in the US, with the release of construction, manufacturing and employment reports.

The euro continues to enjoy a sunny January. The continental currency has gained 2.4% this month, and this week, the EUR/USD touched highs not seen since December 2014. Investors flocked to the euro following the ECB minutes, which has raised speculation that the ECB could wind up its asset purchase program (QE) in September 2018. As well, substantial progress in German coalition talks has also boosted sentiment towards the euro. Talk of the ECB reducing stimulus in September, and perhaps raising interest rates afterwards have boosted the euro. However, on Tuesday, Bundesbank President Jens Weidmann said in a newspaper interview that he did not expect interest rates to rise until mid-2019, even if QE ends in late 2018. If Weidmann reiterates this stance on Thursday, investors may take note and the euro could backtrack on some of its recent gains.

Investors are keeping an eye on the Federal Reserve, which holds its next policy meeting on January 31. A rate hike is a virtual certainty, with CME Fed Watch pegging the odds of a quarter-point hike at 98.5%. Although this means that a rate hike has been priced in by the markets, the dollar could nevertheless gain ground after a hike, as a rate increase would signify an important vote of confidence in the economy by the Fed Reserve. If the US economy continues to expand at a c clip of around 3 percent, there is a strong likelihood of another rate hike in the first half of 2018.

USD/JPY Weakening Short-Term Bullish Momentum?

USD/JPY is consolidating after its rebound from the low at 110.30. A break of the hourly resistance at 110.85 is needed to suggest something more than a temporary bounce. Strong resistance can be found at 113.75 (12/12/2017 high). The technical structure suggests further short-term downside moves.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

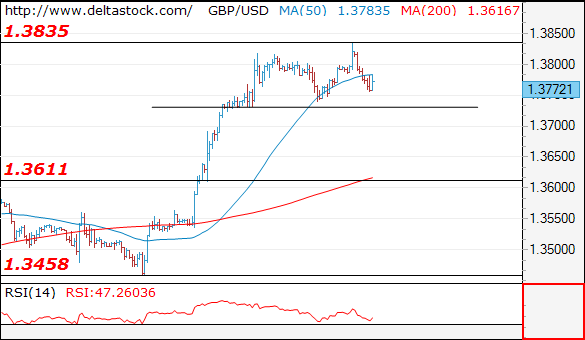

GBP/USD Bullish Consolidation

GBP/USD is trading on an uptrend bias. The technicals are highly positive at the moment. Hourly support is given at a distance at 1.3458 (11/01/2018 low) while strong resistance at 1.3764 (15/01/2018 high) is being monitored.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. The pair has set up a long-term support given at 1.1841 (07/10/2017 low). A reversal is currently happening. Strong resistance is given at 1.5018 (24/06/2016 high).

EUR/USD Bouncing

EUR/USD is bouncing back lower. Hourly resistance is given at 1.2297 (15/01/2018 high). hourly support is located at 1.2190. Stronger support is given a distance at 1.1916 (09/01/2018 low).

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2226

I favor a break through 1.2190 static support, towards 1.2090 break-out area. Initial intraday resistance lies at 1.2260.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2260 | 1.2500 | 1.2190 | 1.2090 |

| 1.2320 | 1.2500 | 1.2090 | 1.1910 |

USD/JPY

Current level - 110.78

The reversal at 110.16 signals another test of 111.00 area and I favor a break through the latter to challenge 112.00 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.00 | 112.00 | 110.00 | 109.50 |

| 112.00 | 113.75 | 109.50 | 109.50 |

GBP/USD

Current level - 1.3772

The intraday bias is bearish after the new peak at 1.3835, for a break through 1.3730 static support, towards 1.3650 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3835 | 1.3835 | 1.3730 | 1.3611 |

| 1.3900 | 1.4000 | 1.3650 | 1.3460 |

AUDCAD Trades Significantly Higher, Touches An Almost 5-Month High

AUDCAD surged to a fresh almost 5-month high during today's European session above the strong psychological level of 0.9900. The price headed for a test of the 0.9915 barrier and successfully surpassed it confirming the recent scenario for further gains.

In addition, the pair jumped above the downward sloping channel, which has holding since May 2017 and is approaching the 50-week simple moving average of 0.9940. In the daily chart, AUDCAD is trading well above the 20 and 40 SMAs and the sharp upward rally started after the rebound on 0.9710.

From the technical point of view, in the near-term, the RSI indicator holds in the positive territory and is moving towards the overbought zone, whilst the MACD oscillator posted a bullish crossover with its trigger line in the previous sessions and is strengthening its bullish momentum.

If traders boost the price further up, they could drive it until the 1.0000 strong handle but it needs first to go through the 50.0% Fibonacci retracement level at 0.9960 of the down-leg with the high of 1.0345 and the low of 0.9580.

Conversely, a dip back below the 38.2% Fibonacci level of 0.9870 and the falling trend line of the downward sloping channel the immediate support level to watch is the 23.6% Fibonacci mark of 0.9760, which coincides with the 40-day SMA.

Market Update – European Session: Euro Off 3-Years Highs As ECB Members Provide Some Verbal Intervention

Notes/Observations

Various ECB members (Nowotney, Constancio and Villeroy) observing the recent price action of the Euro

Focus on whether Bank of Canada will hike for the 3rd time in its current tightening cycle

Asia:

PBOC reminds that targeted RRR cut announced for some banks in Sept, to go into effect Jan 25th

China State-owned Assets Supervision and Administration Commission (SASAC) noted that State companies made progress in handing zombie companies. Would put overly indebted SOEs on watch list. Expected SOEs avg debt ratio to decline by 200bps by 2020

Moody's Official: Recent gains in JGBs yields did not imply that the Japan government's funding conditions would worsen. Did not believe that any BoJ tightening was 'imminent' -Diplomats from 20 countries agreed to enforce more rigorous inspections of vessels at sea to prevent smuggling into North Korea dueing a 1-day meeting in Vancouver

Europe:

ECB Weidmann (Germany): would be appropriate to end ECB's asset purchases this year. ECB could not ignore the negative side effects of the QE program. Analyst expectation for a mid-2019 rate hike was about in line with ECB guidance

Americas:

GOP leaders said to be weighing stopgap bill to avert Govt. shutdown to Feb 16th in order to buy time for a broader spending deal

Economic Data:

(EU) Dec EU27 New Car Registrations: -4.9% v +5.9% prior

(EU) Euro Zone Dec Final CPI Y/Y:% v 1.4%e; CPI Core Y/Y: 0.9% v 0.9%e

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

(DK) Denmark sold total DKK2.92B in 3-month and 6-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.2% at 397.5 , FTSE -0.3 at 7735, DAX -0.1% at 13230, CAC-40 -0.2% at 5501 , IBEX-35 -0.5% at 10469, FTSE MIB -0.1% at 23485 , SMI -0.2% at 9443, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices trade mostly lower across Europe following the slight pullback seen yesterday in the US. US futures are rebounding this morning helping lift European Stocks off the lows. Shares of ASML advance after handily beating estimates, while shares of Casino and Burberry sharply decline following their earnings. In other notable movers Pearson trades over 5% lower after guiding FY18 lower y/y, and Skanska trades sharply lower after a profit warning, and restructuring iniatives. In the M&A space UBM trades higher after a merger agreement with Informa, while GKN received an improved takeover offer from Melrose. Shares of IWG trade higher after reports of bid interest. Looking ahead, major banking names continue to report with Bank of America, Goldman Sachs and US Bancorp all set to announce earnings.

Movers

Consumer Discretionary [UBM [UBM.UK] +12.6%, Informa [INF.UK] -7.3% (UBM to be acquired by Informa in Cash and Stock deal), Casino [CO.FR] -4.6% (Earnings), Pearson [PSON.UK] -6.4% (Trading update), Burberry [BRBY.UK] -6.5% (Earnings), IWG [IWG.UK] +5.3% (Takeover interest)]

Industrials [ Henry Boot [BOOT.UK] +1.4% (Trading update), GKN [GKN.UK] +0.9% (Melrose raises offer), Skanska [SKAB.SE] -6.5% (Profit warning)]

Technology [ ASML [ASML.NL] +5% (Earnings)]

Speakers

ECB's Constancio (Portugal) stated that did not rule out that monetary policy would continue to be very accommodating for a long time (**Note: in-line with Draghi's view). Would be concerned if Euro price action did not echo fundamentals. Had not heard convincing arguments for transforming the ESM into an IMF-like European Monetary Fund.

ECB's Nowotny (Austria): Euro currency rate must be observed; strengthening currency was not helpful. Reiterated that ECB did not have an exchange rate target; could only watch in terms of fundamentals. Recent appreciation of Euro won't necessarily be a permanent development. Main reason for recovery in FX had been export driven

Norway Fin Min Jensen: Economic downturn is over but face challenges ahead. Facing aging population and smaller returns from sovereign wealth fund

Russia Central Bank 1st Dep Gov Yudaeva: Lowering interest rates quite quickly

Czech Govt resigned following a no-confidence vote loss (as speculated)

Kuwait oil official: Dec oil cut compliance at 125%; expects compliance to remain high in 2018. Oman oil meeting would not be about any exit from current production cut agreement as oil producers were committed to cuts no matter what the oil price. Oil market to absorb all new supply in 2018

Currencies

USD moved off its worst levels against the major pairs as dealers noted that recent price action might have been excessive.

EUR/USD moved off its fresh 3-year highs of 1.2323 that was registered during the Asian session. Various ECB members (Nowotny, Constancio and Villeroy) were observing the recent price action of the Euro. Dealers noted that EUR could prove to be unattractive ahead of Germany's SPD vote on whether to go ahead with coalition talks this Sunday

GBP/USD slightly lower ahead of another vote in the House of Commons on the EU Withdrawal bill. The legislation should have no issues in its 3rd reading but could face some turbulence when it moves into the House of Lords.

USD/JPY slightly higher by remaining below the 111 level. Some dealers were looking ahead to next week's BOJ meeting and pondering if the central bank would adjust its Yield Control guidance.

USD/CAD hovering in the mid-1.24 area ahead of the BOC rate decision. Markets are looking for the central bank to hike for the 3rd time in its current tightening cycle. Some analysts noted it could be viewed as a ‘dovish hike'.

Fixed Income

Bund Futures trades up 5 ticks at 160.91 after Euro Zone CPI comes right in line with expectations. Continued upside targets 162.00, while a move lower targets the159.56 low.

Gilt futures trade at 124.11 up 11 ticks as Gilts remained capped so far. Support continues to stand at 123.55 then 122.83, with upside resistance at 124.25 then 124.96.

Wednesday's liquidity report showed Tuesday's excess liquidity fell to €1.871T from €1.874T prior. Use of the marginal lending facility fell to €401M from €286M prior.

Corporate issuance saw 3 issuers set to raise $2.4B in the primary market

Looking Ahead

(UK) EU Withdrawal Bill gets its 3rd reading in the Commons before moving onto the Lords

(IT) ECB's Nouy (SSM chief) to meet Bank of Italy officials and banking sector heads to discuss non-performing loans (NPLs)

05:30 (DE) Germany to sell €1.5B in 1.25% Aug 2048 Bunds

05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.25-1.75B in 6-month and 12-month bills

06:00 (ZA) South Africa Nov Retail Sales M/M: 0.8%e v -0.1% prior; Y/Y: 3.7%e v 3.2% prior

06:45 (UK) BOE Saunders in London

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB40B in 2024 and 2033 OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Jan 12th: No est v 8.3% prior

07:15 (DE) German Chancellor Merkel in Berlin

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (RU) Russia Q4 Preliminary Current Account: +$11.5Be v -$2.5B prior

08:00 (RU) Russia Nov Trade Balance: $9.7Be v $9.8B prior; Exports: $32.5Be v $31.4B prior; Imports: $22.0Be v $21.6B prior

08:00 (PL) Poland Dec Employment M/M: 0.1%e v 0.3% prior; Y/Y: 4.5%e v 4.5% prior

08:00 (PL) Poland Dec Average Gross Wages M/M: 7.4%e v 0.8% prior; Y/Y: 6.9%e v 6.5% prior

08:05 (UK) Baltic Dry Bulk Index

08:50 (SE) Sweden Central Bank (Riksbank) Dep Gov Ohlsson

08:55 (US) Weekly Redbook Sales

09:00 (PT) Portugal Fin Min Centeno with German Fin Min Altmaier in Berlin

09:15 (US) Dec Industrial Production M/M: 0.5%e v 0.2% prior; Capacity Utilization: 77.4%e v 77.1% prior; Manufacturing Production: 0.3%e v 0.2% prior

10:00 (CA) Bank of Canada (BOC) Interest Rate Decision: Expected to leave Interest Rates unchanged at 1.00%

10:00 (US) Jan NAHB Housing Market Index: 72e v 74 prior

13:00 (AR) Argentina Dec Budget Balance (ARS): No est v -29.7B prior

14:00(US) Federal Reserve Beige Book

15:00 (US) Fed's Evans (non-voter, dove) on economy and monetary policy

16:00 (US) Nov Total Net TIC Flows: No est v $151.2B prior; Net Long-term TIC Flows: No est v 23.2B prior

16:30 (US) Weekly API Oil Inventories

16:30 (US) Fed's Mester (voter, hawk) on monetary policy communication

19:00 (AU) Australia Jan Consumer Inflation Expectation: No est v 3.7% prior

19:01 (UK) Dec RICS House Price Balance: -1%e v 0% prior

19:30 (AU) Australia Dec Employment Change: +15.0Ke v +61.6K prior; Unemployment Rate: 5.4%e v 5.4% prior

20:00 (KR) Bank of Korea (BOK) Interest Rate Decision: Expected to leave 7-Day Repo Rate unchanged at 1.50%

Technical Outlook: EURUSD Remains In Directionless Mode On Tuesday, But Deeper Pullback Could Be Anticipated

The Euro stays in a choppy mode for the second day, despite brief probe above 1.2300 barrier overnight.

The pair returned quickly from the session high at 1.2323, staying at the back foot during European trading.

Strong indecision is signaled by long-legged Doji left on Tuesday, with today's action remaining in directionless mode.

Negative signals are developing on daily chart and weigh on the pair, as daily RSI and slow stochastic are reversing in the overbought territory and momentum is turning south, suggesting corrective action.

Close below lows of Mon/Tue at 1.2187/95 would generate initial bearish signal for extension towards pivotal support at 1.2167 (Fibo 38.2% of 1.1915/1.2323 upleg).

Rising 10SMA marks strong support at 1.2093, where extended dips should find ground, before larger bulls resume.

EU inflation data, released today, showed CPI in line with expectations in December (1.4%) which could satisfy hawks.

On the other side, inflation remains below central banks target and policymakers remain cautious about interest rate hike, which could affect the pace of Euro's bulls and fuel corrective action.

Res: 1.2296, 1.2323, 1.2350, 1.2400

Sup: 1.2208, 1.2187, 1.2167, 1.2119