Sample Category Title

WTI OIL – Correction to Precede Fresh Upside

WTI oil stays in red on Wednesday after previous day's negative close which generated reversal signal.

Fresh weakness pressures solid support at $63.25, provided by rising 10SMA, with break here needed to generate fresh bearish signal.

Larger bulls look for correction before continuing higher as overall sentiment remains firm on OPEC-led production cut which resulted in continuous draws in US crude stocks that boosted oil price.

Correction is also signaled by reversal of overbought daily RSI and slow stochastic.

Loss of 10 SMA handle would open rising 4-hr cloud ($63.07/$62.13) and Fibo 38.2% of $56.08/$64.87 at $61.61, in extension.

Conversely, early downside rejection (ideally above 10SMA/4-hr cloud top) would prompt bulls for retest of recent over three-year peak at $64.87 and extension of larger recovery leg from $44.18 (21 June 2017 trough).

Res: 63.94; 64.87; 65.00; 65.88

Sup: 63.25; 63.07; 62.80; 62.13

Loonies Wild Ride: Bank of Canada (BoC) Hikes Rates

The Bank of Canada has hiked overnight rates by a +25 bps to +1.25% on the strength of stellar employment data and a pickup in inflation.

It can be viewed as a "dovish" hike as the BoC signalled a "gradual, cautious approach to further rate increases, warning uncertainty tied to the future of the North American Free Trade Agreement (NAFTA) is likely to exert a drag on growth.

"Recent data have been strong, inflation is close to target and the economy is operating roughly at capacity," the Bank of Canada said in a statement. "However, the uncertainty surrounding the future of Nafta is clouding the economic outlook."

Underlying economic fundamentals at home and abroad have strengthened, and would otherwise suggest a strong pickup in business investment and exports, the bank said. But trade-policy uncertainty on the North American front would slow growth in both categories, it said.

The loonie came under immediate pressure to trade north of the C$1.25 handle. It's currently down -0.78% at C$1.2478.

Yen Slightly Weaker as US Manufacturing Reports Impress

It continues to be an uneventful week for the Japanese yen. In Wednesday's North American session, USD/JPY is trading at 110.75, up 0.30% on the day. On the release front, Japanese Core Machinery Orders posted a strong gain of 5.7%, well above the estimate of -1.1%. Industrial Production accelerated to 0.9%, crushing the estimate of 0.4%. Later in the day, Japan releases Industrial Production, which is expected to edge up to 0.6%. In the US, manufacturing numbers looked sharp. Capacity Utilization improved to 77.9%, beating the estimate of 77.3%. This marked the highest level since July 2014.

Japan's economy continues to gains steam, buoyed by a strong export sector and increased consumer spending. The positive trend has elicited bullish comments from the cautious Bank of Japan. On Monday, BoJ Governor Haruhiko Kuroda sounded optimistic about the economy and inflation, and the Japanese yen responded by climbing to a 4-month high. Kuroda said that core CPI had improved to about 1 percent, and said that the BoJ expected the economy to "continue expanding moderately". This was a much more favorable prognosis compared to October 2016, when Kuroda stated that inflation was around zero. Although Kuroda reiterated that the BoJ will maintain its massive stimulus program, a stronger Japanese economy has raised speculation that the Bank could follow the ECB and reduce its asset purchase program, which would likely strengthen the Japanese yen. The BoJ's quarterly report was also optimistic about inflation, stating that stronger growth would raise inflation closer to the BoJ's target of around 2 percent.

The markets are keeping one eye on the Federal Reserve, which holds its next policy meeting on January 31. A rate hike is a virtual certainty, with CME Fed Watch pegging the odds of a quarter-point hike at 98.5%. Although this means that a rate hike has been priced in by the markets, the dollar could nevertheless gain ground after a hike, as a rate increase would signify an important vote of confidence in the economy by the Fed Reserve. If the US economy continues to expand at a clip of around 3 percent, there is a strong likelihood of another rate hike in the first half of 2018.

(BOC) Bank of Canada Increases Overnight Rate Target to 1 1/4 Per cent

The Bank of Canada today increased its target for the overnight rate to 1 1/4 per cent. The Bank Rate is correspondingly 1 1/2 per cent and the deposit rate is 1 per cent. Recent data have been strong, inflation is close to target, and the economy is operating roughly at capacity. However, uncertainty surrounding the future of the North American Free Trade Agreement (NAFTA) is clouding the economic outlook.

The global economy continues to strengthen, with growth expected to average 3 1/2 per cent over the projection horizon. Growth in advanced economies is projected to be stronger than in the Bank's October Monetary Policy Report (MPR). In particular, there are signs of increasing momentum in the US economy, which will be boosted further by recent tax changes. Global commodity prices are higher, although the benefits to Canada are being diluted by wider spreads between benchmark world and Canadian oil prices.

In Canada, real GDP growth is expected to slow to 2.2 per cent in 2018 and 1.6 per cent in 2019, following an estimated 3.0 per cent in 2017. Growth is expected to remain above potential through the first quarter of 2018 and then slow to a rate close to potential for the rest of the projection horizon.

Consumption and residential investment have been stronger than anticipated, reflecting strong employment growth. Business investment has been increasing at a solid pace, and investment intentions remain positive. Exports have been weaker than expected although, apart from cross-border shifts in automotive production, there have been positive signs in most other categories.

Looking forward, consumption and residential investment are expected to contribute less to growth, given higher interest rates and new mortgage guidelines, while business investment and exports are expected to contribute more. The Bank's outlook takes into account a small benefit to Canada's economy from stronger US demand arising from recent tax changes. However, as uncertainty about the future of NAFTA is weighing increasingly on the outlook, the Bank has incorporated into its projection additional negative judgement on business investment and trade.

The Bank continues to monitor the extent to which strong demand is boosting potential, creating room for more non-inflationary expansion. In this respect, capital investment, firm creation, labour force participation, and hours worked are all showing promising signs. Recent data show that labour market slack is being absorbed more quickly than anticipated. Wages have picked up but are rising by less than would be typical in the absence of labour market slack.

In this context, inflation is close to 2 per cent and core measures of inflation have edged up, consistent with diminishing slack in the economy. The Bank expects CPI inflation to fluctuate in the months ahead as various temporary factors (including gasoline and electricity prices) unwind. Looking through these temporary factors, inflation is expected to remain close to 2 per cent over the projection horizon.

While the economic outlook is expected to warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed to keep the economy operating close to potential and inflation on target. Governing Council will remain cautious in considering future policy adjustments, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.

Information note

The next scheduled date for announcing the overnight rate target is March 7, 2018. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR on April 18, 2018.

Dollar Stabilizes… But for How Long?

The battered Dollar stabilised against its peers on Wednesday as investors pondered the possibility of a US Government shutdown on Friday.

Heightened political uncertainty in Washington is likely to weigh heavily on the Dollar and may fuel the downside. It is interesting that the Dollar remains at such depressed levels despite expectations of a US rate hike in March. Dollar bulls are clearly struggling to find fresh inspiration from Fed hike expectations, and this is reflected in the currency's bearish price action. Appetite for the Dollar is at risk of diminishing even further if major central banks join the Federal Reserve and gradually tighten monetary policy.

From a technical standpoint, the Dollar Index still remains under pressure on the daily charts. A technical bounce could be in process, and might push prices into the 91.40 region. Alternatively, an intraday breakdown below the 90.34 daily low could invite a further decline towards 90.00.

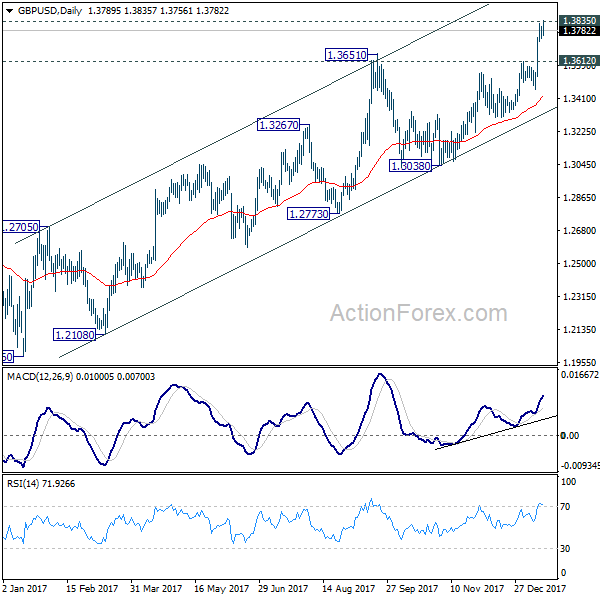

Currency spotlight - GBPUSD

Sterling has jumped to its highest level since the June 2016 Referendum vote, thanks to ongoing Dollar weakness and market optimism over a soft Brexit.

While the Pound could venture higher in the near term, it must be kept in mind that the currency still remains highly sensitive to political and Brexit developments. Taking a look at the technical picture, the GBPUSD is incredibly bullish on the daily charts. Prices are trading above the 50 SMA while the MACD has crossed to the upside. A decisive breakout above 1.3850 could invite an appreciation higher towards 1.3920 and 1.4000, respectively. Alternatively, a failure for prices to close above 1.3850 may open a path back to 1.3700.

Commodity spotlight - Gold

Gold bulls displayed early signs of exhaustion on Wednesday after struggling to maintain control above $1340. Prices are currently trading around $1335.50 and could edge lower later in the day amid a stabilising Dollar.

From a technical standpoint, Gold still fulfills the prerequisites of a bullish trend based on the consistently higher highs and higher lows. A technical correction seems to be in process, with the next level of interest at $1325. If bulls are able to re-awaken before the $1325 level, the price could re-test $1340 and $1360, respectively.

USDCHF: Backs Off Lower Prices On Correction

USDCHF - The pair halted its broader weakness on Wednesday leaving risk of more correction on the cards. On the downside, support lies at the 0.9650 level. A turn below here will open the door for more weakness towards the 0.9600 level and then the 0.9550 level. On the upside, resistance resides at thehttps://www.actionforex.com/administrator/index.php?option=com_content&view=article&layout=edit#publishing 0.9700 level where a break will clear the way for more strength to occur towards the 0.9750 level. Further out, resistance comes in at the 0.9800 level. Above here if seen will turn attention to 0.9850. All in all, USDCHF faces further weakness short term but with caution of a recovery.

Canadian Dollar Subdued Ahead of BoC Rate Announcement

USD/CAD continues to trade sideways this week. In the Wednesday session, the pair is trading at 1.2444 up 0.08% on the day. On the release front, all eyes are on the Bank of Canada, which is expected to announce a rate hike. The BoC will also release its quarterly monetary report, and BoC Governor Stephen Poloz will host a press conference. In the US, there are major releases. On Thursday, there are a host of key indicators out of the US, led by Building Permits and unemployment claims.

Will he or won't he? Most experts are predicting that Governor Stephen Poloz will raise rates by 25 basis points, from 1.00% to 1.25%. Even if the BoC raises rates, Poloz could turn the move into a 'dovish hike', if he emphasizes that future rates will be data-dependent. The BoC last raised rates in September, marking a third rate hike in 2017. The Canadian economy has looked strong of late, underscored by unexpectedly strong employment data. At the same time, Poloz has some concerns about the economy, particularly looming dark clouds over NAFTA. The free-trade agreement, crucial to the Canadian economy, is in trouble, as US President Trump has threatened to cancel the pact unless Mexico and Canada make major concessions to the US. If the agreement is terminated, the Canadian dollar would likely take a tumble.

The markets are keeping one eye on the Federal Reserve, which holds its next policy meeting on January 31. A rate hike is a virtual certainty, with CME Fed Watch pegging the odds of a quarter-point hike at 98.5%. Although this means that a rate hike has been priced in by the markets, the dollar could nevertheless gain ground after a hike, as a rate increase would signify an important vote of confidence in the economy by the Fed Reserve. If the US economy continues to expand at a c clip of around 3 percent, there is a strong likelihood of another rate hike in the first half of 2018.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.14; (P) 110.56; (R1) 110.88; More...

Intraday bias in USD/JPY remains neutral at this point. In case of another fall, we'd look for bottoming again below 61.8% retracement of 107.31 to 114.73 at 110.14. Meanwhile, on the upside, break of 111.26 support turned resistance will suggest that USD/JPY has bottomed slightly earlier than expected. In that case, intraday bias will be turned back to the upside for 113.38 resistance. Decisive break there will confirm completion of the corrective pull back from 114.73 and turn outlook bullish.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

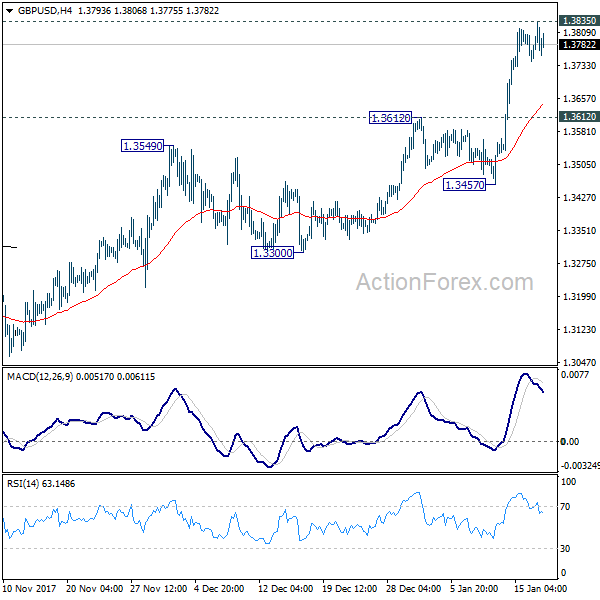

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3752; (P) 1.3778; (R1) 1.3816; More.....

Intraday bias in GBP/USD remains neutral at this point. Also, we'd still expect strong resistance from 1.3835 to limit upside to complete the medium term rally from 1.1946. Break of 1.3612 resistance turned support will be the first sign of reversal and turn bias back to the downside for 1.3457 support first. However, sustained break there will carry larger bullish implication and target long term fibonacci level at 1.5466.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

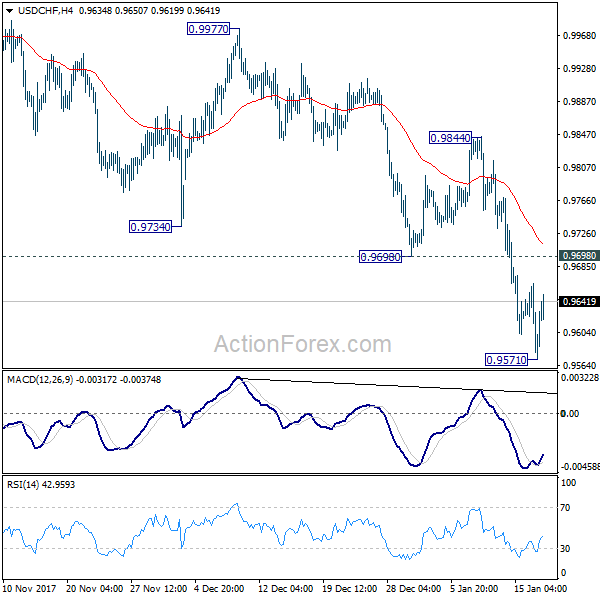

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9562; (P) 0.9613; (R1) 0.9647; More....

Intraday bias in USD/CHF remains neutral for consolidation above 0.9571 temporary low. As long as 0.9698 support turned resistance holds, deeper fall could be seen to 0.9420 low. Nonetheless, break of 0.9698 will indicate short term bottoming. Intraday bias would then be turned back to the upside for 0.9844 key near term resistance next.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.