Sample Category Title

All Your Eggs In The One Basket ?

The majority of the street found themselves with most of their eggs in the short dollar basket as ECB jawboning threw cold water on the Euro rally, and hawkish Fed comments gave rise to pair back on offside dollar risk.

In the NY afternoon, Foreign Exchange Traders were busy digesting Apple’s new US campus news while attempting to protect the actual repatriation impact and some incorrect calculations could have contributed to USD correction. But with headlines suggesting that most of the proceeds are in dollar-denominated accounts, it should have minimal impact on currency markets over the near term. But at least this will make peace with the Trump administration for Apple executives farming out iPhone production to Asia.

Interesting note from the Tic data is that China’s US treasury holding fell to the lowest level since July, so perhaps there is some truth to last weeks “Fake News” story out of China.

Oil Market Overview

WTI prices are firming up in early Asia after The American Petroleum Institute figures for the week ended January 12 showed a larger-than-expected draw. The draw indeed confirms that inventories are contacting at much quicker pace than the market anticipated and with confirmation from tomorrows more conclusive DoE report, it would provide a substantial boost to the bullish demand side narrative.

Gold Market Overview

A weaker US dollar has primarily driven gold prices of late.And what started as a ripple of risk reduction after printing four-month highs, has morphed into a mini-correction as UST’s fell with gold and the greenback has jumped on speculation Congress will avoid a government shutdown. Also, a more hawkish tone from Fed member Kaplan has sent UST 10’s to 2.58 %. Moreover, the Hawkish Fed rhetoric could temper near-term dollar weakness suggesting we could see a deeper correction on Gold prices over the next few session and a period of consolidation awaiting the eventual next dollar demise.

US Equity Markets

The song remains the same. Broader equity markets surged higher with the Dow closing above 26,000 for the first time as earnings fervour takes grip cementing Investor bias that the new corporate tax code will substantially raise earnings this year.

Is Bitcoin headed for the Crypt?

From its dizzying ascent to its precipitous and rapid decline over the past 48 hours, bitcoins retail bagholders would be well-served to keep an eye on the regulatory clampdown risks that are lurking in the shadows. Frankly, it would not be surprising to see more high profile regulators take to the airwaves after Steven Maijoor, the chair of the European Securities and Markets Authority, sounded the alarm yesterday. And It’s not too far of a stretch to assume that regulatory crypto clampdowns designed to discourage speculation in South Korea and China will spread globally.

After a massive two-day selling frenzy now comes the fear of the unknown as the nasty can always get nastier especially for those that keep buying or use similar high-risk strategies. And regardless of how much I torture the data to achieve a modicum of positivity after Bitcoin has all but halved in value since it’s meteoric rise, all roads suggest another halving in value before the falling knife pattern subsides. To say ” Bitty” remains fragile is a massive understatement as we’re little more than a cynical headline or two away from teetering on the edge of the abyss.

G-10

The Euro

With the flurry of ECB speakers upping the dovish rhetoric in the past 24 hours coupled Fed’s Kaplan suggesting that three hikes are his base case with risks to more and boosting the US yield curve steeper. It should be enough to temper some of the Euro’s current optimism.

Indeed The Euro is looking a bit toppy and choppy after the ECB pushback which should favour some long EUR risk reduction, suggesting we could enter and a period of consolidation

Indeed, with more two-way flows coming to market trading conditions become more unsettled and price discovery becomes a function of position risk, while speculation becomes more of a spaghetti test ahead of the SPD vote on Sunday.

The Japanese Yen

After drinking the market kool-aid earlier in the week, it became evident after the second pass at 110 yesterday that moves were becoming brief and robust dollar demand out of Tokyo below 110.50 suggested a base was forming. While dollar bearishness probably has much more room to play out over the medium term, at this time, given the strengthening Yen will trigger stronger pushback at next weeks BoJ policy meeting, short dollar positions are reducing. And with the hawkish chorus of Fed speak triggering a spike in US Treasury yields, USDJPY could pick up some near-term demand and at minimum remain firmly bid on dips

Asia FX

The Malaysian Ringgit

With the broader USD sell-off abating on the back of higher US yields and hawkish Fed rhetoric, it suggests the Ringgit market will pause for thought, and we could enter a period of consolidation awaiting the next domestic catalysts. There were some jitters in the MYR bond markets yesterday as after attempting to rally at yesterdays open the moves were met with a wave of selling, which carried throughout yesterdays session suggesting the market was looking to trim risk. In the absence of any local bond demand, we could see USDMYR edging higher compounded by higher US yields and a moderately stronger US dollar

Bank of Canada Boosts Overnight Rate Highlights NAFTA Risks

Highlights:

- The overnight rate stands at 1.25%, the highest in the post-recession period

- The bank thinks the economy is operating close to its potential but noted that while slack in the labour market has diminished, wage growth remains modest.

- Uncertainty around NAFTA renegotiation was highlighted as risk to the economic outlook. A break-down of talks would likely lead to a more cautious approach from the Bank of Canada.

- The bank noted less monetary policy stimulus is likely over time although still sees the need for some level of accommodation to keep inflation on target. As such they will proceed cautiously and be guided by incoming data.

Our Take:

As expected, the bank raised its policy interest rate today by 25 basis point to 1.25%, the highest level in the post-recession period. The bank believes some policy accommodation will need to be maintained for the inflation to rise to its 2% target on a sustained basis although that does not preclude higher rates with the economy at capacity. The statement also highlighted the elevated uncertainty about the outlook coming from the NAFTA renegotiations which the bank addressed in its forecast by tempering the outlook for investment and trade. That said, on the economic outlook, the bank lifted its forecasts for both 2018 and 2019 looking for exports, business investment and spending on infrastructure to mitigate some of the impact of a moderation in housing and consumer spending. Once again, the bank upped its estimate of the economy's potential growth rate (to 1.6% from 1.5%) reflecting a faster buildup in the capital stock and noted that the economy was close to capacity limits at the end of 2017.

Today's statement provided a positive outlook with the bank stating that the fundamentals supporting the economy solidified since their last report. That said, concerns about the outcome of the NAFTA negotiations and the unsatisfactory pace of wage gains given residual labour market slack remain. Our forecast is for the economy to grow at an above-potential pace and inflation to hold at the 2% target later this year. Absent any negative NAFTA outcome, we expect the policy rate to rise to 2% by year end.

BoC: Poloz Bumps Up Borrowing Costs, But Caution Still the Word

The Bank of Canada increased its key monetary policy interest rate by 25bps this morning, to 1.25%.

The decision was accompanied by the latest Monetary Policy Report (MPR), which provided a fresh view of the Bank's economic outlook. The Bank estimates that growth in 2017 averaged 3.0%, while their outlook for this year has been upgraded slightly, to 2.3%, from 2.1% in October. Growth of 1.6% is projected for 2019, embodying a modest improvement from October's 1.5% forecast.

The pace of potential growth remained a key concern for the Bank. It is possible that strong demand may be motivating increased inputs of capital and labour, and the Bank will closely monitor developments on this front. In practical terms, although strong business investment has led the Bank to upgrade the level of potential in 2017, the output gap is judged to be in the -0.25% to +0.75% range, suggesting that economic slack has been effectively absorbed. The Bank acknowledged that labour market slack is being absorbed more quickly than previously anticipated. However, wage data and other measures suggest that, in contrast to an overall lack of spare capacity in the economy, some slack may still remain in labour markets.

The diminishing slack has made itself felt in core inflation measures. While temporary factors such as energy price swings will generate near-term noise, inflation is expected to trend close to the midpoint of the Bank's 1% to 3% band over the forecast horizon.

As always, the MPR assessed the key risks to the economic outlook. Weaker exports are the top risk in light of NAFTA uncertainty and recent imposition of tariffs by the United States. Faster potential output, stronger U.S. growth and more robust consumer spending (paired with rising household debt) were also seen as risks. A "pronounced" drop in home prices in key overheated Canadian markets rounded out the list of concerns.

Key Implications

In light of an impressive run of labour market data and their latest Business Outlook Survey painting a positive picture, the Bank of Canada was widely expected to hike rates today, and Governor Poloz and company did not disappoint. It has become increasingly clear that emergency level interest rates are no longer warranted. But, while rates look likely to continue to rise, the key question remains "at what pace?"

Today's statement and MPR provided some further indication of the answer. Emergency level rates may not be needed, but that doesn't mean that the Bank is in a rush to continue hiking. NAFTA uncertainty hangs over the outlook, with the Bank explicitly downgrading the outlook for business investment and trade to account for the impact of negotiations. What's more, despite the positive run of labour market data, wage growth remains weaker than the Bank had expected. Most explicit was the statement that while the outlook will likely "warrant higher interest rates over time, some continued monetary policy accommodation will likely be needed".

As such, it remains our base-case view that a gradual pace of tightening is most likely, with the next hike penciled in for July. Data dependency of course means that this is not a lock. Developments in Poloz's list of areas to watch, including interest rate sensitivity, labour market developments, and inflation dynamics could easily bring the next hike forward, or push it back.

Note that the Bank of Canada Governor and Senior Deputy Governor will speak at a press conference at 11:15AM ET.

Gold Edges Lower as US Posts Strong Manufacturing Numbers

Gold has posted slight losses in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1336.32, down 0.18% on the day. On the release front, manufacturing numbers looked sharp. Capacity Utilization improved to 77.9%, beating the estimate of 77.3%. This marked the highest level since July 2014.On Thursday, there are a host of key indicators out of the US, led by Building Permits and unemployment claims.

The Federal Reserve hasn't been in the headlines since New Years', but the lull won't last much longer. The Fed will hold its next policy meeting on January 31. A rate hike is a virtual certainty, with CME Fed Watch pegging the odds of a quarter-point hike at 98.5%. Although this means that a rate hike has been priced in by the markets, the dollar could nevertheless gain ground after a hike, as a rate increase would signify an important vote of confidence in the economy by the Fed Reserve. If the US economy continues to expand at a clip of around 3 percent, there is a strong likelihood of another rate hike in the first half of 2018.

Gold often gains ground when investor risk appetite is weak, but that has not been the case early in 2018. Global stock markets are pointing higher and US economic numbers have been strong. This points to recent weakness in the US dollar as the catalyst for stronger gold prices. If major currencies such as the euro and Japanese yen continue to make inroads against the dollar, traders can expect the gold rally to continue.

Sunset Market Commentary

Moves on the US and European bond markets were modest today. The Bund future traded in a narrow sideways range between 160.78 and 160.97, maintaining yesterday's gain. The ECB warning on the potential impact of a strong euro on inflation and thus on ECB policy, maybe helped to protect the downside in European bonds. The German 10-yr yield is little changed at 0.55%. The very long end outperforms slightly. At the same time, US Treasuries slightly underperformed Bunds, with rates rising 1-2.5 bps across the curve. The 2-yr yield set a new cycle top at 2.04%. The moves were mostly technically inspired. Fed's Kaplan advocating a scenario of at least three rate hikes maybe helped to put a floor for US yields at the short end of the curve. Intra-EMU spread changes versus Germany were mostly limited between -1 bp (Greece) and +2 bps (Italy).

EUR/USD spiked briefly north of 1.23 early in Asia this morning. This time the gain could not be sustained and EUR/USD soon returned back lower in the 1.22 big figure. The quick reversal had some of the characteristics of a ST exhaustion move. The dollar became better bid across the board. After ECB's Villeroy yesterday, ECB members Constancio and Nowotny also warned that a sudden rise of the euro could complicate the ECB's efforts to bring inflation back to target. December EMU inflation was confirmed at a soft 1.4% for the headline inflation and 0.9% for the core. This was no surprise, but it reinforced the case of the ECB speakers. EUR/USD tested the 1.22 mark at the start of the US trading session. The 2-yr US/German interest rate differential rose to a cycle top of over 2.60 %. The 10-yr difference was little changed around 2%. Modest losses on global equity markets after yesterday's sharp intraday decline on WS also contained the risk of further, disorderly USD losses. US December industrial production was strong, but mostly due to growth at utilities and in mining. The reaction of the dollar was limited. EUR/USD trades near 1.2225. USD/JPY is changing hands around 110.75.

Sterling basically followed the broader trends in the euro and the dollar amid an empty UK eco calendar. EUR/GBP drifted south in line with the overall euro correction. The pair trades currently just above 0.8850. Cable is also trading of the overnight top, but levels around 1.38 can be considered as a sign of sterling resilience. BoE Saunders, from the hawkish wing of the BoE, saw chance of faster pay growth. Over time this might translate into faster BoE rate hikes.

News Headlines:

ECB's Nowotny warns on FX loans returning to Eastern European region as surveys show a rise in the number of retail clients considering borrowing in foreign currencies even as interest-rate differences narrow.

Stocks of industrial metals in London Metal Exchange (LME) warehouses fell more than 40 percent last year and further declines are expected in 2018, which should in theory signal tighter supplies and fuel a price rally. However rising inventories of metals at smaller rival exchanges suggest the real supply picture is more mixed.

Fed Kaplan, a non-voting member, says in an interview with the WSJ that he has "a lot of conviction that the base case should be three moves for this year, and if wrong, it could even potentially be more than that,"

The Bank of Canada raised its policy rate by 25 basis points to 1.25%. The move was largely expected after recent strong eco data. The BoC remains cautious on the pace of further rate hikes.

CADJPY Loses Momentum But Stands above Ascending Trend Line

CADJPY remains under pressure after the pullback on the 4-month high of 91.60. The pair plummeted towards the 88.50 support level and is now developing within the two medium-term simple moving averages of 50 and 100, at 88.60 and 89.12 respectively.

Looking at the daily timeframe, technical indicators are holding near their neutral levels. The MACD oscillator slid below its trigger line in the bullish area, however, the RSI indicator is pointing to the upside in the negative territory.

Upsides moves are likely to find resistance at the aforementioned 4-month high. Rising above this area would help to endorse the focus to the upside towards the strong psychological level of 93.00.

If price action drops below 88.50 (immediate support), there is scope to test the 23.6% Fibonacci retracement level at 87.65 of the up-leg with the low of 74.80 and the high of 91.60. Clearing this key level would see additional losses below the ascending trend line towards 86.80, which holds near the medium-term 200-SMA. The diagonal line stands since September 2016 and the price had several failed attempts to break it to the downside.

Pound Ticks Higher, US Industrial Indicators Beat Expectations

The British pound continues to trade sideways. In Wednesday's North American trade, GBP/USD is trading at 1.3804, up 0.09% on the day. In economic news, there are no major British indicators. In the US, there was positive news on the manufacturing front. Capacity Utilization improved to 77.9%, beating the estimate of 77.3%. This marked the highest level since July 2014.

Inflation in the UK edged lower in December, dropping from 3.1% to 3.0%. Still, that is still much higher than the Bank of England target of 2 percent. The BoE finds itself in a tough spot with regard to interest rate policy. The Bank is reluctant to raise rates, especially with the uncertainties over Brexit, but high inflation continues to erode the purchasing power of the British consumer. A weak pound has further dampened consumer spending, although a cheaper pound has been a boon for the export sector. The BoE holds its next policy meeting in February, and as matters currently stand, the BoE is not expected to raise rates.

The financial sector in the UK is expected to take a hit when Britain departs the European Union, and many foreign banks with operations in London are looking at setting up shop on the continent. The Bank of England is trying to help, and in December, the Bank said that it would exempt European bank branches in London from costly capital rules after Brexit, if the EU co-operated with the BoE. On Tuesday, BoE Deputy Governor Sam Woods told a parliamentary committee that the BoE urgently need more clarity on Brexit. Woods stated that foreign banks in London would accelerate their move to the continent, if there is no Brexit transition deal in place by the end of March. This could be very tall order, as negotiations have not gone well between Britain and the EU.

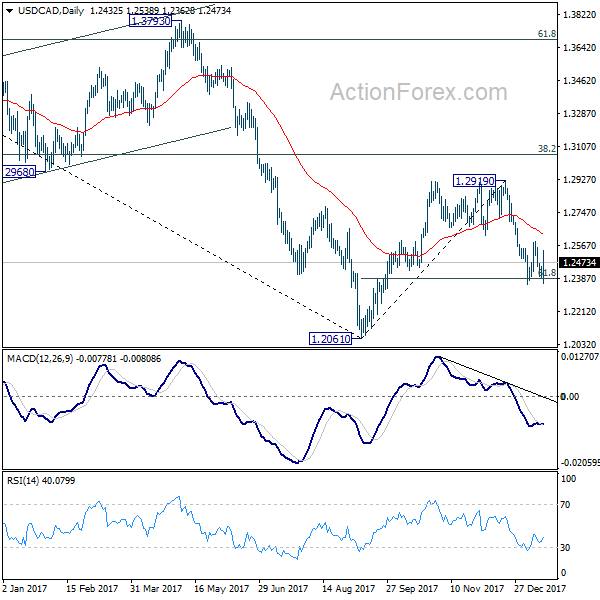

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2403; (P) 1.2428; (R1) 1.2459; More....

USD/CAD rebounds strongly ahead of 1.2354, after dovish BoC rate hike. Technically, consolidation from 1.2354 is still in progress and intraday bias remains neutral. Still, as long as 1.2623 support turned resistance holds, deeper decline is expected. Break of 1.2354 will extend the fall from 1.2910 to retest 1.2061 low. However, sustained break of 1.2623 will argue that the fall has completed and turn bias back to the upside for 1.2919 resistance.

In the bigger picture, current development argues that rebound from 1.2061 has completed at 1.2919, rejected by 55 week EMA (now at 1.2850) and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Euro Pares Gains as ECB Officials Concern On Recent Appreciation, CAD Lower after Dovish Hike

Quick update: Canadian Dollar drops notably after BoC rate decision. Markets are viewing the 25bps rate hike as a dovish one. Firstly, BoC indicated that it will be "cautious in considering future policy adjustments". Secondly, it also pointed out that "uncertainty surrounding the future of the North American Free Trade Agreement (NAFTA) is clouding the economic outlook". USD/CAD would likely extend the consolidation from 1.2354 for a while.

Euro is trading generally lower today after some ECB officials expressed concerns over its recent appreciation against Dollar. The greenback is also trying to gain some footing as the steep broad based selloff is exhausted. But for the momentum, there is no confirmation of a turnaround in Dollar yet. At least, Dollar's recovery today is overwhelmed by the strength in Aussie and Kiwi. Canadian Dollar, on the other hand, remains in tight range as traders await BoC rate decision cautiously.

After strings of strong economic data, BoC is generally expected to hike interest rate by 25bps to 1.25%. That will be the third hikes of the current tightening cycle. Some traders are cautious on the risk of a "hawkish hold" by BoC today. That is, while BoC also expects itself to raise interest rate in Q1, it could wait until March to do so. In that case, we'd probably see more range trading in USD/CAD above 1.2354. Nonetheless, we're seeing a high chance of powering through 1.2354 support should BoC delivers the rate hike.

ECB officials concerned with Euro's rise

ECB Vice President Vitor Constancio expressed concerns over Euro's "sudden movements which don't reflect changes in fundamentals. He pointed to inflation data while "declined slightly in December." He also talked down the expectation of a change in communications in the upcoming meeting on January 25, next week. Constancio said that "we see the need for a gradual adjustment of all the elements of our forward guidance if the economy continues to grow and inflation continues to move toward our goal." But, "this does not mean that changes will be immediate."Separately, Governing Council member Ewald Nowotny complained that Euro's recent appreciation is "not helpful" to the Eurozone's economy. While ECB has no exchange rate target, Nowotny said the central bank would monitor the developments.

Yesterday, Villeroy de Galhau, suggested by some as Mario Draghi's successor, warned that the recent strength in the euro could dampen inflation. As he noted, "the only question is how long it (inflation) will take to meet our target. On this issue, the recent evolution of the exchange rate is a source of uncertainty which requires monitoring with regard to its possible downward effects on imported prices". Concerning the asset purchase program, Galhau indicated that the ECB is "not pre-committed in terms of precise timing [of exit]", noting that "we will make this contingent on the actual progress made in achieving our inflation objective".

BoE Saunders upbeat on employment market

BoE MPC member Michael Saunders, a know hawk, expressed his optimism on the employment market. He forecasts unemployment rate to fall further to 4% or even lower this year. That's a better projection than BoE's, which forecasts unemployment rate to be at 4.2% by the end of 2017. Also, Saunders expects wage growth to hit 3% or higher this year. And, if the economy develops as he expects, "I consider it likely that interest rates will need to rise further over time." But he also emphasized that the tightening would be limited and gradual". And, BoE "would be gradually lifting our foot off the accelerator, with no need to put the brakes on."

Dallas Fed Kaplan: Three rate hikes the base case

Dallas Fed President Robert Kaplan said in an interview that three rate hikes will be the base case for Fed this year. He expect the economy to be strong in 2018, with support from fiscal stimulus too. And risks, to him, are skewed to the upside. That is, if he's wrong on the economy, it could heat up that makes it necessary for more than three rate hikes. Nonetheless, he still expressed some concerns on flattening and even inverted yield curve.

On the data front

Eurozone CPI was finalized at 1.4% yoy in December, core CPI at 0.9% yoy. Australia Westpac consumer confidence rose 1.8% in January, home loans rose 2.1% mom in November. Japan machine orders rose 5.7% mom in November.

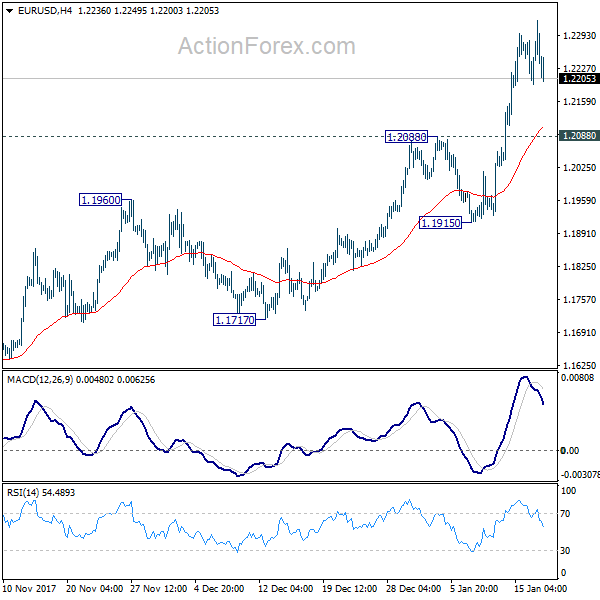

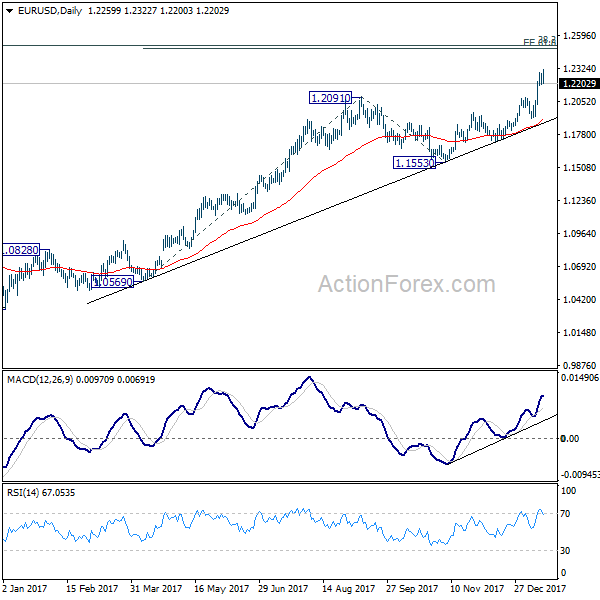

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2208; (P) 1.2246 (R1) 1.2297; More....

Intraday bias in EUR/USD remains neutral at this point and more consolidations could be seen. As long as 1.2088 resistance turned support stays intact, near term outlook remains bullish. Current medium term rally would target 1.2494/2516 key resistance zone next. At this point, we'd expect strong resistance from there to limit upside and bring reversal. On the downside, break of 1.2088 will argue that EUR/USD has topped earlier than expected. In that case, intraday bias will be turned to the downside for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Jan | 1.80% | 3.60% | ||

| 23:50 | JPY | Machine Orders M/M Nov | 5.70% | -1.20% | 5.00% | |

| 0:30 | AUD | Home Loans M/M Nov | 2.10% | 0.00% | -0.60% | |

| 10:00 | EUR | Eurozone CPI Y/Y Dec F | 1.40% | 1.40% | 1.50% | |

| 10:00 | EUR | Eurozone CPI M/M Dec | 0.40% | 0.40% | 0.10% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Dec F | 0.90% | 0.90% | 0.90% | |

| 14:15 | USD | Industrial Production M/M Dec | 0.90% | 0.40% | 0.20% | -0.10% |

| 14:15 | USD | Capacity Utilization Dec | 77.90% | 77.30% | 77.10% | 77.20% |

| 15:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | 1.00% | |

| 15:00 | USD | NAHB Housing Market Index Jan | 72 | 72 | 74 | |

| 19:00 | USD | Federal Reserve Beige Book | ||||

| 21:00 | USD | Net Long-term TIC Flows Nov | 23.2B |

SPOT GOLD Eases on Stronger Dollar; Limited Downside Expected

Spot Gold stands at the back foot on Wednesday and keeps near-term focus at Tuesday's spike low at $1331, after upside attempts in Asian session were rejected just under new four-month high at $1344.

Near-term bias is turning in negative mode as the yellow metal comes under pressure on moderately stronger dollar, with fresh bearish signals coming from overbought conditions on daily chart.

However, corrective action is expected to be shallow and likely to be contained by ascending 10SMA (currently at $1326) before underlying bulls signal continuation of steep uptrend from $1236 (12 Dec low) for final push towards target and key med-term barrier at $1357 (08 Sep peak).

Alternatively, loss of 10SMA handle would signal deeper pullback and risk extension towards key near-term support at $1308 (10 Jan trough).

Res: 1344; 1350; 1352; 1357;

Sup: 1333; 1331; 1326; 1322