Sample Category Title

USD Rebounds But Investors Question If The Dollar Can Hold On To The Gains

The U.S. dollar posted a strong rebound yesterday. Lack of economic data from the U.S. saw investors focusing on the broader macro themes. News about Apple Inc's announcement about repatriating billions of dollars in overseas cash saw the markets react bullishly on the news.

On the economic front, the Eurozone inflation report showed that final inflation figures for December were confirmed at 1.4% on the headline and 0.9% on the core. The Bank of Canada hiked interest rates for the third time yesterday since last year bringing the overnight cash rate to 1.25%. However, the Canadian dollar was seen falling as BoC's Poloz cited concerns about the NAFTA deal and the impact on the Canadian economy.

Looking ahead, China's GDP data is on the tap today. Economists forecast a 0.6% increase in the economy on the quarter. In the U.S. trading session, the building permits data will be coming out followed by the U.S. crude oil inventories report.

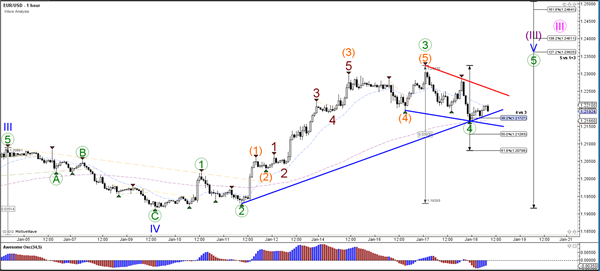

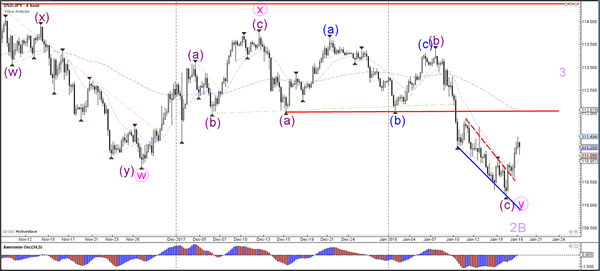

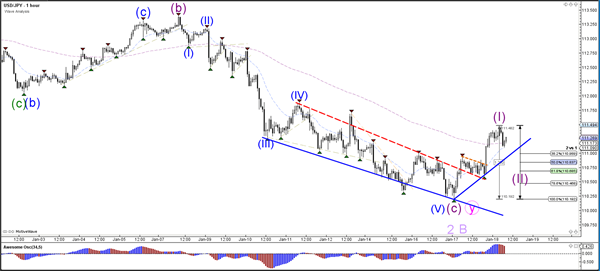

Daily Wave Analysis: EUR/USD, GBP/USD Retracements Testing Fibonacci Support Levels

Currency pair EUR/USD

The EUR/USD is building a bearish retracement at the moment but price is most likely still part of a larger wave 3 (purple) unless price breaks the support trend lines and Fibonacci levels on the 1 chart.

The EUR/USD is testing the support trend lines and Fibonacci levels of wave 4 (green). A bullish bounce and breakout above the resistance trend line (red) could spark a larger uptrend continuation towards the Fibonacci targets of wave 5. A bearish break could indicate that a different wave count is valid although the 50% Fibonacci level of wave 4 remains a strong zone.

Currency pair GBP/USD

The GBP/USD broke abovethe orange horizontal line which indicates the bottom of wave 1 on a weekly chart and indicates a new wave count for the long-term (see weekly wave analysis next Monday for the newest update).

The GBP/USD price action is looking strongly bearish at the moment but the Fibonacci levels of wave 4 (green) remain potential bouncing spots.

Currency pair USD/JPY

The USD/JPY is indeed breaking through the resistance trend line (dotted red) and resistance fractal with strong bullish candles. The bullish breakout could retest the broken bottom (red) and long-term moving average.

The USD/JPY is probably in a wave 1 (purple) at the moment. If price does make a bearish retracement by breaking below the support trend line (blue), then price will probably build a retracement within wave 2 (purple).

Bank Of Canada Rate Hike Expected Today

The BOC is expected to deliver an Interest rate hike of 25bps today as it seeks to catch up with an economy that is flying high. BOC’s Governor Poloz will deliver his decision and Press Conference, where he will outline the factors involved in making the decision. Chief among them will be the broad underlying wage growth and strong price dynamics of the economy, coupled with excesses in the financial system. The Governor down-played NAFTA concerns in his December speech but as the Trade negotiations are on-going this week, they will remain a concern for the economy unless a positive resolution can be found. With this in mind, a somewhat dovish speech is expected today to balance strong economic performance with ongoing uncertainties, maintaining flexibility for future policy decisions. We await the BOC decision at 15:00 GMT.

German Harmonised Index of Consumer Prices (YoY) (Dec) was released unchanged at 1.6%, as expected. Wholesale Price Index (MoM) (Dec) was -0.3% v an expected 0.3%, from 0.5% previously. Wholesale Price Index (YoY) (Dec) was 1.8% v 3.3% previously. EURUSD sold off from 1.22676 to 1.22157.

UK Consumer Price Index (YoY) (Dec) was 3.0%, as expected, from 3.1% previously. Core Consumer Price Index (YoY) (Dec) was 2.5% v an expected 2.6%, from 2.7% prior. Consumer Price Index (MoM) (Dec) came in as expected at 0.4%, from 0.3% prior. Producer Price Index – Output (MoM) n.s.a. (Dec) was 0.4% v an expected 0.3%, from 0.3% previously, which was revised up to 0.4%. Producer Price Index – Output (YoY) n.s.a. (Dec) was 3.3% v an expected 2.9%, from 3.0% previously, which was revised up to 3.1%. Producer Price Index – Input (MoM) n.s.a. (Dec) was 0.1% v an expected 0.4%, from 1.8% previously, which was revised down to 1.6%. Producer Price Index – Input (YoY) n.s.a. (Dec) was 4.9% v an expected 5.4%, from 7.3% previously. PPI Core Output (MoM) n.s.a. (Dec) was 0.3% v an expected 0.2%, from 0.2% previously. PPI Core Output (YoY) n.s.a. (Dec) was 2.5% v an expected 2.3%, from 2.2% previously. GBPUSD sold off from 1.37826 to 1.37416 after the data release.

Australian Westpac Consumer Confidence (Jan) was released, coming in at 1.8%. The previous reading was 3.6%. This release sent the AUDUSD pair higher from 0.79636 to 0.79737.

Japanese Machinery Orders (YoY) (Nov) was released at 4.1% with a consensus of -0.7% expected, from 2.3% prior. Machinery Orders (MoM) (Nov) was released at 5.7% with a consensus of -1.4% expected, from 5.0% previously. USDJPY moved higher from 110.288 to test 110.427 after this data release.

Australian Home Loans was released at 2.1% v a consensus of -0.2%, from -0.6% previously. Investment Lending for Homes (Nov) was 1.5% from 1.6% prior. AUDUSD stepped higher to test 0.79990.

Chinese FDI – Foreign Direct Investment (YTD) (YoY) (Dec) was 7.9% from 9.8% previously.

EURUSD is down -0.26% overnight, trading around 1.22280.

USDJPY is up 0.35% in early session trading at around 110.833.

GBPUSD is down -0.15% to trade around 1.37701.

USDCAD is up 0.20%, trading around 1.24595.

Gold is down -0.34% in early morning trading at around $1,333.65.

WTI is down -0.17% this morning, trading around $63.72.

Major data releases for today:

At 10:00 GMT, Eurozone Consumer Price Index – Core (YoY) (Dec) will be released. The consensus is for an unchanged value of 1.1%. Consumer Price Index (MoM) (Dec) is expected to be 0.4% from 0.1% previously. Consumer Price Index (YoY) (Dec) is expected to be unchanged at 1.4%. Consumer Price Index – Core (MoM) (Dec) is expected at 0.2% from -0.1% prior. EUR pairs could see volatility pick up due to this data.

At 11:45 GMT, UK MPC Member Saunders is due to speak at the Financial Intermediary and Broker Association inaugural conference in London. GBP crosses could be moved by the comments made during this time.

At 14:15 GMT, US Industrial Production (MoM) (Dec) will be released. The consensus is for 0.4% from 0.2% previously. Capacity Utilization (Dec) is also released at this time with an expectation for 77.3% v 77.1% prior. USD crosses can be impacted.

At 15:00 GMT, US NAHB Housing Market Index (Jan) will be released with an expected reading of 72. The previous reading was 74. This release may affect USD pairs.

At 15:00, Bank of Canada Rate Statement will be made public. The Monetary Policy Report will be released and the Interest Rate Decision is expected to be 1.25% from 1.00% previously.

At 16:15, Bank of Canada Press Conference based on the decisions made earlier at 15:00 GMT.

At 19:00, US Fed’s Beige Book compiles anecdotal evidence from 12 Federal Reserve Banks regarding their local economic conditions.

At 20:15, US FOMC Member Mester will speak about Monetary Policy Communication at Rutgers University in New Jersey. Comments during the speech and during the following Q&A session afterwards could move USD pairs.

At 23:50, Japanese Foreign Investment in Japanese Stocks (Jan 12) will be released, with a prior reading of ¥597.9B. Foreign Bond Investment (Jan 12) will also be released at this time, with a previous reading of ¥173B.

Currencies: Dollar Bottoms, But Technical Confirmation Is Still Needed

Sunrise Market Commentary

- Rates: US reflationary spirits back alive

Surging US stock markets, hawkish comments by Fed Mester and a very robust Beige Book revived reflationary spirits and caused an underperformance of US Treasuries. The US 5-yr yield is near key resistance at 2.42% (2011 top). The Bund could continue to outperform as ECB members downplay speculation on communication changes at next week's meeting. - Currencies: Dollar bottoms, but technical confirmation is still needed

The dollar finally rebounded yesterday. The US currency received additional interest rate support, as risk sentiment improved and as the Beige Book sounded positive on the economy. ECB governors continue to show their unease with the recent sharp euro rally. In this respect, we keep a close eye on comments from the ECB Coeure today.

The Sunrise Headlines

- US stock markets eked out impressive gains yesterday (+1%), lifted by Apple's announcement to repatriate cash and invest in the US economy. Asian stock markets started well, but grind lower with Japan underperforming (-0.5%).

- White House Chief of Staff Kelly said that Republican leaders have the votes to avert a government shutdown and push through a stopgap measure until Feb 26.

- Australian employment jumped past expectations to match the longest run of monthly gains on record, yet unemployment still edged up as more people looked for work putting an unwelcome brake on wages and inflation.

- The White House has “zero anxiety” about the prospect of former senior adviser Steve Bannon testifying to the special counsel overseeing the Russia investigation, an administration official.

- Economic activity across the US expanded into 2018, with tight labor markets and modest wage and price growth, according to the Fed's Beige Book.

- Apple has pledged to invest more than $30bn to expand its American operations in the wake of last month's US tax cut, even as it makes an estimated $38bn one-off tax payment on the repatriation of its overseas profits.

- Today's eco calendar heats up in the US with housing starts, building permits, Philly Fed Business outlook and weekly jobless claims.

Currencies: Dollar Bottoms, But Technical Confirmation Is Still Needed

Dollar looking for a bottom?

The EUR/USD rally was a bit exhausted yesterday after setting a new correction top in Asia. ECB members Constancio and Nowotny warned that a sudden rise of the euro complicates the ECB's effort to bring inflation back to target. EUR/USD tested the 1.22 mark early in US trading. The 2-yr US/GE yield spread rose to a cycle top of over 2.60 %. EUR/USD closed the session at 1.2186. USD/JPY finished at 111.29.

Asian equities opened strong overnight, but struggle to maintain the early gains. The dollar is holding most of yesterday's gains on higher US yields. The Japan 10-yr yield nears the 0.10% mark, blocking a further decline of the yen. USD/JPY holds in the low 111 area. The EUR/USD decline also slows. EUR/USD hovers near 1.22. The Aussie dollar fails to profit from strong November/December job growth. An overnight attempt to clear AUD/USD 0.80 failed.

US housing starts and permits are forecast to ease slightly. The Philly Fed business outlook is also expected slightly softer from 27.9 to 25.0. Activity data are not the focus of markets these days. So, any market reaction to these data will probably only be of intraday significance. Yesterday, the dollar finally rebounded. Equities, Fed comments and the Beige book were supportive, but there is no guarantee but there is no guarantee that this is enough to trigger a sustained bigger correction already at this stage. We keep a close eye at an appearance from ECB's Coeure. Will he also warn on the impact of a too fast rise of the euro?

Global Picture: The dollar was in the defensive of late as markets prepare for a change in policy from central banks outside the US, especially from the ECB. This propelled EUR/USD despite a huge interest rate differential in favour of the dollar. Yesterday, the dollar decline finally showed tentative signs of bottoming, but the jury is still out. A return below previous resistance at 1.2092 is needed to call off the ST alert for the dollar. EUR/USD 1.2598 (62% Retracement) is next important resistance on the charts.

EUR/GBP lost substantial ground yesterday even as there were few UK eco data. The EUR/USD decline was an important factor. This morning, UK RICS house prices were better than expected. There are no other UK data today. The day-to-day momentum of sterling improves, but we hold the view that 0.8760/00 is a strong support area ST

EUR/USD rally slows, but technical confirmation still needed

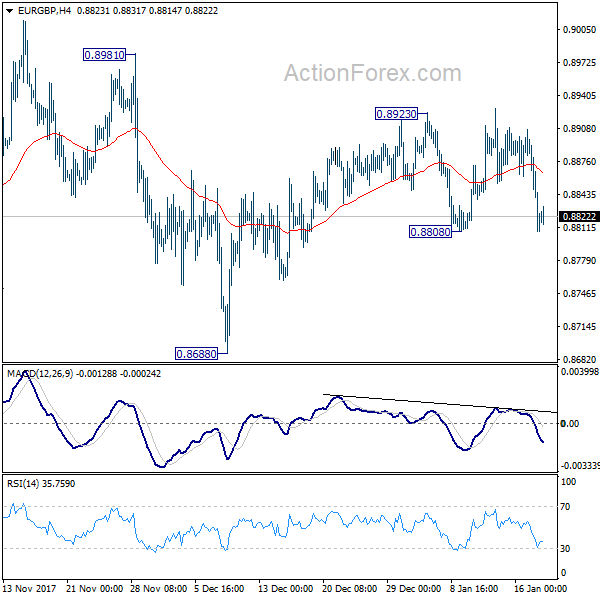

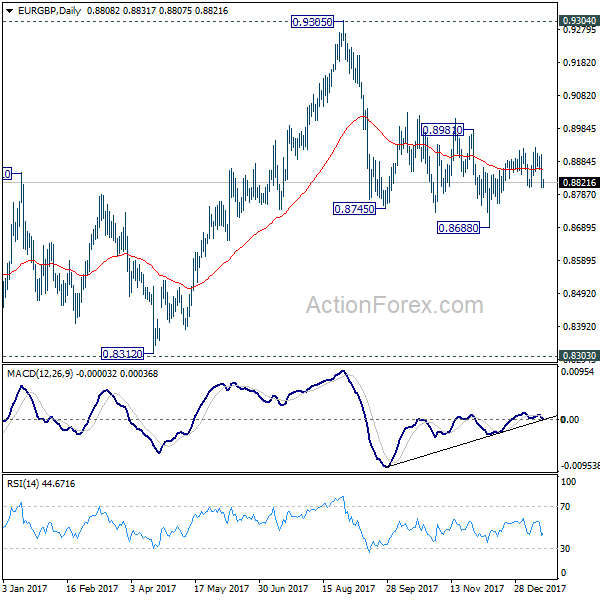

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8777; (P) 0.8842; (R1) 0.8875; More...

No change in EUR/GBP's outlook. Despite the rally attempt, upside momentum remains unconvincing. Break of 0.8981 resistance is needed to indicate completion of the decline from 0.9305. Otherwise, another fall would be mildly in favor. Below 0.8808 support will turn bias to the downside for 0.8688 support first.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

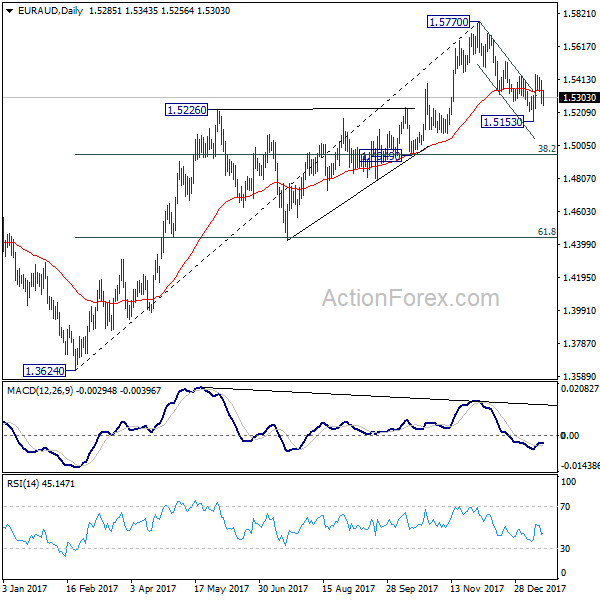

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5231; (P) 1.5320; (R1) 1.5372; More....

Intraday bias in EUR/AUD is neutral for consolidation below 1.5446. At this point, we're mildly favoring the case that pull back from 1.5770 has completed at 1.5153 already. Above 1.5446 will target a test on 1.5770 high. However, break of 1.5153 will resume the fall from 1.5770 to 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950).

In the bigger picture, decline from 1.5770 just breached 1.5226 key support briefly and recovered. The development is reviving the bullish case that rise from 1.3624 is still in progress. But considering bearish divergence condition in daily MACD, we'd prefer to see firm break of 1.5770 resistance to confirm. On the downside, sustained trading below 55 week EMA (now at 1.4950) will likely bring retest of 1.3624 support. Overall, there is still prospect of another medium term rally as long as 61.8% retracement of 1.1602 to 1.6587 at 1.3506 holds.

Cryptocurrencies Fall: Opportunity Or Dead End?

The dramatic plunge in Bitcoin and other cryptocurrencies over the past two days erased almost $300 billion dollars in total market cap. Investors who bought Bitcoin around its peak of $20,000 would have suffered the most as the price fell below $10,000 on Wednesday. It is even more painful for people who decided to borrow money and buy the digital currency, fearing that they would miss the greatest opportunity ever in financial markets.

South Korea and China regulators were the ones to be blamed after they signaled plans to crack down on cryptocurrency trading. In 2017 cryptocurrencies were resilient to such news, particularly after China decided to shut down exchanges dealing with digital currencies in September. Back then, the bitcoin price plunged more than 30% from $4,900 to below $2,900. Three months later, it managed to march towards $20,000, suggesting that such actions attracted more investors. Given that traders and investors may always find a way to circumvent local restrictions, in theory, restrictions should have alimited impact in the longer run. However, when the fight becomes global against cryptocurrencies, this should become a serious warning signal.

Finding a fair value in cryptocurrencies is an impossible mission, as animal spirits will remain the key driver. Most people who were buying bitcoin and other cryptocurrencies most recently, are not using them for transactions, but holding them in the expectation of profiting from the endless rising price. Whether the animal spirits have already released their grip, remains to be seen and this cannot be ascertained from a two-day slump.

Brick and mortar stores have been very slow to accept cryptocurrencies as a method of payment. This is what worries me most. If we don’t see growth in their acceptance as payment method, then it is not serving its true purpose.

Market Update – Asian Session: Equities Higher Tracking US Moves

Headlines/Economic Data

General Trend:

Asian markets generally track US gains

Strength in chip-related companies after S&P500 Tech index outperformed on Wed: Taiwan Semi +2.4%, Tokyo Electron +4%, SUMCO Corp +3%

Australian Dollar and bond yields pare gains: Dec Employment Change, unemployment rate and participation rate all higher than expected

BHP Q2 iron ore production in line

Awaiting China Q4 GDP data, there was a report citing NDRC official, that CHINA 2017 GDP: 6.9% V 6.8%E

Japan

Nikkei 225 opened +0.9; closed -0.4%

(JP) Japan's Topix passes 1,900 for the first time since 1991

Nintendo [7974.JP] +3% (Confirms the launch of Nintendo Labo on April 20th)

(JP) Japan Cabinet: Rising land prices helped Japan's national wealth rebound in 2016 to its highest level in over 15 years, reaching 3.35 quadrillion yen – Nikkei

(JP) Japan investors net bought ¥953.5B in foreign bonds v bought ¥186.6B in prior week; Foreign investors net bought ¥498.7B in Japan stocks v bought ¥598.7B in prior week

(JP) Some at BOJ are said to see need for future normalization talks, see the market getting ahead of itself and agree that current stimulus needed for now – financial press

(JP) Japan MoF sells ¥800B v ¥800B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.832% v 0.848% prior; Bid to cover: 3.77x v 4.38x prior

(JP) JAPAN NOV FINAL INDUSTRIAL PRODUCTION M/M: 0.5% V 0.6% PRELIM; Y/Y: 3.6% V 3.7% PRELIM; Capacity Utilization m/m: 0.0% v 0.2% prior

Korea

Kospi opened +0.5%

(KR) South Korea to check source of funds for cryptocurrency trading - Korean press

(KR) South Korea regulator: Still considering shutting down all virtual currency exchanges; will make a decision soon on cryptocurrency regulation

(KR) BANK OF KOREA (BOK) LEAVES 7-DAY REPO RATE UNCHANGED AT 1.50%; AS EXPECTED

(KR) Bank of Korea (BOK) gives 2019 outlook: GDP at 2.9%; CPI 2.0%

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

Hang Seng Consumer Goods Index -0.7%: Automakers trade generally lower (China to further cut new energy auto subsidies in 2018 – China Daily)

Ping An Insurance [2318.HK] +1.3% (Planning to spinoff 4 units to raise HK$62.4B – HK Press)

CITIC Telecom [1883.HK]: +4.5% (Said to consider increase in final dividend payout - HK Press)

Luk Fook, 590.HK Reports Q3 SSS +1% y/y ; shares down ~10%

(CN) China said to be promoting encryption techniques to go “all domestic” to insure financial security while paving the way to introduce the nation’s own digital fiat currency – CD

(CN) China said to reduce spending through certain bank accounts - press

USD/CNY (CN) PBoC sets yuan reference rate at 6.4401 v 6.4335 prior

(CN) China PBoC OMO: Injects CNY160B in 7,14 and 63-day reverse repos v CNY200B prior; Net injects CNY90B v CNY100B prior

(CN) CHINA NOV PROPERTY PRICES M/M: RISES IN 57 OUT OF 70 CITIES V 50 PRIOR; Y/Y RISES IN 61 OUT OF 70 CITIES V 59 PRIOR

(CN) China Dec Net FX Settlement (CNY-terms): +44.5B v -31.2B prior

(CN) China FX regulator SAFE: 2017 cross border capital flows improved; FX market demand and supply were basically balanced

(CN) China MOFCOM: To support auto related consumption in 2018; 2017 new-energy auto sales +53.3% y/y

HNA unit Bohai Capital: said HNA Capital (parent company) used 2.14B shares as collateral

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.2%

ASX 200 Financials Index +0.4%; Energy Index -1.3%

Woodside Petroleum [WPL.AU] -1.3% (Q4 production and revenues declined y/y)

(AU) AUSTRALIA DEC EMPLOYMENT CHANGE: +34.7K V +15.0KE (15th consecutive monthly gain); UNEMPLOYMENT RATE: 5.5% V 5.4%E

(AU) Australia Dec RBA Govt FX Transactions (A$): -1.36B v -457M prior

BHP [BHP.AU]: Pares gains following Q4 production update: Reports Q2 Iron Ore production 62Mt v 62Mte; Affirmed FY18 iron ore, copper production forecasts, cut metallurgical coal production forecast

Newcrest Mining [NCM.AU] -1.5% (tracks decline in gold prices)

North America

US equity markets ended higher: Dow +1.3%, Nasdaq +1%, S&P500 +0.9%, Russell 2000 +0.9%

S&P500 Technology Sector +1.5%, Consumer Staples +1.1%

Alcoa -5% afterhours: Reports Q4 $1.04 v $1.23e, Rev $3.17B v $3.29Be

(US) Pres Trump: Any changes in China's purchases of US Treasuries wouldn't hurt US economy; everybody wants to buy Treasuries

(US) White House Chief of Staff Kelly: Believes Congress will pass stopgap bill; GOP leaders have votes to avert government shutdown - US Media Interview

(US) Fed's Kaplan (moderate, non-voter): three rate rises in 2018 is unlikely to invert the yield curve - Q&A with press

(US) Fed's Mester (voter, hawk): US has returned to normal and policy is normalizing

(US) Sen Banking Committee approves Fed Chair nominee Powell, Fed board nominee Quarles (as expected); votes now move to full Senate - press

(US) NOV TOTAL NET TIC FLOWS: $33.8B V $152.9B PRIOR; NET LONG-TERM TIC FLOWS: $57.5B V $26.2B PRIOR; China Total holding of US Treasuries: $1.18T v $1.19T prior

(CA) BANK OF CANADA (BOC) RAISES INTEREST RATE DECISION BY 25BPS TO 1.25%; AS EXPECTED

(US) Weekly API Oil Inventories: Crude: -5.1M v -11.2M prior

Looking Ahead: US weekly DOE Crude Oil Inventories due to be released

Corporate earnings are expected from companies including American Express, Bank of NY, IBM, Morgan Stanley

Europe

(UK) House of Commons approves the EU Withdrawal Bill (as expected); Vote was 324 to 295

(IE) Ireland Brexit negotiator Montgomery: freedom of movement is remarkably important; Not a significant chance for second Brexit vote - Dublin speech

(UK) DEC RICS HOUSE PRICE BALANCE: +8% V -1%E

(IT) Bank of Italy says meetings with ECB's Nouy on lenders constructive

Carrefour: Reports Q4 Rev €23.3B, +2.3% y/y; Free cash flow in full-year 2017, excluding exceptional items, should stand around €950m vs. €1,039m in 2016. Capital expenditure in the full year should stand at €2,145mn ex Carg

Levels as of 01:00ET

Nikkei225 -0.4%, Hang Seng -0.0%; Shanghai Composite +0.5%; ASX200 -0.0%, Kospi +0.1%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.2%, Dax -0.1%; FTSE100 -0.1%

EUR 1.2207-1.2166; JPY 111.48-111.15; AUD 0.7996-0.7942;NZD 0.7292-0.7246

Feb Gold -0.9% at $1,327/oz; Feb Crude Oil +0.2% at $64.12/brl; Mar Copper +0.3% at $3.20/lb

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.58; (P) 153.43; (R1) 154.73; More...

Break of 153.66 resistance indicates resumption of medium term up trend. Intraday bias in GBP/JPY is turned back to the upside. Next target is 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. Break will target 100% projection at 160.49. On the downside, below 153.08 minor support will turn intraday bias neutral again. But outlook will stay bullish as long as 150.18 support holds.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

In Norway, Norges Bank’s Lending Survey Is Released

Market movers today

With no major euro area data releases on the calendar, today's highlight will be speeches by Bundesbank President Jens Weidmann and ECB's Benoit Coeuré at a conference on economic policy debates in Germany. With recent ECB at tempts to talk down the EUR over the last days markets will look out for any hints regarding future ECB monetary policy.

In the US, the Philly Fed index for January is released. Consensus is for a decline to 24.0, in line with the observed drop in the earlier released Empire manufacturing index, but despite a possible moderation the index remains at a high level.

This morning we will also get a bunch of data out of China including GDP data, retail sales, industrial product ion and fixed asset investments. Markets will digest these data for any indications of to what extent strong global export demand has cushioned the lower support from construction and infrastructure spending amid the housing market losing steam.

In Norway, Norges Bank's lending survey is released. If banks signal further tightening of their credit practices this could fuel uncertainty as to the out look for private consumption and investments. Meanwhile, we have not had a sniff of any plans in this direction and it seems unlikely with the housing market now beginning to show signs of stabilisation.

Selected market news

Overnight most Asian equity indices have followed US counterparts higher amid earnings and growth optimism. The USD has erased yesterday's losses amid US treasuries continuing to selloff. We at tribute the latest move higher in US yields to US treasury data showing declining foreign holdings and on further US companies committing to plans of repatriating foreign earnings suggesting a lower future treasuries demand (see below).

Also, developments in the US suggest the US as expected will avoid an imminent government shutdown as the Republican leaders seemingly have found sufficient votes for a plan to temporarily fund the government for an additional four weeks up until 16 February. Given the slim 51-49 republican majority in the Senate, the deal needs democrat votes to reach the 60-vote threshold needed to advance the spending legislation pushed forward by the House Republicans. Current government funding will expire by the end of tomorrow.

Yesterday Apple Inc. – the US company with the largest offshore cash reserve – announced that it plans to pay USD 38bn in repatriation taxes from foreign earnings. The announcement follows similar statements from a range of US peers that over the last days have stated they plan to raise US investments, increase US labour force pay and increase dividends/share buy backs via foreign earnings thereby utilising the tax discount brought forward in the US tax reform. Given the tax rate (15.5% on cash, 8% on less liquid asset ) and the latest fiscal reporting, the announcement suggest Apple is repatriating the majority of its foreign earnings. Market analysts estimate USD3.1 tn is held offshore by US companies. For more info see Financial Times.

In line with market pricing and analyst expectations Bank of Canada yesterday delivered the third 25bp interest rate hike since July. Meanwhile, the monetary policy report was to the soft side, not least emphasising the future of NAFTA as a key uncertainty for the rate out look.