Sample Category Title

NZDUSD Maintains Bullish Bias Near 4-Month High

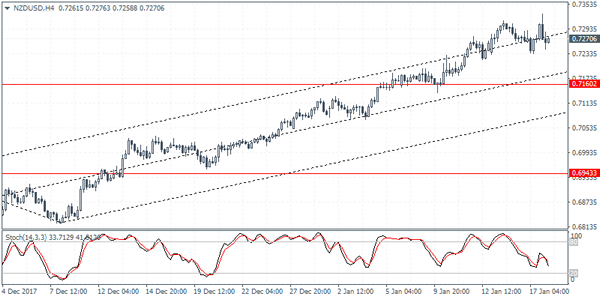

NZDUSD is hovering at 4-month highs close to the key 0.7300 level. After extending a rally to 0.7330 on Wednesday, the market took a breather and is consolidating gains. The uptrend from December remains intact and NZDUSD maintains a bullish bias, with scope for another leg higher.

NZDUSD is currently testing the 0.7300 level and focus is on the upside for a re-test of Wednesday’s high of 0.7330. A break from here could confirm that another leg up is underway with scope to reach the next handle at 0.7400.

Failure to make a sustained move above 0.7300 in the near term could see prices drift to the downside to minor support at the 50-period moving average and yesterday’s low of 0.7234. A drop below 0.7200 would suggest a short-term top is in place at 0.7330 and the bias would shift to a more bearish one.

Overall, the bullish outlook remains in place with the market’s focus on re-testing Wednesday’s high of 0.7330. Looking at the 4-hour chart, the moving averages (50 SMA and 200 SMA) are bullishly aligned and rising. The RSI is above 50. However, overbought conditions on the daily chart (RSI above 70) suggest that NZDUSD could pause at current levels for now.

Loonie Undecided After Rate Hike While Dollar Rebounds

Here are the latest developments in global markets:

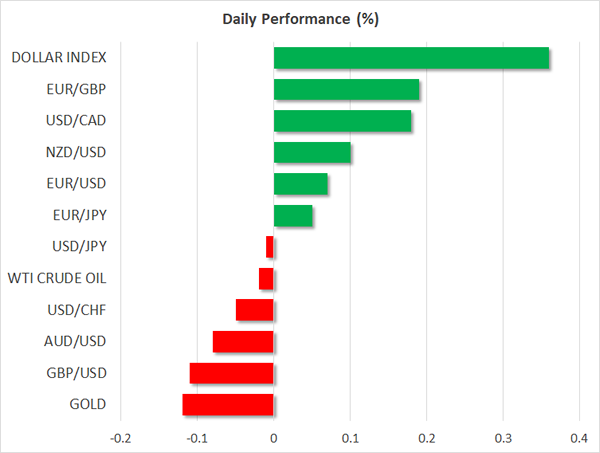

FOREX: The US dollar index continued to recover on Thursday, trading nearly 0.4% higher and extending the gains it posted on Wednesday on the back of rising US treasury yields.

STOCKS: Asian markets were mixed. Japan’s Nikkei 225 and Topix indices fell by 0.4% and 0.7% respectively, while Hong Kong’s Hang Seng index was up 0.4%. In Europe, futures tracking the Euro Stoxx 50 are in positive territory, suggesting the index could open higher. Over in the US, the three major equity indices – the Dow Jones, S&P 500 and Nasdaq Composite – all closed in the green. Specifically, the Dow advanced an astonishing 1.25% and closed above the milestone of 26000, at a fresh record high. Meanwhile, the S&P and Nasdaq closed just shy of their all-time highs. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently in the green, albeit marginally.

COMMODITIES: In energy markets, both WTI and Brent crude prices drifted slightly lower during the Asian session Thursday. Despite pulling back somewhat, WTI and Brent are still hovering near multi-year highs, supported by a broadly weak US dollar despite the rise over the last couple of days, declining US inventories, risks of supply disruptions in Nigeria, and expectations that major oil producers could extend their current output-cut deal again. In this respect, Russian Energy minister Alexander Novak said yesterday that the oil market is not balanced yet, helping to calm the nerves of those speculating that the OPEC-led supply cuts may be unwound this year. In precious metals, gold edged 0.1% lower, after declining yesterday as well.

Major movers: BoC hikes rates; dollar rises alongside yields; ECB 'jawbones' the euro

The Bank of Canada (BoC) hiked its benchmark interest rate by a quarter point yesterday to 1.25%, as was widely anticipated. The accompanying statement maintained a relatively cautious tone on further rate hikes, indicating that NAFTA uncertainties are 'weighing increasingly' on the outlook and that even though wages have picked up, they are rising by less than would be typical in this environment. The key message from the BoC was that despite hiking now, any future rate adjustments will likely depend on the evolution of incoming data and how the NAFTA negotiations play out. Interestingly enough, market pricing continues to suggest the Bank will hike two more times this year, with the next rate increase being fully priced in by May, according to Canada’s overnight index swaps. The loonie plunged initially on the decision as this was interpreted as a 'dovish hike', but recovered its losses almost instantly to trade more or less unchanged against the dollar in the following hours.

The dollar index – which measures the greenback’s performance against a basket of six major currencies- was up nearly 0.4% today, extending the gains it posted on Wednesday. With no clear fundamental catalyst behind the dollar’s recovery, the move is being attributed to the spike higher in US Treasury yields yesterday. Higher bond yields are usually positive for a currency, as bonds become more attractive to hold for investors seeking a higher return.

Elsewhere, sterling surged yesterday amid heightened optimism that the EU and the UK will agree on a transitional Brexit deal soon, perhaps by the end of the month.

Meanwhile, the euro tumbled somewhat on Wednesday, after key ECB members voiced their discomfort with the currency’s recent appreciation. ECB Vice President Vitor Constancio said that he is concerned about sudden exchange rate movements which do not reflect fundamentals, while Governing Council member Ewald Nowotny noted that a strengthening euro is 'not helpful'. These remarks may have served as a reminder that the ECB is unlikely to sit idle and allow the euro to appreciate rapidly, as that could make it more difficult for inflation to return to its target in a sustainable manner.

Day ahead: US data on housing & jobless claims as earnings season continues

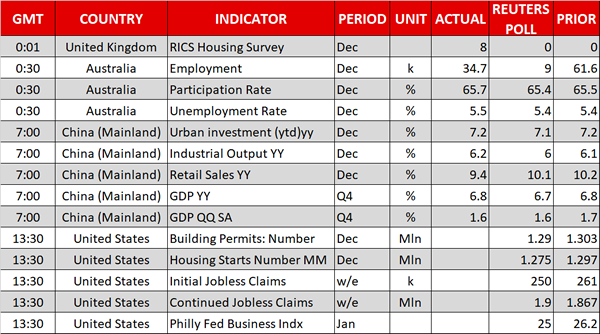

Some releases out of the US could spur positioning on the dollar during Thursday’s trading: the number of housing starts and building permits for the month of December will be made public at 1330 GMT; in November they stood at a more than a decade high and it will be interesting to see if momentum is maintained. It should be said that weather conditions in the US in late 2017 are expected to have played a role, weighing on the number of housing starts. At the same time, weekly data on initial and continued jobless claims will be released. Individuals applying for unemployment benefits for the first time are expected to fall to 250k from the previous week’s 261k which was a more than a three-month high and marked the fourth consecutive week of rises; though the number was still below the 300k mark that is linked to a robust jobs market. The Philly Fed’s Business index is also scheduled for release at 1330 GMT.

Canada will see the release of the ADP nonfarm employment change report at 1330 GMT. This is not typically a market mover though.

Cleveland Fed President Loretta Mester – an FOMC voting member in 2018 – will be speaking on monetary policy at 2305 GMT.

Oil prices could see some volatility when the Energy Information Administration releases its report including information on US crude stocks for the week ending January 12 at 1600 GMT. Crude inventories are forecast to decline by around 3.6 million barrels, registering their ninth straight weekly decline. This compares to a fall by around 4.9m barrels in the week that preceded.

In stock markets, the earnings season continues with Morgan Stanley being among US companies releasing results today.

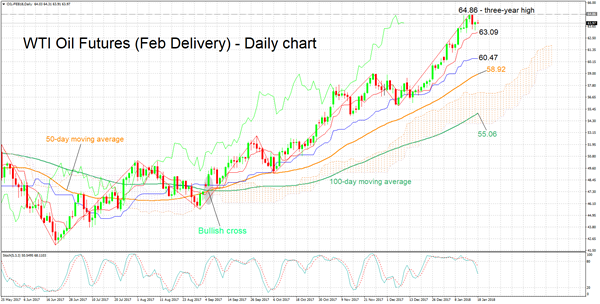

Technical Analysis: WTI oil futures trade close to 3-year highs; bearish signal by stochastics in very short-term

WTI oil futures for February delivery continue to trade not far below 64.86, the highest since late December 2014 hit on Monday. The Tenkan- and Kijun-sen lines remain positively aligned, suggesting that the bullish bias in the short-term is still in place. Notice though that the Kijun-sen has flatlined, this perhaps being an indication that positive momentum is losing steam. Also – looking at the stochastics – the %K line has crossed below the slow %D line, with both lines heading lower. This is a bearish signal in the very short-term.

Should the EIA’s report show a larger-than-forecasted drawdown in crude stockpiles, oil prices could head higher. In this case, immediate resistance could come around Monday’s high of 64.86.

On the other hand, a smaller-than-anticipated decline in crude inventories – or a rise of course – is expected to weaken prices. In this scenario, the range around the Tenkan-sen at 63.09 would be eyed as potential support.

USDJPY Struggles To Make Recovery Back Into 4-Month Range

USDJPY has made a recovery to regain the 111 handle but the pair essentially remains in a neutral phase since mid-September. Momentum oscillators have improved and could potentially lead to another leg higher.

There is immediate resistance at the 200-day moving average at 111.68. Prices need to at least rise above the 50-day MA (currently at 112.50) to see that USDJPY is moving into a more bullish phase in the near term. However, the top of the range at 114 needs to be breached soon in order to confirm that the market is shifting its underlying trend to bullish from neutral.

To the downside, the 111 level remains a key support level which if breached would place USDJPY under increased pressure and the focus would shift to the 108 area.

In the bigger picture, the market does not have any clear direction and this is indicated by the flat moving averages. USDJPY is expected to consolidate within its established 4-month range between 111 and 114. The near-term risk could tilt back to the downside unless the bulls remain in control to lift the market back above the 200-day MA.

EURO Only Intraday Bearish Below 1.2200 Level

The euro has moved back towards the 1.2200 technical level against the U.S dollar, quickly erasing Wednesday’s gains, after the pair surged earlier towards the 1.2290 level. The EURUSD pair lost ground overnight, as the U.S dollar index staged a broad-based recovery and German political uncertainty weighed on the single currency. Going forward, technical traders will be focused on the 1.2200 region and Wednesday bearish daily reversal candle, which created a lower daily price-high, providing some caution for euro buyers.

The EURUSD pair remains intraday bullish while price-action holds above the 1.2200 level, further upside towards 1.2258 and 1.2290 remains possible.

If the EURUSD pair falls below the 1.2200 level for a sustained period, further losses towards the 1.2156 and 1.2093 levels seems likely.

GBPUSD Only Intraday Bullish Above 1.3800

The British pound moved to a new 2018 price-high overnight, reaching 1.3942, marking the highest trading level for sterling since the day of Brexit. The move was sparked by a U.S dollar index sell-off, with the index plummeting back towards the 90.19 level, erasing Wednesday’s trading gains. Price-action on the GBPUSD pair currently trades around the 1.3820 region, as profit taking quickly kicked-in from overstretched level. Traders now look to the 1.3800 support level, as the U.S dollar index continues to recover heavy-losses.

The GBPUSD pair only retains a bullish bias while price-action holds above the 1.3800 level, further upside towards 1.3882 and 1.3942 remains possible.

A loss of the 1.3800 level on the GBPUSD pair, should spark a sell-off towards the 1.3755 and 1.3657 support zones.

Ripple Feeling The Burn

On Wednesday, the selloff in the cryptocurrencies market continued. Bitcoin settled below the $10,000 mark, while ethereum fell by more than 15% to end the day below the $900 mark. Ripple too fell sharply reaching a low of $0.86.

The selloff was attributed to the statements made by Kim Dong-yeon, the South Korean finance minister who said that the country was still exploring shutting down the exchanges. This was in continuation of similar reports that emerged last week.

Traders were also concerned about the news from France where a cryptocurrency sceptic was appointed to lead a taskforce on these currencies.

In total, more than $50 billion in value has been lost in the past two weeks.

Traders will pay close attention to news coming from South Korea, China, and other major countries.

After yesterday's sell-off, Ripple established a double bottom position at the 0.8677 level. It then started moving higher and is currently trading at the 23.6% retracement level of 1.4412.

XRP/USD

If the negative headlines are contained, its price may move higher with the next target being the 1.800 level. This is an important technical and psychological level.

The alternative scenario is where the selloff continues which would make the currency to test the $0.632 level.

China, US Data Headline Active Thursday Session

The economic calendar heats up on Thursday with key reports from Asia and the United States. Meanwhile, the European session will provide little in the way of market-moving events, giving investors time to shift their focus to North America.

Action begins at 07:00 GMT with a deluge of Chinese economic reports. The central government in Beijing will report on retail sales, industrial production, fixed asset investment and gross domestic product (GDP). The Chinese economy is projected to grow at an annualized rate of 6.7% in the fourth quarter, down slightly from 6.8% in Q3. Compared to the previous quarter, that amounts to 1.6% growth.

The US government will issue fresh real estate data at 13:30 GMT with a report on housing starts and building permits. Starts are forecast to decline slightly in December to a seasonally adjusted annual rate of 1.275 million units. Permits, which are a bellwether of future construction plans, are expected to fall to 1.29 million.

The Labor Department will also issue its weekly jobless claims report at 13:30 GMT. The number of Americans filing for first time unemployment benefits is expected to fall by 11,000 in the week ended 13 January to reach 250,000.

Meanwhile, the Federal Reserve Bank of Philadelphia will release the January version of its manufacturing survey at the same time as the other reports. The monthly gauge is forecast to decline slightly.

Energy traders will also be keeping an eye on the weekly crude oil inventory report courtesy of the US Energy Information Administration (EIA). Crude stockpiles are forecast to fall by nearly 3.6 million barrels in the week ended 13 January.

In currencies, the US dollar bounced back on Tuesday, rising 0.4% against a basket of world currencies. However, the greenback is down 1.4% since the start of the year, and faces more downside risk now that central banks all over the world are gradually tightening the screws on monetary policy.

EUR/USD

Europe's common currency experienced a volatile Wednesday session, as prices fell 100 pips to breach the 1.2200 handle. The EUR/USD bounced back on Thursday, climbing 0.2% to 1.2190. Immediate resistance is located at around 1.2230, with opposite side support located at 1.2120.

USD/CAD

The US dollar briefly declined below 1.2400 CAD on Wednesday after the Bank of Canada (BOC) raised interest rates for the third time since last summer. However, it would quickly rebound as investors took in an overly cautious BOC rate statement. The pair was last seen trading at 1.2451.

USD/JPY

The dollar gained ground on the yen Wednesday, with the USD/JPY climbing back above 111.00. The pair was last seen trading at 111.40, where further upside is challenged by weak dollar fundamentals.

NZDUSD Intraday Analysis

NZDUSD (0.7270): The NZDUSD was seen trading flat yesterday despite the currency pair rising to a fresh 4-month high. Forming an outside bar, the current rally in NZDUSD could be seen coming to a close. The downside correction could see NZDUSD falling back to 0.7160 in the near term. Finding support at this level could offer a temporary bounce in price. However, if the support fails, NZDUSD could slip towards the 0.6943 support level.

USDJPY Intraday Analysis

USDJPY (111.45): USDJPY posted a recovery as price action turned bullish yesterday. Closing above the 111.00 level of support, further gains could be expected if USDJPY manages to find support near 111.00 on a dip. We expect that the currency pair will target the next upside resistance at 111.61 region. The main test of resistance will be seen at 112.00 which previously served as support and was eventually breached. A break out above 112.00 could signal further gains in the medium term. However, for the moment, USDJPY could remain below the 112.00 resistance level upon successfully retesting this level.

EURUSD Intraday Analysis

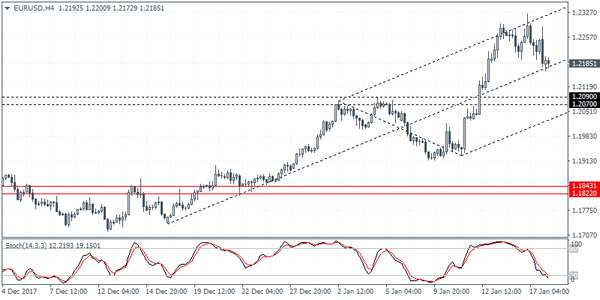

EURUSD (1.2185): The EURUSD posted strong declines yesterday as price fell to a two day low. The declines come following Tuesday's doji candlestick pattern that was formed. On the intraday charts price action is seen currently trading near the median line which could offer dynamic support in the near term. We expect to see a short term bounce following which price action could be pushing higher to form a lower high. As long as the previous highs are not breached, EURUSD is expected to reverse the gains targeting the support level at 1.2090 - 1.2070 support level.