Sample Category Title

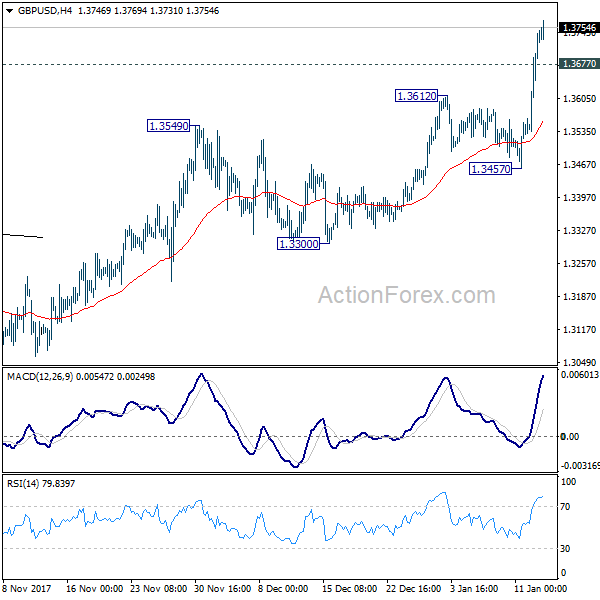

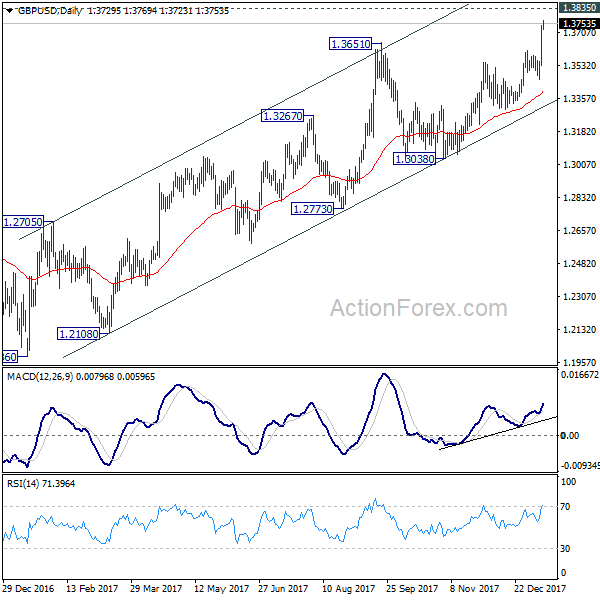

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3590; (P) 1.3666; (R1) 1.3804; More.....

GBP/USD's rally extends to as high as 1.3769 so far and intraday bias remains on the upside. At this point, we'd still expect strong resistance from 1.3835 to limit upside to complete the medium term rally from 1.1946. However, sustained break there will carry larger bullish implication and target long term fibonacci level at 1.5466. On the downside, below 1.3677 minor support will turn intraday bias neutral first. But near term outlook will remain bullish as long as 1.3457 support holds.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

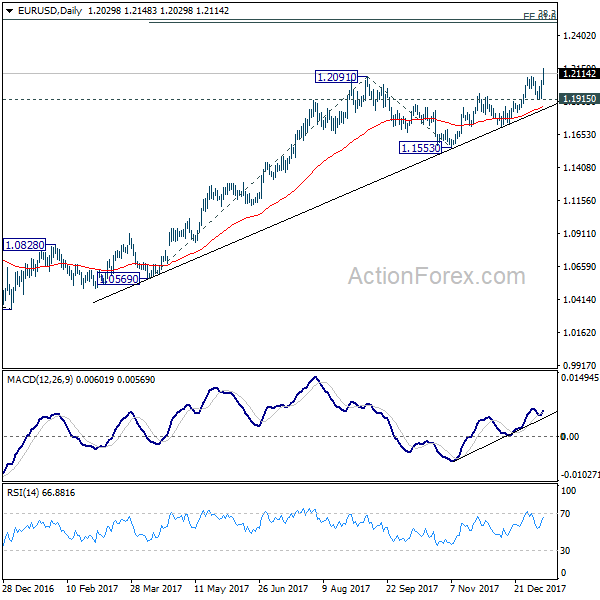

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2079; (P) 1.2149 (R1) 1.2267; More....

EUR/USD reaches as high as 1.2239 so far as recent rally extends. Intraday bias remains on the upside for 1.2494/2516 key resistance zone next. At this point, we'd continue to expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2121 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 1.1915 support holds.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Selloff Continues, BoC to Hike This Week

Dollar continues to trade as the weakest major currency as another week starts. Over the month, the greenback is trading weakest against Kiwi and Aussie. Meanwhile, Euro is catching up as Germany is closer to reforming the grand coalition. Sterling follows on improving prospects of a favorable Brexit deal. For the moment, it's unclear which is the main driving force behind Dollar's selloff. The fact that other global central banks are catching up on tightening is a factor. Surge in commodity prices is another one. But these two factors are not strong enough to send the Dollar index to three year low. The concerns of China's consideration to move away from Dollar assets could be the more important reason.

Bundesbank Weidmann: Immediate risk of hike currently low

ECB known hawk Bundesbank Jens Weidmann tried to tone down the chance of rate hike over the weekend. He expressed that "it would be particularly stressful for the banks if the long period of low interest rates were to be ended by a rapid, sharp increase in interest rates." And, "as far as central bank rates in the euro area are concerned, however, the immediate risk of change is currently low." His comments are generally in line with the view that while ECB minutes hinted on change of communications, the central bank is still far from raising interest rates. And it should be noted that various ECB officials have indicated last year that there is a sequence in stimulus exit, that is, the asset purchase program would have to stop before rate hikes.

BoC to rate hike on Wednesday despite NAFTA concerns

Bank of Canada rate decision on Wednesday will be the major focus for the week. After recent strong economic data, it's widely expected that BoC would hike again by 25bps to 1.25%. There are still concerns over the outcome of NAFTA negotiations. There is possibility of US pulling out from the decades long agreement. But it's clear that labor market slacks have diminished clearly. The Q4 business outlook survey also indicated solid hiring and investments. Hence, BoC will still likely look pass the NAFTA risks and hike again.

Other key focuses include UK inflation and retail sales, Fed's Beige Book report, Australia employment and China data. Here are some highlights for the week ahead:

- Monday: Eurozone trade balance

- Tuesday: Japan PPI; German CPI final; UK CPI, PPI; US Empire state manufacturing;

- Wednesday: Japan machine orders; Australia home loans; Eurozone CPI final; US industrial production, NAHB housing index, Fed's Beige book; BoC rate decision

- Thursday: Australia employment; China GDP, industrial production fixed asset investment, retail sales; US housing starts, jobless claims, Philly Fed survey

- Friday: New Zealand business manufacturing index; German PPI; Swiss PPI; Eurozone current account; UK retail sales; Canada manufacturing sales; US U of Michigan sentiment

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2079; (P) 1.2149 (R1) 1.2267; More....

EUR/USD reaches as high as 1.2239 so far as recent rally extends. Intraday bias remains on the upside for 1.2494/2516 key resistance zone next. At this point, we'd continue to expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2121 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 1.1915 support holds.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Dec | 3.60% | 4.00% | 4.00% | |

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.10% | 0.20% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Nov | 22.4B | 19.0B |

EURUSD Strongly Bullish Above 1.2200 Level

The euro continues to make strong gains against the U.S dollar, with the pair moving a new three-year high, hitting 1.2237 during early Asian trading. After breaking above the 1.2093 level last week, the EURUSD has gained strong bullish momentum, with the pair easily breaking above the 1.2156 and 1.2200 technical levels. Broad-based U.S dollar weakness has been the main contributing factor behind the euros early gains on Monday, with the greenback falling towards levels not seen since 2015.

The EURUSD pair remains strongly bullish while trading above the 1.2200 level, further upside towards 1.2250 and 1.2310 seems possible.

Should price-action move below the 1.2200 level, downside support for EURUSD is currently found at 1.2156 and 1.2093.

GBPUSD Strongly Bullish Above 1.3655 Level

The British pound has moved to yet another yearly price-high against the U.S dollar, climbing above the 1.3700 mark, and reaching 1.3751 during the opening trading session of the week. The move higher in the GBPUSD has been sparked by the falling value of the greenback, with the U.S dollar index sinking to its lowest trading lowest in over 3-years, touching 90.60. Going forward, the key upside levels to watch are 1.3757 and the 1.3800 on the GBPUSD pair, while the 1.3690 level becomes former resistance now turned near-term support.

The GBPUSD pair remains strongly bullish while trading above the 1.3655 technical level, key upside resistance is now found at 1.3757 and 1.3800.

Should price-action on the GBPUSD pair move below the 1.3690 level, critical daily support is now located at the 1.3655 level.

Light Release Schedule On Martin Luther King Day

The global financial markets are off to a whimper this week, as only a small trickle of economic data makes its way to investors. In the United States, traders will be on pause to observe Martin Luther King Day.

The only data release of note on Monday already happened. The Australian TD Securities inflation report showed a 0.1% increase in consumer prices last month, following a gain of 0.2% in November. This translated into year-over-year growth of 2.3% following a gain of 2.7% the previous month.

The Australian dollar rose following the release to trade at fresh three-and-a-half-month highs against the greenback.

In terms of upcoming data releases, the European Commission’s statistics agency will release the November trade balance, which provides a broad glimpse of the regional economy.

The region’s trade surplus is forecast to rise sharply to €28.2 billion in November from €18.9 billion. Germany, which is Europe’s biggest economy and largest manufacturing base, is largely responsible for regional trade.

Later in the session, investors will also have the opportunity to gauge New Zealand’s consumer-driven economy as the government reports on electronic card retail sales.

At 23:50 GMT, Japan will release the domestic corporate goods price index.

It’s important to note that the New Zealand and Japanese releases will take place on Tuesday local time.

AUD/USD

The Australian dollar reached a significant milestone on Monday, as the currency clocked in above 79 US cents for the first time in nearly four months. The improvement has coincided with a broad decline in the US dollar, which ended last week at a three-year low. The US dollar has been unable to muster any gains despite a growing likelihood of higher interest rates over the next 12 months. The AUD/USD exchange rate rose 0.5% to 0.7841, where it was trading near session highs. Investors can expect the pair to make an attempt at 0.8000 level. Along the way, the market could be rangebound.

EUR/USD

Europe’s common currency was little changed on Monday, as traders consolidated last week’s massive rally. The EUR/USD exchange rate is currently trading at 1.2200, its highest level since December 2014. The euro is being pushed higher by an improving regional economy and signs of gradual easing by the European Central Bank (ECB). The euro is now testing new frontiers, as the bulls continue to push the market higher. In the meantime, support is expected to hold near 1.2100.

GBP/USD

Like other dollar crosses, the British pound is enjoying a broad upsurge thanks to prevailing USD weakness. The GBP/USD exchange rate inched higher on Monday to trade at 1.3736. It is currently trading at its highest level since before Brexit, setting the stage for further gains.

Summary 1/15 – 1/19

Monday, Jan 15, 2018

[php_everywhere] [/php_everywhere]

Tuesday, Jan 16, 2018

[php_everywhere] [/php_everywhere]

Wednesday, Jan 17, 2018

[php_everywhere] [/php_everywhere]

Thursday, Jan 18, 2018

[php_everywhere] [/php_everywhere]

Friday, Jan 19, 2018

[php_everywhere] [/php_everywhere].

Currencies: Dollar Continues Fighting An Uphill Battle

Sunrise Market Commentary

- Rates: Consolidation after past week's sell-off?

Risk sentiment on stock markets and technical considerations will probably be today's main trading elements with US markets closed for Martin Luther King Day and amid an empty eco calendar. German yields are near key resistance levels, but a break won't be easy given this week's dull eco/event calendar. Consolidation on core bond markets can be expected. - Currencies: Dollar continues fighting an uphill battle

On Friday, the dollar extended its decline despite solid US data. Investors adapted positions as they anticipate that other major central banks, including the ECB and the BOJ, are coming closer to a less easy policy. EUR/USD cleared important technical resistance. For now, there is no trigger to stop the USD decline even as US fundamentals remains solid, too.

The Sunrise Headlines

- US stock markets closed last week's final session 0.7% higher with Dow Jones outperforming (+0.9%). Asian risk sentiment remains ebullient overnight.

- ECB Weidmann said that the immediate risk of a change in rates is currently low. It would be particularly stressful for the banks if the long period of low interest rates were to be ended by a rapid, sharp increase in interest rates.

- BoJ Governor Kuroda reiterated the central bank's resolve to maintain quantitative easing, but his positive comments on inflation and the economy sent the yen to a four-month high versus the dollar.

- Boston Fed Rosengren thinks that US inflation could pick up faster than expected. He also believes that the flatter US yield curve is a consequence of larger central bank balance sheets, rather than a signs of a coming recession.

- Germany's central bank said it will include the renminbi in its currency reserves, giving the Chinese currency's international stature a boost after 2017 saw its role in global payments diminished.

- Chancellor Merkel's preliminary coalition deal with SPD ran into opposition in Saxony-Anhalt, showing the magnitude of the task for SPD leaders to win over their reluctant party members at the January 21 party convention.

- Today's eco calendar is empty. US markets are closed for Martin Luther King Day. BoE Tenreyro is scheduled to speak

Currencies: Dollar Continues Fighting An Uphill Battle

Dollar continues fighting an uphill battle

The euro traded strong after Thursday's ECB Minutes and this trend continued on Friday. EUR/USD jumped beyond the 1.2092 cycle top after headlines on Government agreement in Germany. The US CPI and retail sales were good but didn't help the dollar. The rise of the euro/decline of the dollar resumed soon. EUR/USD cleared the 1.2167 resistance (50 % Retracement 2014 top to bottom). Soft comments from ECB's Weidemann didn't stop the rise of the euro. EUR/USD closed the session at 1.2202. The dollar remained also in the defensive against the yen, despite the continuation of record race of US equities.

Friday's trends continue overnight. Most Asian equities trade in positive territory. The yen extends gains as BOJ's Kuroda said that Japan could reach 2.0% inflation. At the same time, USD weakness persists. USD/JPY trades in the 110.75 area. EUR/USD is holding north of 1.22. Later today, the calendar is thin. US markets are closed for Martin Luther King Day and there are few data in Europe. Also later this week, the calendar contains few really important data from Europe or the US. Central bank speeches/comments, both from Fed and ECB members will be closely monitored and the earnings' season gains traction.

Euro strength prevailed last week even as US data suggest strong Q4 growth. Markets in the first place adjust positions anticipating a change in policy from major central banks outside the US, including the ECB and even the BOJ. Especially the ECB is preparing a gradual turn. Looking at the fundamentals/interest rate differentials (2-y US/German spread at +250 bps), the euro rise/dollar decline has gone quite far. However, for now there is no trigger for a change in sentiment. The technical picture turned USD negative as EUR/USD cleared 1.2090/1.2167 resistance. The dollar is a failing knife and there is no technical sign of a reversal. 1.2598 (62% Retracement) is the important resistance on the charts.

Sterling traded strong on Friday and resisted the overall euro rally. Spanish and Dutch officials advocating a soft Brexit might have been sterling supportive. EUR/GBP even closed the week at below 0.89. Cable rallied north of 1.37. Overnight, Right move house prices showed a monthly rise of 0.7%, but prices in London stay under pressure. Later this week, the UK CPI (tomorrow) and retail sales (Friday) are interesting. The day-to-day momentum might stay GBP constructive, but we expect the EUR/GBP 0.8700/60 to give solid support.

EUR/USD breaks above 1.2092/1.2167 resistance, improving the MT picture in the cross rate

Despite Expectations Of Further Tightening, Bruised Dollar Not Finding Support

Many traders have been caught by surprise by the extent of the dollar's decline over the last week. The USD index fell below 91 for the first time since January 2015, and Friday's 0.96% drop, was the second biggest since January 2017. More surprisingly, the U.S. data released over the last week certainly doesn't justify a dollar selloff. U.S. core consumer prices recorded their largest increase in 11 months in December, rising 0.3%. Retail sales for December rose 0.4%, whereas core retail sales increased 0.3% after an upwardly revised 1.4% surge in November. The two tier-one economic reports sent expectations for an interest rate hike in March to above 72% from just a 50% chance last month. This clearly suggests that internal data did not inspire the dollar selloff, but rather, external developments played a role.

Given that the Euro holds the most weight in the dollar's index, constituting about 57% of the weight, the single currency movement, spurred by political and monetary policy developments, is dictating the DXY's direction. On the political side, the coalition deal between Angela Merkel and social democrats was a great relief, after nearly four months into Germany's general election. More importantly, the shift in ECB's language is a new development sparked by hints that the Governing Council agreed to review its policy language early this year. Howeverthe hawkish comments recorded in the December minutes, were made before the release of the Eurozone inflation which slipped further away from the Central Bank's target ending the year at 1.4%. The ECB will meet in 10 days, and unless Mario Draghi finds a way to convince markets that the unwinding of stimulus will be very slow, I think the Euro will be marching towards 1.25 by end of Q1.

The Pound's performance was also outstanding after GBPUSD managed to break above the 1.3656 resistance level. Reports released on Friday that the Spanish and Dutch are willing to reach a soft Brexit deal helped to fuel the rally. The U.K. parliament will be meeting on Tuesday and Wednesday for another debate over Brexit, so a close eye should be kept on new developments.

This week, inflation figures once again will be under the spotlight in the UK and Eurozone. I think if we get any surprise on Tuesday, it will be to the downside, so the rally in both currencies may pause.

The Bank of Canada will also be under the investors' radar as the central bank is expected to hike rates by 0.25% on Wednesday. This comes despite lot of uncertainty towards the Nafta talks.

Market Update – Asian Session: China Q4 GDP Due For Release On Thursday

Headlines/Economic Data

General Trend: Equity markets trade generally higher after last week's gains in the US

Gold miners outperform (gold at 4-month high)

US dollar extends weakness seen on Friday's session

Various automakers comment at Detroit Auto Show

China PBoC offers new medium-term lending facility (MLF) as M2 growth rate hits record low in Dec

BoJ leaves bond purchases unchanged at daily operation

Japan

Nikkei 225 opened +0.7%; closed +0.3%

General strength in financials: TOPIX Securities Index +1.2%, Sumitomo Mitsui Financial +2%, Mitsubishi UFJ +1.7%

Softbank (9983.JP) +5% in early trade: Looking to list mobile phone unit this year – Nikkei; Topix Information & Communication Index +1%

(JP) Japan Dec M2 Money Stock Y/Y: 3.6% v 4.0%e (Lowest reading since Sept 2016); M3 Y/Y: 3.1% v 3.4%e

(JP) Bank of Japan (BOJ) Gov Kuroda: Economy is expanding moderately, expected to continue expanding moderately; BOJ reiterates will maintain QQE with YCC for as long as needed to reach 2% inflation in stable manner

(JP) Bank of Japan (BOJ) is likely to revise up its FY18 GDP growth forecast by 0.1-0.2% from the current estimate of 1.4% given at Jan policy meeting - Nikkei

(JP) Bank of Japan (BOJ) raises economic assessment in 3 of 9 regions; keeps economic assessment in 6 of 9 regions

Honda (7267.JP): Targeting 2018 global vehicle sales 5.4M – Nikkei

Korea

Kospi opened +0.6%

Mixed trading in chip sector: Samsung Electronics +0.6%, Hynix -2%

Automakers decline: Hyundai Motor -1.2%, Kia -1.2%

(KR) South Korea Dec Export Index m/m: -1.6% v -1.6% prior; y/y: -2.1% v +2.5% prior

(KR) South Korea Office for Govt Policy Coordination: To strongly respond to illegal cryptocurrency trading; to talk about crypto shutdown bill after full discussion

(KR) According to South Korea Financial Supervisory Service (FSS) foreigners bought KRW10T in South Korea stocks in 2017 - Korean press

(KR) South Korea and North Korea to hold working level talks on Jan 17th

China/Hong Kong

Hang Seng opened +0.9%, Shanghai Composite opened flat

Hang Seng Services Index +1.8%; Gaming names supported by broker commentary

Hang Seng Financials Index +1.2% amid PBoC MLF

Hang Seng Energy Index -1.3%, Materials -1.1%

Steel industry head comments that supply will exceed demand sent Maanshan Iron & Steel and Angang Steel lower

(CN) China Banking Regulatory Commission (CBRC) will step up oversight in the banking sector this year to reduce financial risks, stressing that long-term efforts would be needed to control banking sector chaos

(CN) China PBOC Vice Gov Yin Yong: China will remove policy barriers for cross-border payments and enhance financial infrastructural construction in foreign countries as part of efforts to further promote internationalization of the yuan - CF40 Asset Management Forum

(CN) China PBoC OMO: Injects CNY150B v CNY270B injected in 7, 14-day reverse repos prior: Net injects CNY50B v CNY180B drained prior

USD/CNY (CN) PBoC sets yuan reference rate at 6.4574 v 6.4932 prior (strongest since May 2016)

(CN) PBOC LENDS CNY398B V CNY288B PRIOR IN MEDIUM-TERM LENDING FACILITY (MLF); OFFERS 1-YEAR LOANS AT 3.25% V 3.25% PRIOR

(CN) PBoC comments on reasons for MLF operation: There has been a relatively big drop in total liquidity in banking system; Injected funds to counter liquidity drop due to tax payments, maturing loans and RRR payments by financial institutions.

China Dec Banking Data was released on Friday: (CN) CHINA DEC M2 MONEY SUPPLY Y/Y: 8.2% (record low) V 9.2%E; M1 MONEY SUPPLY Y/Y: 11.8% V 12.6%E

(CN) CHINA DEC NEW YUAN LOANS (CNY): 584.4B V 1.00TE

(CN) China Yunnan Local Government Financing Vehicle (LGFV) said to fail to repay certain trust loans - China Securities Times

Looking ahead: China Q4 GDP and Dec data (Fixed Asset Investment, Industrial Production, Retail Sales) due for release on Thursday, Dec 18th

Australia/New Zealand

ASX 200 opened +0.2%; closed %

ASX 200 Resources Index +1%, Financials +0.2%; Telecom -0.4%

(AU) Australia Dec Melbourne Institute Inflation m/m: 0.1% v 0.2% prior; y/y: 2.3% v 2.7% prior

(AU) Western Australia Chamber of Commerce and Industry WA that found consumer confidence reaches highest in four years - AFR

(NZ) New Zealand Treasury publishes Rennie report on decision making: Recommends multiple committees and external members for the RBNZ

Looking ahead: On the 16th Rio Tinto will kick off Australia with Q4 production data

Australia Dec Employment data due on Thursday, Dec 18th

Other Asia

(ID) Indonesia Dec Trade Balance: -$270M v +$579Me (1st deficit since July 2017)

(SG) Monetary Authority of Singapore (MAS) Managing Direc Menon: Inflation surprise could force global central banks to react faster than they today expect

(PH) Philippines sells total PHP20B v PHP20B indicated in 3-month, 6-month and 12-month bills

North America

Ford [F] Exec: Increasing investment into electric vehicles (EV) to $11B from $4.5B - Detroit Auto Show

(US) President Trump said to be softening his attitude toward NAFTA - financial press

Fed Speak: (US) Fed's Rosengren (moderate, non-voter): additional drop in unemployment rate risks undermining the recovery (from Jan 12th)

(US) Fed's Kashkari (dove, non-voter) tweets: "I do hope inflation is moving reliably toward our target. 12-mo core CPI of 1.8% = 1.5% PCE & our target is 2% PCE. I, for one, need to see more data." (from Jan 12th)

(US) Fed's Harker (non-voter, moderate): reiterates two rate hikes probably appropriate for 2018 (from Jan 12th)

(US) Fed's Kaplan (non voter, moderate): base case still three hikes this year – CNBC (from Jan 12th)

Looking Ahead: US equity markets closed on Monday in observance of holiday: Detroit Auto Show to be held between Jan 13th to Jan 28th

Europe

(DE) Germany Social Democrats in Saxony-Anhalt state reject proposed German coalition with Merkel's party - German press

(DE) Negotiators working on German govt coalition deal to make changes in immigration and employee insurance contributions – Handelsblatt (from Jan 12th)

EUR/CNY (DE) Germany Bundesbank's Dombret: to include Yuan in currency reserves - financial press

(EU) ECB Weidmann: Reiterates announcing an end date for QE is justifiable; complete policy normalization will be a long path (comments from Jan 12th)

IMF First Deputy Managing Dir Lipton: Upside and downside global risks are currently balanced; notes cyclical global recovery.

(UK) Boris Johnson said to have warned allies that Brexit is far from certain - UK press

(UK) Jan Rightmove House Prices m/m: +0.7% v -2.3% prior; y/y: 1.1% v 1.0% prior

Carillion: Could enter administration as soon as Monday unless UK govt backs a rescue - Sky News

Saeta Yield: Brookfield reportedly in talks to acquire Saeta Yield – press

Rolls Royce: Reportedly nearing deal to sell its L'Orange unit; wants $700M for the assets - press

Levels as of 01:00ET

Nikkei225 +0.3%, Hang Seng +0.8%; Shanghai Composite -0.4%; ASX200 +0.1%, Kospi +0.3%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.2%

EUR 1.2240-1.2188; JPY 111.19-110.58; AUD 0.7961-0.7904;NZD 0.7282-0.7234

Feb Gold +0.7% at $1,344/oz; Feb Crude Oil +0.3% at $64.52/brl; Mar Copper +1.8% at $3.28; AUD 0.7875-0.7905 ;NZD 0.7248-0.7277

Feb Gold +0.5% at $1,328/oz; Feb Crude Oil -0.3% at $63.62/brl; Mar Copper +0.3% at $3.237/lb