Sample Category Title

USDJPY Intraday Analysis

USDJPY (112.88): The USDJPY managed to recover the losses as the currency pair was seen posting strong gains. The yen was seen weakening as USDJPY is likely to extend the gains back to the 113.00 level of resistance. A breakout to the upside based on the bullish momentum could keep the currency pair poised for further upside. However, any weakness could keep the USDJPY range bound within 113.00 and 112.04 level within which the currency pair has been consolidating for the past few weeks.

EURUSD Intraday Analysis

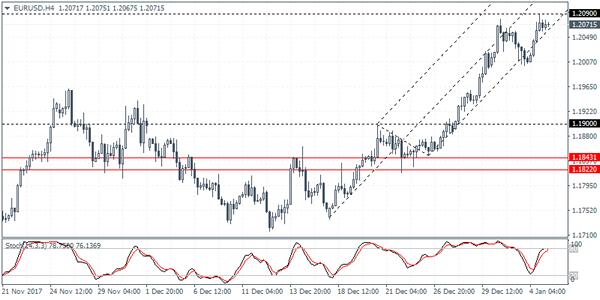

EURUSD (1.2071): The EURUSD managed to erase the intraday losses as the currency pair settled near the previous highs towards the close. Price action briefly tested the highs near 1.2091 before easing back. On the intraday charts, we see the Stochastics posting a bearish divergence. Failure to break out above 1.2091 could signal short term correction in price. The lower support is found at 1.1900 which could be the downside target on a correction in price.

Robust ADP Payrolls Raises The Bar For December NFP

Data from the UK saw the services PMI edging slightly higher. The services sector activity rose 54.2, beating estimates of 54.1 and ending up slightly higher than November's 53.8 reading.

Private payrolls hiring was seen rising robustly on the back of the holiday season. Data from ADP/Moody's showed that the private sector hiring increased by 250k in December. This was higher than the estimates of 191k. November's ADP payrolls were revised down to 185k.

Looking ahead, the markets will be shifting focus to the nonfarm payrolls report that is due today. Market expectations call for a 190k estimate on the jobs added during the month. The U.S. unemployment rate is expected to remain steady at 4.1% while the average hourly earnings are expected to rise 0.3% on the month. Following the payrolls report, ISM will be releasing the non-manufacturing PMI data which is expected to show a modest increase to 57.6.

EURO Buyers Still In Control Above 1.2050

The euro has moved to another new-weekly trading high against the U.S dollar, hitting 1.2089, on Thursday, as strong ADP jobs numbers helped risk-on sentiment in global markets. The EURUSD pair fell just short of the 2017 price-high, at 1.2093, creating a bearish double-top pattern on the price-charts. Price-action currently trades around the 1.2070 level, as buying momentum for euros remains strong. Financial markets now look to the U.S Non-farm payrolls job report, with economists expecting 190,000 new jobs were created during December.

The EURUSD pair is strong bullish while trading above the 1.2050 level, intraday targets above the 1.2093 level are 1.2150 and 1.2200.

Should the EURUSD pair decline below the 1.2050 level, again, sellers will look to test the key 1.2030 region and the psychological 1.2000 level.

GBPUSD Intraday Bullish Above 1.3567 Level

The British pound has continued to erase losses against the U.S dollar, with price action reaching the 1.3570 level during today’s Asian trading session. The GBPUSD pair currently trades above the key 1.3567 resistance level, with the 1.3610 level the next major technical barrier ahead for buyers. Sterling’s rise from the 1.3500 support level has taken place on minimal trading volume, with genuine buying momentum in the pair still at depressed levels. The main market moving event today is this December Nonfarm Payrolls job report, volatility in the GBPUSD pair is likely to increase after the report is released.

The GBPUSD pair is strongly bullish above the 1.3567 level, upside targets above the 1.3610 resistance area are 1.3657 and 1.3710.

Should price-action on the GBPUSD pair fall below the 1.3567 level, decline towards the 1.3550 and 1.3500 support regions seems likely.

US Nonfarm Payrolls Headline Final Session Of Week

After an active first week of 2018, attention shifts on Friday to the most anticipated report of the month: US nonfarm payrolls. The December release is expected to confirm what we already know about the labour market – that it is expanding firmly.

Market participants can expect a steady stream of economic data to be released in advance of the official US report. Action begins at 07:00 GMT with a report on German retail sales. Receipts at German retail stores are forecast to rise 1% month-on-month and 2.5% annually.

Reports on French consumer confidence and Italian retail sales will make their way through the market over the next two hours.

By 10:00 GMT, the European Commission's statistical agency will report the December consumer price index (CPI). Annual inflation in the 19-member euro area is forecast to drop to 1.4% from 1.5% previously. So-called core inflation is projected to pick up to 1% from 0.9% in November.

At 8:30 GMT, the Department of Labor will issue its long-awaited December nonfarm payrolls report. The monthly data set is expected to show the creation of 190,000 nonfarm jobs last month, following a gain of 228,000 in November. The jobless rate is expected to hold steady at 4.1%, with average hourly earnings accelerating 0.3% month-on-month.

On Thursday, payrolls processor ADP Inc. said private-sector employment surged by 250,000 in December, with services employment driving the bulk of the gains. The figure was much higher than the 190,000 predicted by economists, and may have raised the stakes for Friday's official data release.

However, solid payrolls data failed to lift the US dollar, which returned to multi-month lows against a basket of world currencies. The US dollar index (DXY) closed at 91.87 on Thursday, and was little changed at the start of Asian trade.

In addition to the non-farm payrolls report, investors can expect headline factory orders and ISM non-manufacturing PMI to be released later in the North American session.

North of the border, the Canadian government will also report on employment Friday. Canada's jobless rate is expected to rise slightly to 6% in December from 5.9% previously.

EUR/USD

The euro returned to strength on Thursday, with prices approaching the 1.2100 US handle. The uptrend peaked at 1.2086, and a clean break above this level is needed to confirm a bigger uptrend.

GBP/USD

Pound sterling returned to positive territory on Thursday following a sharp correction the previous session. Cable was last seen trading at 1.3565, having gained 0.1%. The pair now faces immediate resistance at the weekly high of 1.3612.

USD/JPY

The dollar resumed its uptrend against the yen on Thursday, as risk sentiment faded. The USD/JPY was last seen trading at 112.84, where it is holding above the 100-DMA. Prices are eyeing the short-term resistance of 112.90.

Forex Analysis: Australian Trade Balance Misses Expectations

Australian Trade Balance for November came in very wide of the mark at -628M v an expected 915M. The previous reading was revised down to -302M from 105M. This was the second month in a row where there was a substantial miss to the downside. AUDUSD moved lower from 0.78679 to 0.78429.

Eurozone Markit Services PMI (Dec) data was out Wednesday morning, coming in at 56.6 v an expected number of 56.5, with the previous reading coming in at 56.5. Markit PMI Composite (Dec) was also due out at this time, coming in at 58.1 v an expected number of 58.0, with a prior of 58.0. EURUSD moved higher from 1.20247 after the release of the data.

UK Markit Services PMI (Dec) was 54.2 v 53.8 expected, with a prior number of 53.8. Net Lending to Individuals (MoM) (Dec) came in as expected at £4.9B, with a previous reading of £4.8B. Mortgage Approvals (Nov) was 65.139K v 64.000K expected, from a prior 64.887K. Consumer Credit (Nov) was £1.400B v £1.500B expected, with the prior figure being revised to £1.362B. GPBUSD found support around 1.35400 and moved up to 1.35555.

US ADP Non-Farm Employment Change jumped to 250K v an expected 190K, and the prior value was revised down to 185K from 190K. USDJPY gapped up to 112.745 from 112.622 on this data release and continued up to 112.838. US Continuing Jobless Claims (Dec 22) was 1.914M, from an expected number of 1.925M, with the prior of 1.943M revised to 1.951M. Initial Jobless Claims (Dec 29) was 250K v an expected 240K, with a previous read of 245K revised to 247K.

US Markit PMI Composite (Dec) was 54.1 v an expected 53.7, from a prior of 53.0. Markit Services PMI (Dec) was 53.7 from an expected 52.4, with a previous reading of 52.4. Stocks rallied higher after these data points, with the Dow Jones Index moving higher from 25000.

US EIA Crude Oil Stocks change (Dec 29) was released with a headline number of -7.419M v -5.182M expected, from a previous -4.609M. This data release was delayed due to New Year’s festivities. WTI Oil rallied back to $62.00 after the news.

EURUSD is unchanged overnight, trading around 1.20628.

USDJPY is up 0.32% in the early session trading at around 113.099.

GBPUSD is up 0.11% to trade around 1.35635.

AUDUSD is down -0.28% this morning, trading around 0.78386.

Gold is down -0.33% in early morning trading at around $1,317.75.

WTI is down -0.16%, trading around $61.82.

Major data releases for today:

At 10.00 GMT, Eurozone Consumer Prices Index – Core (YoY) (Dec) is expected at 1.0% from a previous 0.9%. Consumer Price Index (YoY) (Dec) is expected at 1.4% from a prior 1.5%. EUR pairs may see price movement if the data released varies from the consensus.

At 13:15 GMT, US Non-Farm Payrolls (Dec) is expected at 190K v a prior 228K. This measures the change in the number of employed people in December. The Unemployment Rate (Dec) is expected unchanged at 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during December. USD crosses could experience volatility around this data release.

At 13:30 GMT, Canadian Unemployment Rate (Dec) is expected at 6.0% from a prior of 5.9%. Net Change in Employment (Dec) is expected to be 1.0K with a previous read of 79.5K. CAD crosses can make sudden moves to test support and resistance after the data points are released.

At 15:00 GMT, US ISM Non-Manufacturing PMI (Dec) is expected at 57.6 from a prior of 57.4. Factory Orders (MoM) (Dec) is expected at 1.1% with a previous reading of -0.1%. This data can move USD pairs upon its release.

At 18.00 GMT, Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 747. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

Currencies: EUR/USD Testing Range Top Ahead Of The US Payrolls

Sunrise Market Commentary

- Rates: Big day ahead

Today's eco calendar heats up with EMU CPI, US Payrolls and US non-manufacturing ISM. We have a positive intraday bias for core bonds especially if this week's risk/oil rally shows signs of fatigue. The risk scenario is a big upward surprise in the average hourly earnings components in the US payrolls report. - Currencies: EUR/USD testing range top ahead of the US payrolls

Yesterday, the dollar showed a mixed picture and couldn't fully profit from a very strong ADP labour market report. Today, EMU inflation is expected soft, but it isn't evident that this will break the strong euro momentum. The dollar probably needs very strong payrolls and, in particular strong wage data, to change fortunes

The Sunrise Headlines

- US stock markets closed positively with Nasdaq slightly underperforming because of the Intel chip's flaws. Asian stock markets copy WS's positive risk sentiment with Korea and Japan outperforming.

- The Trump administration proposed opening up nearly all the country's offshore areas for oil and gas drilling, a move that would touch every coastal state, some that have been off limits to drillers for decades.

- Australia's trade deficit widened to A$628 million ($494 million) in November from a revised A$302 million a month earlier. Expectations were for an A$550 million surplus. AUD/USD slightly suffered, declining to 0.7850.

- UK shop prices slipped further into deflationary territory as retailers offered discounts on non-food products, according to the British Retail Consortium. The BRC-Nielsen shop price index found prices fell 0.6% Y/Y in December.

- China released new rules tightening bond trading regulations, with a focus on restricting leverage and banning under-the-table deals.

- North Korea accepted a proposal to hold talks with South Korea on Tuesday, reducing tensions as President Moon Jae-in's government prepares to host the Winter Olympics next month.

- Today's eco calendar heats up with EMU CPI data, US payrolls and US non-manufacturing ISM. Fed Harker and Mester are scheduled to speak

Currencies: EUR/USD Testing Range Top Ahead Of The US Payrolls

EUR/USD testing cycle top ahead of payrolls

The dollar showed a mixed picture yesterday. It returned most of Wednesday's gains against the euro. A very strong ADP labour report couldn't change fortunes in favour of the dollar. Strong growth prospects for EMU kept the euro well supported. EUR/USD tested the 1.2081/92 range top, but a break didn't occur (close at 1.2068). At the same time, USD/JPY profited from slightly higher US yields and buoyant risk sentiment. The pair filled offers in the 112.85 area and closed at 112.75. The combined rise of both EUR/USD and USD/JPY propelled EUR/JPY above 136, the highest level since October 2015.

The risk rally continues overnight, but the pace is easing a bit. The USD trading pattern persists. EUR/USD holds within reach of the 2017 top. USD/JPY maintains a good bid and tries to regain the 113 handle. The recent rally of the Aussie dollar was blocked as the country recorded an unexpected trade deficit in November. AUD/USD returned to the 0.7850 area. Today, the EMU December CPI is expected to have declined to 1.4% Y/Y from 1.5%. A big base effect is at play. An upward surprise looks unlikely. Question is whether a soft EMU CPI will block the recent strong euro momentum. In the US, the payrolls, the nonmanufacturing ISM, the trade balance and the order data will be published. Evidently, the focus will be on the payrolls and in particular on the wage data. The consensus expects a rise of 0.3% M/M and 2.5% Y/Y. This consensus probably needs to be met (or surpassed) to prevent further USD losses. Recently, the greenback suffered as the global recovery might force other major CB's (including ECB) to join policy normalisation. For now, we maintained the working hypothesis that enough good news on the euro/'bad news' on the dollar was discounted and that a sustained break beyond the 1.2092 cycle top is not evident. Today's payrolls (wage data) might decide whether this approach remains valid.

Yesterday, UK eco data had only a limited impact on sterling trading. The overall rise of the euro helped EUR/GBP to regain the 0.89 barrier. Cable (close 1.3550) gained slightly as the dollar held a soft bias. There are only second tier UK eco data today. Sterling is rather well bid this morning despite soft BRC shop price data. EUR/GBP struggles not the fall back below the 0.89 mark. We expect more sideways trading today. Recent UK data were mixed. We don't expect the BoE to raise interest rates soon. EUR/GBP 0.8700/60 support looks solid. Euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buy-on-dips in case of return action to 0.87

EUR/USD holding near 1.2092 range top going into US payrolls report

Market Update – Asian Session: Asian Equities And Currencies Trade Generally Higher

Australia/New Zealand

ASX 200 opened +0.3%: closed +0.7%

ASX Resources Index +0.9%, Financials +0.8%; REITs -0.6%

Aussie declines after weaker than expected Nov trade data; Australia Nov Trade Balance (A$) -628M v +550Me (2nd straight deficit); Prior trade revised lower from +105M to 302M (first deficit since Oct 2016)

China/Hong Kong

Hang Seng opened +0.5%, Shanghai Composite flat

Chinese beer companies trade sharply higher: Brewers in China reportedly boost prices by 10-20%, said a local press report

HSCI Property/Construction Index +2.5%, Energy +0.6%; Consumer Goods -0.6%, Financials -0.2%

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.4915 V 6.5043 PRIOR (strongest CNY fix since May 2016)

(CN) China PBoC: Skips OMO for 10th straight session: Net drain: Nil v CNY130B prior

(CN) China issues rules for equity investment by insurance funds: to ban insurers from guaranteed return of equity on investments; China's insurance regulator, CIRC, says the rules are aimed at curbing 'implicit' local government debt.

(CN) China to collect personal debt information related to online finance – Chinese Press; Says the purpose of the credit information platform is to help deal with systemic risks

(CN) There is renewed press speculation that China may maintain GDP growth target at around 6.5% for 2018 – financial press

(CN) Yuan unlikely to see sharp rises or falls in 2018; likely to be mostly stable - Chinese press: **Note: The report is in line with some of the recent comments by Chinese officials.

Japan

Nikkei 225 opened +0.6% after gaining 3.3% in prior session in catch-up rally: closed: +0.9%

TOPIX Iron & Steel Index +1.5%, Securities +0.7% (gained 4.9% prior session), Electric Appliances +0.7%

Toshiba +3%: Brookfield Business Partners announces deal to acquire Westinghouse for $4.6B

Continued strength in the auto sector, following Thursday’s gains: Toyota +1.8%, Nissan +1.4%

Financials track the strength seen in the NY session: Sumitomo Mitsui +1.4%, Mitsubishi UFJ +1.4%

Softbank -1.1%

Fast Retailing +0.9%: To report Dec SSS after the close

(JP) Japan Finance Min Aso: Reiterates needs to raise sales tax for fiscal consolidation, but if economy is not good tax hike can't proceed; To craft new primary balance goal around next year.

(JP) Japan Dec Nikkei PMI Services 51.1 v 51.2 prior; Composite: 52.2 v 52.2 prior

(JP) Japan Dec Monetary Base: ¥480.0T v ¥471.5T prior; Y/Y: 11.2% v 13.2% prior

Korea

Kospi opened +0.4%

Chipmakers trade higher: Samsung Electronics +1%, Hynix +2.5%

Financials also generally higher: Industrial Bank of Korea +1.7%, KB Financial +1%. Hana Financials +0.9%

Korean Won (KRW) trades near 3-year high amid equity flows

(KR) Follow Up: South Korea Unification Ministry: North Korea said it accepts offer for talks on Jan 9th; talks to include Winter Olympics and 'other issues of mutual interest'; Expects additional hotline talks with North Korea over the weekend.

(KR) White House spokesperson: confirms Pres Trump and South Korean Pres Moon agreed to continue campaign of maximum pressure against North Korea; Agreed to de-conflict the Olympics and our military exercises to ensure Games' security

(KR) China said to send an envoy (to discuss North Korea) to South Korea between Jan 5th- 6th - press

(KR) North Korea said to be ‘likely’ preparing for new rocket engine test (no timeframe given) – US financial press

(KR) South Korea Nov Current Account Balance: $7.4B v $5.7B prior; Balance of Goods (BOP): $11.5B v $8.6B prior

Other Asia

USD/MYR: Trades at the lowest level since Aug 2016: Malaysia Ringgit (MYR) +0.3%

(MY) Malaysia Nov Trade Balance (MYR) 9.95B v 10.9Be; Exports to China +3.3%, US+13.4%

USD/INR: Indian Rupee (INR) trades at highest level since July 2015.

(PH) PHILIPPINES DEC M/M: 0.3% V 0.3%E; Y/Y: 3.3% V 3.3%E; CORE Y/Y: 3.0% V 3.1%E**Note: Central Bank has 2.0-4.0% target range for inflation

North America

US equity markets ended broadly higher: Dow +0.6%, S&P500 +0.4%, Nasdaq +0.2%, Russell 2000 +0.2%

S&P500 Financial Sector +1%, Materials +0.8%

Apple: Said all Mac systems and IOS devices are affected by chip security issue, but no known exploits are currently impacting customers; recently uncovered security issues known by the names of 'Meltdown' and 'Spectre'

(US) Fed’s Bullard (non-voter, Dove): inflation targeting has been major achievement for the Fed; price level targeting is worth consideration

(US) DOE CRUDE: -7.4M V -4.5ME

Looking ahead: US Dec Nonfarm payrolls due for release, along with US Dec ISM Non-Manufacturing PMI and Canada Dec Employment Change

Europe

(UK) UK 2017 New Car Sales down ~5.6% to 2.54M units (largest decline since 2009); Sees 2018 new car sales down 5-7% – SMMT

(UK) UK Dec BRC Shop Price Index Y/Y: -0.6% v -0.1%

Looking Ahead: Euro Zone Dec prelim CPI to be released (German Dec prelim CPI was released on Dec 29th)

(IR) United Nations (UN) Security Council reportedly to hold meeting on Friday at 15:00ET concerning situation in Iran - press

Levels as of 01:00ET

Hang Seng flat; Shanghai Composite +0.3%; Kospi +1%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.1%; FTSE100 -0.1%%

EUR 1.2065-1.2080; JPY 112.72-112.97; AUD 0.7843-0.7870 ;NZD 0.7146-0.7165

Feb Gold +0.1% at $1,322/oz; Feb Crude Oil flat at $62.02/brl; Mar Copper +0.4% at $3.272/lb

USDCAD Turns More Bearish After Falling Out Of 2-Month Range

USDCAD is looking weak after falling out of a 2-month range. Prices broke below key support at 1.2500 although appear to have stabilized for now just below this level. The daily RSI is in bearish territory but has turned neutral in the short term, very close to oversold levels.

Looking at the bigger picture, USDCAD was trading in a range between 1.2680 and 1.2900 from late October to late December.

Strong resistance was found at the Fibonacci retracement level at 1.2922 (50% of the 1.3793 – 1.2061 decline). Further resistance was provided by the 200-day moving average around the same area. The rejection of this resistance zone was a major negative for USDCAD and so there was consequently a break out from the range. The triple top chart formation implies scope for additional losses.

Further support would be expected at 1.2420 and 1.2330 ahead of the 1.2061 low. Near-term resistance is expected at 1.2500 – 1.2550.

Short-term price action may be turning neutral and the market appears to have found support, with risk of a bounce higher. But the overall picture is weak and unless USDCAD can reclaim the 1.27 handle soon, there is risk for more weakening with scope to push towards the low 1.23 area.