Sample Category Title

Canadian Dollar Steady as Investors Eye Employment Data

The Canadian dollar has ticked lower in the Friday session. Currently, the pair is trading at 1.2500, up 0.10%. On the release front, there are a host of key events on both sides of the border. In the US, wage growth is expected to gain 0.3%, but the markets are braced for a slowdown in Nonfarm Payrolls, with an estimate of 190 thousand. We'll also get a look at ISM Non-Manufacturing PMI, which is expected to edge up to 57.6 points. In Canada, Employment Change is expected to post a soft gain of 1.8 thousand, after a sparkling gain of 79.5 thousand in November. Canada will also release Ivey PMI and Trade Balance. Traders should be prepared for some movement from USD/CAD during Friday's North American session.

The Canadian dollar climbed 2.5% in December, and continues to move higher early in the New Year. Much of the loonie's climb can be attributed to the rise in oil, which has jumped 6.8% since mid-December. Geopolitical tensions have boosted oil prices, in particular tensions with North Korea and the recent civil unrest in Iran. There is pressure on the Bank of Canada to raise its benchmark rate of 1.0%, which is lagging behind the Federal Reserve rate of between 1.25-1.50%. With the Fed widely expected raise rates in January, the Canadian dollar could lose ground if the BoC fails to respond with a rate hike of its own on January 17. However, the BoC may hold back, as it concerns continue over US threats to dismantle the free trade agreement.

As expected, the Federal Reserve minutes from December were positive in tone. At that meeting, the Fed raised interest rates for a third time in 2017. Policymakers noted in the minutes that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

USDJPY Strongly Bullish Above 113.10 Level

The U.S dollar has continued to firm against the Japanese yen in early Friday trading, with price-action now trading well above the key 113.10 technical level. The USDJPY pair is currently trading around the 113.25 region, as daily buying momentum accelerates as the U.S dollar index recovers lost ground. Going forward, the 113.60 resistance zone is the next major technical barrier for medium and long-term USDJPY bulls. The upcoming U.S Non-farm payrolls job report will impact the pair also, with expectations high for a solid headline number.

Buyers retain control of the pair while price-action trades above the key 113.10 level, upside targets for the USDJPY pair are located at 113.60 and 114.40.

Should the USDJPY pair decline below the 113.10 technical level, well-defined daily support is found at 112.70 and 112.30.

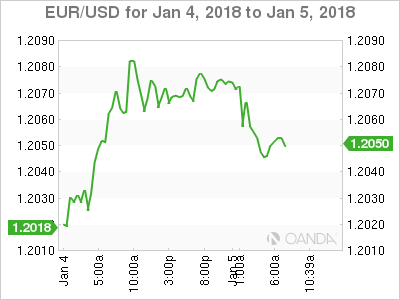

EURUSD Direction Defined by 1.2050 Level

The euro has moved marginally lower against the U.S dollar during the European trading session, falling to a session low around the 1.2040 region. The EURUSD slipped back despite a round of positive economic data points from the eurozone, which showed rising monthly inflation in the euro trading block and positive German Retail Sales figures. Moving into the U.S session, buyers will look to breach the 1.2089 weekly price- high, while sellers will be focused on the psychological 1.2000 support region.

The EURUSD pair remains bullish while trading above the 1.2050 level, a break of the 1.2089 weekly-high should expose further upside towards 1.2150 and 1.2200.

If sellers can contain the EURUSD below the 1.2050 level, sellers will try to move price-action back below the 1.2030 and 1.2000 levels.

US Jobs Report Eyed After Strong Start to 2018

Optimism Builds Ahead of Earnings Season

It's been a strong start to the year for equity markets and that looks set to continue on Friday, with the Dow seen adding to its gains after flying through 25,000 on Thursday.

Any concerns about a post-tax reform pull-back in equity markets have quickly been quashed, with indices in the US posting decent gains in the first week of the year as investors anticipate another good earnings season. We've seen very good earnings growth from companies in the US and Europe in recent quarters and I think the optimism that we're seeing at the start of the year is potentially being driven by expectations of a similarly positive fourth quarter.

Can US Jobs Report Offer Reprieve For Battered Greenback

That isn't helping to lift the dollar which has sold off heavily over the last few weeks despite optimism over tax reform. It's possible that the difference in fortune for the dollar and US stocks is partly a reflection of who investors believe stands to gain from the reforms and how significant an economic - and therefore inflationary - impact they'll have.

Of course there are other factors at play including the impact that a flattening of the yield curve is having on interest rate expectations and the changing tightening prospects of other central banks. For the dollar's fortunes to change I think we'll need to see signs that inflation is heading towards target because what we're seeing right now is Fed chat fatigue. We've been promised higher inflation and wage growth for some time and investors are increasingly not buying it.

Even some policy makers are starting to question why nothing has not materialised and should that continue, rate hike forecasts will start to slip, especially with interest rates now already elevated. Today's jobs report should offer some insight on this, with average earnings having arguably become the most important component of it. Still earnings are only expected to have risen by 2.5% compared to a year ago, below last year's peak and well below where they need to be for inflation to sustainably return to target.

Naturally, the unemployment and non-farm payrolls numbers will also attract a lot of attention, with the former expected to remain at 4.1% and the latter rising by 190,000. While the ADP has often not been a great estimate of the NFP number, a 250,000 number on Thursday may suggest NFP expectations are a little low, creating some upside potential. Whether the dollar follows and holds will likely depend on those wage numbers though.

U.S Dollar Seeks Guidance From NFP

Friday January 5: Five things the markets are talking about

After a positive week of global economic data boosted markets, investor focus now turns to today's U.S. jobs release (8:30 am EDT) as the next key economic barometer.

The 'mighty' greenback, which had been battered and bruised throughout 2017 – U.S dollar index lost just under -10% against G10 currency pairs – requires today a much-stronger-than-expected December non-farm payroll (NFP) headline print to garner much needed support.

Note: The market is not expecting any changes to the U.S jobless rate (+4.1%), and a healthy headline print of +180k new non-farm jobs last month, with average hourly earnings set to rise +0.3% on the month.

However, a stronger reading may not even be the answer. Market consensus ahead of yesterday's ADP reading was for an increase of +193k, but the payroll firm's report put growth at +250k. That reading was incapable of pushing up U.S Treasury yields further yesterday or even encourage the U.S dollar "bulls" to add to their positions.

Canada is also reporting its labor market data this morning (8:30 am EDT). Of late, the headline print has been surprisingly strong (+2K expected and +6% unemployment rate).

1. Global stocks print new records

In Japan, the Nikkei share average extended Thursday's gains overnight, probing a three-decade high as banking and brokerage firms rose. The Nikkei was up +0.9%, while the broader Topix closed +0.8% higher.

Note: In the holiday-shortened week, the Nikkei has risen +4.2% since opening on Thursday.

Down-under, Aussie shares ended higher on Friday, hitting a fresh decade-peak and completing its first weekly session of gains in the New Year. The S&P/ASX 200 index rose +0.7%. In Korea, the Kospi closed out on a winning note, up +0.4%, as the KRW traded at a three month high due to equity flows.

In Hong Kong, equities were up for their ninth-day and closed atop of their ten-year high. At close of trade, the Hang Seng index was up +0.25%, while the Hang Seng China Enterprises index rose +0.07%.

In China, both major benchmark indexes climbed for a sixth straight session, helped by gains for property developers. The Shanghai Composite index was up +0.2%, a six-week high, while the blue-chip CSI300 index was up +0.25%.

In Europe, regional indices continue to trade higher following strong gains yesterday with the FTSE100 making new all time highs. This morning, the DAX leads the gainers, rising +1% on the back of record closes on Wall Street overnight, where the Dow crossed +25K for the first time.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.6% at 395.9, FTSE +0.3% at 7717, DAX +1.0% at 13300, CAC-40 +0.7% at 5453, IBEX-35 +0.5% at 10369, FTSE MIB 0.8% at 22681 , SMI +0.4% at 9551, S&P 500 Futures +0.2%

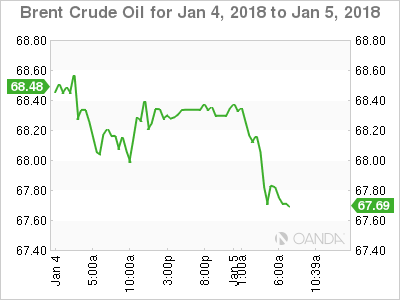

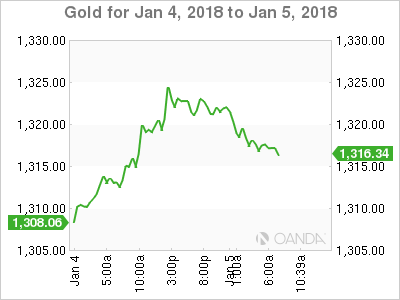

2. Oil slips from 2-year high on rally doubts, gold prices fall

Ahead of the U.S open, crude oil prices fell, dropping away from its two-year-highs, as soaring U.S production undermines its +10% rally from the low print in early December that was driven by tightening supply and political tensions in OPEC member Iran.

Brent crude futures are at +$67.88 a barrel, down -19c, or -0.3% below Thursday's close. U.S West Texas Intermediate (WTI) crude futures are at +$61.81 a barrel. That is -20c or -0.3% below the last close.

Note: Oil prices have received general support from production cuts led by OPEC and by Russia, which started in January 2017 and are set to last through 2018, as well as from strong economic growth and financial markets.

The current momentum, which is also being supported by a record cold spell along the east cost of the U.S, suggests that further upside is on the cards, however, higher prices continues to attract higher U.S shale production, which is a threat to the 'bull' market.

Gold prices have dipped (-0.4% to +$1,317.10 an ounce) ahead of non-farm payrolls (NFP), but the precious metal is set for a month of gains.

3. U.S yields require NFP support

Investors expect more central banks around the world to begin unwinding nearly a decade of stimulus policies in 2018.

These higher global sovereign yields are likely to make the USD less attractive to some investors and any gradual shift in capital flows from the U.S to the eurozone and/or other rising economies will continue to weigh on the dollar in coming months.

Investors are also looking for signs in today's U.S Payrolls that an economic recovery is pushing up wages would bolster the case for the Fed to raise rates more aggressively this year and set up a potential dollar rebound.

Currently, the fixed income market is now pricing in a +68% chance of a Fed March hike and two more hikes for 2018. Any sign of inflation and these odds will tighten and should support the USD.

Overnight, the yield on U.S 10's has increased less than +1 bps to +2.45%. In Germany, the 10-year Bund yield fell -1 bps to +0.43%. In the U.K, the 10-year Gilt yield has decreased -1 bps to +1.222%.

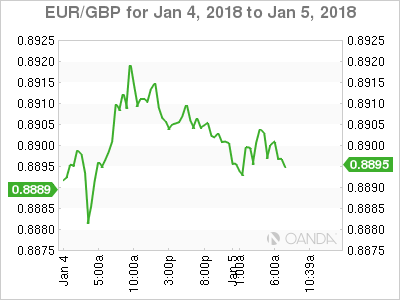

4. U.S dollar seeks guidance from non-farm payroll (NFP)

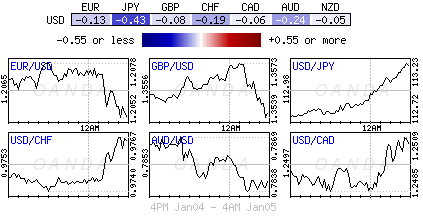

The USD (€1.2050, £1.3541, ¥113.34) remains on relatively soft footing ahead of today's U.S December jobs report. Dollar 'bears' believe the greenback would likely stay under selling pressure if wages component does not show any sign of pick-up.

Note: The current global recovery has everything apart from wage growth (inflation), and this in turn is keeping the Fed rate hikes gradual and currency volatility relatively 'low.'

The EUR/USD (€1.2050) has managed to back away from its recent three-month high print Thursday and has yet to tackle the psychological €1.21 level with any gusto. Even slightly weaker-than-expected December eurozone inflation figures this morning (see below) has thus far failed to upset the 'single' unit.

Note: The EUR had benefited in recent weeks from market reassessment on the ECB policy rate outlook. Markets currently are pricing the first full +25 bps move in Eonia by mid-October 2019, compared to Q1 2020 as seen in early December.

5. Eurozone inflation disappoints

Eurostat data this morning showed that Eurozone inflation fell in December and was in line with market expectations.

Consumer prices eased from their November print last month. The headline print was +1.4% higher than a year earlier versus Novembers +1.5% headline.

Consensus believes that this morning's print is likely to mark the start of a series of declines in the inflation rate in early 2018 as a result of base effects linked to energy prices. Nevertheless, the ECB does expect the inflation rate to pick up again in the latter half of this year.

However, of greater concern for Euro policy makers is the weakness of core inflation. The market had expected to see a rise to +1.0%, but the measure remained at +0.9% for the third consecutive month, exactly where it was in December 2016, when the eurozone economy was on the brink of what appears to have been its best year since 2007.

DAX Rallies to 2-Week High, German Retail Sales Sparkles

The DAX continues to head higher and has posted strong gains in the Friday session. Currently, the index is at 13,310.50, up 1.08% on the day. The DAX is currently at its highest level since December 19 and has jumped 3.2% this week. On the release front, German Retail Sales jumped 2.3%, crushing the estimate of 1.0%. This easily beat the estimate of 1.0%. Eurozone CPI Flash Estimate ticked lower to 1.4%, but matched the forecast. In the US, the focus remains on employment data, led by Nonfarm Payrolls. The markets are braced for the indicator to slow down to 190 thousand.

German economic data hasn't missed a beat, as December numbers continue to impress and have boosted the euro as well as German stock markets. Retail Sales soared 2.3%, its fastest pace since October 2016. Services and Manufacturing PMIs improved and continue to point to strong expansion. The labor market remains robust, as unemployment rolls dropped sharply. The economy hasn't missed a beat, despite an uncertain political landscape in the eurozone's largest economy. President Angela Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are scheduled to begin on Sunday. The negotiations are likely to be lengthy, and strong disagreements on immigration policy and taxation could unravel the talks, which would trigger new elections.

The Federal Reserve minutes released the minutes of its December meeting on Wednesday. At that meeting, the Fed raised interest rates for a third time in 2018, to a range of between 1.25% and 1.50%. The minutes were positive in tone, reflecting a robust US economy. Policymakers noted that economic activity was expanding at a "solid pace", buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

COPPER – Formation of Weekly Bearish Engulfing Threatens for Deeper Correction

Copper remains in red on Friday and is on track for the first negative weekly close after three weeks of strong rally.

Bearish engulfing is forming on weekly chart and could generate stronger bearish signal for deeper correction of $2.9425/$3.3200 three-week rally.

Bears eventually broke below initial support provided by 10 SMA and now pressuring next support at $3.2309 (Fibo 23.6% of $2.9425/$3.3200 ascend).

Sustained break here would open way for deeper correction and expose pivotal supports at $3.1758 (Fibo 38.2% of $2.9425/$3.3200 rally) and $3.1682 (rising 20SMA).

South-heading daily RSI which reversed from overbought territory is showing a plenty of room at the downside for further extension of corrective leg from $3.3200 peak.

Broken 10SMA now acts as initial resistance at $3.2643 which should ideally keep the upside limited.

Res: 3.2643; 3.2970; 3.3085; 3.3200

Sup: 3.2309; 3.2000; 3.1758; 3.1682

Euro Dips Lower, Eurozone Inflation Matches Forecast

The euro is down slightly in the Friday session. Currently, EUR/USD is trading at 1.2048, down 0.17% on the day. On the release front, German Retail Sales sparkled, with a gain of 2.3%. This easily beat the estimate of 1.0%. Eurozone CPI Flash Estimate ticked lower to 1.4%, but matched the forecast. In the US, the focus remains on job data, with the release of Average Hourly Earnings and Nonfarm Payrolls. Wage growth is expected to gain 0.3%, but the markets are braced for a slowdown in Nonfarm Payrolls, with an estimate of 190 thousand. We’ll also get a look at ISM Non-Manufacturing PMI, which is expected to edge up to 57.6 points.

German numbers from December continue to impress the markets. Retail Sales soared 2.3%, its fastest pace since October 2016. Services and Manufacturing PMIs improved and continue to point to strong expansion. The labor market remains robust, as unemployment rolls dropped sharply. The economy hasn’t missed a beat, despite an uncertain political landscape in the eurozone’s largest economy. President Angela Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are scheduled to begin on Sunday. The negotiations are likely to be lengthy, and strong disagreements on immigration policy and taxation could unravel the talks, which would trigger new elections.

The highly-anticipated Federal Reserve minutes were released on Wednesday. The minutes provided details of the December policy meeting, where the Fed raised interest rates for a third time in 2018. The minutes were positive in tone, reflecting a robust US economy. Policymakers noted that economic activity was expanding at a “solid pace”, buoyed by improved consumer and business spending, as well as a stronger global economy. FOMC members revised upwards their projection for GDP in 2018, from 2.1% to 2.5%. The minutes noted that new tax reform is expected to raise economic growth, but the Fed is unsure on the impact of the new law in areas such as the labor market. As for inflation, Fed officials remain concerned that inflation levels are well below the target of 2%, and this trend could continue.

Technical Outlook: FTSE 100 Index Hits New Record Highs

FTSE100 index surged to new record highs on Friday, underpinned by rally in European and US equities as well as rising optimism for strengthening economy. The index rose above previous all-time high at 7649 (29 Dec), heading towards round-figure barrier at 7700 and could stretch towards Fibo 138.2% projection at 7753. Firmly bullish techs support the advance, however, overextended studies give an early sign of corrective action, but no firmer signals seen so far. Rising 10SMA which tracks the rally since mid-Dec, offers solid support at 7581.

Res: 7700, 7753, 7800, 7856

Sup: 7649, 7630, 7581, 7563

Market Update – European Session: Focus On US Dec Jobs Report And Wage Data

Notes/Observations

Euro Zone Dec CPI slows into year-end (as anticipated by ECB); Flash YoY reading at 1.4% v 1.5% prior

Focus on US Dec jobs report particularly on wage components

Asia:

China PBoC: Skips OMO for 10th straight session

Renewed press speculation that China may maintain GDP growth target at around 6.5% for 2018

Japan Dec Nikkei PMI Services 51.1 v 51.2 prior with New orders increase at slowest pace in 15 months

Japan Fin Min Aso reiterated needs to raise sales tax for fiscal consolidation, but if economy was not good tax hike could not proceed (**Note: sales tax increase to 10% is planned for Oct 2019)

Japan Econ Min Moteg reiterated domestic economy doing 'very well', but still needed to monitor risks to outlook

Europe:

France PM Macron said to have warned against 'prisoner's dilemma' splits in EU over Brexit negotiations

Americas:

Fed’s Bullard (non-voter, Dove): inflation targeting has been major achievement for the Fed; price level targeting is worth consideration. During Q&A he noted that the Fed needed to debate wisdom of proceeding with rate rises if the 10-year yields did not increase and the curve flattened

Economic Data:

(DE) Germany Nov Retail Sales M/M: 2.3% v 1.0%e; Y/Y: 4.4% v 2.3%e

(DK) Denmark Nov Gross Unemployment Rate: 4.3% v 4.3%e; Unemployment Rate (Seasonally adj): 3.4% v 3.4% prior

(NO) Norway Nov Credit Indicator Growth Y/Y: 5.8% v 5.7% prior

(FR) France Dec Preliminary CPI M/M: 0.3% v 0.3%e; Y/Y: 1.2% v 1.2%e

(FR) France Dec Preliminary CPI EU Harmonized M/M: 0.4% v 0.4%e; Y/Y: 1.3% v 1.3%e

(FR) France Dec Consumer Confidence: 105 v 103e

(TW) Taiwan Dec CPI Y/Y: 1.2% v 0.9%e; CPI Core Y/Y: 1.6% v 1.3% prior; WPI Y/Y: 0.2% v 1.6% prior

(DE) Germany Dec Construction PMI: 53.7 v 53.1 prior

(UK) Q3 Unit Labor Costs Y/Y: 1.3% v 1.7% prior

(EU) Euro Zone Dec Advance CPI Estimate Y/Y: 1.4% v 1.4%e; CPI Core Y/Y: 0,9% v 1.0%e

(EU) Euro Zone Nov PPI M/M: 0.6% v 0.3%e; Y/Y: 2.8% v 2.5%e

(IT) Italy Dec Preliminary CPI M/M: 0.4% v 0.2%e; Y/Y: 0.9% v 0.8%e

(IT) Italy Dec Preliminary CPI EU Harmonized M/M: +0.3%e v -0.2% prior; Y/.Y: 1.1%e v 1.1% prior

Fixed Income Issuance:

(ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2033 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at at 390.1, FTSE -0.2% at 7482, DAX -0.3% at 13088, CAC-40 -0.2% at 5388, IBEX-35 +0.1% at 10270, FTSE MIB +0.2% at 22442, SMI -0.1% at 9384 , S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

Equities

Indices [Stoxx600 +0.6% at 395.9 , FTSE +0.3% at 7717 , DAX +1.0% at 13300, CAC-40 +0.7% at 5453 , IBEX-35 +0.5% at 10369, FTSE MIB 0.8% at 22681 , SMI +0.4% at 9551, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes:

European indices continue to trader higher following strong gains yesterday with the FTSE100 making new all time highs. The Dax leads the gainers rising 1% on the back of record closes in Wallstreet overnight, where the Dow crossed 25K.

Shares of Ion Beam in Belgium is a notable decliner this morning after cutting its 2017 outlook and withdraws all other guidance, while Norwegian Airlines trades higher after lifting its outlook. UK Car retailers are under pressure with Vertu and Pendragon trading lower after UK Car registration data. In the M&A space Takeda announced intention to acquire Tigenix for €1.78, and Emmi divested its minority stake in Icelandic Milk and Skyr.

In the US shares of Intel remain in focus following the security flaws in their computer chips, with press reports noting the company has been dealing with the issue since June.

Looking ahead to the US morning notable earners include Constellation Brands, Greenbrier and Cal-Maine Foods.

Movers

Consumer Discretionary [ Johnson Service Grp [JSG.UK] +2.3% (Trading update), Cairn Homes [CRN.UK] -2.3% (Trading update), Emmi [EMMN.CH] +2.1% (Divestiture), Norweigen Air [NAS.NO] +12% (Lifts outlook), Pendragon [PDG.UK] -3.3%, Vertu Motors [VTU.UK] -2% (UK Car registration data)]

Consumer Staples [Greenyard [GREEN.BE] +1.5% (Ends talks with Dole foods)]

Healthcare [Ion Beam [IBAB.BE] -17.4% (Cuts outlook))]

Speakers

Austria Fin Min Loeger: Govt has agreed to €2.5B in budget cuts in 2018

Thailand Central Bank Dep Gov Supapongse reiterated view that ready to step in if THB currency (Baht) price movements are too fast

Currencies

USD remained on soft footing ahead of the US Dec jobs report. Dealers noted that the greenback would likely stay under selling pressure if wages did not show any pick-up. The current global recovery has everything apart from wage growth/inflation which in turn is keeping the Fed rate hikes gradual and volatility low

EUR/USD moved off its recent 3-month highs and yet to break above the 1.21 level. Dec CPI data dis slow into year-end 9as expected). Overall the Euro had benefited in recent weeks from market reassessment on the ECB policy rate outlook. Markets currently pricing the first full 25bp move in eonia by mid-October 2019, compared to Q1 2020 seen in early December

Fixed Income

Bund Futures trade up 2 ticks at 161.72 after Euro Zone headline inflation declines as expected. A continued move below 161.00 low targets 160.71 then 160.45, with a continued rebound targeting 161.86.

Gilt futures trade at 124.77 down 5 ticks off the session highs and close to the highs for the week. Continued upside eyeing 125.25 then 125.82. Downside targets include 123.25 then 122.75.

Friday’s liquidity report showed Thursday's excess liquidity rose to €1.841T from €1.823T prior. Use of the marginal lending facility fell to €12M from €53M prior.

Corporate issuance saw at least three deals have hit the US high-grade primary, as not even the bomb cyclone can stop eager borrowers from seizing the moment; Lipper reports equity fund inflows of $964M in week ending Jan 3rd. High yield funds saw inflows of $186.4M in the week.

Looking Ahead

06:00 (BR) Brazil Nov Industrial Production M/M: -0.1%e v +0.2% prior; Y/Y: 3.8%e v 5.3% prior

06:00 (IE) Ireland Nov Retail Sales M/M: No est v 0.0% prior; Y/Y: No est v 4.5% prior

06:00 (IE) Ireland Dec Live Register Monthly Change: No est v -2.6K prior; Live Register Level: No est v 244.3 prior

06:00 (UK) DMO to sell combined £3.0B in 1-month, 3-month and 6-month Bills (£0.5B, £0.5B and £2.0B respectively)

06:30 (IN) Weekly India Forex Reserves

06:45 (US) Daily Libor Fixing

07:00 (IN) India GDP Annual Estimate for 2018 Y/Y: 6.6%e v 7.1% prior

07:00 (CL) Chile Nov Economic Activity Index (Monthly GDP) M/M: +0.2%e v -0.3% prior; Y/Y: 2.5%e v 2.9% prior; Ex-Mining: No est v 2.2% prior

07:00 (CL) Chile Nov Nominal Wage M/M: No est v 0.2% prior; Y/Y: 5.3%e v 5.3% prior

08:00 (PL) Poland Dec Official Reserves: No est v $113.4B prior

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:05 (UK) Baltic Dry Bulk Index

08:20 (BR) Brazil Dec Vehicle Production: No est v 249.1K prior; Vehicle Sales: No est v 204.2K prior; Vehicle Exports: No est v 73.1K prior

08:30 (US) Dec Change in Nonfarm Payrolls: +190Ke v +228K prior; Change in Private Payrolls: +193Ke v + 221K prior; Change in Manufacturing Payrolls: +18Ke v +31K prior

08:30 (US) Dec Unemployment Rate: 4.1%e v 4.1% prior; Underemployment Rate: No est v 8.0% prior

08:30 (US) Dec Average Hourly Earnings M/M: 0.3%e v 0.2% prior; Y/Y: 2.5%e v 2.5% prior; Average Weekly Hours: 34.5e v 34.5 prior

08:30 (US) Nov Trade Balance: -$49.9Be v -$48.7B prior

08:30 (CA) Dec Net Change in Employment: -2.0Ke v +79.5K prior; Unemployment Rate: 6.0%e v 5.9% prior; Full Time Employment Change: No est v +29.6K prior; Part Time Employment Change: No est v +49.9K prior; Participation Rate: No est v 65.7% prior

08:30 (CA) Canada Nov Int'l Merchandise Trade: -C$1.1Be v –C$1.47B prior

08:30 (US) Weekly USDA Net Export Sales data

10:00 (US) Nov Factory Orders: +1.1%e v -0.1% prior; Factory Orders (ex-transportation): No est v 0.8% prior

10:00 (US) Dec ISM Non-Manufacturing. Composite: 57.6e v 57.4 prior

10:00 (US) Nov Final Durable Goods Orders: No est v 1.3% prelim; Durables Ex-Transportation: No est v -0.1% prelim; Capital Goods Orders (Non-defense/ex-aircraft): No est v -0.1% prelim; Capital Goods Shipment (Non-defense/ex-aircraft): No est v 0.3% prelim; Durables Ex-Defense: Mo est v 1.0% prelim

10:00 (CA) Canada Dec Ivey Purchasing Manager Index (Seasonally adj): No est v 63.0 prior; PMI (unadj): No est v 62.4 pror

10:15 (US) Fed’s Harker on economic outlook

12:30 (US) Fed's Mester speaks on Panel on Monetary Policy Coordination

13:00 (US) Weekly Baker Hughes Rig count data

19:00 (CO) Colombia Dec CPI M/M: 0.3%e v 0.2% prior; Y/Y: 4.0%e v 4.1% prior

Fed's Bullard speaks at Economics Convention in Philadelphia

Weekend:

(DE) Germany political parties begin grand coalition talks