Sample Category Title

The Weekly Bottom Line: Economy Added 2.2 Million Jobs in 2017

U.S. Highlights

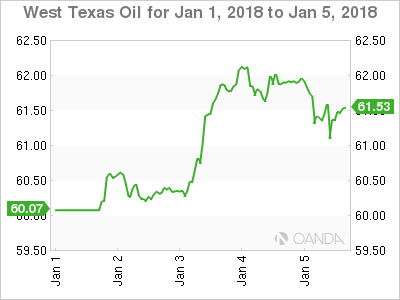

- Investors celebrated tax cuts by snapping up U.S. equities this week, extending last year's record-setting rally into the first week of 2018. Energy stocks were lifted as WTI hit $62 for the first time since 2014.

- December's solid jobs report capped the end of a stellar year for the labor market as the unemployment rate remained at a 17-year low of 4.1%. Overall, 2.2 million jobs were added in 2017.

- In 2018, tax cuts will provide employers with more ammunition for pay upgrades, which will help inflation edge higher. We expect the Fed to hike twice in 2018, with inflation expected to reach 2% later this year.

Canadian Highlights

- The hot streak in Canada's labour market continued, with a robust 79k jobs added in December.

- Other details of the jobs report were similarly upbeat, with the unemployment rate falling to a multi-decade low, hours worked surging and wage growth holding near 3%.

- For a data dependent Bank of Canada, across-the-board labour market strength likely seals the deal on a January rate hike.

U.S. - Economy Added 2.2 Million Jobs in 2017

Investors celebrated tax cuts by snapping up U.S. equities this week, extending last year's record-setting rally into the first week of 2018. The Dow Jones Industrial Average, S&P 500 and Nasdaq Composite reached fresh highs, owing to rising profit expectations and strong fundamentals. Energy stocks were lifted as WTI hit $62 for the first time since 2014, a result of strong global demand that has fueled a production boom and helped drain oil surpluses. Strong activity was reflected in global manufacturing indices in December. The U.S. ISM manufacturing index reached its highest annual level since 2004 in 2017, while similar indices in the Eurozone, China, and the UK also reflected roaring factory activity (Chart 1).

Production has been supported by solid spending figures, with U.S. vehicle sales in December being a prime example. Auto sales rounded out 2017 strongly, helping make the annual total the fourth best in history for auto dealers. Although pent-up demand for vehicles dwindled over 2017, sales in 2018 should continue to be supported by lengthening loan terms and tightening labor markets. Moreover, personal income tax cuts should provide an additional boost to demand.

Tax reform was also a topic discussed by the FOMC in December. The pace of monetary policy normalization could increase to offset any inflationary pressures that materialize from the plan. This prospect sent the U.S. dollar higher temporarily while the ten-year benchmark bond yield rose. Still, the Committee expressed concern over low inflation that has remained despite persistent labor market tightening.

Indeed, this morning's data confirms that the U.S. labor market continues to tighten. December's solid jobs report capped the end of a stellar year for the labor market as the unemployment rate remained at a 17-year low of 4.1% for the third consecutive month. Strong hiring brought the total jobs added in 2017 up to roughly 2.2 million, outperforming 2016 (Chart 2). As the labor market approaches full employment, the pace of hiring will subside as the unemployment rate stabilizes in the medium term. Employers will have to dole out larger pay increases in order to attract and retain workers. And, with tax cuts providing more ammunition for pay upgrades, it is just a matter of time before inflation edges higher. Additionally, the recent increase in commodity prices may squeeze profit margins further, and should translate into consumer price increases as the year progresses. Next week's CPI report should illustrate the extent to which this has impacted price growth in December.

All told, the strong finish to 2017 provides ample momentum for a pickup in growth in 2018. We still expect the Fed to hike twice in 2018, assuming that inflation builds steadily, reaching the Fed's 2% target later this year. However, political uncertainties still loom large. This includes a federal budget resolution, as temporary funding runs out on the 19th of this month. Although another short-term extension could be passed in order to curtail a government shutdown, several contentious issues will eventually need to be addressed.

Canada - Blowout Jobs Report Supports January Rate Hike

The economic calendar began the New Year on a relatively quiet note. However, this soon gave way to end-of-week fireworks with a blowout jobs report sending yields and the loonie higher. Meanwhile, markets shrugged off a weak merchandise trade report and oil rose further above $60 on optimism surrounding global growth, tensions in Iran and supply disruptions in Libya.

December's jobs report stole the show this week, shattering expectations with a massive gain. Recall that employment surged by 80k in the prior month, leading observers to expect some payback in December. However, this simply did not materialize, as employment jumped 79k in the month, leading Q4 to the strongest quarterly gain since 2010. Other aspects of the report were similarly positive, with the unemployment rate falling to a multi-decade low of 5.7% (Chart 1), labour force participation increasing, hours worked surging and wage growth holding near 3%. Furthermore, employment increased in every province, led by Quebec and Alberta. Quebec's unemployment rate now sports a "4-handle" and is nearly 1 percentage point lower than the national figure. Notably, employment in the finance, insurance and real estate sector was up a robust 4.6% year-over-year in December, providing some comfort ahead of the implementation of the B20 guidelines. For the year as a whole, employment increased by 423K, marking a significant acceleration from 2016 and the fastest December-to-December gain since 2002 (Chart 2).

If there were a minor quibble in today's data, it was that the gain skewed towards part-time work. Moreover, youth employment, flagged by Governor Poloz as an on-going concern, dipped modestly following three straight gains. While the Governor continues to fret about declining youth participation, we contend in an upcoming report (out on Tuesday January 9th) that this phenomenon is explained by rising school enrolments – a positive long-term development. Hence, in our view this shouldn't be a roadblock preventing the Bank from taking rates higher, particularly in an environment of excess demand and rising core inflation.

Despite some wrinkles, today's jobs report was overwhelmingly solid and points to economic growth ending the year on a solid footing. This is important as a sharp hike in Ontario's minimum wage took effect on January 1st, casting a shadow on the labour market outlook. For a data dependent Bank of Canada, across-the-board labour market strength in December likely seals the deal on a January rate hike, though one potential fly in the ointment could be the upcoming winter Business Outlook Survey (out Monday January 8th). However, a very weak report would probably be needed to dissuade a January move. We do not view this as a likely outcome given a healthy labour market, rising inflation and a solid economic backdrop during the survey period. As such, we look for the Bank to take rates higher on January 17th. That would certainly be an interesting way to ring in the New Year.

U.S.: Upcoming Key Economic Releases

U.S. Consumer Price Index - December

Release Date: January 12, 2018

Previous Result: 0.4% m/m, core 0.1% m/m

TD Forecast: 0.1% m/m, core 0.2% m/m

Consensus: 0.2% m/m, core 0.2% m/m

We expect headline CPI inflation to moderate to 2.1% y/y in December, with prices up a seasonally adjusted 0.1% m/m. Energy prices should be a net positive, led by higher gasoline prices but partially offset by higher natural gas and electricity prices. We maintain a cautious view on grocery prices, which have declined in the prior four months. Excluding food and energy, we expect core CPI to print a 0.2% m/m increase after disappointing with a relatively weak 0.1% rise in November. Much of the prior month's weakness, notably in hotel prices, airfares, and physician's services, is likely to reverse, with the exception of apparel. Our forecast suggests core inflation should stabilize at 1.7% y/y. Going forward, USD weakness and rising commodity prices should provide a net tailwind and allow core prices to firm gradually over the course of 2018.

U.S. Retail Sales - December

Release Date: January 12, 2018

Previous Result: 0.2%, ex-auto 0.1%

TD Forecast: 0.2%, ex-auto 0.1%

Consensus: 0.5%, ex-auto 0.4

We expect retail sales to rise 0.2% in December, a relatively modest gain but consistent with Q4 real consumer spending near a robust 3%. Motor vehicle sales are likely to be a small positive, in line with the better than expected pickup in light weight auto and truck sales (17.8m vs 17.4m previously). Gasoline station receipts will likely make a neutral to negative contribution due to lower gasoline prices, while the cold snap in winter temperatures suggests a hit to spending on building materials and at restaurants. We also expect a modest 0.1% rise in the control group (excluding auto, gasoline station, food services and building material sales), mostly reflecting a moderation following the unsustainable strength in the prior three months.

Canada: Upcoming Key Economic Releases

Canadian Business Outlook Survey

Release Date: January 8, 2018

The BOS will balance an positive assessment of business conditions against the persistent threat of restrictive trade measures. We expect firms to note an increase in foreign demand on stronger growth south of the border, though concerns over the future of NAFTA may receive more prominence after a contentious turn in negotiations. Ongoing competitiveness challenges may also receive mention after a sharp cut to the US corporate tax rate. After the last survey noted an increase in the intensity of labour shortages, any notion of labour market slack will be downplayed amid the creation of another 193k jobs over the last three months. Firm-level inflation expectations could also edge higher to reflect recent strength in CPI. On balance, we expect the report to deliver a constructive tone which should clear the way for the Bank to hike in January.

Canadian Housing Starts - December

Release Date: January 9, 2018

Previous Result: 252k

TD Forecast: 225k

Consensus: N/A

Housing starts are forecast to slow to a 225k pace into year-end, reflecting a more modest pace of multi-unit construction. Multi-unit starts hit their highest level on record in November and are unlikely to sustain such a pace in light of a more sluggish demand environment. As such, we expect a pullback in multi-family starts to drive the headline result. Single family starts should prove more stable though a blanket of cold weather will weigh on construction for all home types.

Chart: Canadian Employment

Dollar Fails to Gain Traction Despite Positive Inflation Signs

US hourly wages went up 0.3% in December

The US dollar is lower against major pairs only appreciating against the CHF and the JPY. The greenback got a small boost from the release of the U.S. non farm payrolls (NFP). The US added 148,000 well below expectations but with the hourly wages rising 0.3 percent but that was not good enough to counter positive economic indicators released in Europe and the stronger jobs report in Canada.

- UK monthly manufacturing production forecasted to rise by 0.3%

- US inflation could continue positive trend after NFP

- US retail sales expected to show strong December gains

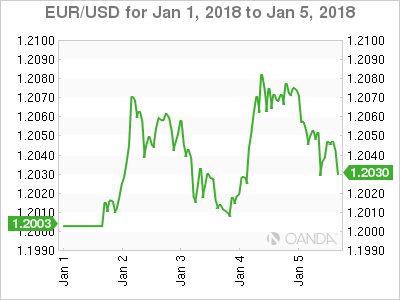

The EUR/USD advanced 0.34 percent during the week. The single currency is trading at 1.2046 after economic data in Europe supported the euro. German retail sales beat the 1.0 percent improvement forecast with a 2.3 percent advance. Inflation estimates in the EU were flat at 1.4 percent, with the core falling slightly to 0.9 percent. Although lower than expected the fall in inflation validated the guidance from the European Central Bank (ECB). Without pressure from rising inflation the ECB can keep the German and Dutch members at bay with their calls urging for a quicker end of QE. German retail sales alongside inflation data released last week does show why German policy makers are worried given the strength of the currency.

The awaited release of the U.S. non farm payrolls (NFP) did little for the US dollar as fewer than the 190,000 jobs were added (148,000) and although there were some positive signs of inflation with hourly wages climbing 0.3 percent it was not enough. Employment has been one of the strongest pillar of the US economic recovery after the 2008 crisis, but as time wears on there are fewer people available to be employed so the gains will be limited. Inflation remains subdued and the U.S. Federal Reserve is divided on the pace of rate hikes in 2018.

There is few probabilities of a rate hike in January, with a lot of the anticipation surrounding the March Federal Open Market Committee (FOMC) which will be the first of Jerome Powell as chair of the central bank.

The economic calendar for the EUR/USD will be focused on US retail sales and inflation that will be released on Friday, Jan 12 at 8:30 am EST. Inflation is expected to come in lower putting some pressure on the Fed to slow down its path of rising rates, but retail sales are anticipated to show an improvement in December.

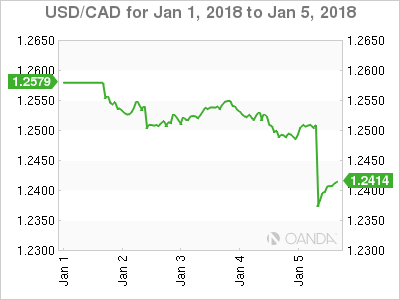

The USD/CAD lost 1.37 percent in the last five days. The currency pair is trading at 1.2407 after Statistics Canada released the December jobs report. The Canadian unemployment rate fell to its lowest reading in 40 years on Friday. The number of jobs added to the economy in December was 78,600 much higher than the forecasted 1,000. The monster gain has prompted Canadian financial institutions to update their forecasts for the January policy meeting of the BoC with the majority expecting a rate hike. The loonie continued rising after the slow start to the year of the US and the boost from higher oil prices.

The solid job report is another sign that the Canadian economy is going strong. Governor Poloz has not denied that interpretation but he was also careful to keep a neutral tone when he spoke in December. The market has now moved to predicting a rate hike in the January 17, but it will be Stephen Poloz who makes the final call. Heavy in his mind will be the fate of NAFTA. Poloz has shown that he is not afraid to be proactive as he cut interest rates twice in 2015 to shield the Canadian economy from the worst of the oil price crash. With the efforts form the Organization of the Petroleum Exporting Countries (OPEC) and strong growth, those 50 basis points were added back to the benchmark rate.

NAFTA remains a bigger puzzle than the oil market given that its fate its tied to the Trump Administration. The victory of the tax reforms is now in the past and NAFTA could provide a rolling thunder for the administration as ending the agreement could be done unilaterally by the White House. The effect is hard to quantify for Canada and even the United States which is why Poloz has chosen not to speculate until a reaction is needed. The decision of the BoC will take that uncertainty into consideration so it would also not a surprise if the central bank decides to stand pat, despite the strong indicators of late.

The Canadian economic calendar will be brief with a focus on housing. The Bank of Canada (BoC) will release its business outlook survey on January 8 at 10:30 am EST. Housing starts will be published on January 9 at 8:15 am EST, building permits on January 10 at 8:30 am and the New House Pricing Index (NHPI) on January 11 at 8:30 am EST.

The price of West Texas Intermediate is trading at $61.45. The oil rally is finding it hard to continue as US production is ramping up. The Organization of the Petroleum Exporting Countries (OPEC) agreement with other major producers stabilized prices and its extension to the end of the year set the foundation near the $50 price level, but disruptions based on weather and geopolitical events have driven the price to 2 year highs.

Iranian unrest, storms in the US and the outage of the Forties pipeline are keeping prices at current levels, but demand has remained stagnant and prices could fall once again once those temporary issues are sorted and higher production from Brazil, Canada and the US threatens to put downward pressure on the price of energy.

US crude inventories to be release on Wednesday, January 10 at 10:30 am EST will shed more light on demand and will impact the price of a barrel of oil as US shale production is ready to kick into a higher gear in 2018.

Market events to watch this week:

Wednesday, January 10

- 4:30am GBP Manufacturing Production m/m

- 10:30am USD Crude Oil Inventories

- 7:30pm AUD Retail Sales m/m

- Thursday, January 11

- 8:30am USD PPI m/m

- 8:30am USD Unemployment Claims

- Friday, January 12

- 8:30am USD CPI m/m

- 8:30am USD Core CPI m/m

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

All times EDT

Week Ahead – US Inflation & Retail Sales and Chinese Trade Numbers Among Next Week’s Highlights

The coming week will feature numerous important releases that definitely have the potential to lead to notable movements in forex markets, though it will lack a release of the magnitude of the US nonfarm payrolls report that hit markets during this past week. Among the highlights in the coming days will be Chinese trade data, eurozone unemployment figures, UK manufacturing output and US inflation and retail sales.

Quiet week in Australia with building approvals and retail sales gathering attention

The only major releases out of Australia will pertain to building approvals and retail sales, both for the month of November. The former is due on Tuesday while figures on retail sales will be made public on Thursday. Approvals to build new homes rose to their highest in eight months in October, beating expectations for a decline and raising hopes for an increase in overall economic activity, while retail sales also stormed past analysts' projections in October, boosting sentiment in the economy. It remains to be seen whether positive momentum will be maintained. Both releases have the capacity to spur positioning on the aussie. New Zealand will not see the release of major data in the coming week.

Producer & consumer price data and trade numbers out of China; Japanese current account figures due

Data on December producer and consumer prices are due out of China on Wednesday. Year-on-year, PPI is expected to stand at 4.8%, its lowest since November 2016. This compares to the 5.8% recorded in November, a then four-month low coming on the back of softer factory activity as a result of the government's efforts to reduce pollution as part of its goal to shift focus to the quality of growth rather than merely the quantity. CPI is anticipated to came in at 1.9% y/y. It grew by 1.7% in November.

Remaining in China, Friday will see the release of December trade data. In November, both exports and imports blew past expectations, growing by double digits on an annual basis. It would be interesting to see if there is continuity in upbeat data. Lastly, it is increasingly the case that rising debt levels are a topic of discussion in the world's second largest economy and December loan data out next week will also be eyed; these though are due between January 10-15, lacking a specific release date. Besides the yuan, the Australian dollar, which is considered a liquid proxy for China's economy due to the two nations' strong economic ties, will also be in focus ahead of and in the aftermath of the above releases.

Of most interest out of Japan is expected to be current account numbers for the month of November. Those are scheduled for release on Thursday (Friday morning Japanese time).

Eurozone unemployment figures, business surveys and retail sales on the agenda; UK house prices and manufacturing output

Numerous eurozone business and consumer surveys are scheduled for release on Monday. Those include January's Sentix index, gauging investors' sentiment for current conditions and expectations for the coming months, the European Commission's December business climate and economic sentiment surveys, as well as the final reading on December consumer confidence. Eurozone retail sales figures for the month of November will be made public on the same day, while industrial orders out of Germany, the eurozone's – and Europe's – largest economy, will also be released earlier in the day. Beyond these, Germany will see the release of industrial output and trade figures – exports, imports and trade balance – on Tuesday.

The eurozone's November unemployment rate is projected to fall by 0.1% relative to October, matching its lowest since January 2009 of 8.7% and pointing to a labor market that continues to improve. A positive surprise could instill further confidence in the eurozone growth story, leading to long euro positions.

Concluding the week in terms of eurozone releases will be Thursday's data on industrial production for the month of November.

Moving to the UK, it will be a mostly quiet week with data on house prices due on Monday and manufacturing output due on Wednesday gathering most attention. Analysts expect the Halifax house price index to show house prices rising for the sixth straight month in December, albeit at a weaker pace. Manufacturing output expanded for the sixth consecutive month in October – the longest stretch in decades – kindling hopes that the British industry could be in for a strong performance in 2018 despite analysts predicting a slowdown in economic activity. Wednesday's release on November manufacturing production will shed light on whether factories will continue to defy downbeat forecasts on the UK economy. Forex market participants will place their sterling positions accordingly. Data on industrial output and figures on the goods trade balance will also be released alongside manufacturing output numbers.

US inflation and retail sales in focus; Canadian housing starts due

Friday will see the release of important data out of the US as December inflation figures and retail sales for the same month will be hitting the markets; both releases are due at the same time. Month-on-month, the pace of inflation growth is expected to ease to 0.2% from November's 0.4% and come in at 2.2% on an annual basis, the same rate as in the previous month. Year-on-year, core CPI is forecast to expand at a slightly faster pace in December after slowing down a bit in November. Although the Federal Reserve's preferred inflation measure is the core personal consumption expenditures (PCE) price index, next week's CPI figures still have their significance and they could spur speculation on the outlook for interest rates and thus result in dollar movements.

Turning to retail sales, those are expected to grow at a slower pace in December after expanding by 0.8% in the month that preceded, far outstripping expectations and pointing to a robust economy. Retail sales excluding automobiles are also anticipated to ease in December. Other data out of the US in the coming week will include November figures on consumer credit and JOLTS job openings as well as December PPI numbers.

Weekly Focus: Inflation Figures in Abundance

Market movers ahead

- In the US, we estimate core CPI inflation stood at 1.7 in December.

- In the euro area, the minutes from the ECB's December meeting are the highlight next week. We intend to look primarily for nuances in the assessment of the new staff projections, in particular on inflation.

- We estimate Chinese CPI inflation rose to 1.9% y/y in December.

- In the Nordic countries, inflation is in focus and we are set to get December figures for Denmark, Sweden and Norway.

- In Sweden, we also get the Riksbank Minutes from the previous meeting, which we hope will reveal a discussion on property prices and the importance that Board members attach to recent developments.

Global macro and market themes

- 'Reflation' beliefs have been spurred anew by a continued strong global cyclical stance, the enactment of the US tax reform and commodity-price rises. However, we doubt that 2018 will be the year when the global economy 'reflates', despite what looks like a benign growth environment near term.

- Central bank pricing appears increasingly aggressive in our view and we see potential for eventually fading 'reflation' hopes to postpone expectations for a first ECB hike, while the case for a Fed March hike could stay alive for now. This should send EUR/USD firmly below 1.20 in Q1.

Job Gains Slow to End 2017 Amid Solid 2018 Growth Start

Hiring slowed to 148,000 jobs in December, with the unemployment rate steady at 4.1 percent. Demand for labor remains strong, but sustaining 3 percent GDP growth will be difficult due to labor supply challenges.

Slower Hiring in December, But Trend Still Strong

Nonfarm payrolls came in a bit softer than expected for December, with employers adding 148,000 jobs over the month (top graph). Over the past three months, job gains averaged 203,700, which looks consistent with the 2.5-3.0 percent growth we expect to see in the first half of 2018. We continue to expect the FOMC to raise the fed funds rate again in March.

The weaker outturn in December can be traced to the service sector. Notably, retail employment fell by 20,000 jobs in December as the industry continues to adjust to changing buying patterns both on a seasonal and long-term basis. Hiring also slowed in transportation & warehousing, professional & business services and education & health relative to November. Hiring in the goods-producing sector held up better, rising by 55,000 amid solid gains in construction and manufacturing.

Beyond Nominal Wages: The Real Consumer Income

To get closer to 3 percent GDP growth, the demand side of the economy will need to be sustained by real income and thereby consumer spending. Average hourly earnings rose 0.3 percent in December. That pushed the 12-month gain up to 2.5 percent. For 2017 as whole, average hourly earnings grew 2.6 percent, the same as in 2016.

Moderate inflation has helped to generate real gains in average hourly earnings over the past few years, supporting household income and spending. When combined with aggregate hours worked (which takes into account payroll gains), real labor income looks to have picked up to about a 3.5 percent annual rate over the past three months.

We do not believe that recent months' weakness in hourly earnings suggests wage growth is stalling out. Broader compensation gains, including one-off bonuses or more generous benefits, have led a clearer uptrend in the Employment Cost Index over the past year (middle graph). Average hourly earnings can be somewhat noisy, but demand for workers remains strong and should generate some upward pressure on wages in the current year.

Will Labor Force Participation Rates Rise to Support 3 Percent?

Supply may be the bigger challenge for the coming year. The unemployment rate held steady at 4.1 percent, the third month in a row it has done so. However, we expect the rate to trend downward to 3.8 percent by the end of the year as total employment outpaces growth in the labor force. In 2017, 1.79 million jobs were added, while the civilian labor force increased by just 861,000 – we expect these tightening dynamics to continue.

Digging a little deeper, it is clear that structural issues persist. For example, while the labor force participation for men is higher than for women, growth in the prime age participation rate has only been experienced by women (bottom graph). These growth dynamics, or lack thereof, will pose a challenge to achieving sustained 3 percent growth.

Widening Trade Deficit Will Exert Drag on GDP Growth in Q4

The trade deficit widened markedly in the last two months of 2017. Consequently, real net exports likely exerted a significant drag on overall GDP growth in the fourth quarter.

Deficit Widens as Imports Jump More than Exports

The U.S. trade deficit widened to $50.5 billion in November from $48.9 billion in October (top chart). Not only was the outturn a bit higher than most analysts had expected, but it was the first time that the deficit has exceeded $50 billion since March 2012. Although exports of goods and services jumped by 2.3 percent in November, imports were up 2.5 percent.

There was broad-based strength on the export side of the ledger. The $2.5 billion increase in the export of capital goods was flattered by the $1.2 billion jump in exports of civilian aircraft, which can be volatile on a monthly basis. This sizeable increase in overall capital goods exports in November may reflect, at least in part, some statistical payback for weakness during the previous two months. Smoothing through the monthly volatility shows that overall exports clearly have rebounded in 2017 after their weakness in 2016. The value of American exports was up 6.0 percent in the September-November period relative to the same period in 2016 (middle chart).

There was also broad-based strength on the import side of the ledger. The value of imported petroleum products was up $1.5 billion in November. This increase in the value of petroleum imports largely reflects the trend increase in oil prices that occurred during the autumn. The volume of petroleum imports edged higher in November, but they remain well off their peak of a decade ago. Imports of cell phones jumped about $1.1 billion, which likely reflects the introduction of the Apple iPhone X. These one-off factors notwithstanding, import growth also strengthened over the course of 2017. Some of the increase in import values reflects higher commodity prices (e.g., oil), but growth in import volumes has strengthened as growth in domestic demand has picked up.

Net Exports Probably Exerted Headwinds on GDP Growth in Q4

In real (i.e., price adjusted) terms, the trade deficit widened by $1.1 billion in November. The real trade deficit is important because it enters directly into calculations of real GDP growth. Real net exports of goods and services provided modest positive contributions to overall GDP growth in the first three quarters of 2017, but it appears that the string will end in the last quarter of the year because real net exports of goods deteriorated significantly in October and again in November (bottom chart). If real exports and real imports in December remain at their respective November levels, then real net exports would slice more than one percentage point off of the topline GDP growth rate in Q4. Although we do not expect that the overall drag will be quite that large, real net exports likely exerted significant headwinds on overall GDP growth in Q4. Moreover, we look for a modest drag from trade to continue for the next few quarters.

Sunset Market Commentary

Global core bonds traded sideways going into the US payrolls report. Mixed EMU price data were ignored and oil & equity markets gave diverging impetus for bond trading. Brent crude corrected lower towards $67/barrel while the stock market party continued. US payrolls missed consensus by a wide margin, but earnings rose in line with expectations. US Treasuries spiked higher, while the Bund was unmoved. We don't expect the uptick to last as markets mainly focus on price instead of activity data. Changes on the German and US yield curves remain limited between -1 bp and +1 bp at the moment. The 2yr/10yr US yield differential narrowed to 50 bps, the lowest level since 2007. On intra-EMU bond markets, 10-yr yield spread changes versus Germany range between +1 bp (Portugal) and -3 bps (Spain) with Greece outperforming (-8 bps).

Trading in the major USD cross rates also focused on the US payrolls. Yesterday, the dollar was in the defensive, but investors apparently found themselves positioned a bit too much USD short going into the US payrolls. Soft EMU inflation data had hardly any impact on the euro. EUR/USD traded in the mid 1.20 area just before the publication of the payrolls. Employment growth disappointed, but the key wage data were in line with consensus. The dollar spiked briefly lower upon the publication. EUR/USD jumped to the 1.2080 area, but the 1.2092 range top was again left intact. Even more, the dollar soon reversed post-payrolls losses. EUR/USD trades currently even below the pre-payrolls' level (1.2030 area). USD/JPY trades marginally below the pre-payrolls' level (currently 113.20 area). To conclude, payrolls disappointed, but the report caused hardly any damage for the dollar as price data are more important than activity data. The jury is still out, but the 1.2092 resistance again proves not that easy to break.

Risk sentiment on European stock markets remains ebullient with the German Dax posting another >1% gain, putting the YTD balance already at +3%. The Intel chip flaws can't spoil sentiment. US stock markets opened around 0.25% higher.

News Headlines

December EMU headline inflation declined in line with expectation from 1.5% Y/Y to 1.4% Y/Y, mainly due to negative energy base effects. Core CPI stabilized at 0.9% Y/Y, below 1% Y/Y consensus. Higher-than-expected November PPI readings (0.6% M/M & 2.8% Y/Y) balanced the core CPI miss from a market point-of-view. Higher producer prices might filter more rapidly through to consumer prices in a context of strong growth.

The December payrolls report disappointed. Net job growth amounted to 148k, below 190k forecasts. Taking into account revisions to the previous two months' figures results in a combined 51k miss. Bad weather wasn't to blame with less than average employees remaining home due to poor weather conditions. The unemployment rate stabilized as expected at 4.1%. Average hourly earnings, key to markets, printed as well bang in line with consensus (0.3% M/M & 2.5% Y/Y), but November data faced slight downward revisions.

The US non-manufacturing ISM disappointed in December, declining from 57.4 to 55.9 (vs 57.6 consensus).

The Canadian job market is firing on all cylinders. The number of jobs rose by 78 600 (vs 2 200 consensus) in December, bringing the full-year employment gain to 422 500. That's the best annual increase since 2002. Canada's unemployment rate unexpectedly declined from 6% to 5.7%, the lowest level in more than 40 years. Average hourly earnings climbed by 2.7% Y/Y, down from 2.8% Y/Y in November. Canadian yields shot up to 9 bps higher with the 2-yr yield now at 1.7%, the highest since 2011. The loonie profited as well. USD/CAD dropped from around 1.25 to 1.2350. The market implied probability of a January rate hike from 1% to 1.25% increased from 41% to 73%.

USDCAD Falls Over 150 Pips on Weak US and Upbeat Canada Jobs Data

USDCAD fell to the lowest levels since late Sep 2017, on over 150-pips bearish acceleration after US / Canada jobs data. The greenback came under pressure on US NFP data miss while upbeat Canada employment figures (78.6K new jobs created in December vs 1K f/c) strongly boosted the loonie. Fresh bearish acceleration today is seen as extension of bear-leg from triple-top at 1.2915 zone, which broke below significant support at 1.2387 (Fibo 61.8% of 1.2061/1.2916 ascend and is expected to confirm strong bearish signal on daily close below 1.2387. Extension of bear-leg from 1.2915 lower platform below 1.2387 pivot would open way for full retracement of 1.2061/1.2916 corrective phase in the coming sessions. Meanwhile, bears may take a breather on oversold daily studies, with extended corrective upticks expected to stay capped under daily cloud base (currently at 1.2555).

Res: 1.2432; 1.2488; 1.2513; 1.2555

Sup: 1.2355; 1.2300; 1.2263; 1.2194

Canada Adds an Impressive 79K Jobs for a 13th Straight Monthly Gain

The Canadian labour market extended its gain in December, adding an impressive 78.6k net positions. Despite more Canadians being drawn to labour markets in December, the gains were enough to push the unemployment rate to 5.7% - the lowest rate since 1974.

Part time employment led the way again, adding 54.9k net positions, but full-time employment also rose, up 23.7k for a fourth straight monthly increase and a healthy 2.7% year-on-year gain.

Jobs were mainly among employees (as opposed to the self-employed) with 50.4k added in December. These positions skewed slightly towards the private sector (+28.2k), with the public sector adding 22.1k positions. Self-employment rose 28.2k on net.

By industry, the services side of the economy led the way, adding 72.6k positions. Notable standouts were finance, insurance, and real estate (+25.0k), educational services (+11.2k) and other services (+12.6k). The goods-producing side of the economy saw a more modest 6.0k net positions added as gains in construction and natural resources offset modest weakness in agriculture and manufacturing.

Among the provinces, all saw net hiring in December, but Quebec (+26.9k) and Alberta (+26.3k) topped the leader board. December's reports were impressive for both provinces: Quebec's unemployment rate, at 4.9%, reached another record low despite a climb in the participation rate, while Alberta recorded the strongest monthly job growth since 2011.

The hourly wage rate accelerated again, reaching 2.9% on a year-on-year basis. Strength could also be seen in the hours worked, which were up 3.1% year-on-year basis, helped by a robust month-on-month gain.

Key Implications

Unbelievable. We can now chalk up 13 straight months of job gains (a post-crisis record). What's more, nearly all details of the report were solid: despite more Canadians looking for work, job growth was enough to push the unemployment rate to 5.7%, its lowest level since 1974. It seems that Canadian job markets have been going from strength to strength of late.

The strength of the labour market is perhaps best reflected in further gains in wages, where growth has been robust – the 2.9% yearly climb is a far cry from the lows seen earlier in 2017. A solid climb in hours worked also bodes well for overall economic output in December.

For Bank of Canada governor Stephen Poloz, today's data should act as a further sign that despite hiccups in some areas of the economy, the underlying trend remains healthy. While risks to the outlook remain and may temper the overall pace of rate hikes, another policy interest rate hike in the near term now seems almost certain.

Canada’s Trade Deficit Narrowed Significantly in October

Canada's trade deficit widened to $2.5 billion in November (previously $1.6 billion) as the 5.8% rise in imports outpaced the 3.7% gain in exports. In real terms, the picture was worse, with import volumes up 5.0% and export volumes rising 0.6%.

The rise in imports was widespread, with nearly all industries reporting gains. Leading the way was metal ores and non-metallic minerals (+28%), aircraft and other transportation equipment and parts (+19%) and electronic and electrical equipment and parts (+11%). The only industry in which imports declined during the month was energy products (-3.6%).

Export gains were also fairly broad based, led by a rebound in motor vehicle and parts (+15%) which had fallen in the previous four months. Consumer goods (+7%) also had a strong showing in November, rising to the highest level seen in nearly a year. However, in volume terms, exports excluding autos were soft, falling 1.4%.

Canada's trade surplus with the U.S. slid to $3.3 billion in November (previously $3.5 billion), as the rise in exports (+5.4%) trailed that of imports (+6.5%). Canada's trade deficit with the rest of the world widened to $5.9 billion (previously $5.0 billion) as imports were up 4.4% and exports were down 1.4%.

Key Implications

This was a disappointing report, but unlikely the start of a trend. The strength in imports is suggestive of a return to normality in previously disrupted sectors such as autos. Still, the outperformance of imports versus exports means that net trade will act as a drag on growth during the month, and the decline in export volumes ex-autos is not very encouraging.

Going forward, the outlook for Canada's trade picture remains bright. A healthy US economy and a loonie sitting at around the 80 US cent level should keep demand for Canadian exports propped up, helping net trade support overall growth in the coming months. The biggest risk facing exporters is the ongoing NAFTA renegotiations, which have yet to make much progress.

The Bank of Canada may be disappointed in this report, but it is more than offset by this morning's spectacular employment report, which points to a labour market with little slack. As such, after this morning's releases, the Bank will be inclined to move interest rates higher sooner rather than later.