Sample Category Title

Canada’s Unemployment Rate Plunged To Its Lowest Level Since January 1976 In December

For the 24 hours to 23:00 GMT, the USD declined 0.67% against the CAD and closed at 1.2407 on Friday.

The Canadian Dollar gained ground against the USD, after stronger-than-expected data on Canada's labour market boosted odds for a January interest rate hike.

Data revealed that Canada's unemployment rate unexpectedly fell to a four-decade low of 5.7% in December, on the back of a surge in job creation, thus highlighting a rapidly diminishing slack in the nation's labour market. In the prior month, the unemployment rate had recorded a level of 5.9%, while market participants had envisaged for a rise to a level of 6.0%.

Other data showed that Canada's seasonally adjusted Ivey–PMI fell to a level of 60.4, compared to a reading of 63.0 in the previous month. Moreover, the nation's international merchandise trade deficit surprisingly expanded to C$2.54 billion in November, after recording a revised deficit of C$1.55 billion in the prior month and confounding market expectations for the nation's trade deficit to narrow to C$1.13 billion.

In the Asian session, at GMT0400, the pair is trading at 1.2397, with the USD trading 0.08% lower against the CAD from Friday's close.

The pair is expected to find support at 1.2331, and a fall through could take it to the next support level of 1.2265. The pair is expected to find its first resistance at 1.2488, and a rise through could take it to the next resistance level of 1.2579.

Going forward, the Bank of Canada's (BoC) business outlook survey report, scheduled to release later in the day, would be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

German Manufacturing Orders For November Are Due Out

Market movers today

NEW RESEARCH WEBSITE: We have launched a new research website, with all our research across asset classes and countries.

We are heading for a quiet er week in terms of data where inflation takes centre stage after activity numbers were in the spot light last week. On Wednesday, inflation is due out from China, Denmark and Norway followed by inflation releases for the US and Sweden on Friday.

Focus this week will also turn to the scheduled meeting between North and South Korea tomorrow to see if the apparent easing of tensions can be sustained and if it can pave the way for talks between the US and North Korea. There are doubts, though, as to whether North Korea are serious about the talks.

Make-or-break talks on forming a German government between CDU/CSU and SPD began on Sunday and continue this week. If the exploratory talks find enough common ground, the SPD leaders will ask for a party convention on 21 January to back full-fledged negotiations.

This morning, German manufacturing orders for November are due out , which are estimate by consensus to be flat m/m after a 0.5% m/m increase in October . The monthly changes are very volatile but the underlying trend is robust and supports the picture of strong manufacturing activity.

Todays' batch of confidence numbers from the EU Commission is expected to show a similarly strong development . Euro area retail sales should have rebounded in November after a fairly big drop in October.

Finally, we look for a 0.5% rise in Norwegian industrial production for December, taking the annual increase to 2.5% y/y – the highest level since March 2015.

Selected market news

Market sentiment continues to be strong with further decent increases in stock markets on Friday. The Japanese market is closed today but other Asian markets continued the positive trend this morning. The US labour market report on Friday was on the soft side, suggesting that the Fed will continue to move slowly this year. On inflation, stock markets are seeing the best of all worlds at the moment with robust increases in producer prices feeding into profits, but with limited pass-through to consumer price inflation, which could make the Fed step on the breaks.

Former White House st rategist Steve Bannon yesterday issued an apology over his comments in the book ‘Fire and Fury: Inside the White House' published on Friday, see Reuters.

Over the weekend, China FX reserves for December showed a bigger increase than expected. Reserves rose by USD20bn to USD3,139.9bn – the 11th increase in a row. USD/CNY is again trading close to the September lows below 6.5 after CNY has st rengthened over the past three weeks in parallel with the general USD weakness over the same period.

Daily Wave Analysis: EUR/USD Bearish Price Action Testing Wave 4 Fibonacci

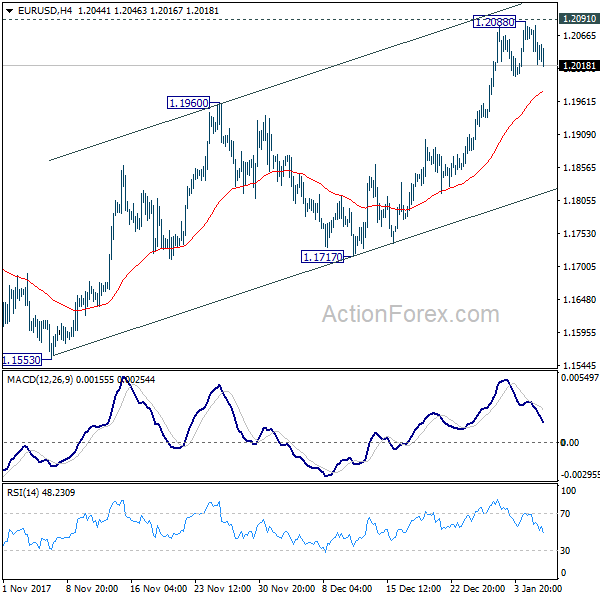

Currency pair EUR/USD

The EUR/USD seems to be building a bearish correction within a larger uptrend continuation where waves 3 prevail. The alternative is that price is not completing a 123 (pink) but a larger ABC correction. A break below the support trend line (blue) makes a bearish scenario more likely whereas a break above the top (red) makes a continuation more likely.

The key support zone for the EUR/USD are the Fibonacci levels of wave 4 vs 3. A break below the 50% Fib makes a wave 4 (blue) unlikely.

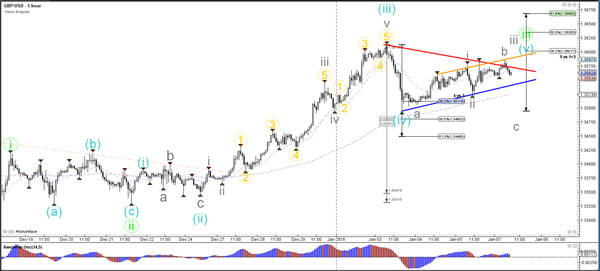

Currency pair GBP/USD

The GBP/USD is building a retracement within the uptrend. A break above the resistance trend line (red) could see price move towards the Fibonacci targets.

The GBP/USD is either building a 123 wave pattern or ABC correction depending on the breakout direction versus the trend lines.

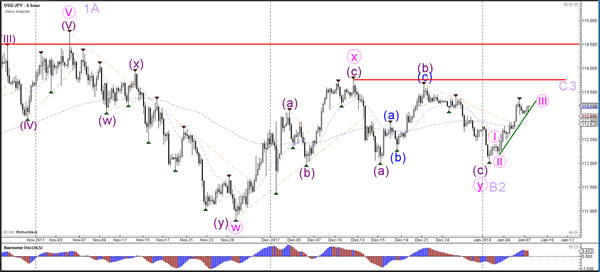

Currency pair USD/JPY

The USD/JPY is moving higher towards the next top (red). A break above this resistance level could be the start of a larger bullish push higher.

The USD/JPY uptrend is indicated by the bullish trend channel (green).

Market Update – Asian Session: China Foreign Reserves Gain For 11th Consecutive Time

Headlines/Economic Data

General Trend: Asian markets trade generally higher after Friday's gains in the US

Property developers in China and Hong Kong outperform amid release of Dec sales figures

Chinese cement names (Anhui Conch, China Res Cement ) raise FY17 outlooks on higher prices

South Korea steps up currency warning: Korean Won (KRW) weakens ahead of Tuesday’s expected talks with North Korea

Japan

Nikkei 225 closed for holiday

Fast Retailing: Reports Dec Uniqlo SSS +18.1% y/y (includes online sales); cites factors including cold weather conditions (from Jan 5th after close)

Korea

Kospi opened +0.5%

Automakers gain: Hyundai Motor +0.9%, Kia +1.1%

Chipmakers trade mixed: Samsung Electronics flat, Hynix -1%

General strength among financials and chemicals: KB Financial +4%, Lotte Chemical +8%, LG Chemical +3.5%

LG Electronics, 066570.KR Reports prelim Q4 (KRW)Op 366.8B v 464Be; Rev 16.97T v 16.3Te

(KR) South Korea reiterates will take steps if one-sided moves are seen in FX market; to take steps 'sternly' in case of drastic move in FX; Amid the comments, USD/KRW is now moving higher on the session, currently +0.4%, speculation that South Korea officials may have intervened on today's session by purchasing US dollars (USD) in order to slow the rise of the Korean Won (KRW)

(KR) Bank of Korea (BoK) sells KRW600B in 6-month monetary stabilization bonds: yield 1.60%

(KR) Bank of Korea (BOK) banks are likely to tighten their rules on household loans in Q1 of this year amid a recent trend of rising interest rates

(KR) South Korea Finance Ministry: finalized the details on a tax code overhaul whose main features are the levying of an additional tax on owners of multiple homes, a move intended to curb rising housing prices, and the raising of the highest corporate income tax rate

(KR) South Korea official: special investigation will be implemented on virtual accounts used for cryptocurrency deals, as part of the government’s recent pledge to crack down on excessive speculations

Looking Ahead: LG Electronics may report prelim Q4 results later today; Samsung Electronics may report prelim Q4 results on Tuesday

South Korea and North Korea expected to hold talks on Tuesday which are expected to cover the Winter Olympics and other issues

China/Hong Kong

Hang Seng opened -0.1%, Shanghai Composite -0.2%; Shanghai markets later pare losses

Hang Seng Property/Construction Index +1.8%; Financials -0.5%

China airlines trade broadly higher: China to permit airlines to independently set prices for top routes – US financial press

(CN) China NDRC: China to support merging of coal and electricity companies, sector names stronger on the news from Friday

(CN) PBOC has asked banks to let foreign firms freely remit yuan profits, dividends - China Daily

(CN) China Hebei province planning to cut 6.0Mt steel capacity in 2018 - Chinese press

(CN) China NDRC: China to support merging of coal and electricity companies

(HK) Hong Kong Monetary Authority (HKMA) Chan: As of Nov Hong Kong home prices 101% above the 1997 peak

(CN) CICC sees PBOC raising interest rates by 25bps in 2018

(CN) China PBOC deputy head of research Ji Min: There is room for an increase in interest rates in the short term as industrial product prices and enterprises' profitability have improved since last year - China Daily

(CN) Chinese Academy of Social Sciences (CASS) expected China's economy to post stable growth in 2018 and expand by around 6.7% from 2017, despite headwinds from both home and abroad - China Daily

(CN) China PBoC: Skips OMO for 10th straight session; Net drains CNY40B v CNY130B prior

USD/CNY (CN) China PBoC sets yuan reference rate at 6.4832 v 6.4915 prior (strongest yuan fix since May 2016)

(CN) China Dec Foreign Reserves: $3.140T v $3.127Te (highest since Sept 2016, 11th consecutive gain, biggest gain since July); 2017 FX reserves rose $129.5B to $3.1405 v $3.011Tin 2016 (first annual rise since 2014)

1169.HK Reports FY17 Pretax CNY30B, +41% y/y; Rev CNY241.9B, +20% y/y

HNA Holdings -2.5%: HNA units said have missed payments to more China banks – press

Australia/New Zealand

ASX 200 opened +0.3%; closed +0.1%

ASX 200 REIT Index +0.6%, Financials +0.2%

(AU) Australia Dec Foreign Reserves (A$): 85.4B v 85.8B prior

(AU) Australia Department of Industry, Innovation and Science quarterly Resources and Energy report made near-term changes to the iron ore price outlook but kept longer-term projections unchanged

(AU) Australia Dec AiG Performance of Construction Index: 52.8 v 57.5 prior

Looking Ahead: Australia Nov Building Permits due to be released on Tuesday

Other Asia

(TW) Apple supplier LARGAN Precision -4.5%: Reports Dec Rev NT$4.88B, -10.4% y/y

2409.TW Reports Dec Sales NT$25.8B, -17.1% y/y

North America

(US) S&P 500 companies are expected to report Q4 y/y earnings growth of 10.5%, revenue growth seen at 6.7% - Financial Times; Earnings growth is expected to be led by Energy, Materials and Technology sectors

(US) Pres Trump: will try to get a bipartisan deal on welfare reform or will hold the issue for a later time - meeting with GOP leaders at Camp David; Hopefully economic advisor Gary Cohn will be staying for a long time

(US) Fed's Williams (2018 voter): Reiterates three rates hike in 2018 makes sense - financial press interview

(US) White House chief economist Hassett: Fed would not need to tighten policy at a faster rate in response to recently passed tax cuts - American Economic Association; White House modelling shows the economic effects of the tax plan result in interest rates that are not inconsistent with the Fed’s current guidance.

Celgene: Confirms to Acquire Impact Biomedicines for $1.1B upfront and up to $1.25B in contingent payments, Adding Fedratinib to Its Pipeline of Novel Therapies for Hematologic Malignancies

Looking Ahead: Consumer Electronics Show (CES) to be held in Las Vegas Jan 9-12

Europe

(UK) UK PM May said to plan cabinet changes, which are expected to include a cabinet minister for 'no deal' – UK Press

(EU) ECB's Weidmann (Germany, head of the Bundesbank): central bank should set a concrete date for ending its QE program; signs for inflation to return to a level that is sufficient to maintain price stability - El Mundo

(UK) UK Visa Dec Consumer Spending Y/Y: -1.0% v -0.9% prior (first Dec decline since 2012)

(SA) Saudi prosecutors confirm 11 princes were arrested for 'disturbing public order' after they staged a sit in at a royal palace

UBS CEO Ermotti: Will not discuss relationship with HNA; Wealth management business needs to continue to evolve; premature to discuss stock buybacks

ABLX.BE Rejected proposal from Novo Nordisk to acquire it for up to €30.50 per share in cash

Levels as of 01:00ET

Nikkei225 closed, Hang Seng -0.1%; Shanghai Composite +0.5%; ASX200 +0.1%, Kospi +0.5%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.3%; FTSE100 -0.0%

EUR 1.20.52-1.2012; JPY 113.27-113.02; AUD 0.7873-0.7836;NZD 0.7184-0.7161

Feb Gold -0.3% at $1,318/oz; Feb Crude Oil +0.2% at $61.55/brl; Mar Copper -0.2% at $3.23/lb

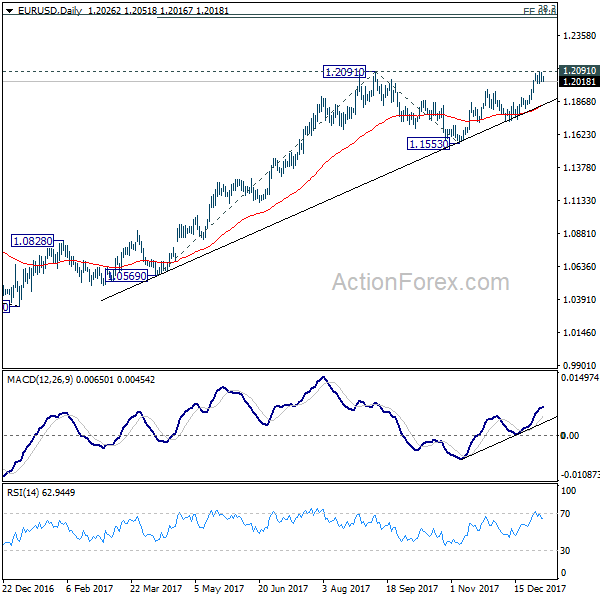

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2006; (P) 1.2044 (R1) 1.2068; More....

Intraday bias in EUR/USD remains neutral for the moment. Further rise is expected as long as 4 hour 55 EMA (now at 1.1977) holds. Firm break of 1.2091 will confirm medium term rally resumption and target next key fibonacci level at 1.2494/2516. However, sustained break of 4 hour 55 EMA will extend the consolidation pattern from 1.2091 with another decline through 1.1717 support.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

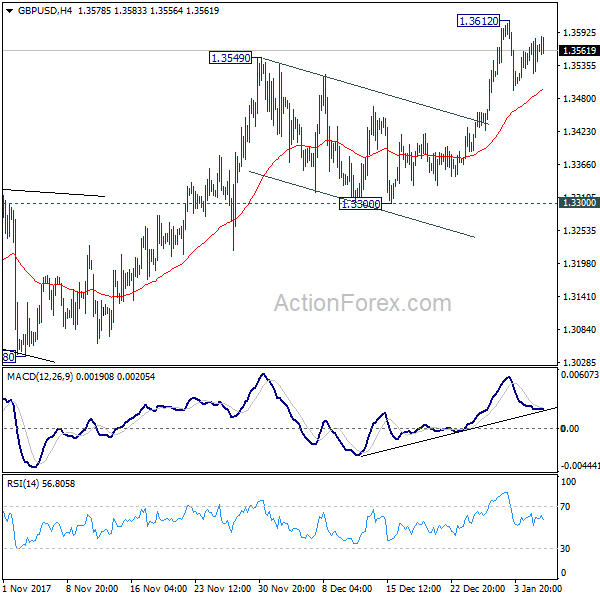

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3528; (P) 1.3555; (R1) 1.3587; More.....

Intraday bias in GBP/USD remains neutral at this point and consolidation from 1.3612 temporary top could extend. But as long as 4 hour 55 EMA (now at 1.3496) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

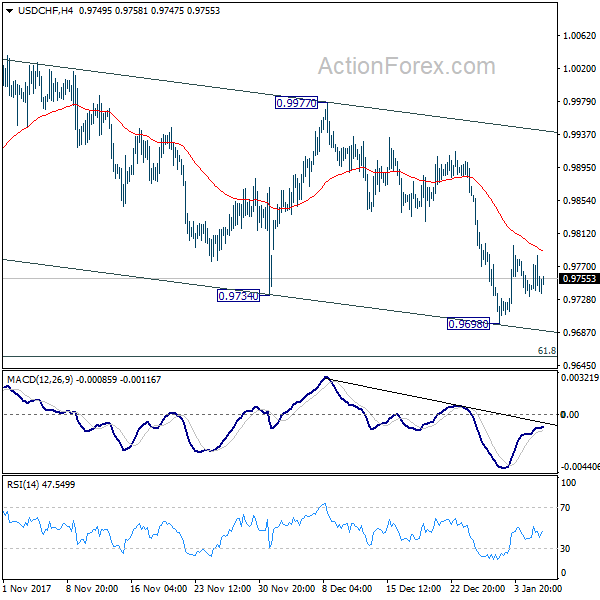

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9723; (P) 0.9753; (R1) 0.9771; More....

Intraday bias in USD/CHF stays neutral first. As long as 4 hour 55 EMA (now at 0.9789) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.73; (P) 113.02; (R1) 113.32; More...

Intraday bias in USD/JPY remains neutral at this point. Outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

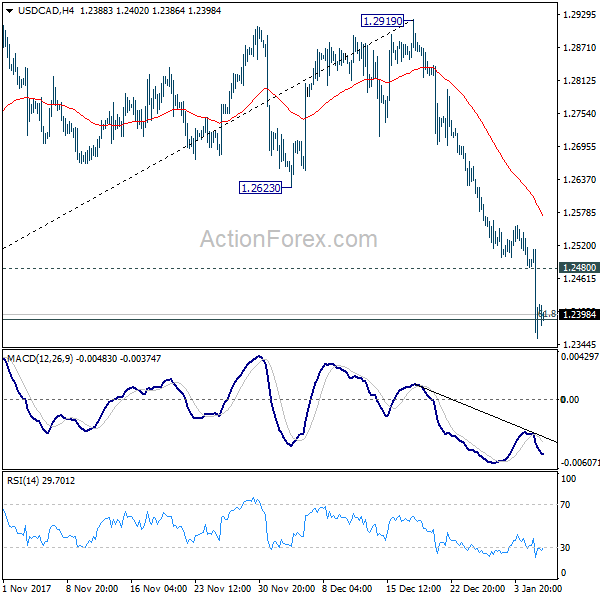

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2339; (P) 1.2425; (R1) 1.2497; More....

Intraday bias in USD/CAD remains on the downside for the moment. Current momentum argues that larger down trend from 1.4689 might be resuming. Deeper fall should be seen back to retest 1.2061 low first. On the upside, above 1.2480 minor resistance will turn bias neutral and bring consolidation before staging another decline.

In the bigger picture, current development argues that rebound from 1.2061 has completed at 1.2919, rejected by 55 week EMA (now at 1.2850) and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2929 resistance holds.

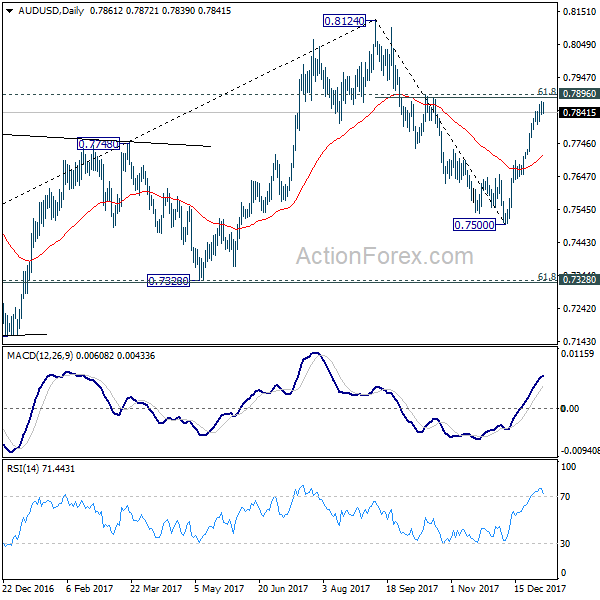

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7840; (P) 0.7857; (R1) 0.7879; More...

AUD/USD weakens today but downside is contained above 0.7804 minor support. Intraday bias remains neutral first. Considering bearish divergence condition in 4 hour MACD, even in case of another rise, upside should be limited by 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886) resistance zone to bring short term topping. Break of 0.7804 minor support will turn bias to the downside for 55 day EMA (now at 0.7711).

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is completed at 0.8124, after hitting 55 month EMA (now at 0.8032). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.