Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

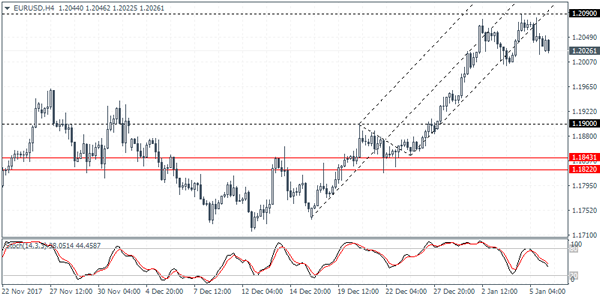

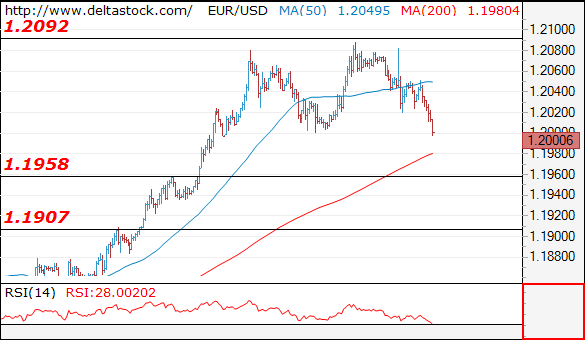

EUR/USD

Current level - 1.2006

The consecutive failures below 1.2090 hurdle signal a bearish bias, for a slide towards 1.1960, towards 1.1910 area. Minor intraday resistance lies at 1.2020.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2020 | 1.2090 | 1.1960 | 1.1910 |

| 1.2090 | 1.2240 | 1.1910 | 1.1715 |

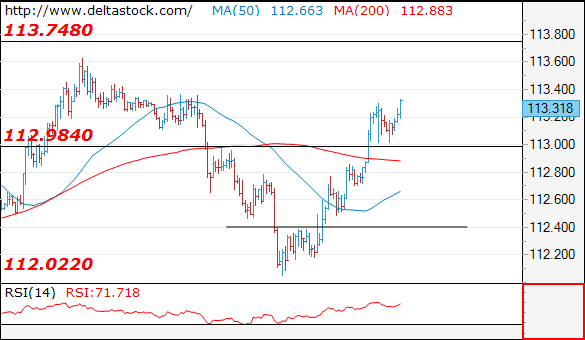

USD/JPY

Current level - 113.31

The rise from 112.00 is intact, heading towards 113.70 resistance area. Initial support lies at 112.95.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.46 | 113.75 | 112.95 | 112.00 |

| 113.75 | 114.70 | 112.00 | 111.00 |

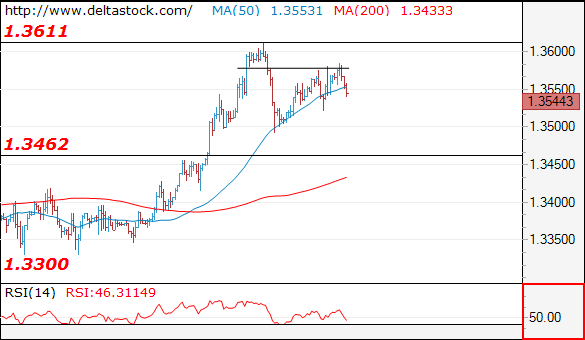

GBP/USD

Current level - 1.3544

My outlook here is bearish, for a break through 1.3520 support, towards 1.3460. Initial intraday resistance lies at 1.3580.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3575 | 1.3660 | 1.3520 | 1.3460 |

| 1.3660 | 1.3660 | 1.3460 | 1.3300 |

GBP/JPY Bearish Divergence At W L3 Camarilla Resistance

As the BoJ commenced some minor tapering to its massive Balance Sheet in the month of December, the past week has seen some strong risk-on across Commodities, Equities and JPY crosses. Manufacturing data across the major exporters are still in expansion mode, including Japan, this is good longer-term for the Nikkei, but may complicate JPY price moves. I expect a retrace to the downside on JPY pairs.

Technically the GJ is showing bearish divergence very close to weekly L3 camarilla pivot. The divergence is aligned with historical sellers and if we see a 4h close below M H3, the pair should drop faster towards 152.80- intraday targets and possibly 152.30. Continuation of the bearish drop is expected only if the pair gets below 152.30.

L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Technical Outlook: USDJPY – Bulls Probe Again Above Double Fibonacci Barrier At 113.25

The pair holds firm tone and extends recovery rally from 112.00 zone into fourth consecutive day.

Bulls probe again above cracked double Fibo barrier at 113.25 (Fibo 61.8% of 113.74/110.83 descend / Fibo 76.4% of 113.63/112.05 downleg), firm break of which would be bullish signal for final push towards key points at 113.63 (21 Dec high) and 113.74 (12 Dec peak).

Bullish daily techs continue to underpin, however, converged 10/55/20SMA which now act as initial supports at 112.97/92 zone, are moving sideways, suggesting that bulls may enter consolidative phase before resuming higher.

Daily cloud top marks key near-term support at 112.78 and break lower would generate negative signal.

Res: 113.38, 113.63, 113.74, 114.00

Sup: 113.00, 112.92, 112.78, 112.68

Dollar Recovers Following Decline Caused By NFP, Eurozone Retail Sales Due

Here are the latest developments in global markets:

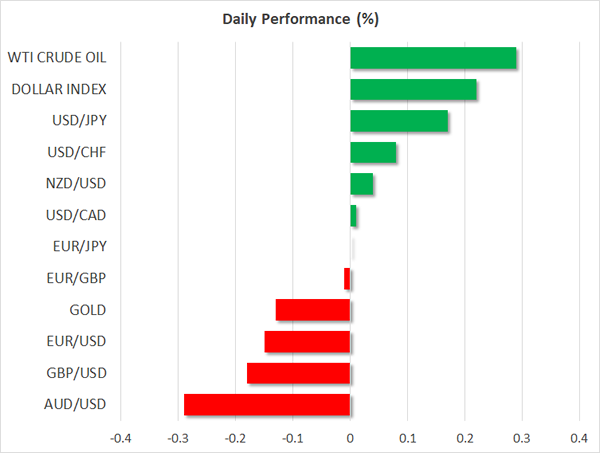

FOREX: The US dollar index traded 0.2% higher during the Asian trading session Monday, recovering the losses it posted on Friday following the slightly softer-than-anticipated US employment report.

STOCKS: In Asia, Hong Kong's Hang Seng was up 0.2% while China's CSI 300 was 0.5% higher. Meanwhile, Japanese equity markets remained closed today for the Coming of Age holiday. In Europe, futures tracking the Euro Stoxx 50 are currently up by 0.4%. The three major US equity indices – Dow Jones, S&P 500, and Nasdaq Composite – extended their recent gains on Friday, all closing at new record highs as the so-called “Goldilocks” environment of solid economic growth with subdued inflation continued to support risk appetite. As the earnings season kicks off, JPMorgan Chase, Wells Fargo and Blackrock will be among US companies reporting quarterly results this week. Futures tracking the Dow, S&P, and Nasdaq 100 are currently in positive territory.

COMMODITIES: In energy markets, WTI and Brent crude oil were up 0.3% and 0.2% respectively, likely supported by data released on Friday showing a decline in the number of active US oil rigs, even despite the recent surge in crude prices. Gold was down marginally on Monday, last trading near the $1317 per ounce zone, perhaps weighed on by the broader risk-on market sentiment.

Major movers: Dollar recovers its payrolls-related tumble; loonie flies

The US dollar index inched up by 0.2% on Monday, recovering all the losses it posted on Friday after the US employment report for December fell short of meeting market expectations. Nonfarm payrolls came in at 148k, notably less than the consensus estimate of 190k, but the previous figure was revised higher somewhat. The unemployment rate remained unchanged at 4.1% as was expected, and although the all-important average hourly earnings met their forecast of +0.3% m/m, the previous print was revised lower. Overall, these data confirmed what we already knew about the US economy; that the labor market is relatively tight, but wage growth remains subdued and thus, they are unlikely to have much impact on the Fed's thinking.

Both euro/dollar and sterling/dollar were down slightly, likely a reflection of the greenback's rebound rather than euro or sterling weakness.

The Canadian dollar skyrocketed on Friday, reaching a 3-month high against its US counterpart, after the nation's employment data for December crushed market expectations, showing that the labor market continues to tighten at a rapid pace. At the time of writing, market pricing has tilted in favor of a rate hike at the Bank of Canada's upcoming meeting in January, with the implied probability for such action resting at nearly 70% according to Canada's Overnight Index Swaps.

The antipodean currencies were mixed against the greenback, with aussie/dollar trading 0.3% lower on Monday, but kiwi/dollar being marginally higher.

Day ahead: UK house prices and eurozone retail sales among day's releases

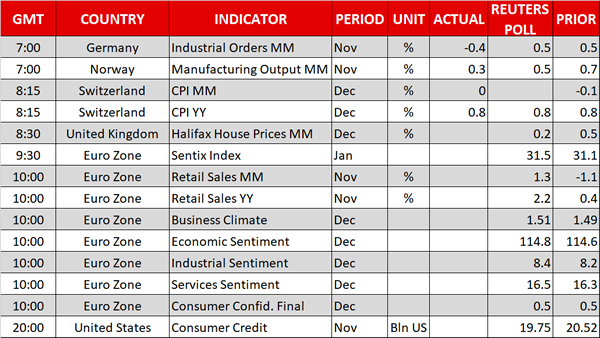

The UK will see the release of data on house prices at 0830 GMT. The Halifax house price index is anticipated to show house prices rising for the sixth straight month in December, though at a weaker pace relative to November.

Numerous eurozone business and consumer surveys are scheduled for release today. Those include January's Sentix index, which gauges investors' sentiment for current conditions and expectations for the coming months, due at 0930 GMT. The European Commission's Directorate General for Economic and Financial Affairs will later – at 1000 GMT – release its December business climate and economic sentiment surveys, as well as the final reading on December consumer confidence. Although these surveys will be gathering some attention, they're not typically major market movers.

Eurozone retail sales figures for the month of November will also be made public today at 1000 GMT. Sales are expected to reflect an acceleration on both a monthly and yearly basis.

Loonie traders might be paying attention to the Bank of Canada's survey on the business outlook scheduled for release at 1530 GMT.

Out of the US, consumer credit figures for the month of November are due at 2000 GMT.

Fed speakers making appearances today include Atlanta Fed President Raphael Bostic who will be speaking on the economic outlook and monetary policy at 1740 GMT. John Williams and Eric Rosengren, the San Francisco and Boston Fed Presidents, will also be participating in discussions scheduled to begin at 1835 GMT and 2125 GMT respectively.

Technical Analysis: EURUSD under pressure in short-term

EURUSD is on its second straight day of declines and the falling RSI indicator is pointing to negative momentum in the short-term.

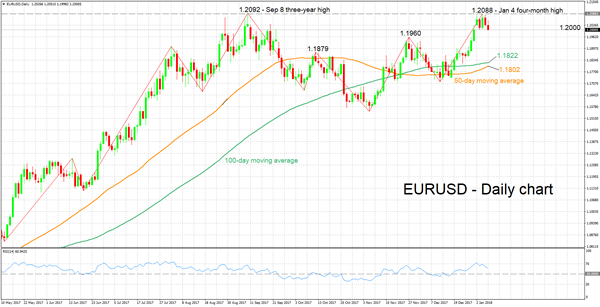

Stronger-than-anticipated eurozone retail sales figures later today could lend some support to the pair. In such an event, the area around last week's four-month high of 1.2088 is expected to act as a barrier to the upside. Notice that this level is extremely close to September 8's three-year high of 1.2092, something which perhaps increases its significance.

If on the other hand retail sales disappoint, market participants are anticipated to push the pair lower; below the 1.20 handle. The range around this level – which was momentarily breached earlier for the pair to hit its lowest since late December – seems to be providing some support at the moment. It should be mentioned that the area around this mark also encapsulates a top from the recent past at 1.1960. Further below, 1.1879 – a top recorded in October – would be eyed for additional support; the area around this level was a congested one recently as well.

Technical Outlook: GBPUSD – Repeated Failures To Regain 1.3600 Handle Turn Near-Term Focus Lower

Cable holds in red at the beginning of the week and moves lower after repeated failure to regain 1.3600 handle.

The pair hit session high at 1.3585 in early Asian trading (ticks above Thu/Fri rally’s peak at 1.3581) before starting to ease.

Overall picture remains bullish and would keep immediate focus at the upside while current congestion stays above key supports at 1.3490/83 (last week’s low / rising 10SMA).

Rising 4-hr cloud (spanned between 1.3480 and 1.3465) also underpins the action and sustained break here would generate negative signal for deeper pullback towards next strong support at 1.3420 (Fibo 61.8% of 1.3301/1.3612).

Bullish scenario requires firm break above 1.3600 zone to expose key barrier at 1.3655 (20 Sep high) the highest point of post-Brexit recovery rally.

Res: 1.3585, 1.3600, 1.3612, 1.3655

Sup: 1.3522, 1.3493, 1.3483, 1.3457

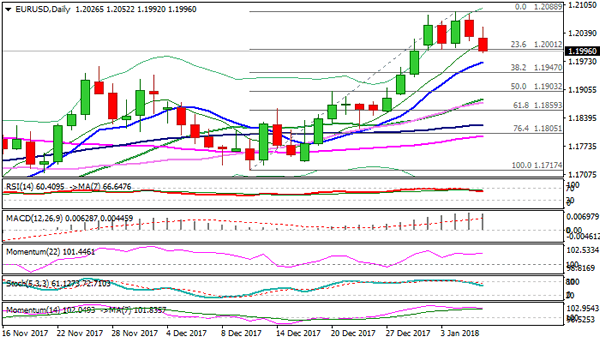

Technical Outlook: EURUSD – Signal Of Correction On Break Below 1.2000 Trigger

The Euro stands at the back foot in early Monday's trading and pressures the top of key near-term support zone between 1.2000 and 1.1970 (last week's triple-bottom / rising 10SMA).

As I mentioned in previous comments, repeated failures under pivotal 1.2100 resistance zone could result in corrective action.

The pullback was also signaled by reversal of daily RSI / slow stochastic from overbought zone.

The indicators are heading south and showing room for further extension of pullback from 1.2080 zone peaks, with sustained break below 1.2000/1.1970 to generate bearish signal.

Next good support lies at 1.1947 (Fibo 38.2% of 1.1717/1.2088 upleg, where corrective action should be ideally contained, before broader bulls resume.

Extension below 1.1947 would risk test of pivotal support at 1.1900 (daily Kijun-sen / 50% retracement) loss of which would signal reversal.

Res: 1.2000, 1.2052, 1.2088, 1.2100

Sup: 1.1961, 1.1947, 1.1928, 1.1900

Currencies: Dollar Survives Mediocre US Payrolls

Sunrise Market Commentary

- Rates: Focus on US inflation this week

US Treasuries eventually lost some ground on Friday despite disappointing headline payrolls and non-manufacturing ISM. Today's eco calendar contains EMU EC confidence data and a speech by Atlanta Fed Bostic. The latter has market-moving potential, but investors are already eying US inflation releases at the end of the week. Inflation expectations are rising. - Currencies: Dollar survives mediocre US payrolls

On Friday, the dollar was hardly affected by a disappointing US payrolls report. The overall picture of the US currency remains fragile, but EUR/USD 1.2092 resistance wasn't broken. We start the week with a neutral bias on the dollar. US price data later this week may guide the next directional move of the US currency.

The Sunrise Headlines

- US stock markets ended the week with a bang, adding 0.8% to close the first week of the year 2.3% to 3.3% higher. Asian risk sentiment remains positive overnight with Japan closed for coming-of-age day.

- San Francisco Fed Williams, FOMC voter, said that something like three rate hikes this year made sense, confirming the Fed's median view. Philly Fed Harker, no voter, revealed his dovish feathers, putting forward 2 hikes in 2018.

- Britain is pushing to remain under EU regulation for medicines after Brexit, the latest sign ministers want to stay close to Europe in some sectors despite the bloc warning the UK cannot “cherry-pick” parts of the single market.

- ECB Weidmann told Spain's El Mundo newspaper he believes setting a clear end for institution's bond-buying program is justifiable. Monetary policy will remain very expansive, even after the end of net purchases, he added.

- Faster factory inflation and higher industrial profits in the past year have created space for an increase in overall interest rates, PBOC researcher Ji Min said, according to a report by China Daily.

- China's FX reserves rose to their highest in more than a year in December ($3.14 tn), blowing past economists' estimates, as tight regulations and a strong yuan continued to discourage capital outflows.

- Today's eco calendar contains EC confidence indicators. Fed governors Bostic, Williams and Rosengren are scheduled to speak

Currencies: Dollar Survives Mediocre US Payrolls

Dollar ‘survives' mediocre payrolls

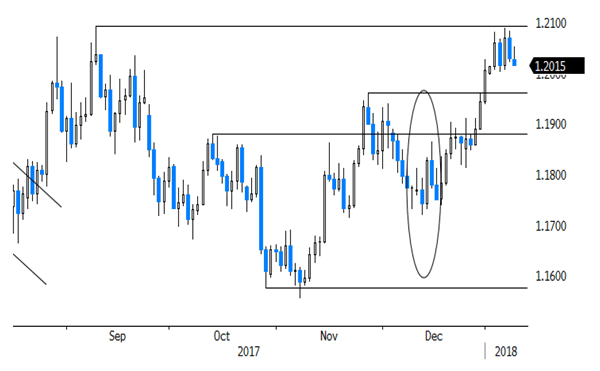

The dollar was in the defensive early last week, but regained a few ticks going into the payrolls. Investors were apparently positioned a bit too much USD short. Employment growth disappointed, but the key wage data were as expected. The dollar spiked briefly lower upon the release. EUR/USD jumped to the 1.2080 area, but the 1.2092 range top was again left intact. The dollar soon reversed post-payrolls' loss. EUR/USD even returned below the pre-payrolls' level and closed the session at (1.2029). USD/JPY failed to regain the pre-payroll level, but still closed the day in positive territory (113.05). So, the payrolls disappointed but caused little damage for the dollar.

The dollar shows no clear trend overnight. EUR/USD was initially well bid, maybe supported by hawkish comments from ECB Weidmann. However, the moved had no strong legs. EUR/USD trades again in the 1.2020 area. USD/JPY maintains a cautious bid as global risk sentiment stays constructive. The eco calendar is only modestly interesting today. EC confidence data will confirm the strong growth momentum in the region. Fed members Bostic, Williams and Rosengren speak. We keep an eye at the comments of Fed's Bostic, but don't expect them to really change the outlook on the Fed's intentions in 2018. We start the week with a neutral dollar bias. Slightly disappointing payrolls didn't cause additional damage and EUR/USD 1.2092 resistance survived. This week's US price/CPI data might be a next tipping point for the dollar. Recently, the greenback suffered as the global recovery might force other major CB's (including ECB) to join policy normalisation. For now, we maintained the working hypothesis that enough good news on the euro/'bad news' on the dollar was discounted and that a sustained break beyond the 1.2092 cycle top is not evident.

Sterling was in better shape compared to earlier last week on Friday. EUR/GBP returned below 0.89, but stayed within established ranges. This weekend, there was a lot of talk about a UK Cabinet reshuffle. If May succeeds, it might be an indication that she is regaining some grip on her party. Signs of more political stability in the UK might be slightly supportive for sterling. However, we don't see a strong case for a sustained sterling rebound (against EUR) anytime soon. GBP Medium Term: Recent UK data were mixed. We don't expect the BoE to raise rates soon. EUR/GBP 0.8700/60 support looks solid. Euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buy-on-dips in case of return action to 0.87

EUR/USD 1.2092 range top survives despite disappointing payrolls

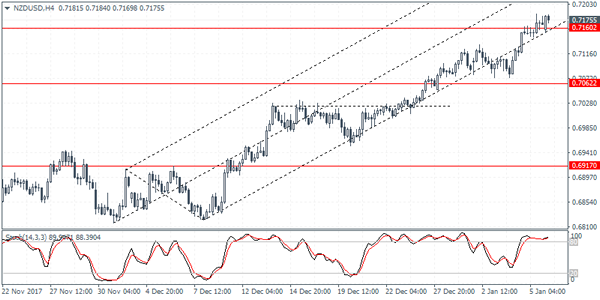

NZDUSD Intraday Analysis

NZDUSD (0.7155): The New Zealand dollar managed to complete its rally to the target area of 0.7160. Price action is showing some signs of exhaustion to the rally at this level. This is seen by the lower highs formed on the Stochastics oscillator. A convincing close below the previous low of 0.7144 could confirm the downside bias in price. The first support level that could be targeted comes in at 0.7062 which could mark the initial correction. However, further declines cannot be ruled out if price breaks down below this support. Expect to see a modest rebound off the 0.7062 with NZDUSD likely to make a lower high ahead of further declines to 0.6917.

USDJPY Intraday Analysis

USDJPY (113.21): USDJPY extended gains for three consecutive days, with Friday's session briefly rallying to highs of 113.30 before the dollar eased back to settle at 113.08. Price action remains trading within the consolidation pattern on the daily chart, as resistance at 114.07 remains a major hurdle. On the 4-hour chart, the reversal coincides with a medium-term trend line that has held on two past occasions. A continued follow through to the downside could mean that USDJPY could potentially signal declines to 112.04 level of support. The bias shifts to the upside if the currency pair can post a bullish close above the falling trend line.

EURUSD Intraday Analysis

EURUSD (1.2026): The EURUSD closed with some losses on Friday and in the process, price action formed an inside bar near the current highs above 1.20. The break out from this inside bar could potentially spell the next stage of gains or declines in the common currency. On the 4-hour chart, the EURUSD is seen falling away from the lower median line after price broke to the downside. With the exception of some consolidation taking place here, the common currency could be seen extending the declines towards 1.190 at the minimum in the near term. However, this scenario could change on a bullish close above 1.2090. This would keep the upside momentum intact although, in the longer term, the possibility of a correction to the rally remains high.