Sample Category Title

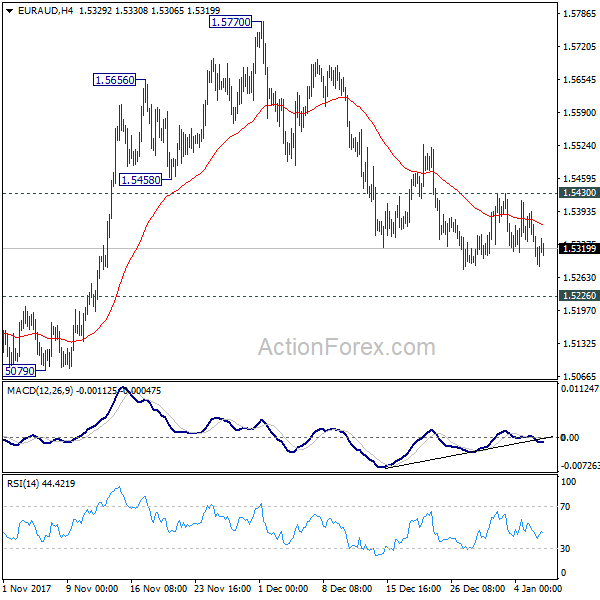

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5255; (P) 1.5324; (R1) 1.5361; More....

No change in EUR/AUD's outlook. While deeper decline cannot be ruled out, near term outlook stays bullish as long as 1.5226 resistance turned support holds. Break of 1.5430 minor resistance will now indicate completion of the correction from 1.5770 and turn bias back to the upside for retesting 1.5770. However, sustained break of 1.5226 will indicate larger reversal and target 1.4949 support next.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low). However, sustained break of 1.5226 will indicate trend reversal and target 1.3624 again.

A Critical Week For The U.S. Dollar After A Fragile Start

After having the worst annual performance since 2003, the dollar continued to struggle in the first trading week of 2018. The dollar index fell to a three-and-a-half-month low to trade below 92, leaving many traders wondering whether this year will be another devastating one for the greenback. When looking at the Commitment of Traders (COT) report, speculators are not showing interest in buying the U.S. dollar yet, and the latest groupof data did nothing to support the dollar.

Friday's jobs report did not motivate the dollar bulls to return, with non-farm payrolls rising 148,000 in December, versus expectations of 190,000. Although I think the numbers weren'tbad, and the labor market remains healthy with unemployment at 4.1%, wages are not yet showing signs of acceleration, and this remains the key missing ingredient of the U.S. economy's recovery.

The latest minutes of the Fed's meeting also showed that policymakers aren't sure whether inflation will return to the central bank's target, which is why markets believe that only two rate hikes will occur in 2018, as opposed to the three in the Fed's dot plot. This week, many Fed speakers are due to speak, including the two dissenters that were against a rate hike in December, Neel Kashkari and Charles Evans. Whether they have changed their mind, or still believe rates shouldn'tbe hiked remains to be seen, but we'll also tune into other Fed speakers for fresh insights.

If the Fed speakers don't delivernews, tier one economic releases may provide needed clues. Consumer prices and retail sales are both due forrelease on Friday. Given that energy prices spiked in December, consumer prices are expected to increase 0.2%. However, I think traders will be more interested in the core CPI figure, which strips out volatile items like food and energy. Any upside surprise in the inflation numbers will likely bring back the dollar bulls.

Given that the major U.S. economic releases are four days away, many traders will focus on whether any technical breakouts will occur. EURUSD failed to break above 1.2092 (2017 high) last week, but a successful breakout will likely lead to further buying of the single currency, towards 1.22. Similarly, Sterling is only 100 pips short of 1.3656 (2017 High). So traders should keep a close eye on these levels.

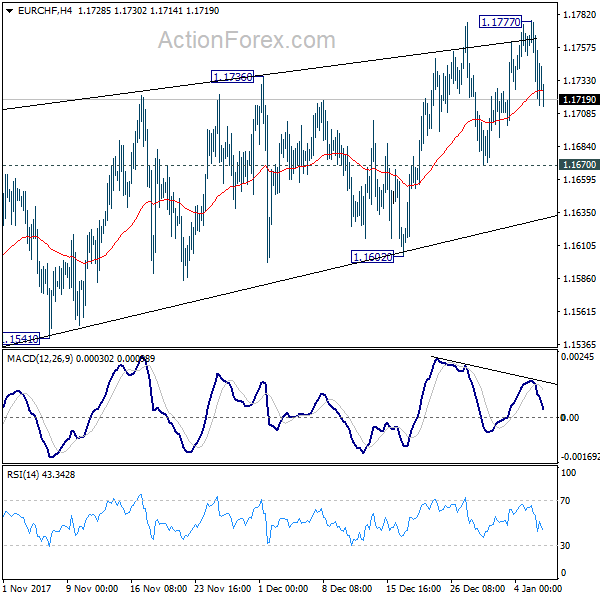

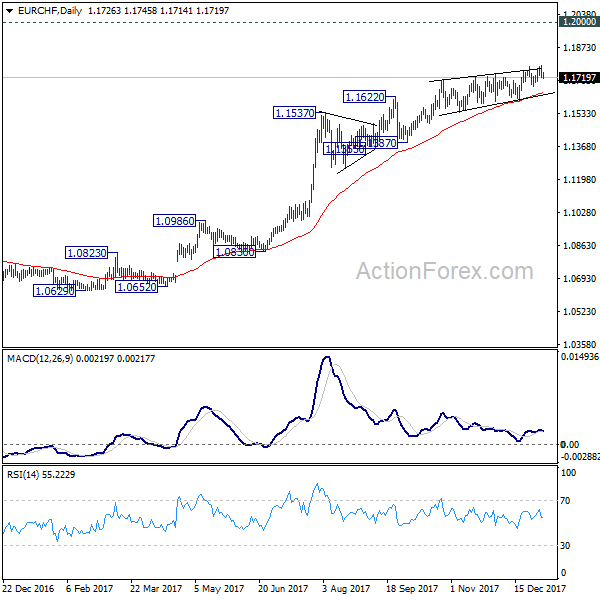

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1701; (P) 1.1740; (R1) 1.1759; More...

EUR/CHF weakens today but stays above 1.1670 minor support. Intraday bias remains neutral first. We're holding on to the view that it's close to topping, if not formed. And even in case of another rise, strong resistance should be seen well below 1.2 handle to bring medium term reversal. On the downside, below 1.1670 minor support will turn bias to the downside for 1.1602 support first. Further break of 1.1602 will indicate reversal and turn outlook bearish for 1.1387 and below.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

Australia’s Construction Sector Growth Slid In December

For the 24 hours to 23:00 GMT, the AUD rose 0.08% against the USD and closed at 0.7870 on Friday.

LME Copper prices declined 1.5% or $105.5/MT to $7097.0/MT. Aluminium prices declined 1.1% or $24.5/MT to $2205.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7849, with the AUD trading 0.27% lower against the USD from Friday's close, after overnight data revealed that Australia's AiG performance of construction index dropped to a level of 52.8 in December. In the prior month, the index had recorded a level of 57.5.

The pair is expected to find support at 0.7831, and a fall through could take it to the next support level of 0.7813. The pair is expected to find its first resistance at 0.7871, and a rise through could take it to the next resistance level of 0.7893.

Going ahead, traders would keep a close watch on Australia's building approvals data for November, slated to release overnight.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Euro-Zone’s Annual Inflation Slowed As Anticipated In December

For the 24 hours to 23:00 GMT, the EUR declined 0.2% against the USD and closed at 1.2047 on Friday, after data indicated that annual inflation in the Euro-zone slowed in December.

The Euro-zone's preliminary consumer price index (CPI) climbed 1.4% on an annual basis in December, meeting market expectations and after recording a rise of 1.5% in the prior month, thus indicating that strong economic conditions in the common currency region have not translated into higher inflation.

Separately, Germany's retail sales rebounded more-than-expected by 2.3% on a monthly basis in November, surging by the most in a year and hinting that an upturn in the nation's private consumption is on the cards. Retail sales had recorded a drop of 1.2% in the previous month, while markets had anticipated for a gain of 1.0%. Additionally, activity in the nation's construction sector expanded at its quickest pace in four months, after it advanced to a level of 53.7 in December, driven by robust growth in commercial building work. The PMI had recorded a reading of 53.1 in the preceding month.

The greenback advanced against a basket of major currencies, as investors shrugged off downbeat US non-farm payrolls report and cherished robust wage growth data.

Non-farm payrolls in the US increased less-than-anticipated by 148.0K in December, against market anticipations for an advance of 190.0K. Non-farm payrolls had recorded a revised increase of 252.0K in the previous month. On the other hand, the nation's average hourly earnings of all employees gained 0.3% on a monthly basis in December, meeting market expectations, thus offering initial signs of a pick-up in wage growth. Average hourly earnings of all employees posted a revised increase of 0.1% in the prior month. Moreover, the nation's unemployment rate remained steady at 4.1% in December, in line with market expectations.

Another set of data revealed that the ISM non-manufacturing PMI in the US unexpectedly eased to a level of 55.9 in December, defying market expectations for a rise to a level of 57.6 and compared to a reading of 57.4 in the prior month. Further, the nation's trade deficit widened to a nearly six-year high level of $50.5 billion in November, as imports of goods jumped to a record high amid strong domestic demand. The nation had posted a revised trade deficit of $48.9 billion in the prior month, while market participants had envisaged for a deficit of $49.9 billion.

Nevertheless, the nation's factory orders climbed 1.3% on a monthly basis in November, surpassing market expectations for an advance of 1.1%. Factory orders had registered a revised rise of 0.4% in the previous month. Also, the nation's final durable goods orders gained 1.3% in November, confirming the preliminary print and following a revised decline of 0.4% in the prior month.

Meanwhile, the Philadelphia Federal Reserve (Fed) President, Patrick Harker pencilled-in only two interest rate increases in 2018, while the San Francisco Fed President, John Williams shared his expectation of three interest rates hikes this year, citing an already strong economy. Further, the Cleveland Fed President, Loretta Mester, stated that she expects roughly four interest rate hikes this year.

In the Asian session, at GMT0400, the pair is trading at 1.2033, with the EUR trading 0.12% lower against the USD from Friday's close.

The pair is expected to find support at 1.2008, and a fall through could take it to the next support level of 1.1984. The pair is expected to find its first resistance at 1.2070, and a rise through could take it to the next resistance level of 1.2108.

Moving ahead, investors would focus on the Euro-zone's retail sales figures for November, the Sentix investor confidence index for January as well as Germany's factory orders data for November, all due to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading A Tad Higher This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.11% against the USD and closed at 1.3566 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.3568, with the GBP trading marginally higher against the USD from Friday’s close.

The pair is expected to find support at 1.3533, and a fall through could take it to the next support level of 1.3497. The pair is expected to find its first resistance at 1.3595, and a rise through could take it to the next resistance level of 1.3621.

Looking ahead, traders would keep a close watch on UK’s Halifax house prices for December, scheduled to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading Marginally Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD rose 0.32% against the JPY and closed at 113.14 on Friday.

In the Asian session, at GMT0400, the pair is trading at 113.18, with the USD trading a tad higher against the JPY from Friday’s close.

The pair is expected to find support at 112.89, and a fall through could take it to the next support level of 112.60. The pair is expected to find its first resistance at 113.39, and a rise through could take it to the next resistance level of 113.60.

On account of a national holiday in Japan today, Yen investors would focus on global macroeconomic events for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading A Tad Higher, Ahead Of Swiss Inflation Report

For the 24 hours to 23:00 GMT, the USD rose 0.08% against the CHF and closed at 0.9754 on Friday.

In the Asian session, at GMT0400, the pair is trading at 0.9752, with the USD trading slightly lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9734, and a fall through could take it to the next support level of 0.9715. The pair is expected to find its first resistance at 0.9778, and a rise through could take it to the next resistance level of 0.9803.

Ahead in the day, all eyes would be on Switzerland’s inflation data for December.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Canada’s Unemployment Rate Plunged To Its Lowest Level Since January 1976 In December

For the 24 hours to 23:00 GMT, the USD declined 0.67% against the CAD and closed at 1.2407 on Friday.

The Canadian Dollar gained ground against the USD, after stronger-than-expected data on Canada's labour market boosted odds for a January interest rate hike.

Data revealed that Canada's unemployment rate unexpectedly fell to a four-decade low of 5.7% in December, on the back of a surge in job creation, thus highlighting a rapidly diminishing slack in the nation's labour market. In the prior month, the unemployment rate had recorded a level of 5.9%, while market participants had envisaged for a rise to a level of 6.0%.

Other data showed that Canada's seasonally adjusted Ivey–PMI fell to a level of 60.4, compared to a reading of 63.0 in the previous month. Moreover, the nation's international merchandise trade deficit surprisingly expanded to C$2.54 billion in November, after recording a revised deficit of C$1.55 billion in the prior month and confounding market expectations for the nation's trade deficit to narrow to C$1.13 billion.

In the Asian session, at GMT0400, the pair is trading at 1.2397, with the USD trading 0.08% lower against the CAD from Friday's close.

The pair is expected to find support at 1.2331, and a fall through could take it to the next support level of 1.2265. The pair is expected to find its first resistance at 1.2488, and a rise through could take it to the next resistance level of 1.2579.

Going forward, the Bank of Canada's (BoC) business outlook survey report, scheduled to release later in the day, would be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

German Manufacturing Orders For November Are Due Out

Market movers today

NEW RESEARCH WEBSITE: We have launched a new research website, with all our research across asset classes and countries.

We are heading for a quiet er week in terms of data where inflation takes centre stage after activity numbers were in the spot light last week. On Wednesday, inflation is due out from China, Denmark and Norway followed by inflation releases for the US and Sweden on Friday.

Focus this week will also turn to the scheduled meeting between North and South Korea tomorrow to see if the apparent easing of tensions can be sustained and if it can pave the way for talks between the US and North Korea. There are doubts, though, as to whether North Korea are serious about the talks.

Make-or-break talks on forming a German government between CDU/CSU and SPD began on Sunday and continue this week. If the exploratory talks find enough common ground, the SPD leaders will ask for a party convention on 21 January to back full-fledged negotiations.

This morning, German manufacturing orders for November are due out , which are estimate by consensus to be flat m/m after a 0.5% m/m increase in October . The monthly changes are very volatile but the underlying trend is robust and supports the picture of strong manufacturing activity.

Todays' batch of confidence numbers from the EU Commission is expected to show a similarly strong development . Euro area retail sales should have rebounded in November after a fairly big drop in October.

Finally, we look for a 0.5% rise in Norwegian industrial production for December, taking the annual increase to 2.5% y/y – the highest level since March 2015.

Selected market news

Market sentiment continues to be strong with further decent increases in stock markets on Friday. The Japanese market is closed today but other Asian markets continued the positive trend this morning. The US labour market report on Friday was on the soft side, suggesting that the Fed will continue to move slowly this year. On inflation, stock markets are seeing the best of all worlds at the moment with robust increases in producer prices feeding into profits, but with limited pass-through to consumer price inflation, which could make the Fed step on the breaks.

Former White House st rategist Steve Bannon yesterday issued an apology over his comments in the book ‘Fire and Fury: Inside the White House' published on Friday, see Reuters.

Over the weekend, China FX reserves for December showed a bigger increase than expected. Reserves rose by USD20bn to USD3,139.9bn – the 11th increase in a row. USD/CNY is again trading close to the September lows below 6.5 after CNY has st rengthened over the past three weeks in parallel with the general USD weakness over the same period.